Nem humano. Nem máquina.

O investidor do futuro será os dois.

Estamos construindo a Better Call US — uma plataforma de decisão para operar o mercado global com clareza, contexto e convicção.

IA organiza.

Traders refinam.

A decisão é sua.

Leia o manifesto:

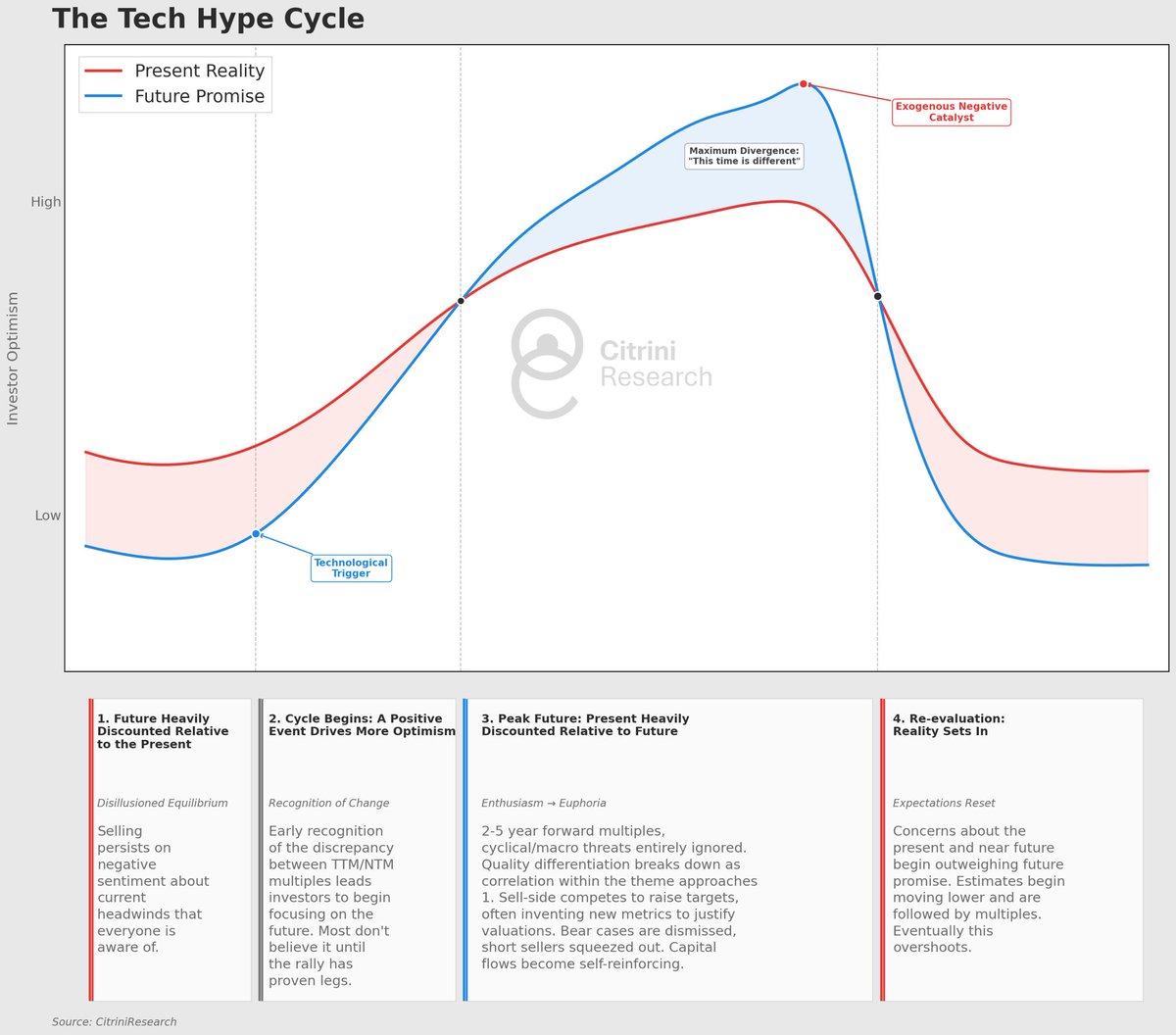

This is how I think about hype cycles in markets. It is basic, but that’s the point (frameworks shouldn’t be overly complex, I think).

Investors are always either discounting the promise of the future or the reality of the present. And they are never equally weighting them.

During the early part of a hype cycle, leading up to and directly following a technological advancement, investors are typically discounting the future while focusing on the present. A good example for this is Nvidia at the end of 2022: investors were solely focused on the headwinds presented by the crypto GPU glut, the anemic gaming PC market and the recent rise in rates causing fears about a near term recession.

Then, as the cycle begins, investors begin to shift to incorporate the future - they stop focusing so much on the present and see the promise. They move out in terms of valuing away from last twelve months current price / current earnings to next twelve months. Then, as price climbs and the technology becomes more exciting, their imagination takes hold. At a certain point they begin discounting the present much more heavily and the future becomes the only thing that matters. Valuation metrics over the next twelve months become useless in favor of 2, 3 or 5 years forward.

At the peak, the present is not considered at all, it is 100% driven by an imagined future (even when that imagination doesn’t necessarily align with a bullish outcome for the stocks driving the rally). Analysts aggressively raise estimates in ways that, at the time, seem fundamentally justifiable (if you take the assumptions at face value - for example, “everyone in the world will have two cell phones” was a good one from the mobile phone hype cycle). Capital is sucked in which ultimately forces performance chasing and crowds stocks with money that doesn’t really believe in the thesis. “A twilight period where people continue to play the game, but no longer believe in the rules” emerges, as Soros put it.

The valuation of SaaS stocks in mid-2021 is a great example of what happens when the future is overvalued relative to the present - nobody cared about climbing inflation, that rates had nowhere to go but up, that these companies were reliant on ZIRP or that software could become more competitive.

Then, a negative catalyst occurs - this can but doesn’t have to be related to the technology, macro, credit, underwhelming earnings. The estimates start to seem unattainable, and the present begins to matter more when the future seems more uncertain. That exact mechanism that drove future optimism to unsustainable heights mechanically reverses, everyone needs out. The future begins to be discounted until it results in a sense of disillusionment with not just the stocks but the technology itself. This overshoots to the downside, investors eventually become disillusioned and seemingly allergic to anything having to do with the technology. This happens in a very asymmetric manner to the climb (“stairs up, elevator down”).

This is the crucible in markets for truly transformative tech. If advancements persist, another opportunity to get long presents itself before capital once again begins flowing into the companies (the internet, for example). If they don’t - not necessarily “the tech goes away” but rather that it ceases to advance once the capital isn’t free or plateaus or the economics prove to be unfavorable - the cycle will still start again, just with a new technology.

Or maybe not…maybe this time is different.

Você não gasta dinheiro para comprar coisas, você gasta para cobrir buracos emocionais.

A neurociência é clara: o jeito que você lida com o seu patrimônio revela as suas questões mal resolvidas. Muito profissional brilhante e bem-sucedido gasta um dinheiro que não tem para tentar comprar respeito, status ou afeto de pessoas que ele nem gosta.

O nome disso não é "estilo de vida", é ego sangrando para cobrir uma falta.

Aperte o play. Eu te explico como a falta de autoconhecimento te faz tomar decisões financeiras que destroem silenciosamente o que você demorou anos para construir.

Se você quer aprender a governar o seu dinheiro com inteligência emocional e parar de ser refém da própria mente, seja bem-vindo.

#InteligenciaComportamental #FinancasComportamentais #NeurocienciaAplicada #SteadyTrade #GestaoDePatrimonio #ComportamentoHumano

@breno00iwf Aqui mesma coisa

Meu problema continua sendo gordura, pq eu AMO iguarias de gordura

Capinha da picanha, ossobuco, pele de porco do feijão...

Glicose e triglicerídeos excelente, colesterol socorro

Para quem assim como eu toma muito café, comecei a fazer algo que a princípio era horrível mas acostuma.

Diluir o café em uma quantidade absurda de água quente. O famoso chafé, te garanto que em 3 dias você acostuma e melhora muito a hidratação e o sono a noite.

Pare de tomar às 16h.

E ah, sim

É legal de comprar as coisas quando elas estão esquecidas

Todo mundo lamentando chip e IA.... e $XRT continua impávida colossa rumo ao ATH fora do radar.

$NKE um Wyckoff de livro. Tanto que tirei o print pra usar de exemplo para o meu livro.

Preliminary support com volume forte, rompido pra baixo, que virou resistência do range

Range bem definido e respeitadinho

Spring com volume forte e retorno rápido ao range

Rompimento e batida na POC é buy.

$NKE um Wyckoff de livro. Tanto que tirei o print pra usar de exemplo para o meu livro.

Preliminary support com volume forte, rompido pra baixo, que virou resistência do range

Range bem definido e respeitadinho

Spring com volume forte e retorno rápido ao range

Rompimento e batida na POC é buy.

$KORU - chegou agora na linha mágica de resistência estrutural.

$MU (e outras semis memória etc.) - zona ideal para um sweep e prender um monte de ursos no vácuo de liquidez da POC (zona de rejeição).

Acredito sim que ainda vai dar uma bela corrida pra cima, nem que seja na forma de "para cair mais tem que subir"

Enquanto isso, $QQQ empacado, mercado de lado, sweep nos índices, mas $MAGS e ETFs de real economy andando bem.

Não cansada de tomar muito olé em $COPX, dei reentrada nela hj.

Acredito em bull case pra miners em geral, e virada em metais preciosos com a resolução nos yields/$DXY.

Incluindo $VALE que foi outra que me deu olé.

$COPX, nosso bull case para os Copper Miners:

Em ciclos de afrouxamento monetário combinados com aceleração do crescimento (especialmente o chinês), os miners costumam performar muito bem.

Isso converge com toda a análise que temos feito (e surfado) em Indústria ($XLI) e Basic Materials ($XLB, especialmente indústria química, que também estamos bullish e comprados até às tampas).

Desde meados do ano passado temos apontado aqui a dinâmica favorável do $XAUXAG (Gold/Silver Ratio) para a prata (que nós surfamos também), privilegiando, portanto, a parcela risk-on e de demanda industrial do metal.

Isso beneficia o cobre, para quem enxergamos um belo ciclo pela frente. E miners são trades de preço do metal e spread do custo. Juros mais baixos beneficiam indiretamente, pela via estímulo da demanda + relaxamento da dívida.

Nossa tese é $COPX, o ETF de maior liquidez, que pegamos sobre a POC na compressão de vol recente, em triângulo.

Já rompendo e dando alegria.

$COPX, nosso bull case para os Copper Miners:

Em ciclos de afrouxamento monetário combinados com aceleração do crescimento (especialmente o chinês), os miners costumam performar muito bem.

Isso converge com toda a análise que temos feito (e surfado) em Indústria ($XLI) e Basic Materials ($XLB, especialmente indústria química, que também estamos bullish e comprados até às tampas).

Desde meados do ano passado temos apontado aqui a dinâmica favorável do $XAUXAG (Gold/Silver Ratio) para a prata (que nós surfamos também), privilegiando, portanto, a parcela risk-on e de demanda industrial do metal.

Isso beneficia o cobre, para quem enxergamos um belo ciclo pela frente. E miners são trades de preço do metal e spread do custo. Juros mais baixos beneficiam indiretamente, pela via estímulo da demanda + relaxamento da dívida.

Nossa tese é $COPX, o ETF de maior liquidez, que pegamos sobre a POC na compressão de vol recente, em triângulo.

Já rompendo e dando alegria.

You say you'd never compromise

With the mystery tramp, but now you realize

He's not selling any alibis

As you stare into the vacuum of his eyes

And say: Do you want to make a deallllllll