Eventhough Fredun Pharma has various pharma related business in its fold,brand 'Freossi' is expected to be a game changer for the company.Growing love for pets in India is only likely to increase. Trading @ Rs.780. Stock is out of flavour,perhaps the best reason to accumulate.

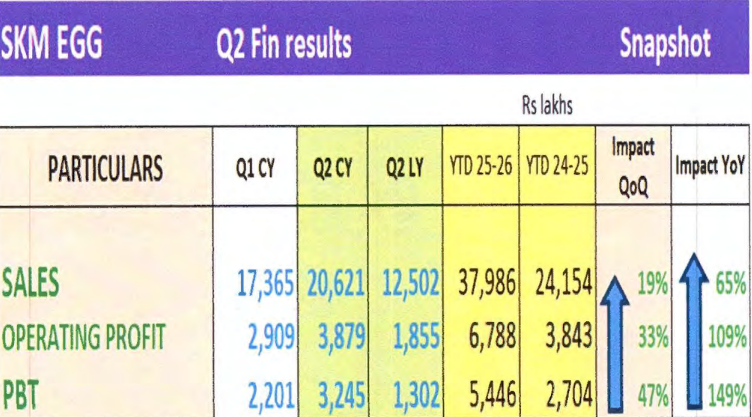

Another set of exciting results from Skm Eggs .Company is on a growth trajectory with increase in exports and currency favouring it. Split announced to FV of 5. Re-rating is bound to happen.

Huge promter buying in last few months plus solid results is a rare combination to watch out. Increased Exports and stable currency is a boon and it seems a re-rating is on the way.

The next multibagger rarely comes with flashing neon signs or front-page headlines. It’s usually hiding in plain sight—quiet, overlooked, even ridiculed. The crowd doesn’t see it, the analysts don’t model it, and most investors dismiss it outright. That’s precisely why it has room to surprise.

Great winners are almost always born misunderstood. In the early days, the narrative is confusion, doubt, and disbelief. The market sees “risk,” while the few who dig deeper see “optionality.” And as the business executes step by step—building moats, scaling operations, defying skeptics—the price begins its quiet march.

Then one fine day, the switch flips. The world “discovers” it. Media calls it visionary, institutions pile in, and the same voices that once mocked it now call it a “wonderful business.” But by then, the outsized gains have already been harvested by those who believed before the spotlight arrived.

The essence of superior investing lies in this gap—between perception and reality, between doubt and conviction. The crowd waits for validation; the true investor moves before it.

So remember: the next big winner won’t look obvious. It will look questionable, messy, maybe even boring. And that’s the very disguise that hides greatness until it’s too late.

The recent issues associated with NH66 works in kerala is attributable to design flaw and construction of viaduct will set back KNR by atleast 100 crores.

As you drive through Ramanattukara to Kappirikkad in Kerala which is a part of ongoing 6 lane NH66, the quality and professionalism in construction is a marvelous treat to watch. This project is done by KNR constructions which is making a name for itself in major works.

Majority of the companies discussed here had posted average to flat results this quarter.Salzer stands out as an exception with profits doubling from previous quarter.A wondeful company to keep it for a long term compounding.

With sales close to 1000 crores and a market cap of 600 crores, this Coimbatore based company is on a growth trajectory. Trading at Rs. 368. Notes will follow after a visit to the factory.

Great feeling to be followed by none other than Arun Mukherjee,my guru in small cap treasure hunts.Visiting companies is a norm that i learned from him.Grateful to you @Arunstockguru .

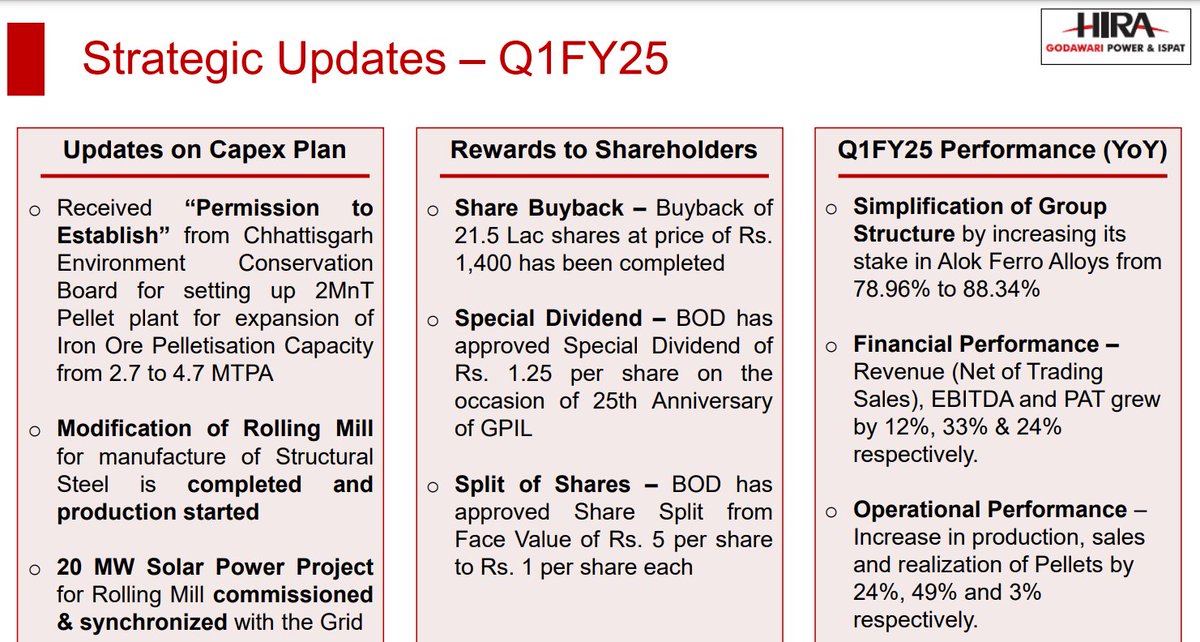

A perfect example of good capital allocation with cost savings from solar power project,forward integration,buybacks,special dividend and various expansion projects.A company for good long term relation.

A steady compounder. A company with deposits from employees and advances from students and patients amounting to Rs.60 crores. Customers from all walks of life.Medical education is a new advantage .Would contine to grow well.Kovai medical KMCH) trading at Rs.4184

@MukeshJ62353123 Dilution of equity would be there,but would have negligible effect on share price as it is priced at 14% of current price. Company had announced this price long back and stood for existing investors even after a run up in share price. Company is well placed for good growth.

Rights issue by Jaykay Enterprises @ Rs.25 is an offer too good to resist as existing price is Rs.120. Business is progressing well as expected with lot many MOUs and foray into defence manufacturing.

Buyback by GPIL is proposed at a price of Rs.1400. I feel investors should not tender their shares at this price as the share price likely to appreciate much more in next one year. It is an amazing company worth hoding for long term.

Annual Results: with an yearly EPS of Rs.75,GPIL is tarding at 12 PE which is very cheap compared to its valuations. As expected,value added products are contributing to the profits.Amazing company to stay invested for next 5-10 years.

I have a strong feeling that GPIL will turn out to be a great investment even at this level.Rarely we get all things right in any company.Recent appoinment of renowned independant directors adds to this conviction.Lets wait and watch.

Very soon majority of profits for GPIL will come from specialized steel and this company will no longer be normal commodity player. Profits can surge with increased capacity, new steel plant, and increasing iron and steel prices. A major re-rating is on the way.