Anglo Asian Mining $AAZ.L reports FY 2025 results:

Revenue +208%

Net income $18m vs $18m loss in 2024

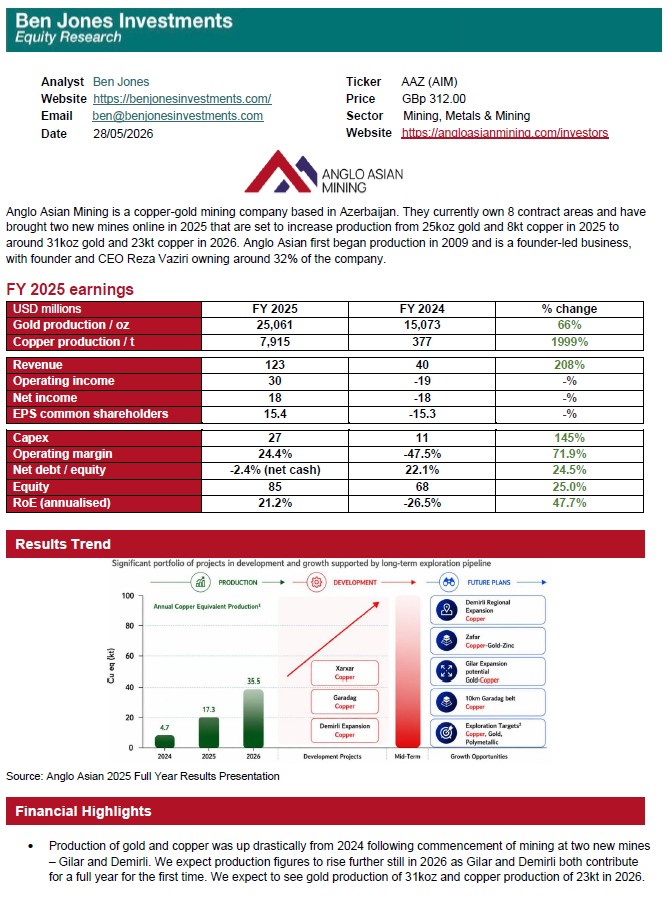

2 new mines operational: Gilar & Demirli

2026 expected revenue >$300m with net income >$100m

3 new mines to develop over next 5 years continuing growth over the medium term

$IBKR posted another strong earnings. IBKR demonstrate their ability to consistently beat competitors on price, rates and product offering as they become increasingly dominant in the low-touch broker market.

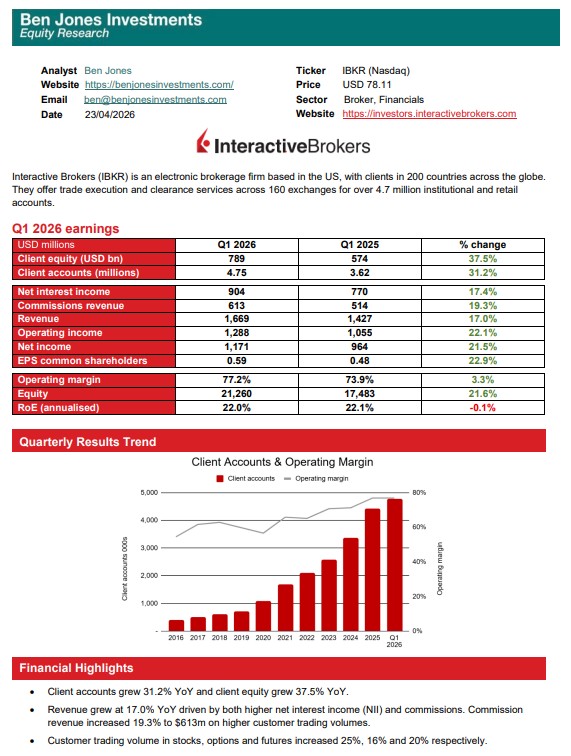

Client accounts +31%

Revenue +17%

Net income +22%

Op margin 77%

$PSN.L 2025 earnings

Completions +11.6%

Operating income +14.9%

Net income + 7.1%

Forecast growth in completions and margin improvement for 2026

Forward p/e 11.2x

BV 1.1x

0 debt and landbank with 7 years worth of build

UK structural housing deficit

Looks cheap

$IGIC priced as if they won't grow premiums or generate any underwriting income again. For a company that has grown premiums earned at a 10% CAGR since 2010 and has an average combined ratio of 87% over the same period, the market seems off.

Looks much too cheap

$GRBK 2025 earnings

Completions +4.2%

Earnings -18.1%

Operating margin 19.5%

Strong balance sheet, industry high margins and looks cheap even with further margin contraction as ASP stalls

$EG 2025 earnings:

Premiums earned +2.5%

NI +15.9%

Combined ratio 98.6%

Thesis is simple: market cap is $13.7bn, book value is $15.5bn and EG earns >$2bn per year from investment income. EG could make $0 through core (re)insurance business each year, and still be undervalued.

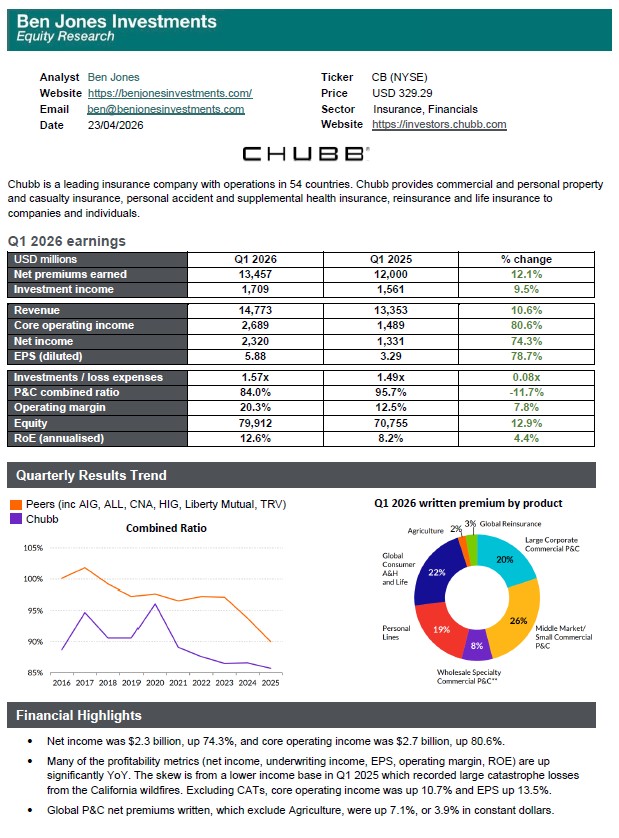

$CB reported record 2025 results.

Net premium earned +6.4%

Combined ratio 85.7%

EPS +13.1%

Low combined ratio across all lines suggests broad underwriting discipline. Growth continuing despite rates softening.

Looks cheap at 12x earnings

$EVO growth stalled in 2025

Revenue +0%

Operating income -5%

PE 10x prices no future growth

Online casino grew at 24% CAGR over last 5 yrs and Evolution remains market leader

Stricter regulation hampers short-term growth but raises barrier to entry and widens moat

Difficult to externally verify the measures taken to combat cyber-attacks in Asia and growth in Europe remains uncertain following ring-fencing. North America and Latam are bright spots.

$MHO reports in-line earnings for 2025

Completions -1.5%

ASP -0.8%

Operating margin 11.5%

Given scope for moderate completion growth and long-run 11% operating margin, $MHO looks cheap at 8x earnings. Strong BS with 0 net debt