Breaking News:

- $PYPL rumored to be in talks with Stripe.

- $PYPL rumored to not be in talks with Stripe.

- Hedge funds rumored to be in talks with your stop losses.

Fair point with Jamie being trained to only look at deals with govt backstops and low risk…but generally large cap companies do like these types of deals because they can actually move the needle.

JPM was just a way of illustrating synergies specific to them but synergies can be found with a lot of the larger fintech companies and traditional retail banks. PayPal/Venmo is a massive distribution asset. Fintechs and banks pay a fortune for user acquisition. This acquisition would be instant scale. Plug PYPL into a broader platform and you can upsell lending, cards, investing, deposits, BNPL. The lifetime value math gets interesting and I'm sure this headline will light fires under these companies M&A teams to figure out WHY Stripe is going after them.

I think $JPM can come in and bid against Stripe for $PYPL -

Today:

- PayPal earns ~10 USD/year per account; JPM pays 161 USD per account at 70B, i.e., 17 years of current earnings. That’s too rich on a stand‑alone basis.

Post‑deal:

- JPM lifts PayPal’s own economics to ~16 USD/year profit per user (2.8B more profit).

- Uses PayPal/Venmo as a giant digital distribution channel to drive ~4B/year of incremental JPM profit via cards, deposits, and loans.

- Removes ~1B of annual duplicate opex.

Result:

- Once synergies are fully realized, the combined entity is earning ~7.8B/year incremental profit on the 70B outlay, with a ~9‑year payback and a high‑teens‑type IRR when you include a reasonable terminal value.

Bottom Line:

- At 70B it’s not a “cheap multiple” deal – it’s a distribution + data + cross‑sell where JPM turns a low‑monetized 10 USD/year PayPal user into a 20–30+ USD/year profit stream and a deeper bank relationship, while materially lowering CAC per future JPM customer.

100% speculative but agree to your point that shareholders will not be happy with an outcome under $70…so naturally offers gravitate towards that

Valuation now makes it much more of an attractive target to a plethora of buyers ranging from strategic, big name acquirers like Stripe/JPM/AMZN to bloodsucking cash flow guzzlers like large PE firms

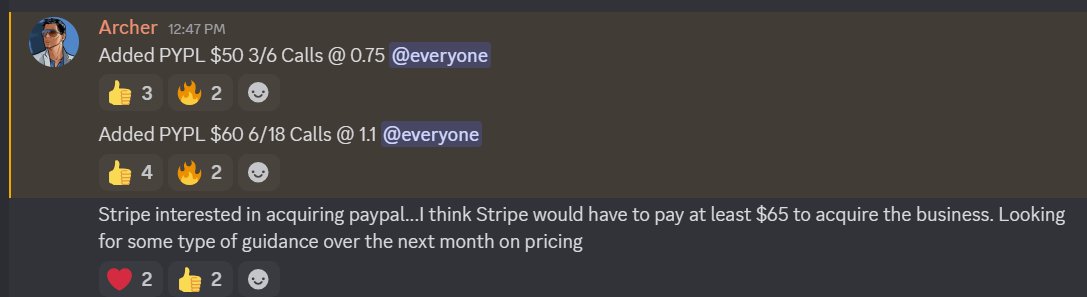

$PYPL Stripe saying they’re interested in buying all or parts of PayPal opens the door for other fintechs or even traditional banks to step in. These other companies will not want Stripe walking away with that user base uncontested.

PayPal/Venmo is a massive distribution asset. Fintechs and banks pay a fortune for user acquisition. This acquisition would be instant scale. Plug PYPL into a broader platform and you can upsell lending, cards, investing, deposits, BNPL. The lifetime value math gets interesting and I'm sure this headline will light fires under these companies M&A teams to figure out WHY Stripe is going after them.

If this turns competitive, I have a hard time seeing it below $65. That’s ~40% over today’s close. And if it actually becomes a bidding situation, $75–$80 seems plausible given the stock was valued there a few months ago before acquisition chatter.

$PYPL Stripe interested in acquiring PYPL. I would think they know a competitive offer is over $70. Buy now, ask questions later with the assumption multi month contracts probably haven't been priced right yet.

Swinging AAPL 3/13 $285 Calls @ 0.7. Targeting $275 and then $285+

- Institutional, aggressive call flow

- Relative strength especially compared to the tech bleed today

- Only one that stands against the CAPEX burn, so seeing rotation from META/MSFT/GOOGL to AAPL...showing inverse price correlations

- Can move to 272.5-275 this week

Swinging AAPL 3/13 $285 Calls @ 0.7. Targeting $275 and then $285+

- Institutional, aggressive call flow

- Relative strength especially compared to the tech bleed today

- Only one that stands against the CAPEX burn, so seeing rotation from META/MSFT/GOOGL to AAPL...showing inverse price correlations

- Can move to 272.5-275 this week