I wrote about the Social Security trust fund this week, which is set to run dry some time in 2032-33. The fund has been saved before, notably in 1983 by a bipartisan deal that broadened the tax base and raised the retirement age. Ask yourself: can you imagine such a deal now?

First, the supreme court collapsed the Trump administration's tariff wall.

Then the Trump erected a temporary tariff fence, due to fall down again in late July.

Last night USTR shared how it plans to rebuild the tariff wall's foundations. 🧵

I wrote about the American side here

America is experiencing a productivity miracle

https://t.co/UCeZbwr8ck…

from The Economist

Facially implausible, given just the GDP growth numbers, that western Europe’s seen ~2% productivity growth over that period.

(Again, all this precedes the debate on levels.)

Important point here— the data are certainly unambiguous that western Europe’s productivity growth for the past decade has been dramatically worse than in America.

And that should be enough to fuel worries about competitiveness, quite apart from the levels.

On the Krugman et al/Aghion et al discussion. Working my way through it.

The easy part. Let’s settle the central issue, the measurement of productivity growth, i.e. the rate of change of output per hour.

There can be no question that the best measure of the rate of change of output is obtained by using chain indexes. This is what advanced countries, the US and European countries do. (slight difference between the US and other: Fisher versus Laspeyres indexes. Not irrelevant for the question at hand, as the two can differ when one sector, say AI, experiences sharp decreases in prices. But, I believe, not serious enough an issue to change conclusions) Quality adjustments vary across countries, but it is not clear how they bias the comparison between the US and Europe.

Main point re discussion: No reason whatsoever to use anything else (such as PPP prices) than the national measures of productivity growth.

Implication: Almost surely, productivity growth is lower in Europe than in the US.

This does not settle the issue of how to compare levels (as opposed to growth rates) between the US and Europe, or what this implies for the relative standards of living (and the role of terms of trade, and the potential for immiserizing growth in the US). More on those later.

“Main point re discussion: No reason whatsoever to use anything else (such as PPP prices) than the national measures of productivity growth.

Implication: Almost surely, productivity growth is lower in Europe than in the US.” — start with this from Blanchard, and look at the national-accounts measures of real output per hour in the US versus any of France, Britain, Germany etc and the difference is pretty staggering, especially post-Covid.

Would love to see how one gets to any other conclusion (barring either cherry-picking windows or smuggling in Eastern Europe’s catch-up growth).

For what it’s worth 2.5% aligns far better with my intuitions about

— Post-2016 performance of comparable economies

— The places in the data Brexit is most visible (business capex, goods trade)

— The scale of plausible trade policy impacts on GDP

than the 4-8% numbers out there

June 2026 - 10 years on from the Brexit Referendum. What is the economic verdict? Negative, certainly. We estimate the UK economy is 2.5% smaller (~£75bn/year) as a result. But it is not the biggest negative impact on growth over the last decade. Domestic failures in energy, capital, construction & labour markets have had an impact twice as large. Charitably you could argue that Brexit took away the policy bandwidth that allowed these domestic failures to emerge unchallenged. But the evidence is they were done willingly, and look like noble intentions that got out of hand. More here in today’s @TimesBusiness https://t.co/e95BYxVfYi and a nonpaywall version here: https://t.co/ugOV4ZfCDH

A test for this: if you doubled your token use, how much would you increase the value you get from AI? This gets elasticity.

My guess would be it's much less than double. (and if you don't usually hit your token limits then implied marginal value is zero).

"A genuinely neoliberal system begins with the presumption of liberty. Modern Britain increasingly begins with the presumption of requiring permission." -- exactly right

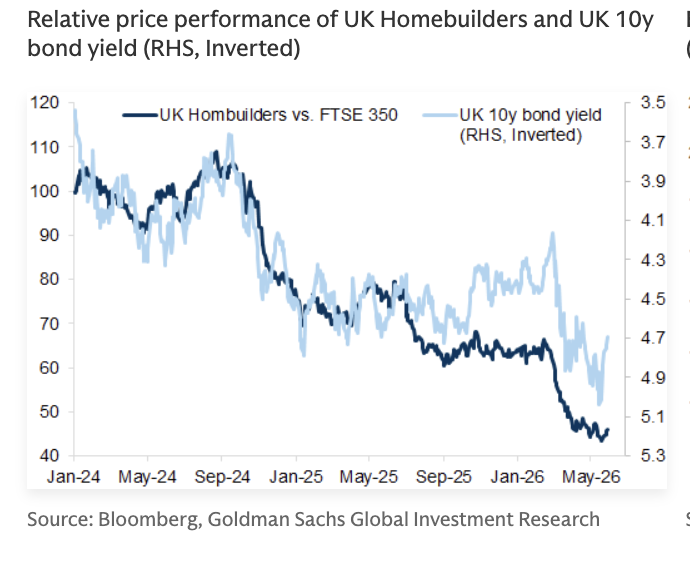

Since Britain elected a purportedly pro-housebuilding government two years ago:

— Homebuilders' share price has fallen by around half vs the index

— That is sharply in excess of what you'd expect given rising bond yields alone (and on those, too, the gov't is far from blameless)

@_night_brain__ Not sure where you see gloating, just sharing a well-written piece from the archive.

As it happens though, our Con/Lib coalition endorsement in 2015 has to my mind aged perfectly well-- not least given what we've seen of Miliband in cabinet recently.

https://t.co/jpH175bLfs

Obligatory reminder that the “k-shaped” economy is basically a mirage:

— Better spending measures show no new rich-poor divergence

— Little else (eg consumer confidence measures split by income, credit card spending data) shows that pattern

https://t.co/kMiwRofcvd