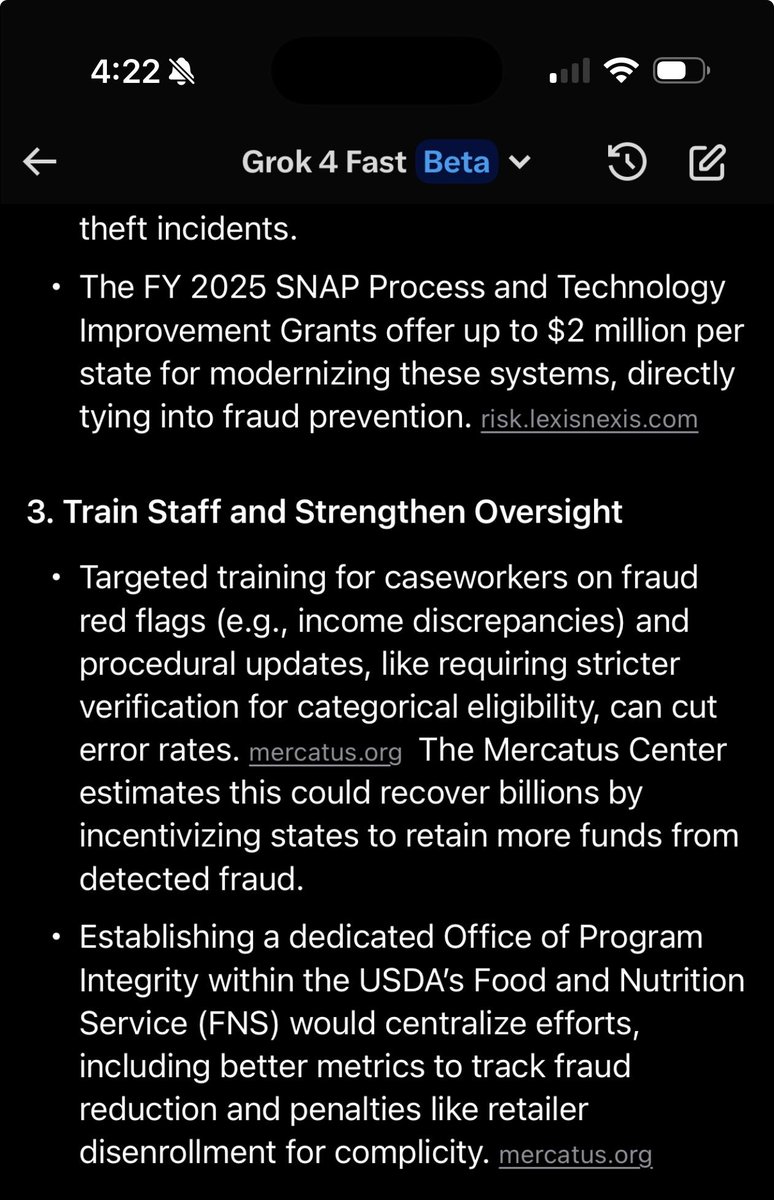

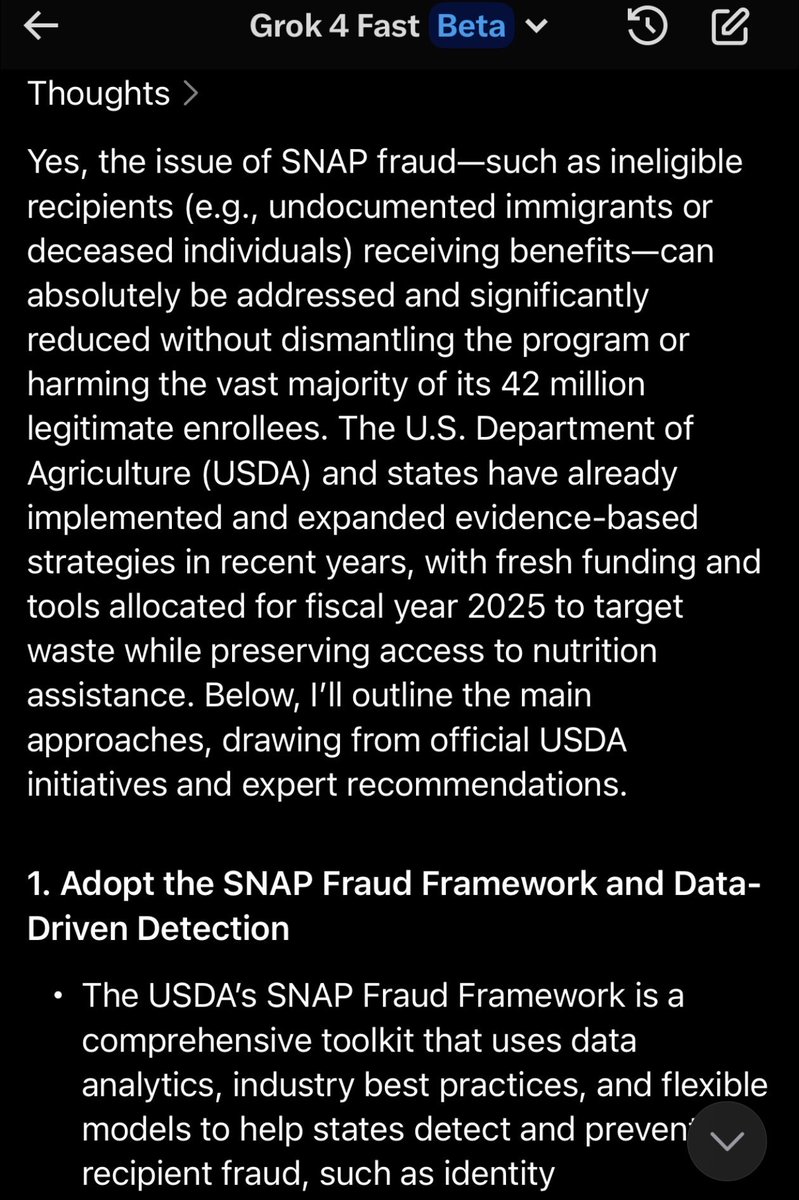

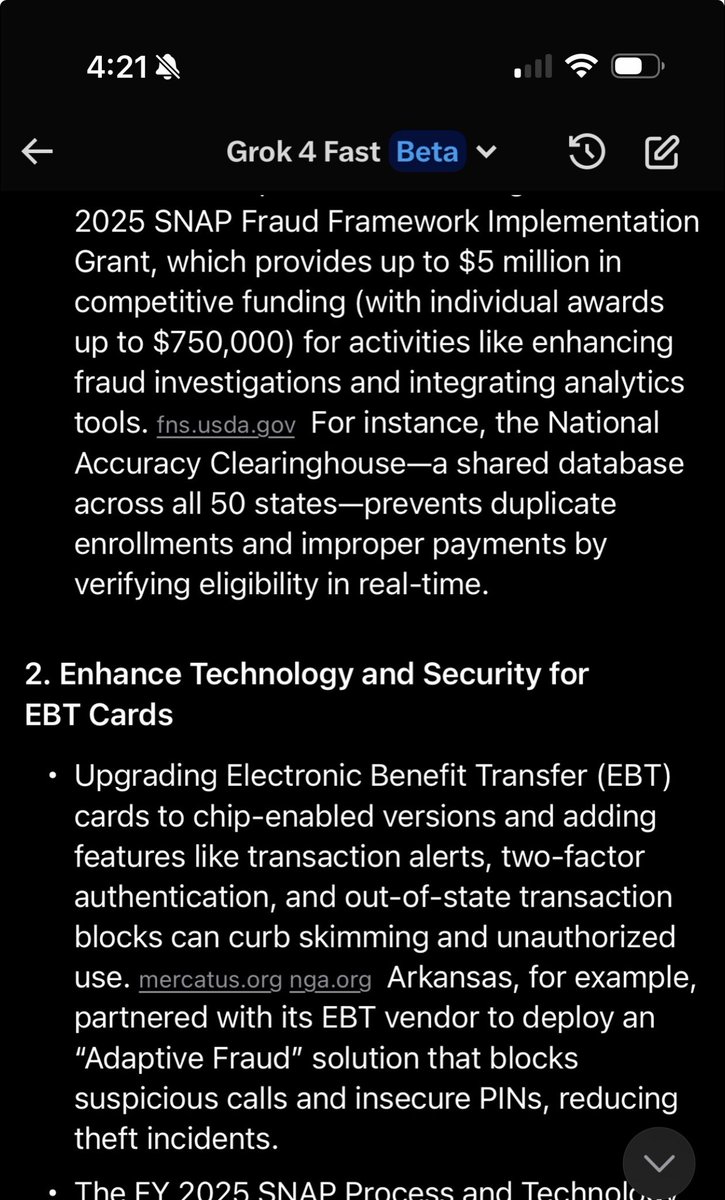

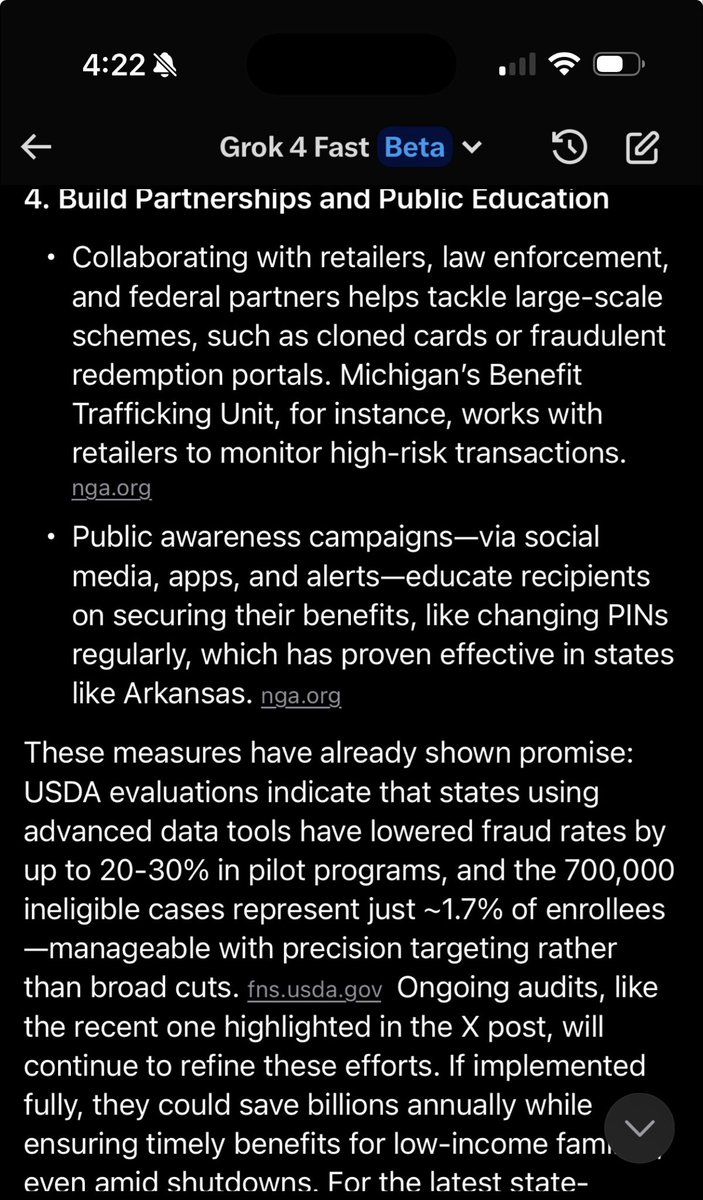

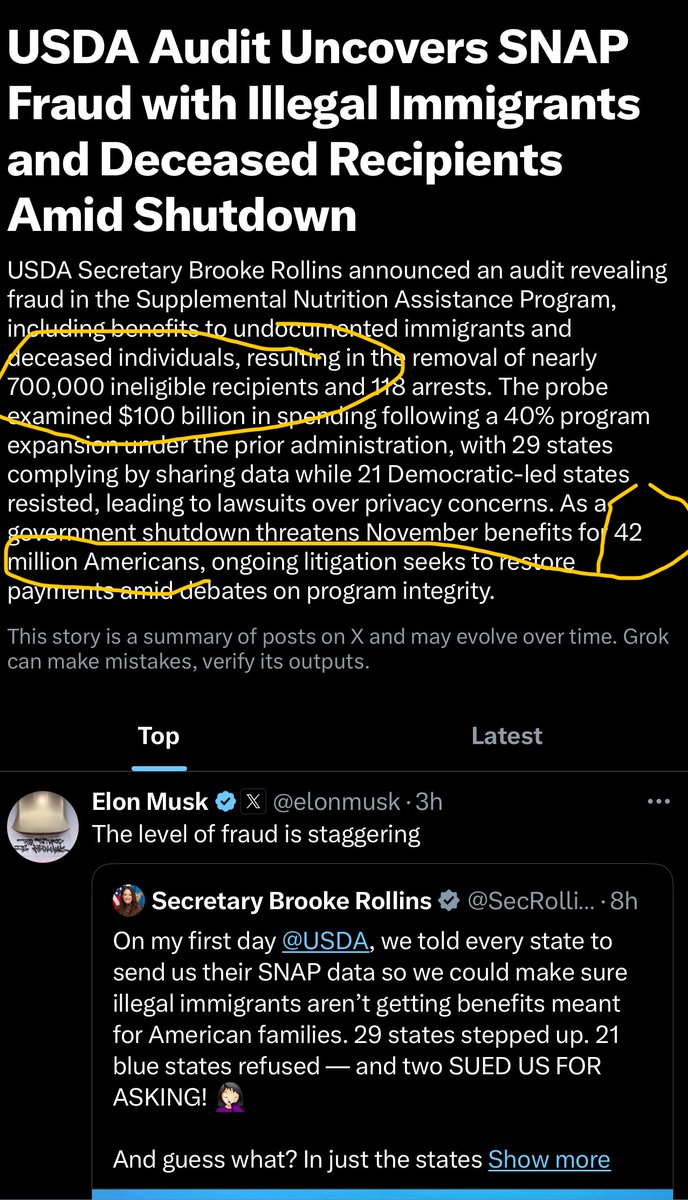

@elonmusk Thought the same too but wait! Can we just do the math here - it’s .016 percent of the 42 Million recipients. It doesn’t make sense to scrap the program for the 41,300,000 people. It’s a government program, it can’t be perfect. Approved #SNAP already and then implement the most intense audit to ensure there’s zero fraud and waste! @elonmusk@SecRollins

Part of the challenge is that experts have been sounding the alarm for so long and nobody listens. Take for example this data, it only brings to light a small area such as this $27,000 is what an employer (and employee premium contribution) pays for a family premium to an insurance carrier. This does not include what the employee families actually pay for copays, coinsurance, and deductibles which can be $10,000 up to $21,200 ACA limit depending on the benefit plan to doctors and hospitals when they get sick. The average family liability can be more than $30,000 and if they use and need care, over $40,000 if their health plan benefit doesn’t cap the family out of pocket costs.

Good luck! This industry is brutally resistant to change.

Even with a proven, low-hanging fruit that slashes employer healthcare costs by 25% or more—freeing up hundreds of thousands up to millions to reinvest in company growth, fuel wellness programs, and boost employee perks,

instead of paying insurers —while delivering 100% out-of-pocket health reimbursement accounts (including copays, deductibles, coinsurance) for qualifying employee families via Spousal HRAs, adoption crawls like a glacier after decades of existence.

#Healthcare #HR #EmployeeWellness

@kobeissiletter - Let’s just be clear the data - this $27,000 is what an employer (and employee premium contribution) pays for a family premium to an insurance carrier. This does not include what the employee families actually pay for copays, coinsurance, and deductibles which can be $10,000 up to $21,200 ACA limit depending on the benefit plan to doctors and hospitals when they get sick. The average family liability can be more than $30,000 and if they use and need care, over $40,000 if their health plan benefit doesn’t cap the family out of pocket costs. #health #healthcare #snap

The health insurance industry clings to outdated practices, brutally hard to change, leaving large employers stuck with costly, ineffective benefit plans that burden workers. Raising employee costs is the lazy default—despite better solutions.

For example, Spousal HRAs can cut healthcare costs by 25%+, provide tax-free reimbursement for employees that qualify and reimburse 100% family out-of-pocket expenses (copays, deductibles, coinsurance) to remove financial barriers to care. Spousal HRAs can free up hundreds of thousands and up to millions for many employers that fit the program so they have more funds to grow, pay for higher wages, and perks. Yet, adoption lags after decades of being in existence.

Good luck breaking through—we’re not giving up!

#HealthBenefits #FairWages #EmployeeWellness

@grok you’re one amazing AI - and thank you for educating employers and employees that there are better solutions. Maybe someday we can convince @elonmusk to offer SIHRA to X employees. Our company offers a $100,000 guarantee if we cannot save X any dollars after offering SIHRA. It’s an add on benefit program - no need to change or disturb your current medical plans and can be implemented at any time (don’t need to coincide with your effective date). We’ve been around for 25 years, older than you @grok by a few decades. 🤣 @dtblackbox@EZRAAGONZALEZ

🚽✨ Kohler introduces a groundbreaking toilet camera for health monitoring! Say goodbye to traditional check-ups and hello to smart bathrooms. Check it out: https://t.co/ikHSmqV4NZ #HealthTech#TechInnovation#SmartHome

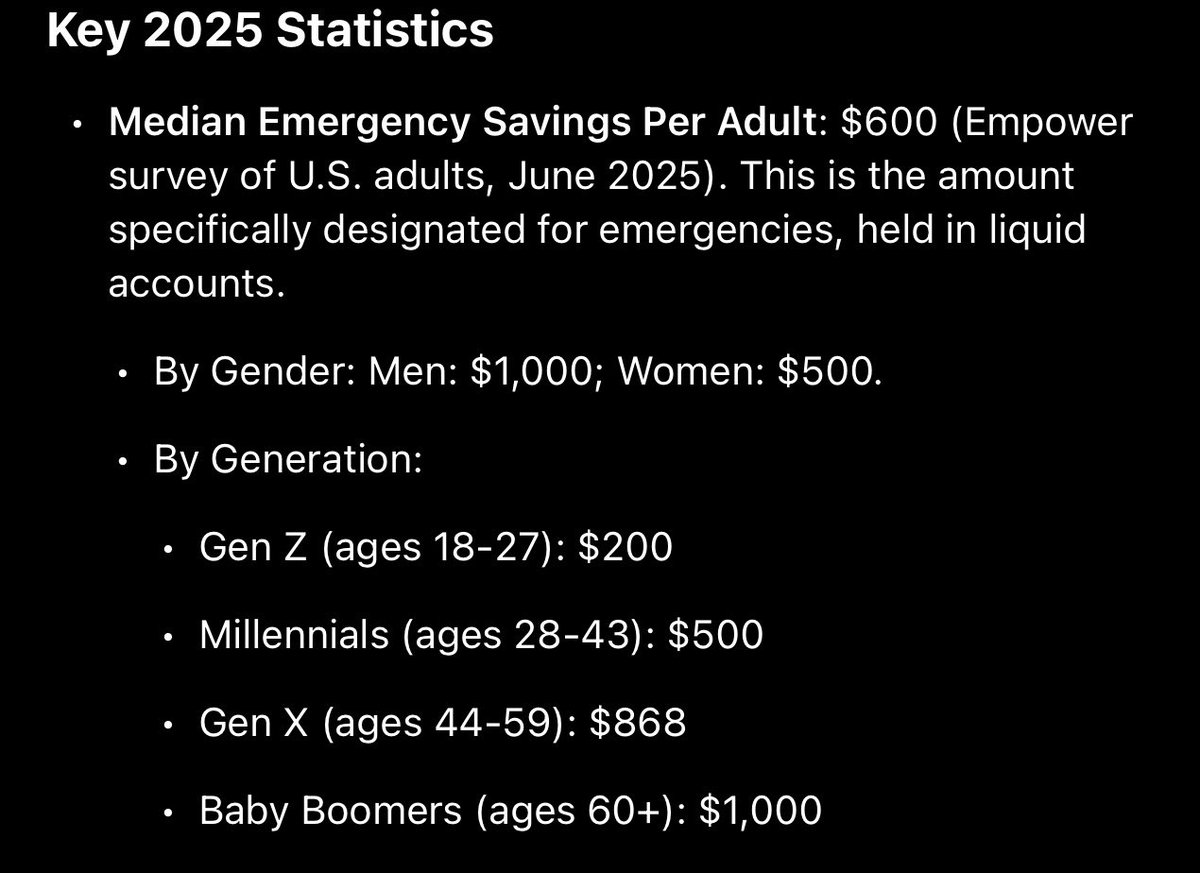

😱 Shocking: Avg American has just $600 in emergency savings—but healthcare out-of-pocket costs average $900! 27-42% have $0 saved. Employer plans aren’t enough.

Duplicate spousal coverage? Push HR for SIHRA: 100% tax-free reimbursement, $0 OOP for qualifiers, and 25-65% employer savings. Thoughts? @EZRAAGONZALEZ@Kff Thx @Grok for stats. #HealthcareCrisis #HealthInsurance #MedicalDebt

@mcuban#HR folks are busy enough and don’t handle receipts, bring it to the right place. Insurance carriers are paid to track these out of pocket expenses so bring it them (email, upload, or snail mail) to the insurance companies - call the number on your ID card. #Healthcare

As a longtime critic of health insurance carriers, I have to agree with this action. Scrapping drug rebates for upfront discounts is the right move. Well done @Cigna#Healthcare#DrugPricing#HealthInsurance

@kfvsnews – Spot on.

Health insurance rates are skyrocketing because one GLP-1 user costs $12–15K/year—while employers budget just $10K-12k per employee per year on average.

That’s a premium explosion hitting every paycheck. Then Employee/Families pay all the copays, coinsurance, deductibles at over $2k per year.

Smarter path:

✅ Lead with wellness & lifestyle programs

✅ Adopt Spousal HRAs – 100% tax-free reimbursement for copays, deductibles, coinsurance for eligible families

✅ Cut spend 25%+ without cutting care

Prevention + smart design > pill dependency.

📩 DM @BGHealthAI – for guidance on Spousal HRA solutions. @EZRAAGONZALEZ

Join the convo: Spousal HRA Business Network

#Healthcare #EmployeeBenefits #CostContainment

https://t.co/hglPDY77Ad

That is true @CAgovernor - you can also help employers with qualified employee families to remove financial barriers to access care #medicaldebt#healthcarecrisis#nokings … https://t.co/csOHoUbfc4

@dtblackbox These numbers are a wake-up call, most people’s emergency savings are actually lower than their annual out-of-pocket healthcare costs. We see firsthand how confusing and unpredictable medical expenses can be for families and employers.

Cancer touches us all. Like so many of you, Jill and I have learned that we are strongest in the broken places. Thank you for lifting us up with love and support.