Due to popular demand, after a brief hiatus, Oak’s ASGCT abstract dump is back - now it’s 5th installment, better than ever

Posting later than I’d hoped - still shaking off the rust - but the show must go on; & what’s better than starting ASGCT Day 2 with the thread you needed 2 weeks ago?

(1/21)

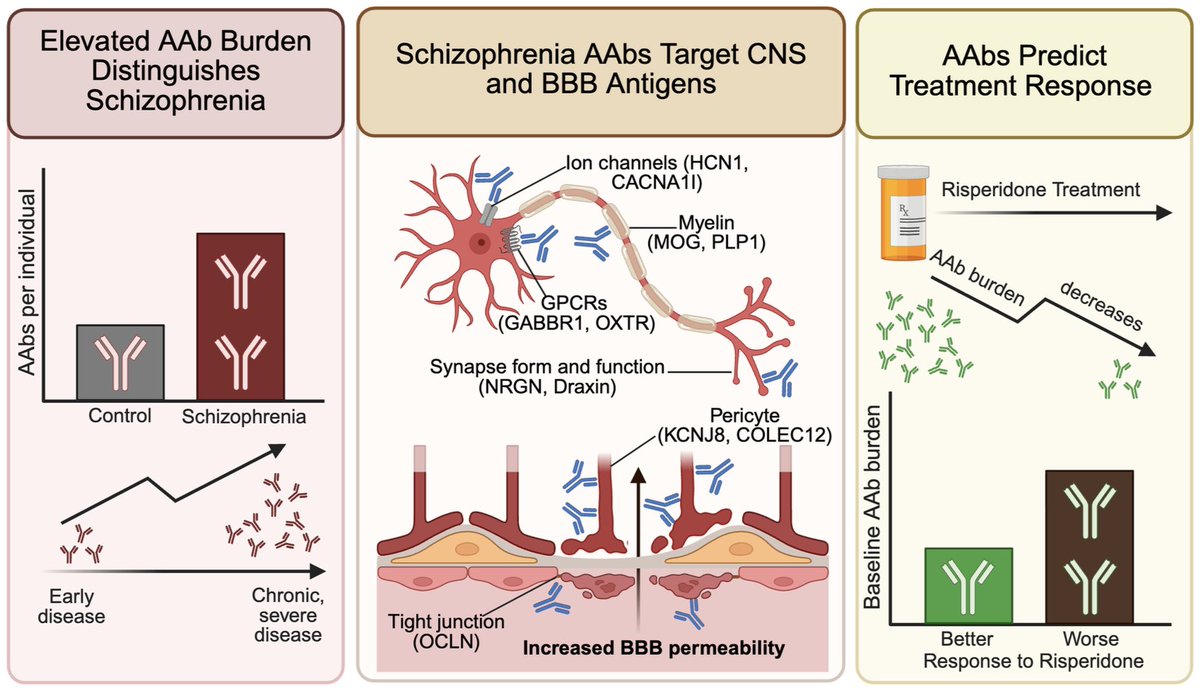

Autoantibodies cause autoimmune disease, shape infection outcomes, and alter cancer immunotherapy. But what role might they play in neuropsychiatric disease? In our new preprint, Katlyn Nemani and @JillianRJaycox take on this question in schizophrenia. 🧵

https://t.co/lmL4sx7QSz

Drug hunters everywhere, sear the lesson of Revmed and daraxonrasib in your brain:

Life is too short for incrementally me-too and me-better. Drug the fucking undruggrable and you can double OS, even in pancreatic cancer.

Absolutely inspiring. LFG.

It may be that failure to count competitors stampeding towards your de-risked target is now the single biggest reason drug R&D programs fail in Phase 2 & 3.

"Commercial" termination overtakes "efficacy" circa 2019: https://t.co/xnqjAGiBMi

Recent oncology example (TIGIT herding): https://t.co/TUAdjnm7Px

Biotech is a lottery business: most drugs fail, a few wins pay for everything.

BridgeBio’s insight: manage biotech like a portfolio, not a single bet ($10M to IND & $25M IND to POC)

Source: https://t.co/8WpCVMfBbz

Earnouts are mostly illusory. Across life‑sciences M&A since 2008, SRS Acquiom finds $95.1B in potential milestones, $9B paid = 9.5% of potential value realized. https://t.co/dptorrzD60

In Bio/Pharma specifically, only 7% of earnout dollars were paid according to their 2023 lifesciences study. https://t.co/RqLNw4x6Zj

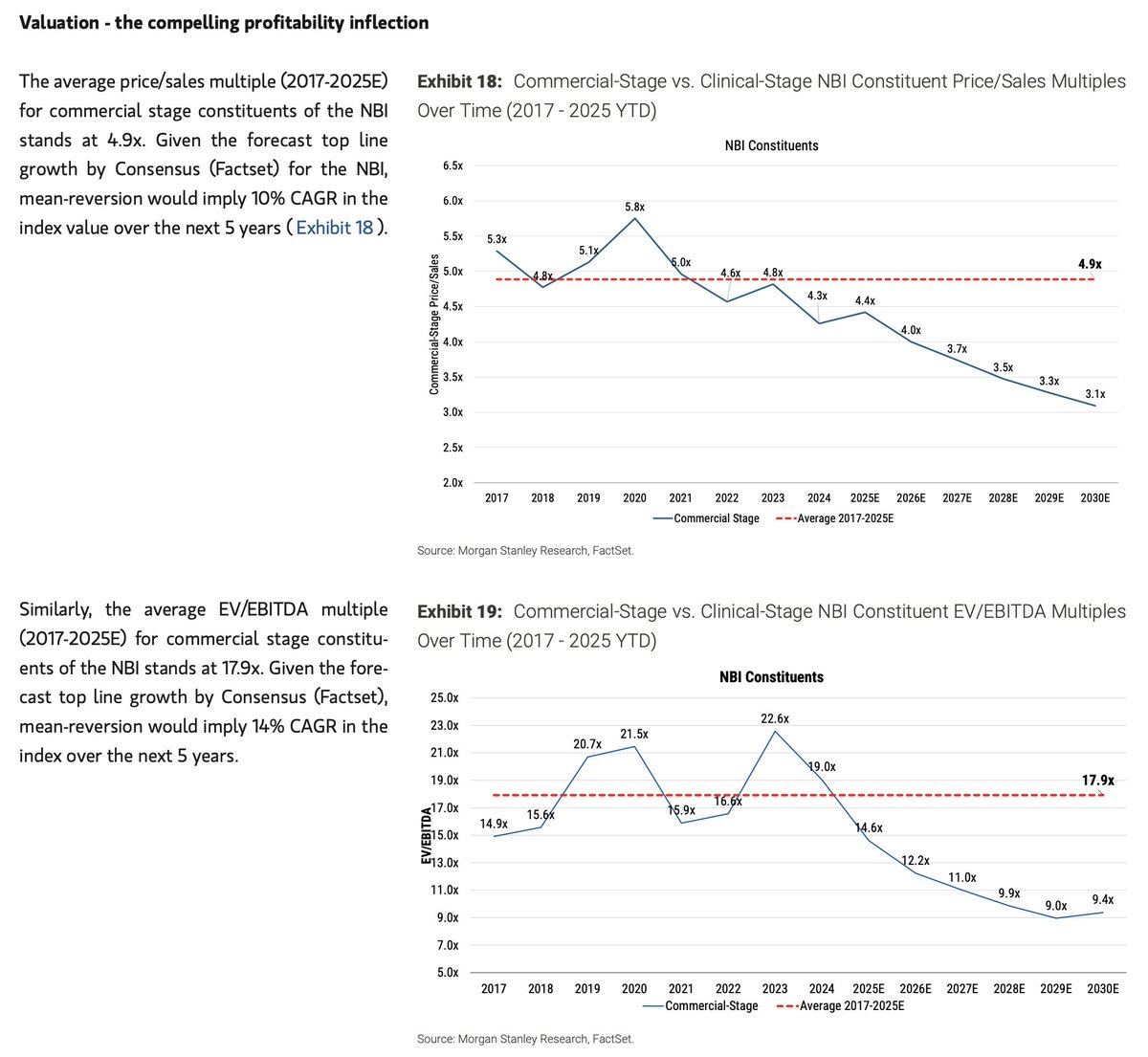

Another distillation of the forthcoming inflection in SMid biotech profitability from Morgan Stanley $XBI $NBI $BBC

Projected 14% topline ’25-30 CAGR, with aggregate EBITDA reaching ~$40B at a mid-teens ROE. At historical multiples, implies a 10-14% CAGR for NBI through 2030

And with current commercial-stage valuations still lagging historical averages, hard to argue the setup isn’t attractive

China vs. US biotech in a nutshell: $340M vs $22M to Ph1 in vivo CART data

- Capstan Therapeutics: Founded 2022, raised $340M, launched Ph1 for in vivo CAR-T in June 2025 (3yrs + $340M to Ph1), bought for $2.1B by @abbvie

- Starna: Founded 2021, raised $22M, launched Ph1 in June 2025 (4yrs + $22M to Ph1), just raised $44M Series B; note they also spent some time/money on a vaccine platform prior to the in vivo CART work

“Tx w/ prednisolone, mesalamine, infliximab, ustekinumab, ozanimod, filgotinib, vedolizumab, upadacitinib, & cyclosporine + mirikizumab had not induced remission”

Sheesh. Imagine that journey

Then, <1M after CAR-T, you’re in remission, off drugs, 20lbs heavier, & back to work

Have followed $ARGX MuSK Agonist for years - simply b/c it’s an elegant scientific story (MOA inspired by autoAbs in MG), & the preclinical data are striking

$ARGX announced Ph1b success in June, along with bullish comments re: functional benefit

Those data, disclosed yesterday, fail to match the description. Selective disclosure & perplexing development decisions - atypical for this company / team - further muddy the water

It all feels shockingly non-Argenx, and I’m not sure what to make of it

This. Is. What. Makes. Biotech. Great!

“Regeneron’s relentless pursuit of science and use of proprietary technologies to improve the lives of people with debilitating and life-threatening diseases, no matter their prevalence.” https://t.co/RPDcWqBcvX

Why Corporate VCs Just Took Over Biotech Funding

Crossovers left. Corporates stepped in.

Now they’re not just sprinkling checks, they’re leading rounds, shaping trial endpoints, and pre-wiring the M&A path.

Know your audience. If you’re raising, you’re not selling “platform optionality.” You’re selling a pipeline gap filler on a corporate’s 2028 LoE slide.

Fundable today = fast human data that aligns to a buyer’s P&L.

Not “possible,” not “innovative,” but acquirable.

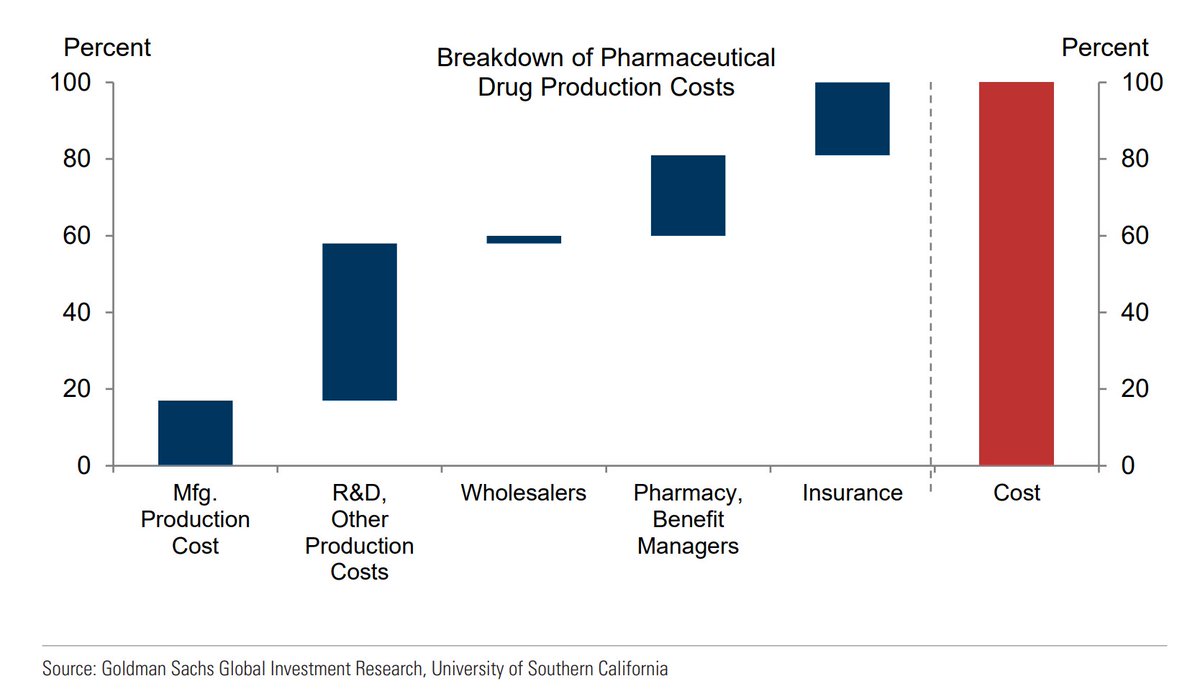

Per @GoldmanSachs, pharmacy benefit managers account for a fifth of the cost of producing drugs in the U.S.

That's a lot of added cost thanks to some easily removed middlemen!

During biotech’s retrenchment, the shift toward validated and/or “hot” targets has been palpable

Two recent reports nicely visualize this trend of increasing competitive intensity, as well as its influence across the full life cycle of asset development $XBI $BBC

The race to reset autoimmune diseases https://t.co/QPKFw21JPV

This new article analyses the characteristics of drugs in development that aim to reset the immune system to treat autoimmune diseases, such as CAR-T cells that deplete B cells, and key trends in the field

ACT-EARLY is worth watching, not only for ATTR but for genetic diseases writ large $BBIO

Prophylactic therapeutic intervention in genetically-confirmed patients with the goal of delaying clinical diagnosis

Creative and interesting model that could be replicated elsewhere

People are crazy to do these trades - People should have expected problematic $BMY Camzyos data based on the MAVERICK-nHCM trial - Different from REDWOOD Cohort 4 in Afi - if anything - IF $CYTK Afi wins in nHCM - in any way - just being stats sign w/ KCCQ - would be all by itself - .. $EWTX nHCM data got the black marks w/ Afib concerns..