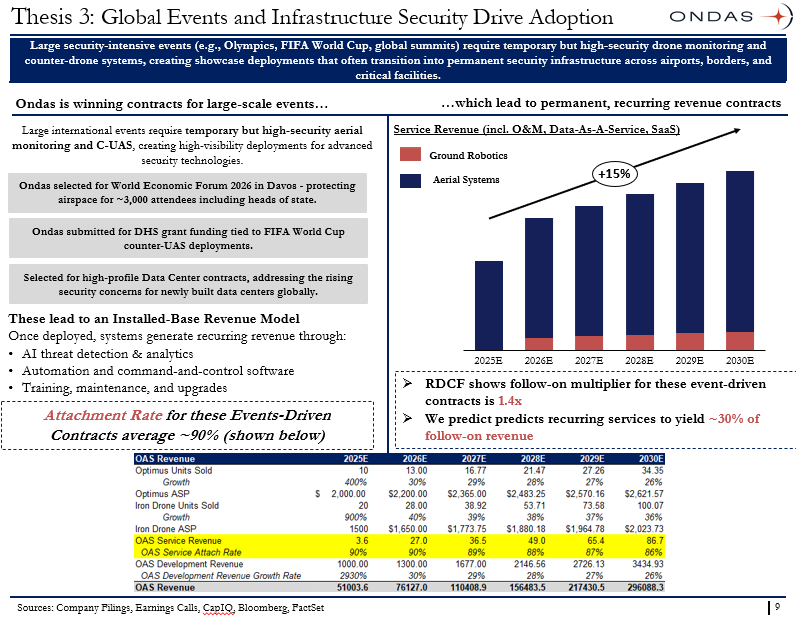

Here’s a slide (1 of our 3 main theses) from an $ONDS pitch that a peer and I drafted out

Core idea:

> Large global events (World Cup, summits, etc.) act as entry points for Ondas to deploy drone security systems, which then convert into long-term, recurring revenue

How it works:

> Events require high-security, temporary aerial monitoring = Ondas wins contracts

> These deployments transition into permanent infrastructure (airports, data centers, borders)

> Leads to recurring revenue from software, analytics, maintenance, and upgrades

Why it’s attractive:

> High attachment rate (~90%): most deployments convert to ongoing services

> Follow-on contracts grow (1.4x multiplier)

> Recurring revenue mix scales (~30% of total), driving more stable, higher-quality earnings

@CeoOndas@BlackPantherCap@YoYInvestor@moninvestor@KawzInvests@jiahanjimliu@BMSInvests@ive_m5@retail_mourinho

$ORCL RPO growth is absolutely wild with backlog adding $85B sequentially while OCI accelerated to 93% growth in Q4.

Oracle is taking on one of the most aggressive AI infrastructure builds in the market and while its Q1 guide implies RPO conversion is stepping up, bookings are still outrunning conversion roughly 4-to-1.

That is why the $40B financing plan is smaller than it looks since customers are already covering $75B of the buildout themselves.

@perplexity_ai is the crappiest LLM known to man - I could vibe code a better one

@plaffont@DanielSLoeb1 you can attest to this - to this day, I can't believe that y'all hosted a pitch comp publicized via @partiful

If this IPO actually happens, I'm liquidating everything

*PERPLEXITY PLANS IPO IN 2028 REGARDLESS OF WHAT HAPPENS TO ANTHROPIC OR OPENAI, CEO TELLS CNBC

The IPO we’ve all been on the edge of our seats for just confirmed

WTF - $FAC opened at $12.33, hit an intraday low of $9.65 and high of $149, closed at $13.80, and swung toward $24 before settling near $21 after hours, with @Nasdaq pausing trading multiple times amid high volume

I had no clue that a company bringing in over $100 million for commercialization... and backed by @MercedesBenz and Stellantis, could pull such meme stock behavior... then I learned that it went public through a SPAC merger and now everything makes sense lol

[BULLISH]

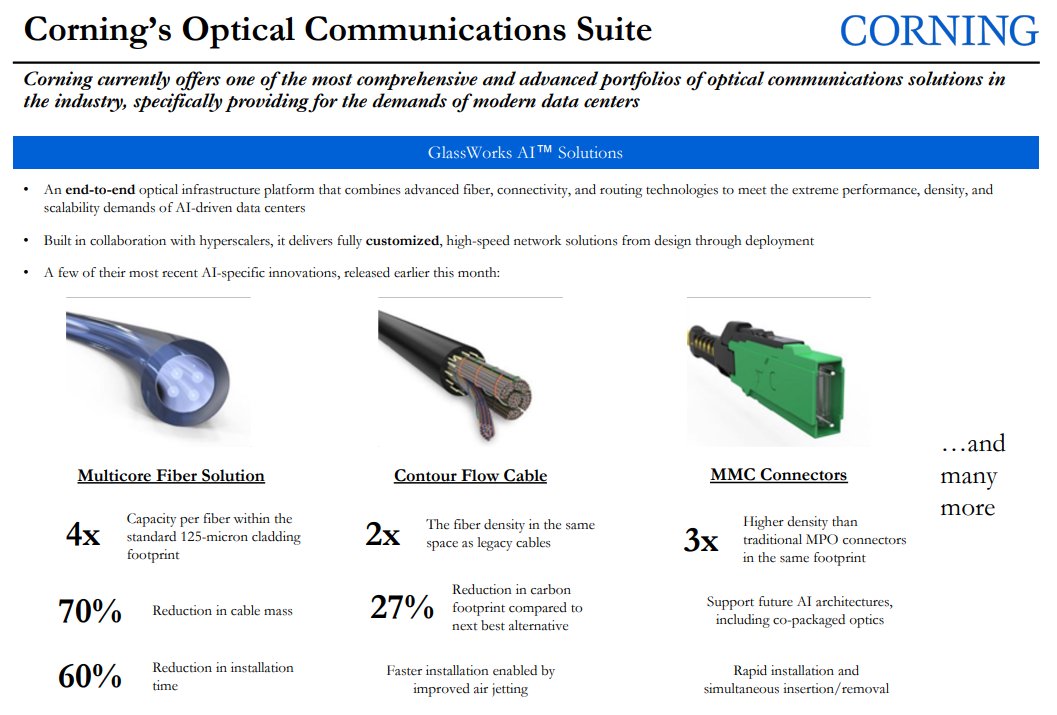

$AMZN announced a multibillion-dollar agreement with $GLW to supply optical fiber, cable, and connectivity solutions for Amazon’s U.S. data center infrastructure. The deal is expected to create 1,000 advanced manufacturing jobs at Corning’s North Carolina facilities and support hundreds of additional construction jobs. Amazon said the agreement will help strengthen the U.S. fiber optics supply chain as demand for AI data centers continues to accelerate.

@amitisinvesting thanks for the insight

[BULLISH]

$AMZN announced a multibillion-dollar agreement with $GLW to supply optical fiber, cable, and connectivity solutions for Amazon’s U.S. data center infrastructure. The deal is expected to create 1,000 advanced manufacturing jobs at Corning’s North Carolina facilities and support hundreds of additional construction jobs. Amazon said the agreement will help strengthen the U.S. fiber optics supply chain as demand for AI data centers continues to accelerate.

@amitisinvesting thanks for the insight

Literally all you need to know about $GLW is here (assuming you're able to infer what the applications and growth trajectory look like)

Copper:

> cheaper and easier to install

> works well over short distances

> lower bandwidth (10 Gbps)

> signal degrades over distance

> heavier, bulkier, more heat/power issues

> vulnerable to electromagnetic interference

Fiber:

> transmits data using light instead of electricity

> massively higher bandwidth (400 - 800+ Gbps)

> maintains signal quality over much longer distances

> thinner + lighter

> lower heat generation and power draw

> immune to electromagnetic interference

What’s interesting is how the hardware itself is evolving around this transition. Some of Corning’s newer optical products:

> multicore fiber = packs multiple light paths into the footprint of one traditional fiber

> higher-density connectors = more connections in the same physical space

> contour flow cables = designed to improve airflow and cable management in dense AI racks

One statistic from the @WSJ jumped out at me:

The AI hyperscalers ($GOOGL, $AMZN, $META, $MSFT, $ORCL) have already issued $159B of bonds in 2026, versus $108B in all of 2025 and just $17B in 2024.

At the same time:

> OpenAI and Anthropic have each raised $100B privately

> SpaceX, OpenAI, and Anthropic are pursuing IPOs

> Google is raising $85B of equity

> Data center developers are tapping HY debt markets

> AI cloud providers are borrowing from banks and private credit firms to buy GPUs

The interesting story is capital formation. Every layer of the capital stack is being mobilized toward the same trade. Historically, that's what happens when investors become convinced that future demand is not only real, but inevitable. Think about it. Railroads.

Telecom. Fiber. Housing. Now AI.

What's fascinating is that the bottleneck is no longer technological innovation. It's financing.

Just 4 hyperscalers are expected to spend over $670B this year on AI infrastructure alone - larger relative to the economy than the railroad expansion of the 1850s. When investment opportunities genuinely exceed internally generated cash flow, companies move up the capital structure. First retained earnings. Then debt. Then equity. Then increasingly creative forms of financing.

That's exactly what we're seeing. The bull case is obvious: AI becomes the foundational infrastructure layer of the global economy and today's capex looks cheap in hindsight. The bear case is more subtle. When every financing market is open simultaneously, capital discipline tends to weaken. The constraint shifts from access to capital to the ability to deploy it at acceptable returns.

The question isn't whether AI demand exists. The question is whether the marginal dollar of AI capex will earn its cost of capital. That's ultimately what determines whether this becomes the next internet or the next telecom buildout.

@OpenAI, @AnthropicAI, and $SPCX all moving toward IPOs at roughly the same time feels less like a technology story and more like a capital markets story.

For the better part of a decade, the highest-quality growth companies stayed private. Capital was effectively unlimited, private valuations rivaled public valuations, and management teams avoided the scrutiny and short-termism of public markets. That's changing.

The companies coming public today are not early-stage businesses looking for funding. They're some of the most heavily capitalized private companies in history. OpenAI alone has raised capital on a scale that would have been unimaginable for a private company a decade ago. So why go public?

One possibility is that private market valuations have reached a point where founders, employees, venture funds, and crossover investors increasingly prefer liquidity over another funding round.

Another is that AI has become one of the few sectors capable of absorbing enormous amounts of public market capital despite highly uncertain long-term economics.

What's particularly interesting is that these IPOs are arriving before the industry structure is settled. We don't know who will ultimately capture the economics of AI. We don't know what steady-state margins look like. We don't know whether model providers, infrastructure providers, application companies, or enterprises will capture the majority of value creation. Yet investors are already being asked to underwrite trillion-dollar outcomes.

Historically, IPO booms occur when the market becomes comfortable capitalizing narratives that extend far beyond observable fundamentals. That doesn't mean the narratives are wrong. The railroad boom happened. The internet boom happened. AI is happening.

But history also suggests that technological adoption and investment returns are not the same thing. The reopening of the IPO market may be less a signal about AI's future and more a signal that investors are once again willing to fund long-duration assets whose valuation depends heavily on terminal assumptions.

One of the most interesting trends in investing is the financialization of uncertainty.

Hedge funds, banks, and trading firms are aggressively hiring catastrophe modelers, weather analysts, and insurance-linked securities (ILS) specialists to quantify everything from hurricanes and wildfires to floods, cyberattacks, civil unrest, and even war.

Most investors think of these as "unpredictable" events, but the market increasingly views them as probabilities. In my opinion, that's a subtle but important distinction.

Historically, a hurricane was an insurance problem. A wildfire was a local problem. A flood was a government problem. And today, they're investment problems.

If you can estimate how a storm affects power demand, mortgage defaults, insurance losses, supply chains, commodity production, real estate values, or utility infrastructure before everyone else, you've created an edge. What's fascinating is that the same framework is now being expanded beyond weather. Firms are exploring catastrophe-style models for cybersecurity, civil unrest, and geopolitical conflict.

In other words, investors are attempting to do for tail risks what quants did for factors decades ago. The implication for public equities is significant. I believe that the next generation of alpha may not come from building a better DCF. Instead, it may come from building a better probability distribution around events that most investors still treat as unknowable.

Markets don't pay you for knowing what will happen. They pay you for estimating the odds better than everyone else.

Long lines for restaurants, bakeries, and trendy food concepts are a sign of economic dynamism and social-media-driven demand. But as an investor, I'd take it in a different direction - the interesting insight is that the line itself has become part of the product.

Historically, companies competed on product quality, price, and convenience. Today, many consumer brands compete on visibility and cultural relevance. A 1-hour wait for a sandwich is objectively inefficient, yet consumers willingly participate because the experience signals status, authenticity, or belonging. The article cites surveys showing a significant portion of Gen Z and Millennials have waited 30+ minutes for specific foods, often motivated in part by social media.

From a public equities perspective, that's important. The highest-multiple consumer businesses increasingly aren't selling just products, but also attention.

A line outside a store is effectively user-generated advertising. Every person waiting becomes a marketing asset. Every TikTok post lowers customer acquisition costs. Every viral queue creates scarcity, even when supply isn't actually constrained.

This helps explain why certain restaurant concepts, beauty brands, athletic apparel companies, and consumer platforms achieve outsized valuations relative to their current earnings power. Investors aren't paying for today's cash flows. They're paying for evidence that a brand has become culturally embedded.

The challenge, of course, is that cultural relevance is not the same thing as durable competitive advantage. A line can be a moat... Or it can be a symptom of a fad. The investing question isn't whether people are willing to wait in line today, but rather whether that attention compounds into repeat purchases, pricing power, and long-term customer lifetime value.

That's the difference between the next $SBUX and the next frozen-yogurt craze.

The Bloomberg headline is that the likes of Point72 and Citadel are exploring paying other hedge funds for trade ideas. Frankly, the more interesting story is what it says about the evolution of alpha itself.

For decades, the hedge fund business was built around the assumption that alpha was generated internally. You hired smarter analysts, built better research processes, and produced differentiated views. But today, many of the largest platforms appear to be reaching a different conclusion - alpha may be generated externally, but the edge comes from identifying, aggregating, filtering, sizing, and risk-managing it better than everyone else.

There are obvious benefits. A multi-manager platform can observe thousands of signals across sectors, styles, geographies, and time horizons. Even if any individual idea has limited value, the portfolio-level information content can be significant.

But there are also obvious tradeoffs. Once everyone is buying from the same ecosystem of contributors, differentiation becomes harder. Crowding risk increases. Consensus trades emerge faster. The value of a signal decays the moment it becomes broadly distributed.

Ironically, alpha capture programs may make markets more efficient while simultaneously making alpha harder to find.

The firms most likely to benefit are not necessarily the ones with the best ideas. They're the ones with the best infrastructure for determining which ideas are worth acting on. The winning hedge fund increasingly looks less like a research shop and more like an information processing engine.

so first @realDonaldTrump (most recently with $DELL)

then Jensen (most recently with $MRVL)

now @elonmusk with $ASML

not even gonna do anymore DD - I'm long lol

Chart from @coatuemgmt

Investors spend enormous effort searching for the next unicorn while overlooking a simpler reality: the hardest part isn't growing from $10B to $100B. Tbh, it's surviving long enough to prove you deserve to

By the time a company reaches $100B, it has often already solved the existential risks that kill most businesses. That's why scale isn't always the enemy of returns (it tends to be the source for them)

Last week's jobs report may have made this week's inflation prints even more important. A soft labor market would've given the Fed cover to look through a hot CPI

Instead, payrolls came in stronger than expected and unemployment held steady, meaning the burden shifts back to inflation. If CPI reaccelerates, the "cuts are coming" narrative gets a lot harder to defend tbh

Last week's jobs report may have made this week's inflation prints even more important. A soft labor market would've given the Fed cover to look through a hot CPI

Instead, payrolls came in stronger than expected and unemployment held steady, meaning the burden shifts back to inflation. If CPI reaccelerates, the "cuts are coming" narrative gets a lot harder to defend tbh

Key Events This Week:

1. May Existing Home Sales data - Tuesday

2. May CPI Inflation data - Wednesday

3. May PPI Inflation data - Thursday

4. OPEC Monthly Report - Thursday

5. MI Inflation Expectations data - Friday

6. MI Consumer Sentiment data - Friday

All eyes are on inflation this week.

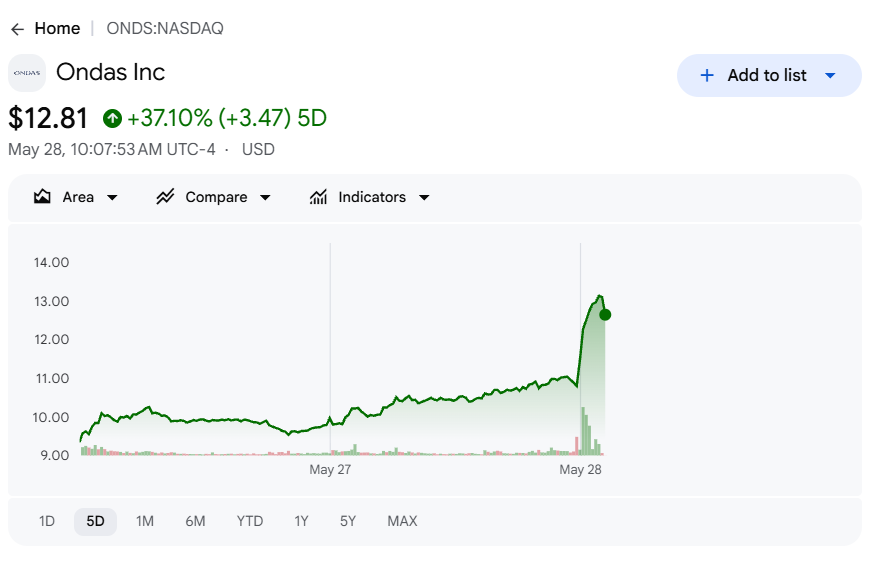

After market participants saw what the SpaceX IPO did for space stocks it’s pretty reasonable to assume the Anduril IPO anticipation could have a similar effect on drone and defense stocks…

After watching the likes of $OUST and $ONDS run these past couple of trading sessions, I went through our original $ONDS pitch from a couple of months ago. Was taking a look at one of the theses that my partner and I came up with, and I immediately thought of this:

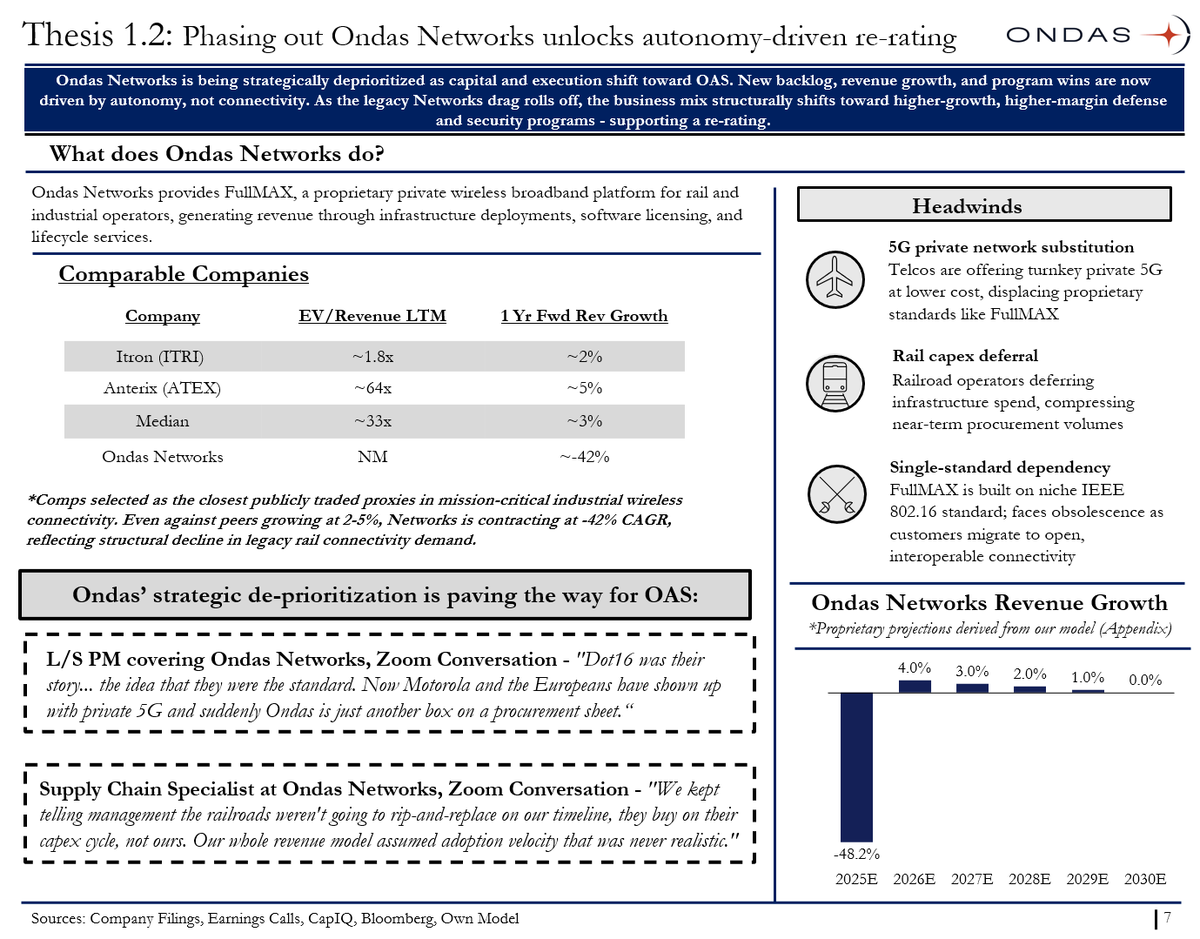

No one's talking about Ondas Networks. Not management, not the @X community... and for good reason

> FullMAX is contracting at -42% CAGR against comps growing 2 - 5%. Railroad capex is deferring, private 5G is commoditizing the product, and the whole segment is built on a niche IEEE 802.16 standard facing obsolescence

If I'm an activist here, the play is simple: stop subsidizing a structurally declining connectivity business with capital that should be accelerating OAS. Trim the fat, wind down Networks, and let the autonomy/defense story trade on its own merits

@CeoOndas hasn't spoken about Networks at all in the past few earnings/press releases... if management can acknowledge the elephant in the room, I think we're due for a significant re-rate (much crazier than another acquisition or contract)

Thoughts? @BlackPantherCap@YoYInvestor@moninvestor@KawzInvests@jiahanjimliu@BMSInvests@ive_m5@retail_mourinho@itschrisray@StockSavvyShay

After watching the likes of $OUST and $ONDS run these past couple of trading sessions, I went through our original $ONDS pitch from a couple of months ago. Was taking a look at one of the theses that my partner and I came up with, and I immediately thought of this:

No one's talking about Ondas Networks. Not management, not the @X community... and for good reason

> FullMAX is contracting at -42% CAGR against comps growing 2 - 5%. Railroad capex is deferring, private 5G is commoditizing the product, and the whole segment is built on a niche IEEE 802.16 standard facing obsolescence

If I'm an activist here, the play is simple: stop subsidizing a structurally declining connectivity business with capital that should be accelerating OAS. Trim the fat, wind down Networks, and let the autonomy/defense story trade on its own merits

@CeoOndas hasn't spoken about Networks at all in the past few earnings/press releases... if management can acknowledge the elephant in the room, I think we're due for a significant re-rate (much crazier than another acquisition or contract)

Thoughts? @BlackPantherCap@YoYInvestor@moninvestor@KawzInvests@jiahanjimliu@BMSInvests@ive_m5@retail_mourinho@itschrisray@StockSavvyShay

Here’s a slide (1 of our 3 main theses) from an $ONDS pitch that a peer and I drafted out

Core idea:

> Large global events (World Cup, summits, etc.) act as entry points for Ondas to deploy drone security systems, which then convert into long-term, recurring revenue

How it works:

> Events require high-security, temporary aerial monitoring = Ondas wins contracts

> These deployments transition into permanent infrastructure (airports, data centers, borders)

> Leads to recurring revenue from software, analytics, maintenance, and upgrades

Why it’s attractive:

> High attachment rate (~90%): most deployments convert to ongoing services

> Follow-on contracts grow (1.4x multiplier)

> Recurring revenue mix scales (~30% of total), driving more stable, higher-quality earnings

@CeoOndas@BlackPantherCap@YoYInvestor@moninvestor@KawzInvests@jiahanjimliu@BMSInvests@ive_m5@retail_mourinho