#Biotech Investor | Recovering Scientist | May have L/S position in names mentioned | Opinions are strictly my own and not intended as investment advice

Amazing to see translational science is moving at a much faster pace in #biotech these days from bench to bedside!

#CRISPR 11yrs

2012 Doudna/Charpentier paper

2020 Nobel

2023 First FDA approval $CRSP

#RNAi 20yrs

1998 Fire/Mello paper

2006 Nobel

2018 First FDA approval $ALNY

End of an era!

As a long-time follower of global #biotech/healthcare, I have learned a lot from the many good analysts at @CreditSuisse esp for their ex-US coverage, which was often more critical than typical US sell-side coverage. Best wishes to everyone on their new endeavor!

$SRPT ELEVIDYS priced at $3.2M

This is probably the biggest problem w/ accelerated approvals for the healthcare system.

How does it make sense that a drug under AA w/ unproven benefits priced 50% higher than $NVS Zolgensma at $2.1M w/ full approval and established efficacy?

"The exception is more interesting than the rule."

#Biotech reverse merger occasionally turn into >$1B buyout

Aduro➡️ $KDNY ➡️$3.2B $NVS

shell➡️Medivation➡️$14B $PFE

Trimeris➡️Synageva➡️$8.4B ALXN

CancerVax➡️Micromet➡️$1.2B $AMGN

Biodel➡️Albireo➡️$1B Ipsen

shell➡️Cougar➡️$1B JNJ

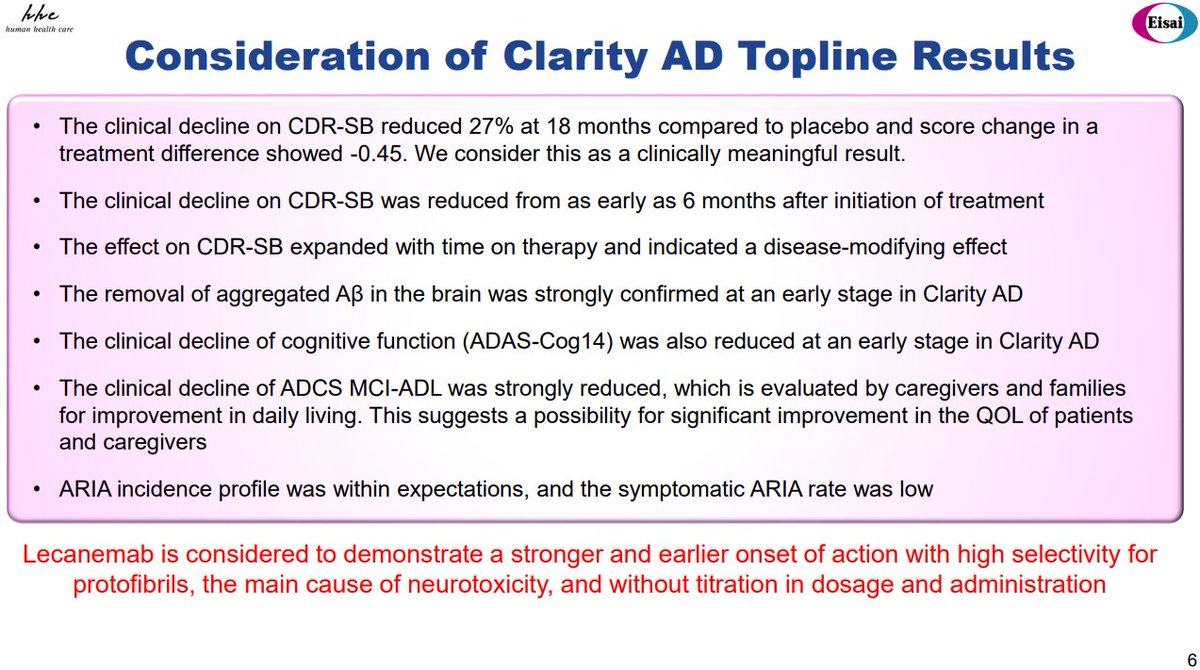

As expected, FDA AdCom on $BIIB/Eisai lecanemab is setting up to be a "clearing the air" event after the whole Aduhelm saga.

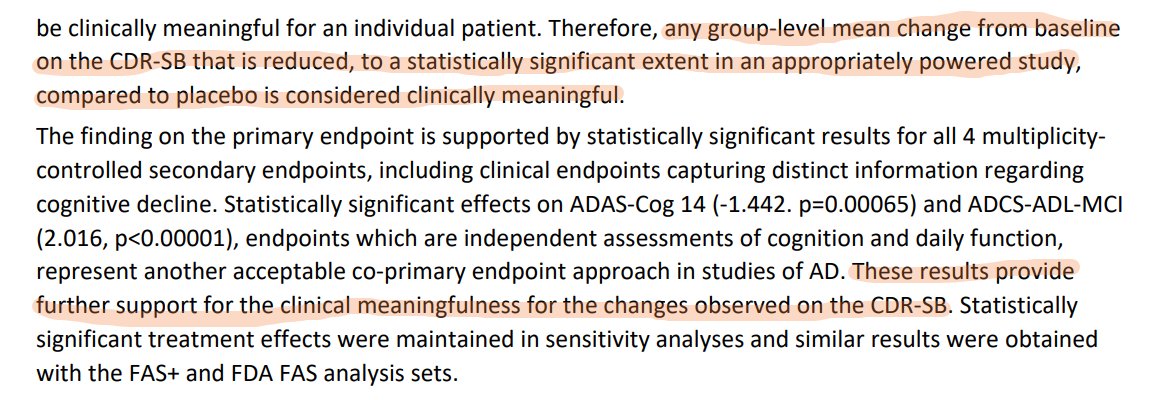

More importantly, FDA reviewer made it very clear the changes observed on the CDR-SB is considered "clinically meaningful".

$BIIB My thought on lecanemab "clinical meaningfulness" debate:

18-mo rx slowed disease progression by 6~8mo.

Is it not meaningful to pts and families to have 6~8 more months of your memory and freedom?

An oncology drug w/ 6~8mo of PFS benefit would be heralded as breakthrough!

Making it even harder for $KDNY atrasentan to get FDA approval is a competing drug, sparsentan, has exclusive orphan drug approval. Atrasentan would have to show it is more efficacious and/or safer. Comparing trial data, atrasentan seems to be inferior https://t.co/j2TYNV7ZGz

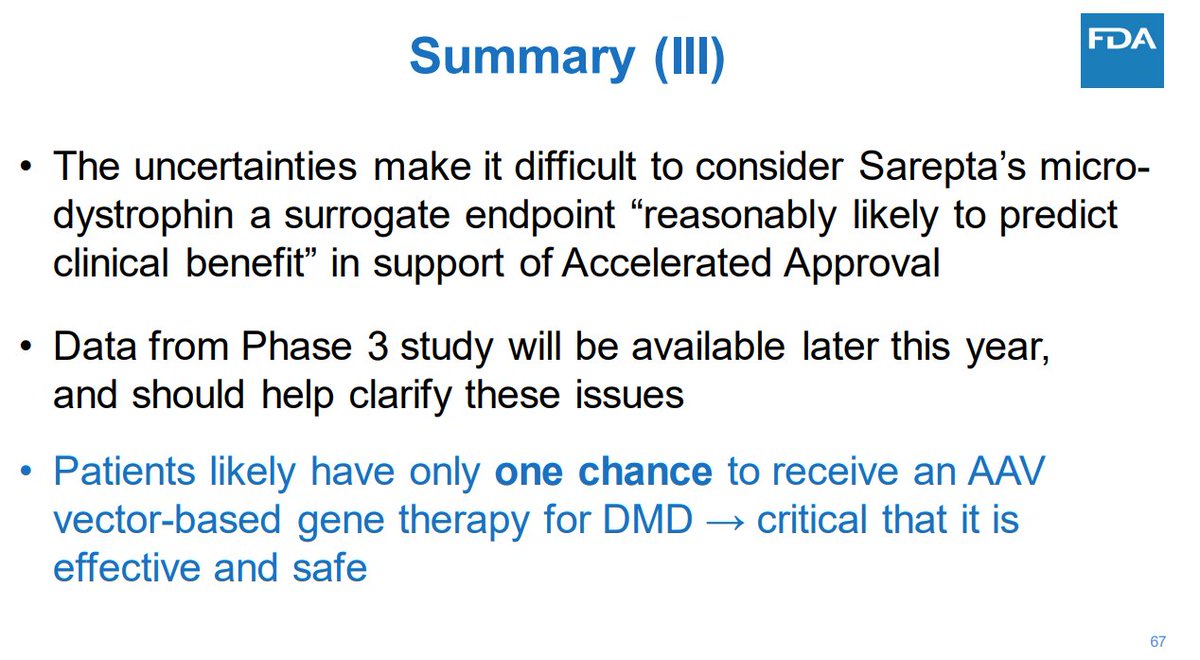

$SRPT FDA summary slides today emphasizes the key point that "Patients likely have only one chance to receive an AAV vector-based gene therapy for DMD", which could drive the panel discussion today to wait for Ph3 data that will be available later this year.

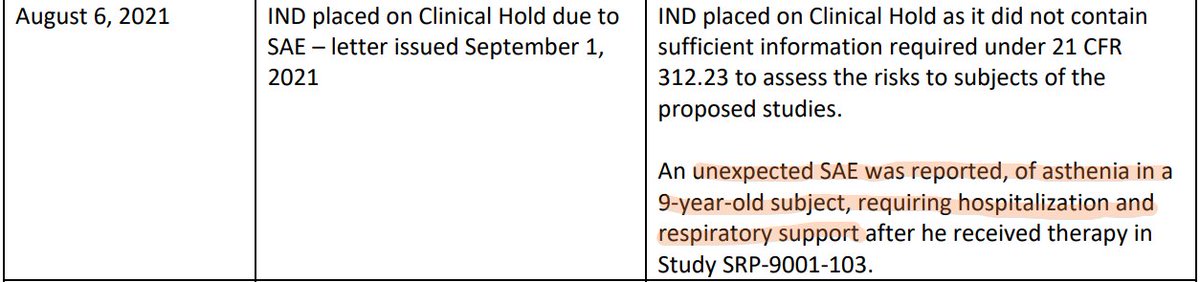

$SRPT Apparently FDA placed SRP-9001 on clinical hold in Aug 2021 due to an unexpected SAE of asthenia requiring hospitalization and respiratory support, but the company never disclosed it to investors AFAIK.

Did it not count as a material event for most important pipeline drug?

Overall great news for #Alzheimer pts! Another unequivocally positive Ph3 should further validate Aβ MoA, bolster doctor confidence and derisk CMS reimbursement.

$LLY comment to STAT about curve widening over time provides further evidence for the promise of "disease modifying"

A new addition to #Biotech best turnaround M&A

$ISEE $1➡️40X $ALPMY BO in 4y

$FPRX $2➡️20X $AMGN BO in 1y

$IMMU $2➡️40X $GILD BO in 4y

$ARQL $1➡️20X $MRK BO in 2y

$ARRY $2➡️20X $PFE BO in 3y

$ECYT $1➡️20X $NVS BO in 1y

$MDVN $2➡️40X $PFE BO in 6y

$PCYC <$1➡️200X $ABBV BO in 6y

Two big FDA Adcom mtg dates just released on FDA agenda

May 12 -- $SRPT DMD gene therapy

https://t.co/iVVwoUCsrn

June 9 -- $BIIB/Eisai lecanemab

https://t.co/ITRSinWRf0

$SNY continues its quest as biotech shorties' worst enemy

$3.3B $PRVB at 273% premium ahead of first earning after launch

$2.5B $THOR at 172% premium before PoC -> IL2 discontinued + $1.7B impairment

$3.7B $PRNB -> clinical hold due to DILI

$3.2B $TBIO -> COVID19 discontinued

$BIIB/Eisai lecanemab KO $LLY Donanemab in Round 1 of #Alzheimer's new drug fight

FDA Issues Complete Response Letter for Accelerated Approval of Donanemab due to limited number of patients with 12-month drug exposure

$HZNP Cheers for an early Christmas gift!

$145M River Vision acq turned out to be one of the best deals in biotech history:

Pharmacyclics -> Celera for ibrutinib

Vertex -> $538M Aurora for CF franchise

Gilead -> $470M Triangle for HIV franchise

JAZZ -> $122M Orphan Med for Xyrem

$BIIB My thought on lecanemab "clinical meaningfulness" debate:

18-mo rx slowed disease progression by 6~8mo.

Is it not meaningful to pts and families to have 6~8 more months of your memory and freedom?

An oncology drug w/ 6~8mo of PFS benefit would be heralded as breakthrough!

$BIIB/Eisai - money slide for Lecanemab at #CTAD22

https://t.co/ZU1jjCYhyE

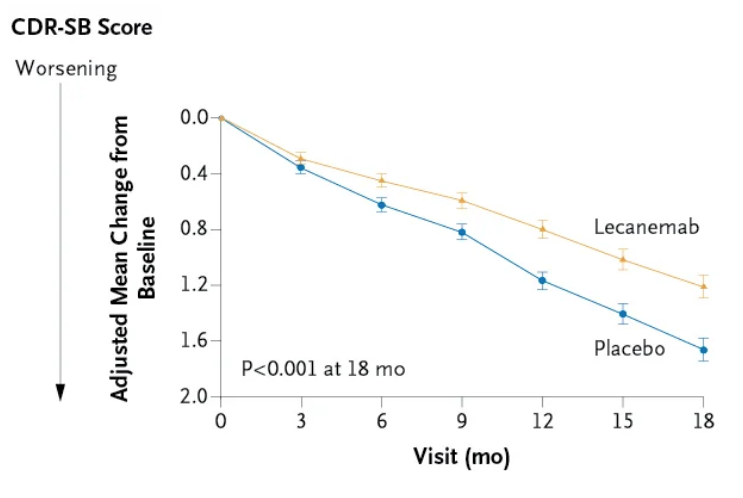

The biggest promise of "disease modifying" (vs. symptomatic) treatments is probably the compounding effect over time.

The widening of curve separation out to 18mo provides an early hint for that promise.

While some debate on clinical meaningfulness, we have to start somewhere for a tough disease like #Alzheimer's and this is a solid first step!

The biggest Q into #CTAD22 is probably whether benefit seen in both ApoE4 carriers and non-carriers given trial enriched w/ 70% carrier.

Great day for #Alzheimer's patients with first unequivocally positive Ph3 for a disease modifying treatment!

Kudos to @EisaiUS for trial execution, believe one big factor for success is how they managed to get dropout rate to only 15% amid COVID19 pandemic (vs >20% historically)

Great day for #Alzheimer's patients with first unequivocally positive Ph3 for a disease modifying treatment!

Kudos to @EisaiUS for trial execution, believe one big factor for success is how they managed to get dropout rate to only 15% amid COVID19 pandemic (vs >20% historically)

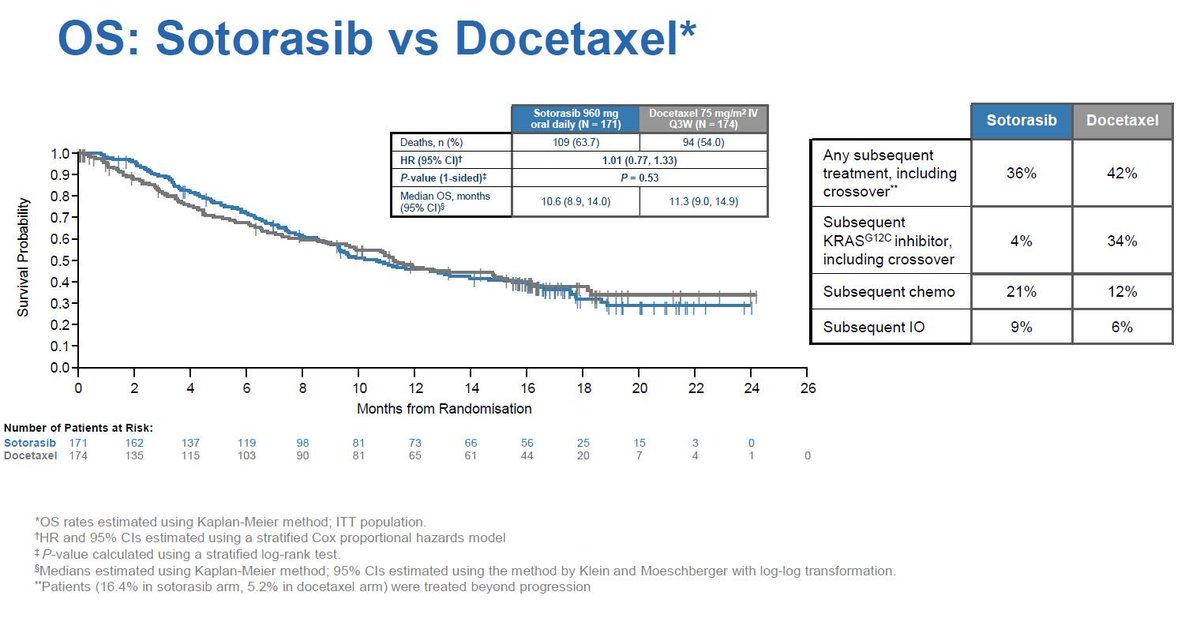

#ESMO22 $AMGN Lumakras very underwhelming Codebreak-200 data on top of an already slow launch

How to justify $18K/mo price w/ ~1mo mPFS benefit and detrimental overall survival?

Double whammy day w/ $BMY Sotyktu clean label re. Otezla.

Silver lining: more need for SMID bio M&A?