Sure - a Tax & STT reduction will help, but where are the blue sky capital market reforms? We need policy mavericks out there willing to advocate for bold reform for the benefit of the whole market. Can't you be one of them @Nithin0dha

A few of my personal ideas for whatever little it is worth:

1) Liberalised and streamlined regime for foreign retail investors? I'd love to invest, but no thanks to going through the lengthy FPI registration process to make retail size investments. Nothing would boost volumes or goodwill more than this.

2) Allow FPI/MF to intraday trade to promote cash market liquidity. Make cash great again. Why can you trade F&O intraday but not cash as an FPI, for example?

3) Create stock lending pools at FPI/ODI issuers, by allowing OTC stock borrowing/synthetic access. (Complex topic, DM me)

4) Allow gross custodian funding for FPIs and even broker funding for well capitalized intermediaries (...no, not just for failed DVP trades) in order to create capital efficiency for investors.

5) Create an after hours cash market to help overseas/domestics to manage overnight risk and spur round the clock trading? (To the 8-4pm brokers: a couple of hours a week on rotation will be good for you :))

6) Futures - given the focus on the linear market, why not allow futures on every BSE 500 stock or more? (Look at the US, nearly every company has listed options)

7) Local Funds- I have friends running PMS/AIFs. The cost is attractive versus other jurisdictions, but they feel suffocated by the bureaucracy. So much to learn from some of the overseas fund jurisdictions, where private funds can be setup with minimal compliance burden and tax efficiency.

8) Allow unsponsored ADRs/GDRs (perhaps in a trusted jurisdiction, FTA countries?). This would helps create visibility for Indian companies and a wider audience. Full fungibility on all ADRs/GDRs would also help some current companies.

I'll add more as I think of them.

Frankly, fund managers, brokers, should take a lot more interest in these market reform topics: your livelihood depends on it...It seems like people are afraid to put their head about the parapet though.

Asked someone from the industry whether foreign investors are still interested in allocating to India. The TLDR:

Interest has pretty much died out. India is seen as geopolitically exposed, especially to an oil shock. There are no real AI plays. Valuations are rich. And the rupee situation doesn't help.

On top of that, investors who were sitting on gains have taken money off the table and are now looking at markets like Japan, Taiwan, Korea, Europe etc instead.

He also pointed out that our LTCG/STCG structure and the increase in STT have made India less attractive compared to other markets that are seeing inflows.

If we need to attract FPIs back, and we do, fixing this feels like pretty low-hanging fruit.

I wrote this:

https://t.co/912OJb3v5Y

A few things that come to mind that should be explored:

- Access for foreign retailers through a streamlined route (like in other markets with simple KYC on brokerages)

- Synthetic SLB Access (more nuanced point, not many have thought about)

- Allowing institutions and funds to trade intra-day in cash (not just retail/prop, other markets have precedent)

- Custodial funding of institutional trades

- After hours cash market (allowing better hedging always been a goal)?

- Continuous block-window (could also be leveraged by tech savvy block crossing networks like Liquidnet, ITG Posit Alert, also a way to improve comm reduction if local mutual access it)

- Great proliferation of futures contracts on new underlying (promoting the linear market, also in tandem helps cash volume and market breadth)

Many more I'm sure!

From a policy perspective, the Jane Street saga in India brings many questions to the fore about market development.

Participants in India have moved into convex (read options) products at the expense of a deeper and more liquid cash market

The reason Jane’s Street strategy was ostensibly so effective is due to the discrepancy between cash market and options volume. In essence, the alleged manipulation is facilitated by the volume mismatch between the two markets.

You may ask, why is that the case?

1) In 2018, SEBI mandated physical settlement in futures. Remember futures are linear in pay-off without the convexity of options. Previously futures were trading multiples of the cash market. Most retailers have long been familiar with the simplicity of the pay-off here (re: the old badla system)

2) As SEBI acknowledges, intra-day cash trading is not allowed by foreign institutions. In other markets, there are many family offices, prop shops and hedge funds that trade intra-day with non HFT strategies. They can bridge (arbitrage) inefficiency.

3) The SLB (Securities Lending & Borrowing) market is not deep, and there are several hurdles to creating a deep borrow pool. This would add to the counterbalance to deliberate stock market ramps in the cash market.

4) Intra-day cash leverage was significantly curtailed after SEBI’s 2019 circular, which limited intra-day leverage in cash markets on transactions. This again is a deterrent to such manipulation discussed.

5) In 2020, SEBI reduced margin requirements on options spreads. This was not a bad thing per se, but crimping cash volume in favour of options seems an interesting policy choice.

Of course, High Frequency Trading (HFT) manipulation is a problem and enforcement action should proceed whether it goes, but this saga should also be a wake-up call for promoting, both in absolute and relative terms, a deeper and more diverse cash market.

This is very welcome news to hear publicly. Devil is always in the detail of course, but there are many low hanging, blue sky reforms out there (have detailed many publicly which have been picked up elsewhere). If different stakeholders are invited to the table to discuss and there's a genuine willingness, cash market volumes could increase significantly on the back of them.

I mean you can. I remember Eurex (index / single stock options) also did this a long time, where they allowed certain participants to go direct into the market.

But, there are many considerations, and you have to be careful not just to dump implicit trading / impact costs on underlying investors:

1) Sell side firms (particularly global banks) have invested millions in algo technology. What are local mutual funds going to use now? Likely creates more impact cost or you stack a load of upfront capex/time on investors (to build a product that likely won't be better).

Just to give you an example, some of the best algorithms that are used to trade Indian markets have a major performance benefit, reducing cost for investors. These include UBS "Swoop", Jefferies "Seek", Macquarie "Neo" to name a few. Just to give you a bit of context, there are local providers of algos (I won't name) that most locals use which see materially worse performance.

2) Most local mutual funds often need to transact size and significant %s or multiples of daily volume, whether that its in large caps or small caps. This means their orders simply cannot be put down a pipe into the exchange in a standardized fashion. That's a horrible idea. A fund trying to do that would simply heap a load of implicit costs on investors.

3) "Value Add" - if they do all their business direct into the exchange, where are all these traders/PMs at mutual funds going to get updates from the sell-side on stock moves, rotation, factor moves, market colour, trade timing, algo selection or impactful sales/trading commentary :))

I get it you might say well they might "pay fees from TER" in the new state of the world, but no chance this is going to happen with such a diktat from the top.

Just to be clear, I'm in no way suggesting that the sell side (brokers/banks) is a paragon of virtue or value add (anywhere in the world, not just India). Quite the opposite, it's filled with some bad actors and there can be perverse incentives that are harmful to the market.

But there are sales traders and brokers in the market who do an incredible job, save massive costs for funds and add to the investment process. In my eyes, it's wrong that shouldn't be rewarded significantly (i.e. much more than close to breakeven: 2bps)

2bps cap on commissions, is it “anti-local”?

I was asked by a few about SEBI’s proposal to cap local mutual fund cash equity trading commissions at 2bps in India (barely above the cost of execution in the market and almost half that of rack commission rates in Europe). Here are my thoughts:

At a high level, there’s a lot of clapping and applauding that this is a move good for investors in mutual funds - it isn’t.

There is still value that the “sell side” (brokerages), including sales and sales traders *can* bring. Sure, there are many awful brokers that add precisely zero value, or maybe even negative value in some cases (refer front running cases and leakage discussion).

Yet there are sales people and sales traders out there who add value: finding difficult liquidity with minimal impact (sometimes even reducing market impact by 5-10%), better execution, excellent market colour and analysis, algo selection, and trade timing, to name a few. I can say this with confidence after having dealt with nearly the entire breadth of the institutional sell side in India.

Let me give you one clear example of why a local fund paying 2bps or less will probably end up costing investors a lot more and be counterproductive:

Let's say you are an investment bank (broker) working on a large investor sell-down, looking for buyers. This could be 5, 10, 20, even 100x daily trading volume in the stock.

Are those sales traders/salespeople at an investment bank really going to give the first call / preference to [Insert Local Mutual Fund] versus a host of other local and foreign clients paying between 5 to 15bps for execution (maybe even 7-8 times more)? It's just basic commercial sense.

In this proposed state of the world, local mutual funds become the "last call", or maybe brokerages simple just say send your flow down the DMA pipe, you'll get zero high touch coverage (including block liquidity) and zero value-add from our trading/sales desks.

Bizarrely, this is probably a great thing for foreign investors (hedge funds and long onlys etc). Offshore investors are going to see all the best liquidity from the sell side, get the best allocations in secondary market block deals, be first to hear interesting market colour and analysis etc.

The impact on brokerages and research is going to be significant (we have a historical precedent in Europe after MIFID). I would be surprised if local mutual funds compensate an 80% cut in the commission cap with spend on research.

Ultimately, “you get what you pay for”.

Why would they care? They're losing business that's barely profitable, and you have a much greater pie that's paying higher commission. It's a simple business question and one of focus.

"Allowing MFs to buy directly." For some trades that could be effective, but it's not going to solve for large liquidity situations on a block/by appointment basis. It's not going to solve for the millions of dollars that banks/brokerages have invested in algo technology, which MFs do not have but currently benefit from and it's not going to solve for having an expert sales trader whose job it is to provide market colour & trade analysis.

All of these things at the end the day can reduce costs for mutual fund investors beyond commissions paid. I say this having seen both sides of the market (buyside/sellside).

I'm not sure you're understanding the commercial reality or how most investment banks/brokerages work. Commissions under the proposal are going from 12bps at top end to 2bps. That's more than an 80% cut and is barely above cost. There is a larger universe beyond local mutual funds (in AUC terms) in the market paying 5-15bps, on a relative basis, why wouldn't they prioritise and focus on that?

Disagree. I would say the reality is probably the opposite. Many brokerages, particularly global banks who were previously very focused on overseas investors, aggressively pivoted to prioritise local mutual fund business, given their huge increase in AUM over the last decade and the decent trading comms available.

Because why would they? Most institutional investors (FPIs included) likely understand that its a fool games to simply drive comms down to cost. There is value in some (not all) sell side coverage on high touch sales and trading that justifies paying let's say between 5bps and 15bps where it is now (i.e. where the market has determined it currently).

On the occasion of Diwali, I wanted to share my firm (Augurium) has made a small investment in micro-cap CakeBox (CBOX LN, £89 Million market cap) – the eggless and vegan cake franchiser in the UK after a long time tracking it. Here's my thesis:

-The biz has averaged 10% underlying/adjusted EPS growth, 20% revenue growth over the last 5 years.

-In March 205, CBOX acquired one of the most well-known mithai (South-Asian sweet) retailers in the UK called Ambala. This could add another £15-20m to revenue next year, £2-3m EBIT in my eyes.

- The company seems to have stabilized/cleaned up from previous internal control/accounting issues in 2022 (new CFO, accounting review & restatements). Definitely worth monitoring and a risk factor.

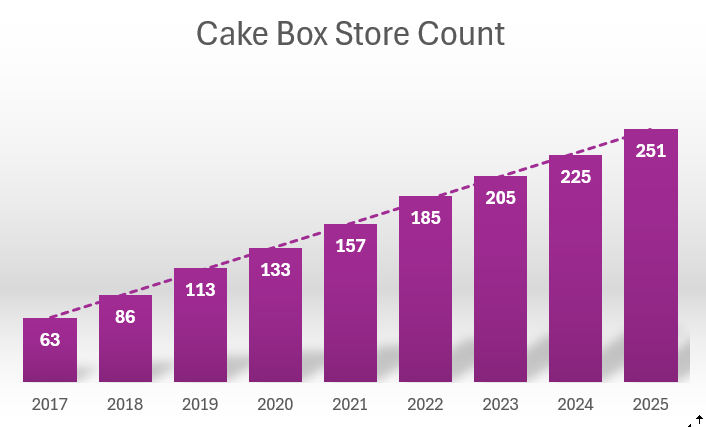

- CBOX has grown stores consistently, from 133 in 2020 to 251 in 2025, with a medium term target of 400 stores

- Personally I’m looking out for: 1) New franchises (does Ambala have international potential like CBOX?) 2) Commentary on the Ambala/Cake Box fusion products (Gulab Jamun Cupcakes anyone?) 3) Scale-up of home delivery (they don’t break this out anymore and its included in online sales, but it still looks to be early innings with the delivery aggregators)

- At 20x FY26 estimated earnings, the stock would trade at 286p, implying ~60% upside from current levels

Happy Diwali to all!

@deepakshenoy When you say “good” I assume you speak from the vantage point of short term fund performance rather than a market development perspective.

Was yesterday's fact finger block trade and subsequent volatility avoidable...?

Fat finger trades like the Clean Science & Technology trade in India, can happen and do happen across all markets but there is nuance here around blocks...

In India, large discounted block transactions like yesterday's error have to be transacted "live" on the market.

Apart from the fact that this gives other market participants the opportunity (and incentive) to interfere in the order book, the process is always going to be chaotic and fraught with risk as the broker is trying to execute while prices are moving and sending orders directly to the exchange. I have seen the risks because I have had to do it.

In my mind, it's absurd that 24% of the company has to be executed through a live order book.

Like the CLEAN block yesterday, this can not be done in the current block window:

- The block was priced more than 1% discount (currently the limit for India's block window)

- The two block window sessions last for 15 minutes and don't cover the whole trading day. Arranging blocks is a dynamic process. This was done after the open.

It would be better to allow participants to trade blocks away from the order book in India without the current restrictions, like nearly every single other major market.

Nice to see my earlier tweet mentioned in a Bloomberg article on the Jane Street order by @matt_levine

From a market development perspective, there are many blue-sky reforms that can transform cash equity volumes in India and restore much needed balance between cash and options.

https://t.co/NtJrkj1kdN

Agree on the enforcement part and yes there's plenty to find out there in the market... Let's not forget though the JS strategies under question would be infinitely more difficult if cash market liquidity was a policy priority (not options and convexity) and relative volume between the two markets wasn't what it is now. I appreciate it's pretty hard for you to agree on this in public as a regulated entity, but I think there is a bigger policy and market development question here too that needs to be addressed.

From a policy perspective, the Jane Street saga in India brings many questions to the fore about market development.

Participants in India have moved into convex (read options) products at the expense of a deeper and more liquid cash market

The reason Jane’s Street strategy was ostensibly so effective is due to the discrepancy between cash market and options volume. In essence, the alleged manipulation is facilitated by the volume mismatch between the two markets.

You may ask, why is that the case?

1) In 2018, SEBI mandated physical settlement in futures. Remember futures are linear in pay-off without the convexity of options. Previously futures were trading multiples of the cash market. Most retailers have long been familiar with the simplicity of the pay-off here (re: the old badla system)

2) As SEBI acknowledges, intra-day cash trading is not allowed by foreign institutions. In other markets, there are many family offices, prop shops and hedge funds that trade intra-day with non HFT strategies. They can bridge (arbitrage) inefficiency.

3) The SLB (Securities Lending & Borrowing) market is not deep, and there are several hurdles to creating a deep borrow pool. This would add to the counterbalance to deliberate stock market ramps in the cash market.

4) Intra-day cash leverage was significantly curtailed after SEBI’s 2019 circular, which limited intra-day leverage in cash markets on transactions. This again is a deterrent to such manipulation discussed.

5) In 2020, SEBI reduced margin requirements on options spreads. This was not a bad thing per se, but crimping cash volume in favour of options seems an interesting policy choice.

Of course, High Frequency Trading (HFT) manipulation is a problem and enforcement action should proceed whether it goes, but this saga should also be a wake-up call for promoting, both in absolute and relative terms, a deeper and more diverse cash market.

Don’t bankers have the right to push for better allocations for clients that have historically paid and they have a good commercial relationship with?

For example if a Mutual Fund historically trades once a year down the pipes, pays almost zero commission and gives gali to a broker who has an exclusive IPO, why would that broker allocate in the anchor to you? Is that wrong?