We have revised our previous yield forecasts; in the case of wheat, this raises the production forecast from 21.8 to 22.1 mln t, barley – from 5.6 to 5.8 and rapeseed – from 3.16 to 3.22 mln t.

Thanks to steady demand from the MENA region, #Ukraine’s #wheat balance has improved slightly. Given the current trends, we are raising our export forecast by 400 Kmt and expect exports to reach 1 mln t in June.

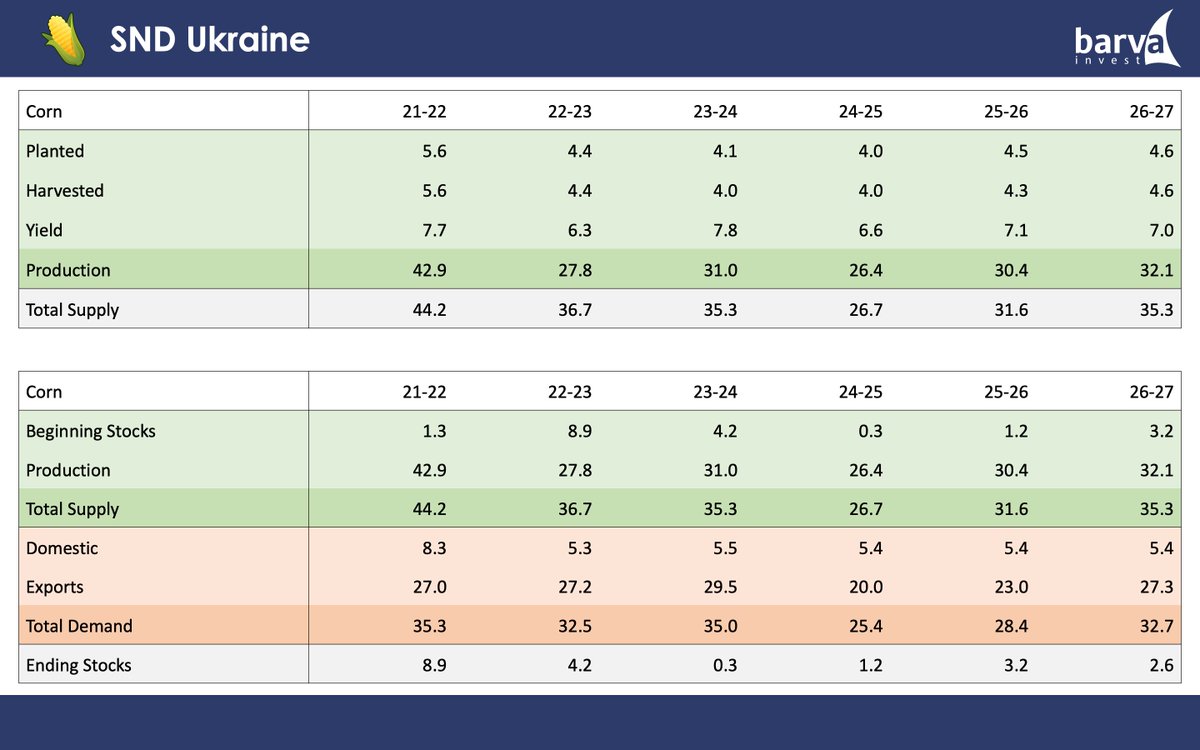

#Ukraine has been able to further reduce its #corn stocks thanks to strong exports. However, our export forecast of 23 mln t is based on a level of demand that we will not see if competitors’ prices remain low this summer (as Brazil is taking market share from Egypt and Spain).

Although the #planting pace is currently behind schedule, we expect #corn areas in #Ukraine to increase slightly for the 2026/27 season. Even assuming mediocre yields, production is expected to reach 32.1 mln t.

#barley stocks in #Ukraine remain among the highest in recent years, but this is no longer a problem. The season is drawing to a close, and the surplus of 200Kmt can be exported without any major issues – provided there is market demand, which we expect to see in July and August.

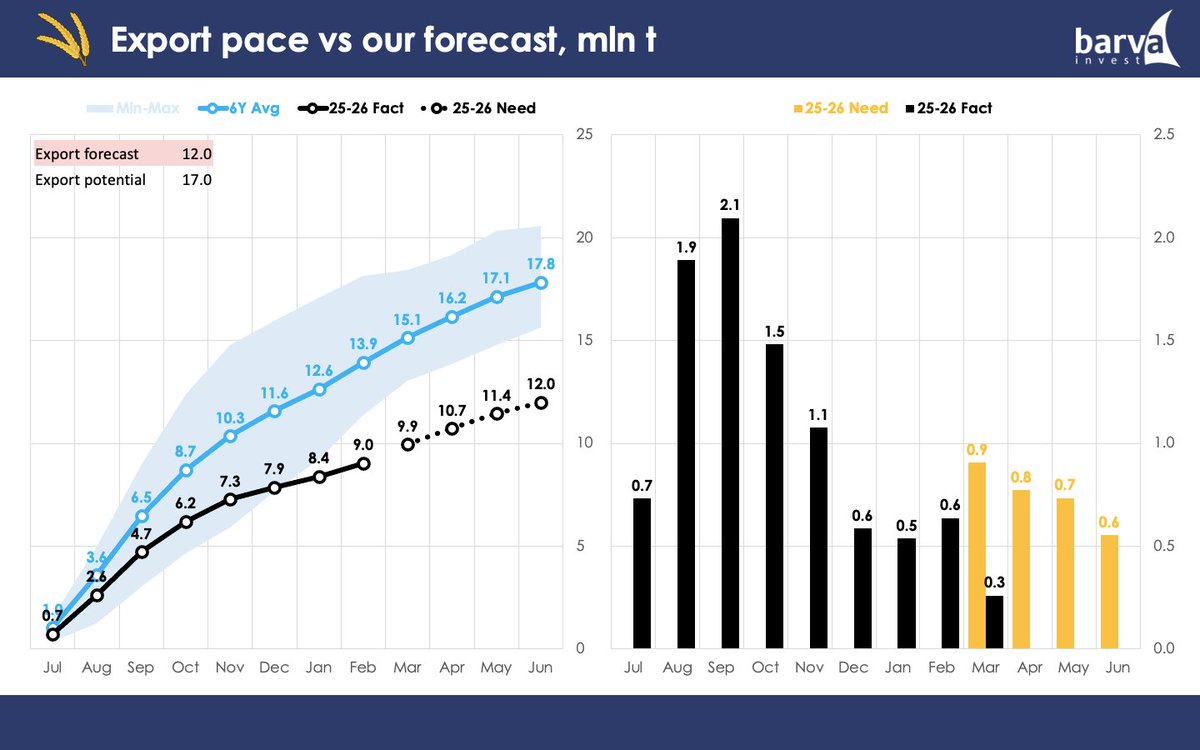

Slow start this season is still having an impact on corn exports out of Ukraine. Although, thanks to increased demand from Turkey and Italy, 2.7 million tonnes of corn were exported in April, matching March’s export numbers and the performance of the 23-24 season.

As of March 17, exports of Ukrainian #corn amounted to 1.4 mln t. For now, we're moving at a pace that promises to repeat the results of previous months. Due to this activity and the emergence of Turkish demand, we have increased the forecast to 23 mln t.

#Ukraine's #corn exports remain geographically constrained. Mediterranean demand still covers most of the export potential, but russian terror remains a major factor impacting our trade.

Kyiv, Kharkiv, Dnipro, Odesa – russia killed people in their sleep today, bragging on socials

Despite three months of strong exports of Ukrainian #corn, slow start to this season is still affecting the market. Corn stocks remain among the biggest in the past few years, and farmers are in no hurry to put them up for sale.

Ukrainian wheat exports are somewhat picking up in comparison to previous trends. But ultimately, they remain sluggish and may not be enough to reach the forecasted 12 mln t – let alone the 17 mln t of full export potential.

@OrcaKoan We base monthly “need” on our assessment of Ukrainian market activity, price levels, and the uncovered needs of key importers.

I.e, UA corn has a limited market (predominantly Mediterranean), and this demand will be even more limited with the arrival of Safrinha corn in Brazil

As of March 29, exports of Ukrainian corn totaled 2.6 mln t, so we would likely see 2.8 mln t this month. And, given the pace, this figure may exceed those for January and February, which led us to raise our forecast to 21.2 mln t.

Current pace of spring barley planting in #Ukraine remains the slowest in recent 10 years. Spring #barley accounts for ~55% of the total area, and we traditionally expect lower yields from these fields; our overall crop forecast stands at 5.8 mln t.

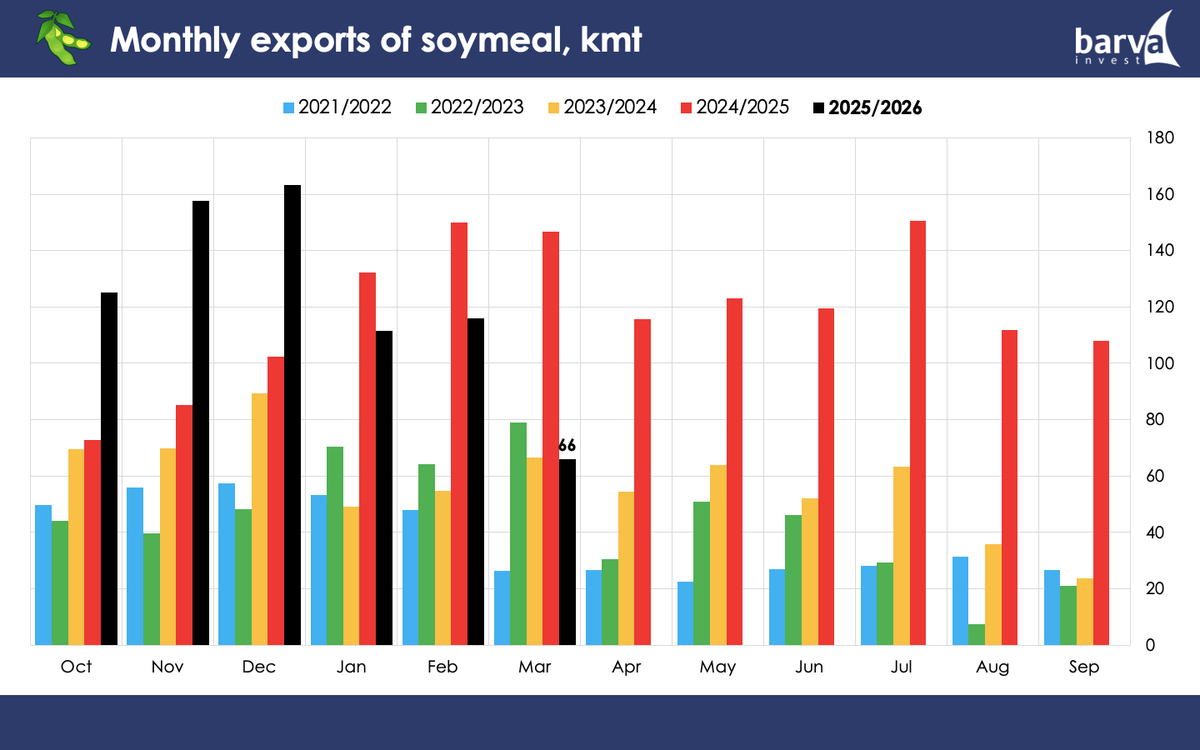

Ukrainian soymeal exports have remained high since the start of the season, whilst soybean's remain relatively low. Soybean exports are being held back by a regulation passed before the start of the 25–26 season, which cuts the number of exporters to whom export tax do not apply.

The pace of #wheat export in #Ukraine remains too slow, and out of 17 mln t of potential, we expect only 12 mln t to be exported. The remaining 5 mln t will create a huge export potential in 26/27 — the largest since the start of the full-scale invasion.

We have concerns now about moisture deficit in key #agricultural regions in #Ukraine, namely southern and central oblasts. Next 10 to 14 days will be predominantly dry.

We've seen sluggish #UA exports, and, as the new harvest approaches, the market is starting to worry about storage capacity. But even if export rates slow further, we will not end up with stocks larger than those of the 21–22 season, the start of russia’s full-scale invasion.

Among all crops in #Ukraine#corn is the most liquid. Stocks remain sufficient, and the need to purchase expensive essentials for the planting campaign will force some farmers to sell their crop more actively, even if they wish to abstain from it amid global market panic.

Before the full-scale invasion, Ukraine supplied sunflower oil to China. War shifted trade: EU preferential access made EU more profitable, so exports pivoted west. Now EU depends heavily on Ukrainian oil (with no russian imports), limiting the flow of exports to other countries.