Back in markets, global macro. Author of "The Paradox of Risk". Former Senior Fellow @piie & economist @IMFnews. Views my own. Soccer player & coach, A license.

Hoy sale ‘Las invasiones bárbaras’, un viaje por las crisis del siglo. Del 11-S a Irán, de las milongas de Aznar a los líos de ZP, Rajoy y Sánchez, de la UE al trumpismo. Un libro pesimista y esperanzado: “Parecía que el mundo estaba a punto de acabarse, pero no se acabó”.

HOW TO WIN A TRADE WAR

is officially published in the US today!!!

Last week was so incredibly amazing

but also so busy

@SoumayaKeynes and I

had some serious Lady Gaga vibes

New @CER_EU policy brief by @SanderTordoir & @Brad_Setser Germany is ground zero of the second #Chinashock, but Berlin is not fighting back, even as the shock erodes the country’s engineering sectors that are vital to its economic security.

Read here: https://t.co/39wGDG2zJm

@Brad_Setser@SanderTordoir It is like saying I got sick because I didn't dress properly for the cold weather. That must be said clearly, with a clear program of - yes - structural reforms to overhaul the economy - or smells of political moral hazard

Needless to say, I fully agree with this brilliant analysis by @upanizza of our Eurobonds proposal and why it doesn’t generate moral hazard - and the graphics rock! @PIIE

1/ Art & the European Debt Trilemma

@DeShindig and @liberioltre at @Unibocconi asked me to discuss European debt.

I like @ojblanchard1 & @AngelUbide@PIIE eurobond paper & was surprised to see suggestions that it would weaken fiscal discipline. My intuition was the opposite🧵

Se sigue confundiendo el debate de eurobonos. No es para emitir nueva deuda y financiar nuevos planes de gasto, sino para optimizar la gestión de la deuda existente y crear una economía europea más estable.

Y añado @judith_arnal: El único bien común 🇪🇺 para el que actualmente se contempla financiación con deuda común es la defensa. Pero cuando el gobierno que con más vehemencia defiende la emisión de nueva deuda común - el de España- solicita solo 1.000 millones de euros del fondo SAFE para compras conjuntas de equipamiento militar, al otro lado de la mesa de negociación muchos se preguntan en qué se gastarían realmente esos nuevos fondos financiados con deuda común.

Y la actual ingeniería contable en torno a los fondos NextGen no ayuda.

@EPoptcheva Querida Eva, te invito a que escuches la intervención del VP1 Carlos Cuerpo en @Piie donde presenta su propuesta similar a la nuestra de optimización de la deuda, no de financiación de nuevas inversiones. Que yo sepa es la única propuesta española https://t.co/1jp0viLUer

@atalaveraEcon La noticia, ademas de basarse en algo que no es cierto, es completamente irrelevante para este debate, a pesar de lo que diga el titular. Eso es lo que digo, si.

No tiene por qué ser así, el debate de eurobonos gira en torno a otras cosas. Y conviene recordar que España se financia al mismo tipo que los eurobonos. España no está pidiendo ayuda, está proponiendo algo positivo para Europa.

No quiero opinar sin saber qué versión es cierta. Pero la mujer del César, además de ser honesta, debe parecerlo. Y lo que está claro es que el daño reputacional ya está hecho y a España le va a costar mucho reparar su imagen, sobre todo en debates sobre la deuda europea común.

Merz opposes taking new debt, including European common debt, to finance current expenditures. We certainly agree. We don't want to increase debt, we want to optimize debt management by replacing some national debt with Eurobonds @PIIE@ojblanchard1

The German media are reporting that €10bn of the recovery fund money earmarked for Spain ended up in the country’s pension system. This is how the good idea of a eurobond gets killed. Mistrust is not only present. It is justified. This example also goes to show that a eurobond can only work as a sovereign debt instrument of a unified state. If you really care about a eurobond to fortify a capital markets union and the euro as a global currency, you should talk about political union first. Don’t make this a technical discussion.

https://t.co/xhrTyJS1Hq

@Manuj_Hidalgo@el_pais Sin duda - Tim Geithner, cuando era secretario del tesoro, siempre nos decía que no quería unicornios, quería propuestas que fueran eficientes y la vez políticamente posibles. Lo más difícil de encontrar.

There is a lively and interesting debate on the pros and cons of Eurobonds. This new piece is highly recommended (irrespective of whether you agree with it or not):

"Eurobonds: Despite objections, they are more needed than ever" by Olivier Blanchard and Ángel Ubide.

"The bottom line is this: European fragmentation severely hampers its economic and geopolitical potential. European leaders have agreed to defragment the single market to boost market size and defragment investment to boost productivity. Our proposal complements these actions by defragmenting the sovereign bond market to lower financing costs."

https://t.co/gJTMusvcqa

Here is a previous piece by the same authors: https://t.co/uRhUTuMiqd

Among many other contributions supporting or rejecting their arguments in favor of eurobonds, this blog post by Hanno Lustig arguing against Eurobonds is particularly recommended: https://t.co/xoLx3A1Qoz

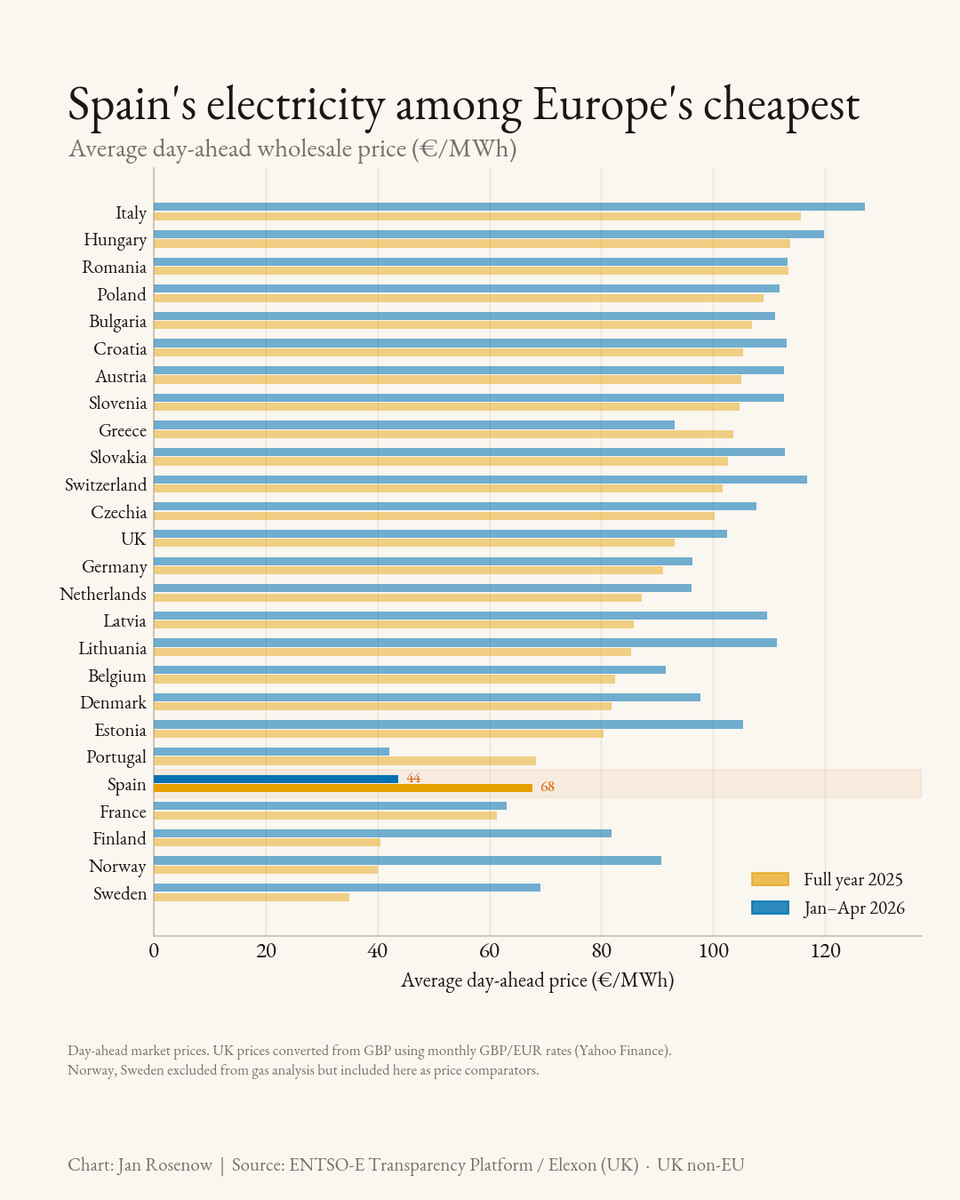

Spain’s power prices have flipped.

A decade ago, Spain was a solar cautionary tale & high-cost market. Now among Europe’s cheapest.

Gas decline is part of the story, but not the whole picture.

More tomorrow: https://t.co/In5lBaF2ox