@MoodyWriter13 Markets are pricing $MIAX as if the growth story will be impacted. I don’t see this happening at all. These things have a liquidity network effect. The liquidity flywheel won’t start spinning for the simple fact that perps are an unfavorable risk/reward vs options for MM’s.

@MoodyWriter13 Spot on. Exchange members/MM’s will demand a wide BA-spread as there is no efficient way to hedge the funding rate risk. There is no maturity anchor. You cannot model future retail flow and MM’s thus also risk unbalanced inventory without a lender of last resort backstop.

@Pickwick2021@zerohedge CFTC chair talking about perpetual futures contracts on cnbc… those products won’t have ant liquidity as it is impossible for market makers to hedge the funding rate risk

$MIAX $CBOE $PURR

A few points for context:

The headline “$1.4 billion in perp volume” sounds like a huge, threatening market. In reality, the live exposure (~$100 million in open interest, of which only a fraction is actual capital, since that $100M is leveraged) is tiny compared to the regulated options market, where MIAX oder CBOE or orhers clears millions of contracts every day. The big number comes from heavy leverage and rapid back-and-forth trading, not from real market weight. That’s exactly why the open interest puts the headline so firmly into perspective.

The timing explains the perp volume. The $1.4 billion built up in the days before and around the $SPCX IPO, when there was no regular way to trade SpaceX yet. Options on SpaceX only became available today. So this was IPO-hype-driven pre-listing speculation. The real question is whether that perp volume sticks now that the stock is listed and regulated options exist, or whether it migrates to the regulated, hedged products. We don’t know yet, but it’s unlikely to stick, for the reasons below.

Second, the risk-profile argument. Even with SPCX now publicly listed, the core difference remains: an option has capped risk, a 50:1 perp does not. Freshly listed IPO stocks are extremely volatile, exactly the environment where unhedged perp traders get liquidated in waves. Over the medium term, that favors the regulated products for institutional and risk-aware traders.

Third, the regulatory question is now real, not theoretical. With a publicly listed mega-cap as the perp underlying, the SEC and CFTC will be watching far more closely. Hyperliquid is a decentralized, largely unregulated venue, whether US institutions are allowed to, or want to, trade SPCX perps there at scale is an open question.

Perps and Hyperliquid aren’t a threat to $MIAX. They’re just another lane being added to the options highway. And historically, adding more lanes to the highway has always led to more traffic, not less.

@MoodyWriter13 And even IF a $MIAX member sees value in launching perpetuals, MIAX has both the flexibility and the capital to pursue that opportunity. But those perps are very inefficient products for market makers to hedge, there won't be any liquidity in those products...

@MoodyWriter13 I’d say the liquidity flywheel effect will be much larger than the cannibalization effect. SpaceX options would likely create substantial incremental volume, not just shift volume from existing names. MIAX’s low-latency infrastructure will attract significant % of flow.

The $SNEX premium over $MRX is getting out of hand. The premium is valid, but the spread has just gotten too large considering their similar future '25-'27 EPS CAGR.

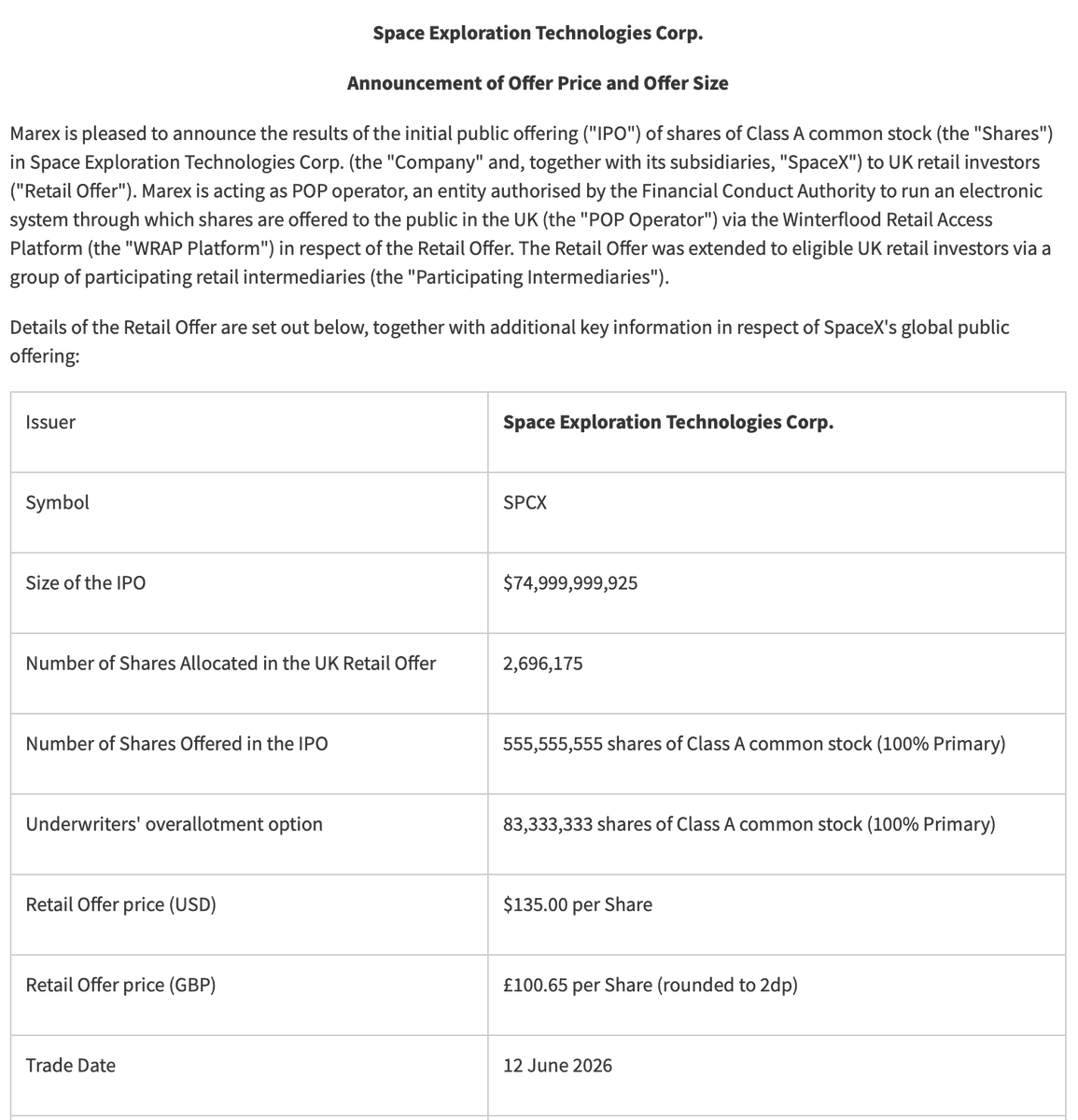

$MRX 's Winterflood Securities is allocating $SPCX shares to UK retail investors. Marex was mandated 2.7mio shares. They take a 0.4% slice and rebate 0.2%. That's an easy 730k 3Q26 net revenue lift, not even considering the consequential increase in trading in popular symbols.

$MRX expands its commodities footprint with the acquisition of Monaco-based Levmet. The deal adds European power & gas trading capabilities and strengthens MRX’s physical market-making business across metals, energy, and derivatives. + Still a lot of companies in the pipeline!

$CME launched futures on compute. The new cash-settled contracts let firms hedge AI compute and GPU price volatility.

As an established CME clearing member and broker, $MRX is positioned to give clients access to these next-gen markets.

Compute will become a tradable asset class

@MoatOwl@ragingbullcap But these MM still need end clients to make a market for. BB indices have been pushed to institutions for some time now. Let’s see whether they will be used or not. Anyway, I think the overall index derivatives market will be better off with some $MIAX disruption ;)

@MoatOwl@ragingbullcap Good thing is that market makers don’t like the current monopolistic market environment in index derivatives. Imo there’s a high probability of MMs allocating flow to the lower RPC contracts if it offers similar risk/reward/exposure.