I've switched my gas exposure from $PEY.TO to $AAV.TO

Reason? Valuation.

$AAV.TO offers a much higher yield. Heavy Buybacks coming. Insiders buying.

AAV: https://t.co/MwK3vYzh0K

PEY: https://t.co/5IS477s7V8

- Even if one is bullish on oil, investing is never a single-oucome bet; that would be gambling.

- If oil prices crash, gas revenue can help.

And shitty AECO gas will soon be sold for HH and TTF. Long $WCP $WCP.TO

https://t.co/xQxlb26z3E

$WCP is a jack of all trades and a master of none. If you are actually bullish on oil, why would you want all that shitty AECO exposure at $1.5CAD when you could simply buy $SU and actually get pure oil leverage instead.

$WCP.TO is much more profitable than its presented 2026 FCF would suggest. My full model in the article below. Adjusting for hedges, gas price, new TTF, HH contracts, and more.

https://t.co/xQxlb26z3E

Production up ~10% YoY May.

Liquids prod up ~18% YoY May.

Capex down ~30% YoY April.

Shaping up to be another really nice quarter for debt paydown, despite summer gas and divy bump 😉.

No close 2nd for Canada dry gas 🍻.

$PEY $PEY.TO #COM#OOTT

https://t.co/lcL1puNkAJ

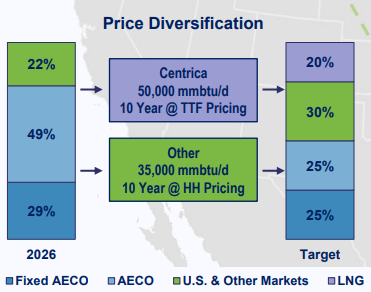

If you wonder what $PEY.TO receives for this contract, it is "TTF price minus associated deductions". From $ARX.TO disclosures, we know the deductions for JKM contract are ~5-6 USD. TTF is closer, so it could be the 5USD.

"TTF - AECO - USD5 = Received netback"

$PEY Peyto Exploration

Implied Price Benefit / Spread TTF premium over AECO:

Roughly US$13.5–14.5/MMBtu (or ~10x higher on a per-unit basis right now).

For Peyto’s 50,000 MMBtu/d volume in 2029:

This translates to a potential daily revenue uplift of ~US$675,000– $725,000 (before any fixed differential, transport, FX, or other adjustments) compared to pure AECO spot sales.

This is an extremely wide spread by historical standards, driven by ongoing European market tightness relative to oversupplied Alberta.

Peyto benefits significantly from TTF indexation in the current environment.

* Full disclosure, I do own some Peyto.

WOW.

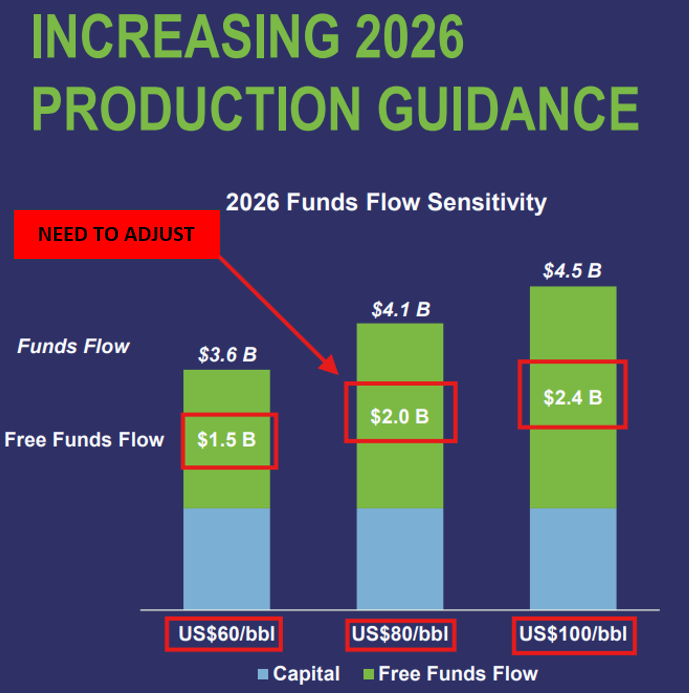

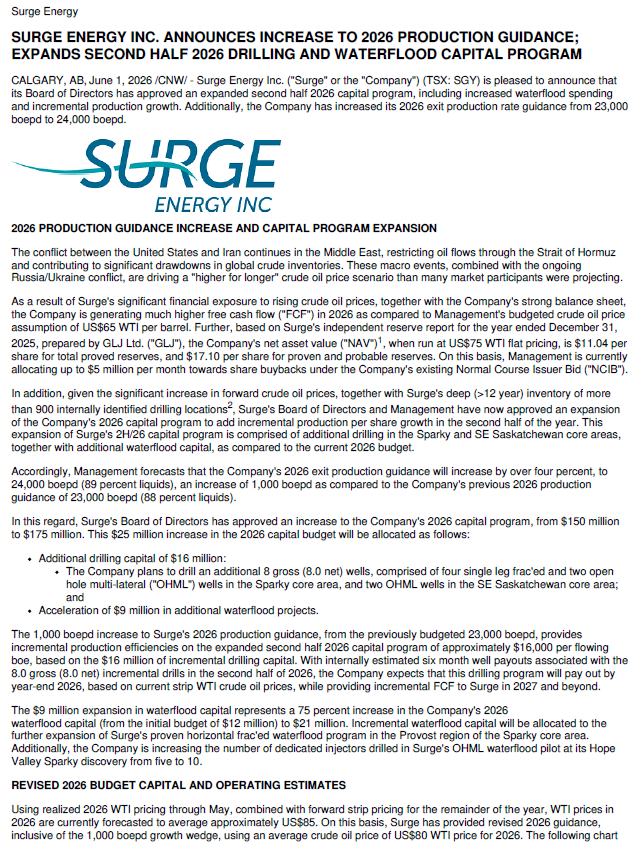

$SGY.TO SURGE ENERGY WITH A PRESS RELEASE ISSUED DURING MARKET HOURS TO NOTIFY THE INVESTMENT COMMUNITY OF A SIGNIFICANT INCREASE IN CAPITAL SPENDING FOR 2026.

GOT @NuggetCapital ETF EXPOSURE? GOT OFS?

@Naveen39778@BubleQe Canada Westcoast is closer to Japan and Korea, but the Landed Costs is nearly the same. The main difference is Henry Hub feedgas is usually much more expensive (>+1$/mmbtu) compared to Canadian gas.

@EnergyInvest0r Yeah. I like the strategy and still hold most of my shares. I liked the shares better a year ago, though.

Their hedges now are great. Looking at it longer-term, I believe it will be close to a zero-sum game and not a cash machine as it has been over the past 25 years.

@Private35271288 If it works out as planned, the share price should rise beyond $20 the closer we are to the spin-off. Decent ROI in 2 years. There is a lot of upside if VMO2 improves etc. I will get much more detailed in the article.

@Private35271288 The RemainCo will have Liberty Growth that will need to be partially sold down to replenish some cash; VM is worth nothing. 50% of VMO2 is valuable, but with declining revenue for now, not attractive. 3/4