Something good is happening at this World Cup.

The Scots turned up. The English turned up. The Norwegians turned up. They sang their songs, got stuck in, and the Americans loved them for it. Glasgow and Boston are getting twinned off the back of it.

For 30 years we’ve been told to view the US as some sort of Great Satan — all imperialism and orange-man clichés. Not everyone buys it of course, but enough do.

And then Europeans actually go, and find a place that feels familiar. Makes sense to them. A bit richer, a bit further ahead, but recognisably ours. Settled by Europeans, still deeply European in its bones.

There’s a gathering-of-the-clans feeling to it. Old neighbours discovering they still like the same songs, the same drink, the same daft humour, and genuinely enjoying each other’s company.

None of it’s a surprise, really. It’s just been buried under so much politics that we forgot we were allowed to enjoy it.

Good to be reminded.

Five-star prospect John Meredith III, ESPN's No. 1 cornerback in the 2027 class, announced his commitment to Texas on Friday.

Meredith picked the Longhorns over in-state finalist Texas A&M following official visits with both programs in recent weeks. https://t.co/6656M3yba3

🇪🇺Europe runs on 🇺🇸American gas now.

Here's the proof.

In 2017, US LNG was barely a footnote in European energy.

In 2025: 58.4% of ALL European LNG came from America.

In Q1 2026: already 63% and climbing.

The energy map has been completely redrawn in 8 years. Here's what it looks like country by country:

🇩🇪 Germany: 92.4% the country that ran on Russian gas now runs on American LNG

🇬🇷 Greece: 90.0% where Chevron just drilled an exploration block

🇫🇮 Finland: 85.5%

🇳🇱 Netherlands: 75.8% Europe's primary gas trading hub

🇬🇧 UK: 75.6%

🇵🇱 Poland: 72.1% NATO's eastern anchor, fully US-dependent on LNG

This didn't happen by accident.

It happened in 2 waves.

Wave 1 2022: Russia invaded Ukraine. Europe had to find an alternative to 150 bcm of Russian pipeline gas. It found American LNG.

Wave 2 2026: Iran closed Hormuz. Qatar went dark. Middle East gas supply collapsed. Europe doubled down on America.

Q1 2026 is already at 63%. By year-end it could be higher.

Full analysis in my latest article.

Link in the comments 👇

🔥 THE GAS WAR JUST SHIFTED

• United States → n.1 global gas producer

• Russia → constrained

• Iran → geopolitically locked

• Qatar → critical LNG exporter

⚠️ Now add reality:

🇶🇦Qatar is about to restart its LNG.

When Iranian strikes hit Ras Laffan, they took out 17% of Qatar's LNG capacity 12.8 million tonnes a year.

That capacity is gone for 3 to 5 years, not 3 to 5 weeks.

📊 And who benefits?

The US

• Largest producer globally

• Flexible LNG export system

• Able to redirect cargoes fast

Gas is no longer regional

It’s fully geopolitical

Are we entering a world where

US LNG = global energy stability?

Do not miss my latest article where I explain the latest and what does it imply for the market, link in the below comments👇

Cushing Crude Stocks Are Approaching Critical Levels 🇺🇸🛢️

Inventories at Cushing, Oklahoma fell another 1.6 million barrels last week to around 20 million barrels

That is the lowest level since 2014

It also marks the 8th consecutive weekly decline

Total draw over that period

🛢️8.3 million barrels

Cushing is the main delivery point for WTI crude

At current levels, the hub holds less than 2 days of US production

Once inventories fall below roughly 20 million barrels

🔹 Pumping becomes less efficient

🔹 Extraction costs rise

🔹 Water and sediment risks increase

🔹 WTI pricing can become more volatile

At the same time, the Strategic Petroleum Reserve has fallen to around 340 million barrels

The lowest level since 1983

US production remains high

But the storage buffer underneath it is getting dangerously thin

Image source : @KobeissiLetter

US commercial crude oil inventories are reaching critical levels:

Crude inventories at Cushing, Oklahoma, the largest commercial storage hub in the US and the pricing point for WTI Crude, dropped -1.6 million barrels last week, to 20 million barrels, the lowest since 2014.

This marks the 8th consecutive weekly decline, totaling -8.3 million barrels.

As a result, Cushing now holds less than 2 days worth of US crude production, approaching the minimum level at which the facility can continue pumping oil efficiently.

Once inventories fall below ~20 million barrels, extracting crude becomes technically difficult and more costly, while oil quality can deteriorate due to water and sediment.

Meanwhile, the Strategic Petroleum Reserve is down to ~340 million barrels, the lowest since 1983, after 172 million barrels were released to contain war-driven fuel price increases.

US oil inventories down to levels rarely seen in modern energy markets.

US crude just hit $73.

📉Down 39% from the $119 March peak.

The market has officially priced the war as over.

Let me tell you what $73 oil is actually pricing in:

✅ Hormuz fully reopened and flows normalized

✅ Qatar LNG back at 100% capacity

✅ SPR being replenished

✅ Tankers freely transiting the Gulf

✅ Inflation falling, demand recovering

Now let me tell you what's actually happening:

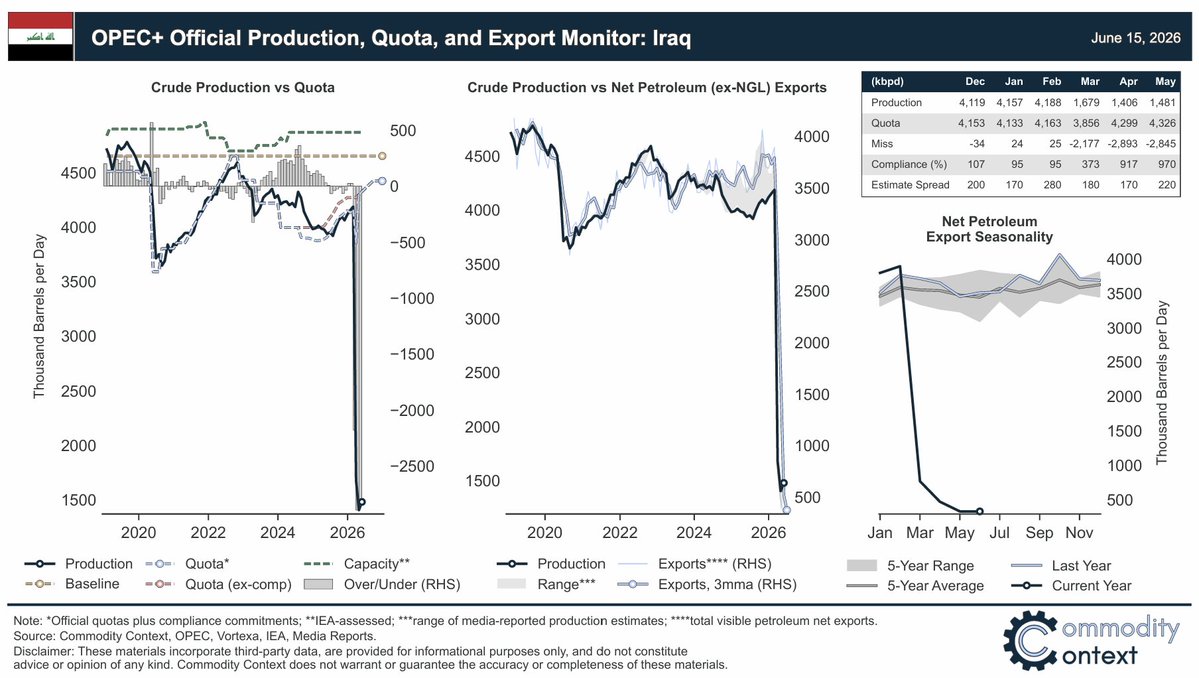

❌ PetroChina couldn't find a tanker to load Iraqi crude this week

❌ Freight rates are still 3x pre-war levels

❌ Hormuz traffic: 29 ships in 5 days, 62% running dark

❌ Qatar capacity: 17% damaged for 3-5 years

❌ US SPR: lowest since 1983, still drawing

❌ Jeff Currie: normalization "not until year-end at the earliest"

The financial market is pricing a political headline.

The physical market is pricing a broken supply chain.

$73 oil with empty SPRs, crippled Hormuz traffic, and damaged Qatari infrastructure is not a relief rally.

It's the biggest disconnect between financial and physical markets I've seen in this crisis.

And disconnects this large don't close slowly.

Full analysis in my article.

Link in the comments 👇

Image Source: Bull Theory

Understanding LNG Import & Regasification Infrastructure

Liquefied Natural Gas (LNG) does not enter a market by chance.

It relies on highly engineered, capital-intensive infrastructure designed to ensure security of supply, flexibility, and market optionality.

An LNG import and regasification terminal typically integrates several critical components:

• Marine unloading facilities allowing LNG carriers or FSRUs to safely berth and transfer cargo

• Cryogenic transfer systems operating at ~-162°C to move LNG from ship to shore

• Full-containment LNG storage tanks providing strategic buffer and seasonal flexibility

• Regasification units converting LNG back into gaseous form using seawater, ambient air, or closed-loop systems

• High-pressure send-out pipelines connecting terminals to national gas grids, utilities, and power plants

• Safety systems including flare stacks, exclusion zones, and continuous monitoring

Beyond engineering, LNG terminals play a strategic role:

• Enable diversification away from pipeline dependency

• Support energy security during demand peaks or supply shocks

• Create trading optionality between regional gas markets

• Anchor long-term offtake, tolling, and capacity contracts

• Act as gateways between global LNG flows and domestic consumption

In today’s energy landscape, #LNG infrastructure is not just physical capacity it is geopolitical leverage, price stability, and strategic flexibility.

#oott

BOOM! 💥 🔥

Texas lands a commitment from four-star offensive tackle Brian Swanson (@BrianSwanson0).

The 6-6, 315-pounder from South Oak Cliff chose the Longhorns over Oklahoma, LSU and SMU. 🤘

US commercial petroleum inventories fell by another 7.9 MMbbl last week, driven by crude and softened by a build in NGLs.

Total crude draws hit 17.2 MMbbl (8.3 commercial, 8.9 SPR), just behind mid-May's all-time high 17.8 MMbbl total crude draw.

OIL INVENTORIES AT 43-YEAR LOW: EXPERT PREDICTS BRENT ABOVE $100 THIS SUMMER

Bob McNally, president of Rapidan Energy Group, just delivered a direct assessment of why the oil market remains far from normal. Even if the Strait of Hormuz reopens by the end of June, commercial tankers will return only gradually while inventories have already crashed to historic lows. The combination of those depleted stocks and a powerful demand rebound from Asia creates a tightening setup that few traders have fully absorbed.

THE HORMUZ REALITY

➡️ It will take through the end of this month before it is really safe and clear for commercial vessels to start moving through Hormuz.

➡️ Agreements must be signed and insurance secured before operators will risk the transit.

➡️ Channels need to be fully cleared of mines for tankers from Europe and the United States to move safely.

➡️ If the MoU holds, a trickle of vessels will gradually become a steady stream.

THE INVENTORY CRISIS

➡️ Gasoline inventories sit at an 11-year seasonal low in the United States.

➡️ Distillate stocks have reached a 29-year seasonal low.

➡️ Crude petroleum reserves just hit a 43-year low.

➡️ These deep stock draws will continue for months as the system works through the disruption.

THE PRICE OUTLOOK

➡️ McNally expects Brent to make another pass above $100 a barrel in July and August.

➡️ Global summer demand rises by about 1.5 million barrels per day.

➡️ Record export levels are adding to an already tight market.

➡️ "I'll be surprised if we can sustainably go much lower," he stated on current price levels.

THE DEMAND REBOUND

➡️ Asia has been on a crash diet since late February, holding back crude purchases.

➡️ Pent-up demand will surge back as countries rush to refill and expand strategic reserves.

➡️ China wants to build even bigger reserves than it held before.

➡️ This demand wave could outpace the return of supply from the Arabian Gulf.

THE BOTTOM LINE

Low inventories and explosive pent-up demand from Asia are about to collide just as Gulf supply struggles to return at full speed.

The oil market is heading into a high-conviction summer where even a successful Hormuz reopening will not prevent prices from testing sharply higher ground.

#OilInventories #HormuzReopen #BrentOil #EnergyMarkets #OilPriceSpike #AsiaDemand #InventoryCrisis

THE WORLD IS QUIETLY DRAINING ITS OIL.

Jeff Currie, one of the most respected commodity strategists in the world and former global head of commodities at Goldman Sachs, recently laid out a setup in the oil market that almost no one is paying attention to.

His core observation is about inventory behavior. Across the world right now, refiners, distributors, and end-users are actively running down their stockpiles in anticipation of lower prices. Drivers are letting their tanks run down on their cars. Buyers are holding off on purchases. Everyone is positioning for a drop that they assume is coming. That's the exact opposite of what was happening a year ago, when precautionary inventories were being built aggressively and that buying behavior helped push oil up to 110 and 120 dollars a barrel.

The dynamic now is the mirror image of that move. Everyone is draining their buffers, expecting supply to arrive and prices to fall. What this actually creates is a massive pool of pent-up demand sitting just below the surface. If the supply doesn't show up the way markets are anticipating, that demand has to come back in all at once, and prices respond accordingly.

Currie's warning on Europe is particularly sharp. The comfort European energy markets have been feeling isn't coming from new production. It's coming from the United States exporting two million additional barrels per day, most of it flowing to Europe, and almost all of that coming directly out of US storage. That isn't a real supply solution. It's a temporary one being financed by drawing down strategic and commercial inventories. It was never sustainable to begin with, and the unwind of that dynamic is one of the most underappreciated risks heading into the summer.

His framing on the geopolitical setup adds another layer. Markets have been trying to price in a flush-out assuming a signed deal would resolve the underlying sanctions and geopolitical issues. Of the roughly 120 to 150 million barrels of leakage in the market, about 40 percent has already come out. The remaining supply response is being priced in as if it's a done deal, when in reality it depends on outcomes that haven't actually happened yet.

The result is a market that is de-stocking aggressively ahead of supply that may not fully materialize, in a structure where Europe's apparent comfort is being financed by a US reserve drain that can't continue indefinitely. That's not a stable equilibrium. That's an asymmetric setup waiting to resolve.