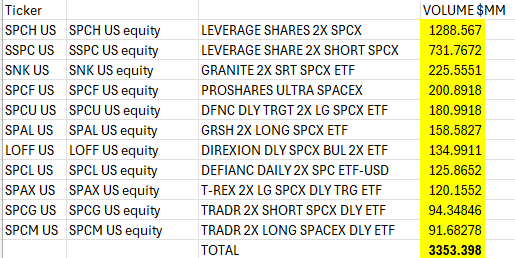

Update on the 2x SpaceX ETF race: over $3b traded (vs $1b yest) and shocker EVERY SINGLE ONE is pretty much at $100m or more. Hard to believe. Also, $SPCH at $1.3b is the most volume ever recorded by ETF on a Day Two ($IBIT 'only' did $500m). Total feeding frenzy. To the ppl who doubted there was enough degens to support this many leveraged ETFs tracking the same stock (incl me) at same time. Well it turns out there is. What a country.

The oil price is now 10% lower than the 88 USDs that the ECB said was the MILD scenario for Q3 2026. All of the assumptions used to hike interest rates last week have vanished into thin air.

Most likely the most tone-deaf central bank meeting this decade. Follow us at Nowcast IQ if you want timely data, so that you can outsmart the central bank!

Aletheia on $MU:

"We forecast MU’s EPS to jump 8.5x in CY27E, followed by a further 1.8x expansion in CY28E. This implies roughly 15x cumulative EPS growth and $350–400bn of FCF generation in FY26-28E."

"We now expect server DRAM ASP to jump a further 30% in C3Q26 (vs previous expectation of 10- 15%); this is likely to rise by another 10-15% in C4Q26 (same as previous expectation)"

"we now expect HBM ASP to double YoY in C2027"

"Our analysis shows that memory devices are becoming the most critical components in the AI hardware system as their combined content value are expected to cross over 70% in 2027 vs mid-40%s in 2025. For DRAM-intensive device such as Vera CPU, the SoCAAM alone contributes over 70% of BOM in 2H26; the full spec Vera CPU rack could reach a staggering $26M ASP per rack..."

Micron is going to be a $4,000 stock and the CEO just told you exactly why in one interview (Save this).

Micron is no longer a chip company but rather a America's monopoly on the most strategically critical material in the AI buildout.

It's the only western company manufacturing memory at advanced nodes, sitting on $200 billion in committed domestic capex, with every unit of its highest value product already sold.

let's start with the supply reality, Mehrotra said Micron can currently meet only 50% to two thirds of the demand from its key customers.

That shortage will last well beyond 2027, and meaningful new supply from anyone in the industry does not arrive until 2028 at the earliest.

Two more years of demand outpacing supply in a market growing 168% year over year and that is the floor on the bull case.

Now layer on what makes this cycle structurally different from every one before it.

Micron is the only American memory manufacturer on earth, Samsung and SK Hynix are South Korean.

In a world where AI infrastructure has become a declared national security priority where Commerce Secretary Lutnick and Trade Ambassador Greer personally showed up to a fab dedication in Manassas, Virginia being the only US memory company is not just a competitive advantage.

It is a government backed structural monopoly on the most critical input to the US AI buildout, backed by $6.2 billion in CHIPS Act subsidies across Idaho, New York, and Virginia.

The $200 billion buildout spans Manassas for DDR4 defense and industrial memory, Boise for leading-edge DRAM with first wafers out mid 2027, a second Boise HBM fab with first wafers by end of 2028, and the Syracuse megafab, the largest semiconductor facility in US history, breaking ground January 2026 with up to four fabs over time.

Combined, these sites take Micron's domestic production from 10% of its total output today to 40% over the next decade, and create 90,000 jobs in the process.

The business model transformation is the real story.

Come join Milk Road Pro for our full breakdown, our complete Micron valuation model incorporating the $200 billion domestic buildout and our entire AI thesis.

Link below.

Mehr News has released a short version of the 14-clauses of the MoU that will be signed on Friday, between Iran & US.

1. The permanent and immediate halt of war on all fronts, including Lebanon.

2. A U.S. commitment not to interfere in Iran’s internal affairs and to respect the sovereignty of the Islamic Republic of Iran.

3. The complete lifting of the naval blockade within 30 days.

4. A U.S. commitment to withdraw its forces from the areas surrounding Iran.

5. The reopening of the Strait of Hormuz within 30 days under Iranian ��arrangements”.

6. The suspension of oil sanctions, petrochemical products and derivatives, and Iran’s full access to the financial proceeds from them.

7. The requirement for the US & its allies to present reconstruction plans for Iran worth at least $300 billion.

8. Sixty days of negotiations to reach a final agreement based on nuclear issues and the complete lifting of primary and secondary U.S. sanctions, as well as UN Security Council resolutions and resolutions of the IAEA Board of Governors.

9. Iran’s reiteration of its commitment under the NPT not to produce nuclear weapons.

10. During the negotiation period, the U.S. has committed not to add to its forces in the region and not to impose any new sanctions.

11. The release of $24 billion of Iran’s frozen funds during the 60-day period of final negotiations. Half of this amount must be made available to Iran before the negotiations begin.

12. The formation of a supervisory mechanism to implement the agreement.

13. The final agreement will be approved through a UN Security Council resolution.

14. Final negotiations will not begin before half of Iran’s frozen funds are released, Iran’s oil sanctions are suspended, and the naval blockade is lifted. The final agreement will be limited only to the fate of enriched materials and enrichment, sanctions relief, and the program for rebuilding Iran’s economy. Discussions about Iran’s missile program and support for Resistance groups have been definitively removed from the agenda.

Key Events This Week:

1. May Industrial Production data - Monday

2. May Housing Starts data - Tuesday

3. May Retail Sales data - Wednesday

4. Fed Interest Rate Decision and Kevin Warsh's First Meeting as Fed Chair - Wednesday

5. June Philly Fed Manufacturing Index - Thursday

6. US Markets Closed for Juneteenth - Friday

All eyes are on the Fed this week.

The shift brought about by HBM:

- From 1957 to 2020, DRAM cost per Gb declined by roughly one order of magnitude every five years, making it one of the clearest examples of Moore’s Law in cost terms.

- However, demand for AI infrastructure and the emergence of HBM have directly overturned the cost-reduction pattern that had persisted for decades.

Korea’s export data for the first 10 days of the month was absolutely absurd, trending close to 90% YoY.

On historical correlations, that would imply a fair value for the semiconductor index that is potentially 50 to 60% higher than current levels.

Yes, I said that.

Dot com peak is meaningless. These companies are apples to those oranges. All you blackpillers do is spread this nonsense in hopes of it sticking but never ask the question as to why the most resilient, powerful and dominant technology companies in the world are all spending like this. Do you think they’re unaware of the dot com bubble? Or unaware of the criticisms? I mean golly there’s gotta be a reason. Man what could it be???

🔼 $AMD upgraded to Buy from Neutral at Citi

Citi analyst Atif Malik upgraded AMD to Buy from Neutral with a price target of $575, up from $460.

The firm says the company's graphics processing unit upside is not fully priced into the shares. AMD is "emerging as a legit second source" in the GPU market, the analyst tells investors in a research note.

Citi sees the company as well positioned to win the "lion's share" at Meta. It believes AMD is still being viewed as a central processing unit stock, which creates upside potential.

🧠 AI MEMORY SHORTAGE (60 SEC BREAKDOWN)

We modeled supply vs demand for HBM4 = the memory every AI chip is bolted to. Only 3 companies on earth make it - $MU is one of them.

▪️Demand > supply every quarter through 2028

▪️Worst gap: late 2027 (only ~70% of orders filled)

▪️Bottleneck isn't fabs, it's stacking machines

▪️16 perfect layers per chip (1 crooked layer= trash)

📡SK hynix just panic-ordered more = the signal.

▪️Price path: $16.60 → $30+/GB. Bull: $53

▪️Buyers not bluffing: each $16.60/memory ~$29/yr AI revenue

▪️Micron at $900 looks expensive, but trades under 8x our 2028 estimate.

▪️Street EPS went $12 → $108 in a year.

The market believes the money, but it just doesn't believe it lasts - our model says it lasts through 2027, but 2028 is the fight.

🔔4 smoke alarms to get us out early:

▪️memory prices below model

▪️machine orders slowing

▪️AI revenue per GB rolling over

▪️+94% YoY industry growth peaking

Every boom funds the overbuild that ends it - our alarms are built to ring 2 quarters before the top🚀

And speaking of the ECB, sorry, the Bundesbank, they still project 0.8% annual growth in 2026 (despite yesterday's updates), which, as far as I can calculate, will require roughly three quarters of 0.5% growth following the contraction in Q1.

I will let you decide for yourself whether you find that assumption realistic given the Eurozone's hit rate of reaching 0.5% quarterly growth in recent years, but those growth assumptions play a major role in understanding the ECB's inflation view.

I will take the under any day, and reiterate that Lagarde's vibe yesterday had a certain Comical Ali element to it.

The Korean export data for the first 10 days of the month came in extremely strong this morning, at 85.9% year-on-year versus 43.7% in May.

And you are telling me that AI demand is not accelerating?