Capital Formation at @GammaPrime_Com and @TokenizedSummit

Deep dives into #RWA, #tokenization & #institutional crypto

Follow for insights on $30B+ market

When the screen says "Yat Siu Fireside Chat" and the room is wall-to-wall family offices + billion-dollar funds...

Tokenized Capital Summit Hong Kong looked exactly like this.

The future of capital is tokenized - and it's happening now.

See you this April at the next Tokenized Capital Summit in Dubai.

The man who built his fortune selling £5 football shirts just bid €2 billion for Hugo Boss.

Hugo Boss shares jumped 7%. Analysts aren't sure he actually wants to buy it.

Mike Ashley's Frasers Group - the UK retail empire behind Sports Direct, House of Fraser, and Flannels - launched a voluntary takeover offer for the rest of Hugo Boss yesterday. The German fashion house that defined the executive suit for a generation is now the target of a discount sports retailer.

On paper, the pairing makes no sense. Sports Direct sells trainers in bins. Hugo Boss sells €600 suits.

But Frasers didn't arrive yesterday. The group already owns 26.06% of Hugo Boss - its largest shareholder, built up over years of quiet accumulation through shares and derivatives. Ashley has been sitting inside the register, watching the company struggle, waiting.

And Hugo Boss is struggling. A December profit warning sent the stock down 11% in a day. Shares fell from above €52 in late 2024 to a low of €33.85 in January. The company itself forecasts declining sales for 2026 as it works through a brand reset. Boss lives in the most dangerous part of the fashion market: too expensive for the mass consumer, not exclusive enough for the luxury one.

That's what makes the timing interesting. This is a bid for a globally recognized brand at a cyclical low, from a buyer who already knows the register, the board, and the business - and who built his entire career buying distressed retail assets nobody else wanted.

And here's the twist analysts are debating: the offer may not be about owning Hugo Boss at all.

A voluntary takeover bid at a modest premium does several things short of full acquisition. It pressures the board. It flushes out other potential buyers. It forces a strategic conversation that a 26% shareholder can't force alone. If someone outbids him, Ashley's existing stake appreciates. If nobody does, he buys a global brand at a discount.

Heads he wins. Tails he wins slightly less.

Whatever the intent, the message to the market is the same one Ashley has been sending for thirty years.

When everyone else is afraid of retail, that's exactly when he buys it.

Partners Group capped withdrawals on $8.6 billion on June 3. Stock dropped 17%.

The structural issue isn't Partners Group. It's the semi-liquid PE category itself.

I work in capital formation in tokenized private markets. The marketing pitch for semi-liquid funds promised two things at once: returns like the biggest institutional PE funds, plus the ability to get your money out every quarter.

The promise only works as long as nobody actually needs to get out.

Quarterly liquidity isn't actual liquidity. It's a contractual right to request redemption - subject to fund-level gates, side-pocket discretion, and whatever the underlying portfolio can generate in cash. In normal conditions, the gates never get pulled. The category functions and feels indistinguishable from a liquid fund.

The gates get pulled when too many LPs want out at the same time.

That's what just happened. Partners Group's Global Value SICAV is now operating under a 5%-per-quarter cap. Twenty quarters to fully exit. Five years.

None of this is fraud. The terms were in the prospectus. The fund is operating exactly as written. What's exposed is the gap between what investors were told they were buying and what they were actually buying.

The alternative the industry is now circling is structural, not marketing. Vehicles where LP positions can transfer between investors directly, without the manager needing to gate the fund. Tokenized infrastructure makes that mechanically easier - but the binding constraint isn't technology. It's secondary demand.

This week's news is the kind of event that moves "tokenization" from a slide in a pitch deck to a conversation about structural risk.

That's a conversation private markets have been avoiding for a long time.

Partners Group just told $8.6 billion of investors they can't have their money.

The fund will return at most 5% per quarter. That's five years to fully exit.

Their stock dropped 17% today - the worst single-day drop in the company's history.

The Global Value SICAV is Partners Group's flagship semi-liquid private equity vehicle. The pitch to investors - many of them individuals, family offices, and smaller institutions - was access to institutional-quality PE returns with the ability to redeem quarterly. That was the promise. Liquidity when you wanted it. Better-than-public-market returns the rest of the time.

The redemption queue grew faster than the fund could process.

On Wednesday, Partners Group announced a hard cap on withdrawals: 5% of net asset value per quarter, indefinitely. Investors who wanted out are now in a five-year queue. The underlying portfolio hasn't changed. The economics of the assets haven't deteriorated. What changed was the gap between what investors wanted and what the fund could deliver.

The market saw the gate and reacted accordingly. Partners Group dropped 17%. US-listed asset managers selling similar semi-liquid PE products dropped in sympathy.

This is the third major retail-PE stress event of 2026.

In January, BlackRock's TCP Capital cut NAV by 19% in a single quarter. In April, KKR's FSK posted $560 million in losses and watched its stock fall to a 43% discount to book value. Now Partners Group has gone further than either - formally restricting redemptions on a flagship retail-facing vehicle.

The pattern is the same in all three cases. A semi-liquid PE product was sold to investors who behaved like they wanted liquidity. The fund held assets that don't have actual liquidity. When the redemption queue grew, the structural mismatch became visible.

The 5% gate isn't dishonesty. It's the contract working exactly as written.

The problem is that most investors never read that part of the contract carefully.

Semi-liquid funds are not liquid. The "semi" is doing all the work. In normal conditions, the gate never gets pulled and the structure feels indistinguishable from a liquid fund. In stressed conditions, the gate is the entire product.

The industry has spent the last decade telling individual investors that private markets are now accessible to everyone.

This week, $8.6 billion of those investors found out what "accessible" actually means.

The Pentagon is building a 30-person investment banking team inside the Department of Defense.

Its job is to deploy $200 billion into the defense industry over three years.

Democrats just officially called it a national security risk.

The unit is being staffed with bankers from Goldman Sachs, J.P. Morgan, and Bank of America. Its mission is to identify, structure, and execute private equity-style investments in companies critical to US defense capabilities - drone manufacturers, semiconductor fabs, hypersonics startups, shipbuilders. The strategic intent is geopolitical: counter China's state-directed industrial capital with American state-directed industrial capital, channeled through Wall Street talent.

In a letter sent this week, congressional Democrats argued the structure creates conflicts that no agency has been built to manage. The Pentagon would be acting as buyer, investor, and customer simultaneously - selecting the companies it invests in, the deals it structures, and the contracts it later awards. The same officials who decide which startups receive equity investments would also decide which startups receive procurement dollars.

"Private equity's involvement in our nation's defense infrastructure poses significant risks to our national security and taxpayers."

That's the political problem. The structural problem is bigger.

Private equity, at its core, is a model for unlocking value in fragmented, undermanaged industries. The defense sector has been neither fragmented nor undermanaged. It's been concentrated among a handful of prime contractors, governed by procurement rules built specifically to prevent the kind of opportunistic capital reallocation that PE practices in commercial markets. The whole premise of defense procurement is that capital allocation is supposed to be slow, scrutinized, and politically accountable.

The Pentagon's new unit reverses that premise.

It treats defense as another sector where capital can be deployed at scale, by professionals, against returns. It assumes that the speed and flexibility of private equity will produce better outcomes than the legacy procurement system. And it assumes that the agency can structurally separate the people doing the investing from the people doing the buying - even when they sit inside the same building.

That separation hasn't been built yet. The unit hasn't deployed its first dollar yet.

But the precedent is being set right now.

The largest customer of the US defense industrial base is about to become its largest investor.

That has never happened in modern American capitalism.

The most successful PE strategy of 2026 isn't a mega-buyout.

It's buying your neighborhood plumber.

In July 2019, Alpine Investors launched Apex Service Partners with a commitment to deploy at least $100 million of equity into founder-owned HVAC, plumbing, and electrical businesses across the United States.

Seven years later, Apex operates 107 brands, generates $1.3 billion in revenue, and is now being valued at $10 billion in a minority stake sale.

A single-asset roll-up from $100 million committed to a $10 billion valuation in seven years.

This is not the story most people associate with private equity.

There are no leveraged megadeals. No celebrity boardrooms. No iconic brands taken private. Apex bought local HVAC companies - the people who fix your air conditioner when it breaks in August. Plumbing companies. Electrical contractors. Family businesses that had operated for decades, often run by founders looking to retire without selling to a competitor down the street.

Alpine's thesis was simple and patient.

Residential services are recession-resistant, geographically fragmented, and structurally underinvested in operations. Most owners are skilled tradespeople, not professional managers. A single roll-up with shared back-office, technology, recruiting, and capital access can outperform any individual operator. The fragmentation never ends - there's always another local HVAC company to buy.

In 2023, Alpine moved Apex into a single-asset continuation vehicle at a $3.4 billion valuation. Three years later, that valuation has roughly tripled.

The math works because nobody else wants to do the work.

Buying 107 small businesses is harder than buying one large one. Integrating them is harder still. Building back-office systems for a national HVAC roll-up isn't glamorous. The press never writes about it. The conferences don't celebrate it.

But the returns compound.

A $100 million commitment in 2019 backing a national plumber roll-up just produced one of the cleanest PE outcomes of this cycle.

The biggest opportunities aren't always the biggest deals.

Manhattan's top prosecutor is now investigating BlackRock.

The question: how did a private credit fund go from "fully valued" to a 19% writedown in two months.

BlackRock TCP Capital Corp - ticker TCPC - is a publicly listed business development company managed by the world's largest asset manager. It lends to middle-market companies that can't access public bond markets. The kind of loans that don't trade. The kind of loans whose value depends entirely on how the fund itself decides to mark them.

In November 2025, TCPC reported its portfolio at full value. No material markdowns. No warning of stress.

On January 23, 2026, the fund disclosed a 19% reduction in net asset value. A string of troubled loans had caught up with it. The stock dropped 14% in the following days. Investors filed a class action lawsuit accusing BlackRock of overstating NAV. And the US Attorney's Office for the Southern District of New York - Wall Street's most aggressive federal prosecutor - opened an investigation into the fund's valuation practices.

The question prosecutors are asking is narrow but consequential.

Did BlackRock know what the loans were really worth before disclosing the markdown? And if they did, when?

This isn't an abstract issue. BDCs and private credit funds hold over $1.8 trillion in loans that don't have public market prices. The value of those loans is determined by the managers themselves, subject to auditor review. Investors - institutions and retail - rely on those marks to be honest. If markdowns are delayed, the fund looks healthier than it is. Yields look stable. New money flows in. Existing investors don't redeem. The system functions on trust in the marks.

When KKR's FSK lost $560 million last quarter, the conversation was about credit quality. When BlackRock's TCPC went from full value to a 19% writedown in two months, the conversation became about the marks themselves.

Federal prosecutors don't open valuation investigations because something is unfortunate.

They open them when they suspect something was hidden.

The same private credit industry that spent the last decade telling investors it was the safer alternative is now being asked, by Manhattan's top prosecutor, to explain its math.

KKR didn't buy a sports team.

They bought the firm that owns stakes in dozens of them.

For up to $1.95 billion, KKR acquired Arctos Partners - the largest institutional investor in professional sports franchise stakes in the world. Arctos manages $15 billion across minority positions in teams across the National Basketball Association (NBA), National Football League (NFL), Major League Baseball (MLB), National Hockey League (NHL), and MLS.

The deal closed yesterday.

For decades, American sports leagues kept private equity out. Team ownership was reserved for individuals, families, and the occasional corporation. Rules limited who could hold stakes and how. The leagues understood something Wall Street didn't yet: a sports franchise isn't a normal business. It's a cultural asset with a community attached.

Then the math changed.

Franchise valuations doubled, then tripled. The Dallas Cowboys are worth $13 billion. The Los Angeles Lakers, $10 billion. The Boston Red Sox, $5 billion. Founding families needed liquidity. New owners couldn't afford full purchases at these multiples. Someone needed to write checks for minority stakes - and write them quietly.

Arctos was the answer. The leagues opened a side door. PE could now own up to 30% of a team in some leagues, 10% in the NFL - all capped per fund, all with restrictions on control. Arctos became the dominant player in that new market - building a portfolio across the major leagues that no single buyer could replicate.

KKR didn't want to compete with that. They bought it.

The acquisition gives KKR instant exposure to the most valuable consumer asset class of the 2020s. Sports franchises have outperformed almost every other private market category over the last decade. Their revenue is contractually locked in for years through media rights deals. Their valuations have a floor that public companies don't - leagues won't let a franchise go bankrupt, and the supply is fixed.

This isn't a buyout. It's an entry ticket.

KKR now sits inside a portfolio of stakes in teams that millions of Americans care about more than they care about most public companies. Every Sunday game, every playoff run, every championship - KKR has a position in it.

Private equity wanted into American sports for years. The leagues finally let them in.

KKR just bought the firm that walked through the door first.

In 2007, KKR, TPG, and Goldman Sachs spent $45 billion buying a Texas power company.

They borrowed $40 billion of it.

Seven years later, it became the largest private equity bankruptcy in history.

Fracking destroyed it.

TXU Energy was the biggest electricity generator in Texas. The thesis was straightforward: natural gas prices were rising. TXU generated most of its power from coal - cheap. Competitors used natural gas - expensive. The wider the gap between the two, the bigger TXU's margins. Three of the smartest firms in private equity agreed to pay $45 billion.

The deal closed in October 2007. It was the largest leveraged buyout in history at the time - a record that still stands. The renamed entity, Energy Future Holdings, carried debt equal to more than 100% of its prior-year revenue. The thesis didn't need everything to go right. It only needed natural gas prices to keep rising.

Then fracking happened.

Hydraulic fracturing technology, developed in the same Texas oil fields, unlocked vast reserves of cheap natural gas across the United States. Gas prices collapsed. The cost advantage TXU was supposed to enjoy disappeared - not slowly, but in a matter of years. By 2012, the company was warning of bankruptcy. By April 2014, it filed.

The $8.3 billion in equity that KKR, TPG, and Goldman Sachs put into the deal was wiped out.

Warren Buffett wasn't an equity investor. He bought $2 billion of Energy Future Holdings bonds. Berkshire Hathaway lost more than $870 million on them. Buffett later called it "a major unforced error."

What made TXU different from other PE collapses isn't the leverage. It's the cause.

Toys"R"Us R Us was killed by Amazon - a competitor in the same industry. Red Lobster was killed by its own promotions. Hertz, Sears, and dozens of other PE-backed failures had visible problems that operators could have anticipated.

TXU was killed by a technology developed in an entirely different industry. The thesis was a bet on commodity prices. Those prices were upended by an innovation no one in the deal room was modeling.

The smartest firms in private equity made a $45 billion bet on a future where natural gas stayed expensive.

A different industry made gas cheap instead.

The most dangerous risk is the one outside your spreadsheet.

Four weeks ago, Intertek's board rejected an $11 billion buyout from EQT Group as "fundamentally undervalues the company."

They rejected three more bids after that.

EQT just won them at $12.7 billion.

The board was right.

On April 16, EQT made its first approach at £7.93 billion - £51.50 per share. Intertek said no. Stock jumped 12% on the rejection. The market signaled the company was worth more than the bid.

EQT came back with a second offer. Intertek rejected it. EQT came back with a third - £8.93 billion. Rejected that too. On May 11, EQT submitted what it called a "final" proposal. The board didn't accept. Two days later, EQT raised again to £9.4 billion - roughly $12.7 billion. £60 per share plus a £1.10 dividend.

The board agreed to recommend it.

Four weeks. Five bids. A 19% increase in equity value from the first offer to the last. Intertek shareholders captured an additional £1.47 billion because the board held the line.

This is what a rejected bid is supposed to do.

In most takeover stories, the headline is the price. The real story is the negotiation between it. Boards that fold early leave value on the table. Boards that hold create it.

EQT wanted Intertek because the testing and inspection industry has the qualities private equity loves - predictable revenues, recurring contracts, low cyclicality, fragmented competition that can be rolled up. That thesis was true at £7.93 billion. It was still true at £9.4 billion. EQT was always going to pay what it needed to pay.

The board's job was to find out what that number actually was.

They did.

In PE, the first offer is rarely the last.

Sometimes it isn't even close.

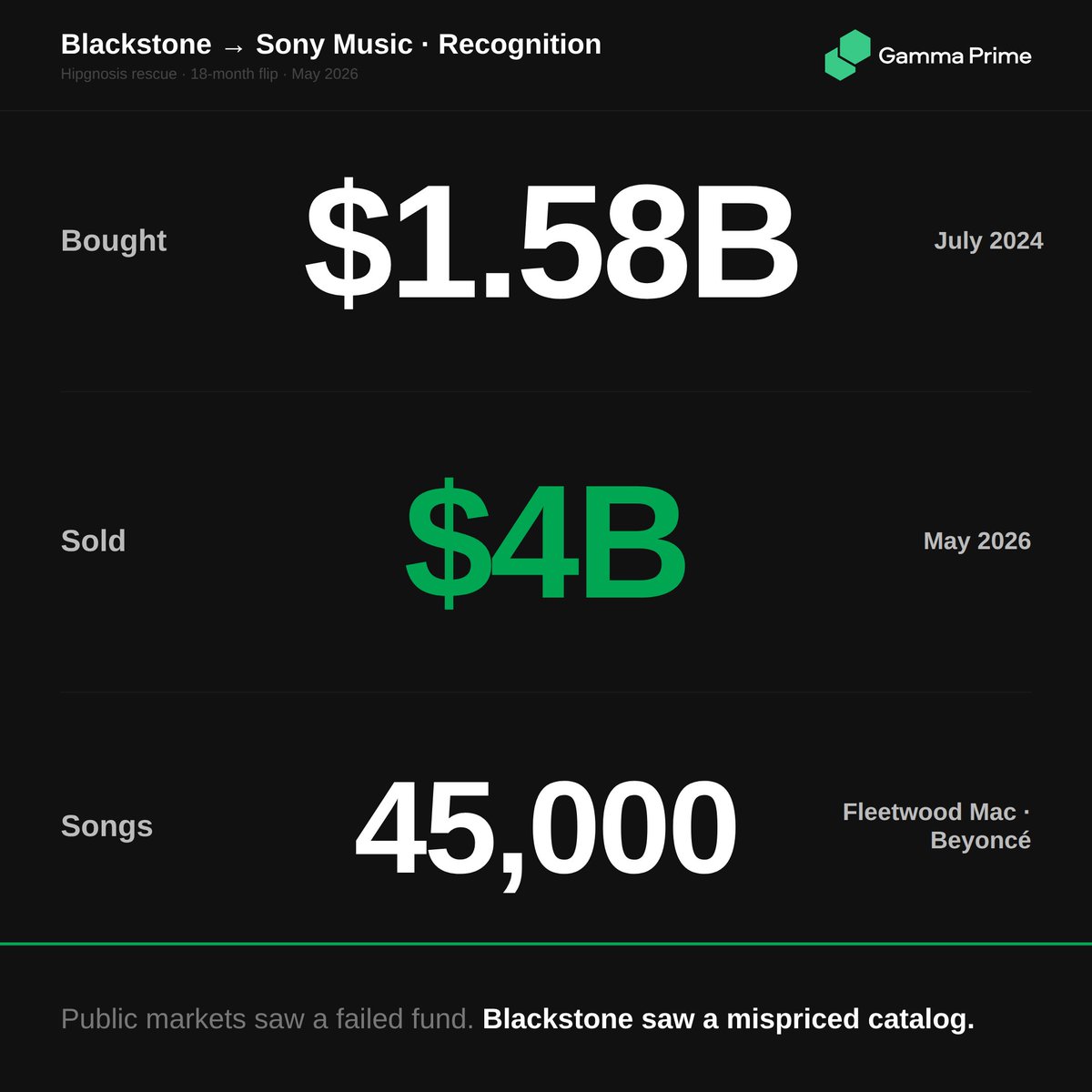

In 2024, Hipgnosis Songs Fund was a disaster - collapsed share price, activist revolt, board forced to sell.

Blackstone bought it for $1.58 billion.

Eighteen months later, they're selling it to Sony for $4 billion.

The rebranded entity - Recognition Music Group - holds rights to over 45,000 songs, including catalogs from Fleetwood Mac, Beyoncé, Shakira, and Justin Bieber. Sony Music Publishing announced the acquisition this week.

Blackstone's all-in cost across the Hipgnosis assets, including earlier acquisitions through Hipgnosis Songs Capital, was around $3 billion. The exit lands at $4 billion. Roughly a billion in gains, in a window when most PE assets are stuck waiting for distributions.

Here's what made the trade work.

Public markets had given up on music rights as an asset class. Royalty income looked unpredictable. Streaming economics looked compressed. Hipgnosis's accounting was being challenged. The stock traded at a deep discount to NAV - sometimes 30%+ below the value of the underlying songs. Buying from a distressed public seller at a discount to private market comparables created instant arbitrage.

Then Blackstone did three things public Hipgnosis couldn't do.

It took the portfolio private - removing the quarterly NAV scrutiny that had been compressing the share price. It rebranded - separating the assets from the Hipgnosis reputation that had become its own headwind. And it waited - long enough for streaming royalty data to stabilize and for strategic buyers like Sony to value catalog ownership at premium multiples again.

This is what private capital is supposed to do. Buy assets the public market is mispricing, fix the structural problems that caused the mispricing, and sell to a strategic acquirer who values the cash flows differently.

Public markets saw a failed fund.

Blackstone saw a mispriced catalog.

The difference was a billion dollars.

KKR's largest private-credit fund just lost $560 million in one quarter.

The fund is held mostly by individual investors.

FS KKR Capital - ticker FSK - is the flagship retail-facing vehicle of KKR's $200 billion-plus credit platform. A publicly listed BDC marketed to ordinary investors as a way to access "institutional-grade private credit." Higher yields than bonds. Smoother than stocks. Backed by one of the most respected names in finance.

Last week, the numbers came out.

$560 million in losses. Net asset value per share dropped 9.9% in a single quarter - from $20.89 to $18.83. Non-accrual loans inside the portfolio reached 8.1% at cost. That means roughly one in twelve dollars the fund lent out is no longer paying interest as expected.

Then it got worse.

A J.P. Morgan-led bank group reined in the fund's credit line, citing rising defaults. KKR announced a $150 million tender offer at $11 per share and a $300 million share repurchase program - capital deployed to stabilize the price.

The market wasn't convinced.

FSK now trades around $10.80 against an $18.83 NAV. That's 0.57× book value - a 43% discount. Translation: the market thinks the underlying loans are worth nowhere near what FSK has them marked at.

That gap is what matters. BDCs hold loans that don't trade in liquid markets. When defaults rise, the fund can't quietly exit positions - the losses get absorbed and the discount to NAV widens.

For an institutional LP with a 10-year horizon, that's noise. For a retiree who put money into FSK looking for stable monthly income, that's a different conversation

Private credit was sold as the safer alternative.

It was never as safe as it sounded.

Red Lobster is bringing back Endless Shrimp.

The promotion that bankrupted them.

In 2014, Golden Gate Capital bought Red Lobster for $2.1 billion. Within months, they executed one of the most aggressive moves in PE restaurant history: they sold off the company's real estate - the land and buildings underneath its restaurants - for $1.5 billion.

On paper, brilliant. Golden Gate recovered almost three-quarters of its investment in a single transaction. But Red Lobster now had to pay rent on property it used to own. Lease payments became a permanent line item. The balance sheet looked cleaner. The P&L took the hit forever.

Then came the shrimp.

In 2023, under Thai Union ownership, Red Lobster made the $20 Ultimate Endless Shrimp a permanent menu item. It cost the company $11 million in a single quarter. Customers ordered more shrimp than the unit economics could survive.

By May 2024, Red Lobster filed for Chapter 11. 550 restaurants. Hundreds of millions in annual lease obligations stacked against shrinking margins.

Now under new ownership and new CEO Damola Adamolekun, Red Lobster is doing one thing: running it back.

Same promotion. Same price pressure. Same menu line that put the company in bankruptcy court eighteen months ago.

The sale-leaseback is still in place. The leases didn't disappear in bankruptcy - they were restructured, but the rent continues. A casual dining chain with thin margins, structural lease costs, and a loss-leading hero product is running the exact playbook that failed last time.

Private equity built the trap. The new owners inherited it. The shrimp is coming back anyway.

The leases don't forgive repeat offenders.

A Qatari royal-backed fund just bid $1.5 billion for Papa Johns.

Pizza is now a sovereign wealth play.

Irth Capital Management LP - founded in 2024 by Sheikh Mohamed bin Abdulla Al Thani, a member of Qatar's royal family - offered $47 per share to take Papa John's private. The board is still evaluating.

Papa John's is not alone.

Pizza Hut's parent, Yum! Brands, announced a strategic review last November. 20,000 locations worldwide. US sales down 5% in 2025. Another 250 stores closing this year. They are actively looking for a buyer.

Two of the four largest pizza chains in America. Both up for sale. At the same time.

This is what the end of a business model looks like.

Uber Eats and DoorDash rewrote the economics of pizza. Consumers stopped walking into Pizza Hut. Delivery became a third-party product with third-party margins. Little Caesars and Domino's won the value segment. Gen Z ordered something else entirely.

Public markets priced it in. Same-store sales declined. Stocks drifted. Quarterly earnings calls became exercises in defending yesterday's model.

Private equity sees something different. Iconic brands. Distressed valuations. Real estate. Franchise networks that still print cash if you restructure the cost base. The kind of situation where going private is the only way to fix things without Wall Street watching every quarter.

The Qatari fund is one bid. More are coming.

When sovereign wealth and private equity start competing for the same American institutions, the question isn't whether they'll be taken private.

It's who ends up owning them.

Wall Street banks spent the last decade funding private credit.

Now they're betting against it.

J.P. Morgan, Barclays, Morgan Stanley, and Citi have started trading credit default swaps tied to flagship funds run by Blackstone, Apollo Global Management, Inc., and Ares Management. These are insurance contracts against defaults - the same instruments that became famous in 2008 when banks used them to bet against the mortgage market.

Private credit is a $2 trillion industry. It grew from almost nothing fifteen years ago into one of the dominant forces in institutional finance. The pitch was simple: higher yields than public bonds, lower volatility than stocks, predictable cash flows. Pension funds, sovereign wealth funds, and family offices poured in.

In Q1 2026, $20.8 billion was pulled out.

The redemption wave is forcing private credit funds to sell assets into a thin market. When you have to sell and there are few buyers, prices fall. The CDS market is Wall Street's way of pricing that risk - and profiting from it.

Here's the uncomfortable part.

The same banks now selling protection against Blackstone and Apollo are the same banks that arranged billions in loans for private credit deals. They built the market. Now some of them are hedging against it.

This isn't 2008. Private credit funds don't have the same leverage or interconnectedness as mortgage-backed securities. But the emergence of a derivatives market designed to bet on private credit stress is a signal worth watching.

When Wall Street starts building tools to short something, it usually means they see risk the rest of the market hasn't priced in yet.

EQT Group offered $11 billion for Intertek.

The board said no.

The stock went up 12%.

Intertek is not a name most people know. But every product you buy - electronics, food, clothing, construction materials - has almost certainly been tested by a company like Intertek before it reached you. They verify that products are safe, compliant, and what they claim to be.

45,000 employees. Operations in 100 countries. FTSE 100.

EQT, one of Europe's largest private equity firms, made an unsolicited approach last week. The offer valued Intertek at £7.9 billion. The board rejected it in three words: "fundamentally undervalues Intertek."

The market agreed. Shares jumped 12% on the news - not because a deal was announced, but because a deal was rejected.

That's the signal. When a stock rises on a rejected bid, it means investors believe the company is worth more than the buyer was willing to pay. The bid itself becomes a price anchor - and the market moves above it.

Intertek also announced plans to split the business into two separate entities to unlock value. The message to EQT was clear: we'll create more value ourselves than you'd create for us.

EQT said it's still exploring options.

So is Intertek.

Netflix walked away from an $83 billion deal.

Warner Bros. Discovery paid them $2.8 billion for it.

Netflix just reported its best earnings quarter in years - and the company that outbid them helped pay for it.

Q1 2026: $12.25 billion in revenue. EPS up 86% year over year. The numbers weren't just good. They were exceptional. And buried inside them was a $2.8 billion termination fee from Warner Bros. Discovery - payment for the deal Netflix agreed to walk away from.

Paramount outbid Netflix for Warner Bros. Warner's board chose the lower offer. Netflix got a check.

That check landed in Q1 earnings.

But the market didn't care about the past. It cared about the future.

Netflix guided Q2 profit below Wall Street expectations. The termination fee was a one-time item - it won't repeat. Without it, the underlying business looks like a slower-growth company raising prices in a world where consumers are increasingly price-sensitive.

The stock dropped 9% after hours. Reed Hastings - the co-founder who built Netflix from a DVD rental service into the world's dominant streaming platform - announced he is stepping down from the board.

One quarter. Record profit. Founder exits. Stock falls.

Wall Street is always looking one quarter ahead.

Private equity bought Toys"R"Us.

Loaded it with $5 billion in debt.

Then Amazon arrived.

In 2005, KKR, Bain Capital, and Vornado Realty Trust paid $6.6 billion to take Toys R Us private. They put in $1.3 billion of their own money and borrowed the rest. The company inherited $5.3 billion in debt on day one.

Toys R Us controlled 20% of the US toy market. The thesis made sense. Stable cash flows. Dominant brand. A category where parents spend money regardless of the economy.

What the model didn't price in: Amazon.

While Toys R Us was spending $400 million a year just servicing its debt - money that should have gone into stores, inventory systems, and e-commerce - Amazon was building the infrastructure that would make physical toy retail obsolete.

Toys R Us couldn't invest. The debt wouldn't let it.

By 2017 it filed for bankruptcy. The third-largest retail bankruptcy in US history. 33,000 people lost their jobs. The equity investors were wiped out.

But KKR and Bain still collected management fees throughout - millions annually, paid while store conditions deteriorated. The bankruptcy filings showed the receipts.

This wasn't unique to KKR, Bain, or Vornado. This is what leveraged buyouts can do to a business when the debt load exceeds what the company can realistically carry.

The LBO playbook assumes the business can carry the debt.

Sometimes it can't.

And when it can't, the fees have already been collected.