$ABOS okay here comes a (somewhat?) wild theory.

Bear with me, I need a minute here. If you hate my thoughts, you will at least have a good laugh on me.

Yesterday $CYCN merged with Korsana, a Paragon company (generally hyped). Their lead asset / technology? A blood brain barrier-penetration technology for drug delivery into the brain, Alzheimer´s lead indication.

Korsana raised 175 mln$ in February and 380 mln$ in connection with yesterdays merger. $CYCN was valued at 10 million$ in the merger (with 0$ net cash) and gets about 1.5% of NewCo which implies a 666 mln$ valuation with probably something like 500 million in cash?

$CYCN trading implies a valuation of more than double that, but since it´s a small market cap, this is probably more driven by trading dynamics than fundamentals. Still, I´m pretty sure the financing happened at deemed investor-friendly levels (akin to an IPO).

GET TO THE POINT MAN. Okay, okay.

1/3

Current $XBI drawdown bringing some opportunities, though summer time might see a lot more things just drifting south, seen that often. Small thread about some stocks which recently had a placement and might be of interest. Trying some lesser known names as well.

I like these because I think placements provide a sense of confirmation / anchoring and I like to trade around that.

Engagement bait: You won´t believe what my tenbagger candidate number 7 is about! (hint: it´s a fucking stock).

1/x

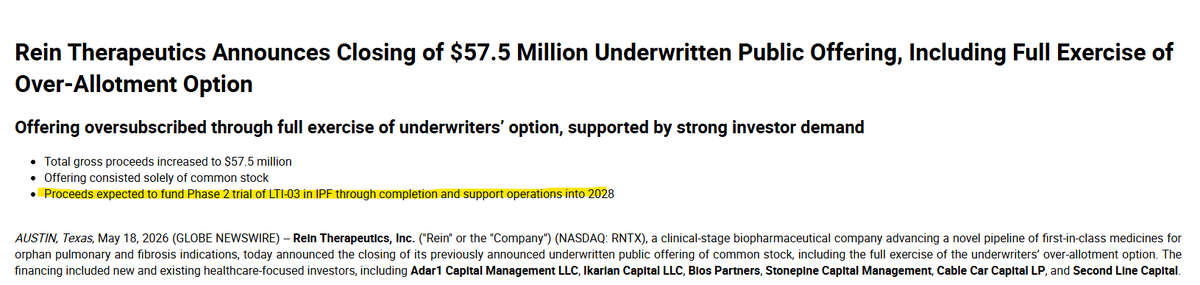

7/x $RNTX 1.02 vs placement at 1$ with some very nice names who love to fish in smaller ponds, love all names on the register. Like this a lot actually, quite the small IPF play, Phase 2 picking up steam. Final data probably 15-24 months out, but there will be an interim Q4 2026.

Probably more likely to fail than not, but a 5x-10x if it succeeds and I think it´s one of the names that will pick up tons of interest once a catalyst arrives.

Probably still 5/10 poops on the ShitCo scala.

$MLYS Really is a strange name. Looked at their deal (buying back ~7% royalty, maybe a bit more, it´s tiered 5-10%) for 200m upfront + 100m in m/s (lets call it 225m NPV).

One hand, they buy like 14-20% (roughly?) of the economics of the drug (assuming a spending-heavy sales force to compete against AZN) for a ~6.9% dilution + 75m in debt which is pretty damn great if you´re a bull.

OTOH Tanabe sells its royalty for an implied "drug value" of ~1.1-1.6B (225/14-20%) against today´s market cap of 2.2B / EV 1.7B.

All of that against AZN expectations they´ll be doing 5-10B with Baxfendy and MLYS possibly taking 15-30% of market?

If they manage to sell the Co for a decent price, this will have been a very strong deal.

@SnupSnus Yeah I thought about that. But it was taken private in 2025, so normally that shouldn´t be an issue. But given how private credit / equity is struggling, might be a reasonable explanation

@SnupSnus@kolnauhc I think the debt financing is neutral as they don´t have to draw the cash. Even if they fully intend to sell the co, they always prepare the launch/finance it anyway

Really striking how basically everybody only makes money if Korea / SOXX trades down.

Even large parts of Biotech and MedTech. MDT is up 10% from yday earnings that guided for 2027 EPS ~1% below estimates

$TXMD Decently weak today with an active seller - an opportunity in my eyes.

Last Q was a nice one. Strange accounting around the minimum royalties from MYX hides the actual PnL.

Case simplified in a few bullets:

- Net cash of ~5.5 mln (rising especially after MYX legal battle is over)

- Just the contractual minimum royalties from MYX are sitting with a PV of 13.17 mln$ on the balance sheet.

- NC + min royalties = 18.64 mln or 1.61$/share

Add the actual US royalties, currently about ~double the minimum royalties my guesstimate based on disclosed MYX sales (adding ~1.14/share)

Add Canada (I think will be ~1mln/year after initial ramp) and Israel (no clue), let´say measly 3mln PV or 0.25/share

Substract legal damage of your choice if they lose to MYX (I have zero clue tbh).

Add ~10mln (0.86/share) valuation for the shell in a reverse merger (which they already prepared at the last AGM).

Looks very asymmetric to me sub 2$ with a rough "value" of ~3.87/share before legal damages. Turning the logic around, the market is pricing in 21.6 mln$ in damages?

And all of that excludes any possible future growth of the MYX US business - see post below how MYX thinks this royalty stream is worth multiple times the amount I am putting into this ... model (lol).

$TXMD update on the update. The day I posted this, Mayne dropped an update for H1 26 at their AGM. Sales on the TXMD-portfolio are up roughly ~1.4% yoy.

They wrote down their contingent consideration a touch. If the old logic applies, that means implied ~9.3$ per share of $TXMD (ex Canada ex SGA).

Also, a shareholder asked why they don´t simply buy $TXMD, lol.

Dude is right, always amazes me. $TXMD was trading at low 1$s a share while Mayne has them at ~7-10$ a share and spends a huge portion of their time valuing the royalties (They said exactly that at the AGM!)

At least accounting wise, taking out $TXMD would create a large profit for Mayne, but their cash position is a bit stretched.

Btw, $MYX.AX looks quite cheap, will probably buy some here.

@given2tweet Think short term important, yes. I think would be prudent for them to strike a smallish placement (150?) and wait for the air to clear.

Long term dilution is prob only a couple %points anyway