🏛️ Ex-Economist | Daily #Finance & #Crypto bites ☕

📈 Smart trades & wealth building for the modern investor

📊 Data ➡ Rumors. Sifting through the market noise

𝗕𝗜𝗧𝗖𝗢𝗜𝗡 𝗨𝗣𝗗𝗔𝗧𝗘 : 𝗘𝘅𝗲𝗰𝘂𝘁𝗶𝗻𝗴 𝗧𝗵𝗲 𝗦𝗵𝗼𝗿𝘁𝗶𝗻𝗴 𝗚𝗶𝗳𝘁 🎯📉

Two months ago I handed you the exact playbook.

I told you to hibernate through the 60s and 70s.

It’s not worth stressing out by entering in a wider counter trend trade, risks are too high.

I warned you and I hope you didn’t let the chop drain your capital or your patience because the moment we’ve been waiting for has finally arrived.

Price is now pushing above 80k. Right into our designated premium shorting zone.

If you look at your timeline people are euphoric. They are screaming that the bull market is back and FOMOing into green daily candles.

This is the exact exit liquidity the market makers engineered this pump to collect…

Discipline pays! We sleep through the noise so we can strike at the extremes!

Gradual entries, no over exposure, always keep dry powder

𝗕𝗜𝗧𝗖𝗢𝗜𝗡 𝗨𝗣𝗗𝗔𝗧𝗘: 𝗧𝗵𝗲 𝗛𝗶𝗯𝗲𝗿𝗻𝗮𝘁𝗶𝗼𝗻 𝗣𝗵𝗮𝘀𝗲 (𝗡𝗼𝘁𝗵𝗶𝗻𝗴 𝗛𝗮𝘀 𝗖𝗵𝗮𝗻𝗴𝗲𝗱) 🐻💤

A quick update to the February 17th roadmap.

We are deep in the “Hibernation Phase”. The price is bouncing and we can already seeing people FOMO back in.

Imagine if we hit 80’s or even 90’s…

For me the strategy has not changed one bit.

🛑 𝗧𝗵𝗲 𝗙𝗢𝗠𝗢 𝗧𝗿𝗮𝗽

I have zero doubt we are going to make a lower low in the coming weeks or months.

Longing this is a statistical a suicide mission. The MM goal right now is to drain your capital and your patience before the real flush happens.

🎯 𝗧𝗵𝗲 𝗦𝗵𝗼𝗿𝘁𝗶𝗻𝗴 𝗚𝗶𝗳𝘁 (𝟴𝟬𝗸 - 𝟵𝟬𝗸)

If the market decides to squeeze late shorters and give us a major relief bounce into the $80k–$90k region, do not mistake it for a trend reversal. It is a liquidity grab. If we get there, it is a highly profitable premium zone to short the market. We sell their hope.

📥 𝗧𝗵𝗲 𝗕𝗶𝗱𝘀 𝗥𝗲𝗺𝗮𝗶𝗻 𝗔𝗻𝗰𝗵𝗼𝗿𝗲𝗱 (<𝟲𝟬𝗸)

My buy orders remain open below $60k.

The Playbook Right Now:

• Pump into the 80s/90s? Short it.

• Chop in the 60s/70s? Ignore it.

• Flush below 60k? Buy it.

➡️ Do not let a bounce break a macro plan. Let the tourists exhaust themselves in the middle.

We hibernate until the extremes are hit.

Until then good night 😴

Highly unlikely we see the 80k–90k zone tagged again. If we do it’s another opportunity to add more shorts.

Entering any new shorts below $80k is not worth it as the risk/reward favorable.

Cash stays king. Better to preserve capital and let the market bleed out until it’s time to enter.

I don’t leverage trade but like I said in my post above 80k was too good to ignore.

𝗕𝗜𝗧𝗖𝗢𝗜𝗡 𝗨𝗣𝗗𝗔𝗧𝗘 : 𝗘𝘅𝗲𝗰𝘂𝘁𝗶𝗻𝗴 𝗧𝗵𝗲 𝗦𝗵𝗼𝗿𝘁𝗶𝗻𝗴 𝗚𝗶𝗳𝘁 🎯📉

Two months ago I handed you the exact playbook.

I told you to hibernate through the 60s and 70s.

It’s not worth stressing out by entering in a wider counter trend trade, risks are too high.

I warned you and I hope you didn’t let the chop drain your capital or your patience because the moment we’ve been waiting for has finally arrived.

Price is now pushing above 80k. Right into our designated premium shorting zone.

If you look at your timeline people are euphoric. They are screaming that the bull market is back and FOMOing into green daily candles.

This is the exact exit liquidity the market makers engineered this pump to collect…

Discipline pays! We sleep through the noise so we can strike at the extremes!

Gradual entries, no over exposure, always keep dry powder

𝗕𝗜𝗧𝗖𝗢𝗜𝗡 𝗨𝗣𝗗𝗔𝗧𝗘: 𝗧𝗵𝗲 𝗛𝗶𝗯𝗲𝗿𝗻𝗮𝘁𝗶𝗼𝗻 𝗣𝗵𝗮𝘀𝗲 (𝗡𝗼𝘁𝗵𝗶𝗻𝗴 𝗛𝗮𝘀 𝗖𝗵𝗮𝗻𝗴𝗲𝗱) 🐻💤

A quick update to the February 17th roadmap.

We are deep in the “Hibernation Phase”. The price is bouncing and we can already seeing people FOMO back in.

Imagine if we hit 80’s or even 90’s…

For me the strategy has not changed one bit.

🛑 𝗧𝗵𝗲 𝗙𝗢𝗠𝗢 𝗧𝗿𝗮𝗽

I have zero doubt we are going to make a lower low in the coming weeks or months.

Longing this is a statistical a suicide mission. The MM goal right now is to drain your capital and your patience before the real flush happens.

🎯 𝗧𝗵𝗲 𝗦𝗵𝗼𝗿𝘁𝗶𝗻𝗴 𝗚𝗶𝗳𝘁 (𝟴𝟬𝗸 - 𝟵𝟬𝗸)

If the market decides to squeeze late shorters and give us a major relief bounce into the $80k–$90k region, do not mistake it for a trend reversal. It is a liquidity grab. If we get there, it is a highly profitable premium zone to short the market. We sell their hope.

📥 𝗧𝗵𝗲 𝗕𝗶𝗱𝘀 𝗥𝗲𝗺𝗮𝗶𝗻 𝗔𝗻𝗰𝗵𝗼𝗿𝗲𝗱 (<𝟲𝟬𝗸)

My buy orders remain open below $60k.

The Playbook Right Now:

• Pump into the 80s/90s? Short it.

• Chop in the 60s/70s? Ignore it.

• Flush below 60k? Buy it.

➡️ Do not let a bounce break a macro plan. Let the tourists exhaust themselves in the middle.

We hibernate until the extremes are hit.

Until then good night 😴

𝗕𝗜𝗧𝗖𝗢𝗜𝗡 𝗨𝗣𝗗𝗔𝗧𝗘: 𝗧𝗵𝗲 𝗛𝗶𝗯𝗲𝗿𝗻𝗮𝘁𝗶𝗼𝗻 𝗣𝗵𝗮𝘀𝗲 (𝗡𝗼𝘁𝗵𝗶𝗻𝗴 𝗛𝗮𝘀 𝗖𝗵𝗮𝗻𝗴𝗲𝗱) 🐻💤

A quick update to the February 17th roadmap.

We are deep in the “Hibernation Phase”. The price is bouncing and we can already seeing people FOMO back in.

Imagine if we hit 80’s or even 90’s…

For me the strategy has not changed one bit.

🛑 𝗧𝗵𝗲 𝗙𝗢𝗠𝗢 𝗧𝗿𝗮𝗽

I have zero doubt we are going to make a lower low in the coming weeks or months.

Longing this is a statistical a suicide mission. The MM goal right now is to drain your capital and your patience before the real flush happens.

🎯 𝗧𝗵𝗲 𝗦𝗵𝗼𝗿𝘁𝗶𝗻𝗴 𝗚𝗶𝗳𝘁 (𝟴𝟬𝗸 - 𝟵𝟬𝗸)

If the market decides to squeeze late shorters and give us a major relief bounce into the $80k–$90k region, do not mistake it for a trend reversal. It is a liquidity grab. If we get there, it is a highly profitable premium zone to short the market. We sell their hope.

📥 𝗧𝗵𝗲 𝗕𝗶𝗱𝘀 𝗥𝗲𝗺𝗮𝗶𝗻 𝗔𝗻𝗰𝗵𝗼𝗿𝗲𝗱 (<𝟲𝟬𝗸)

My buy orders remain open below $60k.

The Playbook Right Now:

• Pump into the 80s/90s? Short it.

• Chop in the 60s/70s? Ignore it.

• Flush below 60k? Buy it.

➡️ Do not let a bounce break a macro plan. Let the tourists exhaust themselves in the middle.

We hibernate until the extremes are hit.

Until then good night 😴

𝗕𝗜𝗧𝗖𝗢𝗜𝗡 𝗨𝗣𝗗𝗔𝗧𝗘 : 𝗦𝘂𝗿𝘃𝗶𝘃𝗶𝗻𝗴 𝘁𝗵𝗲 𝗕𝗼𝗿𝗲𝗱𝗼𝗺 𝘁𝗼 𝗕𝘂𝘆 𝘁𝗵𝗲 𝗕𝗼𝘁𝘁𝗼𝗺

🐻

We are in a confirmed Bear Market nothing new….

The primary driver of losses right now is not price collapse, but boredom.

Retail are forcing capital into a statistically negative environment simply to feel active… donating liquidity in a zone designed to chop them up. 🪚

🚫 𝗧𝗵𝗲 "𝗡𝗼-𝗚𝗼 𝗭𝗼𝗻𝗲" 𝗶𝘀 𝗮 𝗧𝗿𝗮𝗽 𝗳𝗼𝗿 𝗧𝗼𝘂𝗿𝗶𝘀𝘁𝘀

Trading above 𝟲𝟬𝗸 is currently negative EV.

This range is a volatility vacuum, designed to bleed impatient capital through chop and fake-outs.

Most participants are losing money here because they lack the discipline to do nothing.

This is the time to be strategic, to be patient and letting the tourists fight over scraps while the chart paints a clear roadmap for the next 𝟮 𝘆𝗲𝗮𝗿𝘀.

🎯 𝗧𝗵𝗲 𝗦𝗻𝗶𝗽𝗲𝗿 𝗘𝗻𝘁𝗿𝘆: 𝗧𝗮𝗰𝘁𝗶𝗰𝗮𝗹 𝗕𝗼𝘂𝗻𝗰𝗲 𝗣𝗹𝗮𝘆

Entry at 𝟱𝟵𝗸 is strictly a 𝘁𝗲𝗰𝗵𝗻𝗶𝗰𝗮𝗹 𝘁𝗿𝗮𝗱𝗲, not a marriage.

It is highly lucrative if timed correctly, but it is a swing trade, not a lifestyle. Risk management here must be tight.

🏦 𝗧𝗵𝗲 𝗩𝗮𝘂𝗹𝘁 𝗘𝗻𝘁𝗿𝘆: 𝗧𝗵𝗲 𝗖𝘆𝗰𝗹𝗶𝗰𝗮𝗹 𝗕𝗼𝘁𝘁𝗼𝗺

The real opportunity lies around the 𝟱𝟬𝗸 𝗥𝗲𝗴𝗶𝗼𝗻. (Maybe even below but let’s not be too greedy!)

This is the macro target where I intend to deploy 𝘀𝗲𝗿𝗶𝗼𝘂𝘀 𝘀𝗶𝘇𝗲 for the next bull cycle.

This is not a trade it is long-term positioning for a multi-year horizon.

⏳ 𝗣𝗮𝘁𝗶𝗲𝗻𝗰𝗲 𝗶𝘀 𝘁𝗵𝗲 𝗢𝗻𝗹𝘆 𝗥𝗲𝗺𝗮𝗶𝗻𝗶𝗻𝗴 𝗘𝗱𝗴𝗲

The market will likely give us these prices, but not before it makes you wait until you are disgusted.

The algorithm of a bear market is designed to exhaust your patience before it fills your bids.

The question is not if the price will get there, but whether you will still have capital left to deploy when it does…

𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝘆: Have a clear plan and do nothing until the price meets your plan.

➡️ Discipline over activity. Execution over emotion.

From the @WhiteHouse factsheet on the global 10% tariff (section 122):

Critical minerals (which include silver and PGMs), metals used in currency and bullion (all precious metals products), are exempted.

If that still leaves any doubt, there is also a second line item stating they will not tariff any natural resource the US is net short on.

https://t.co/taZfRLmBf9…

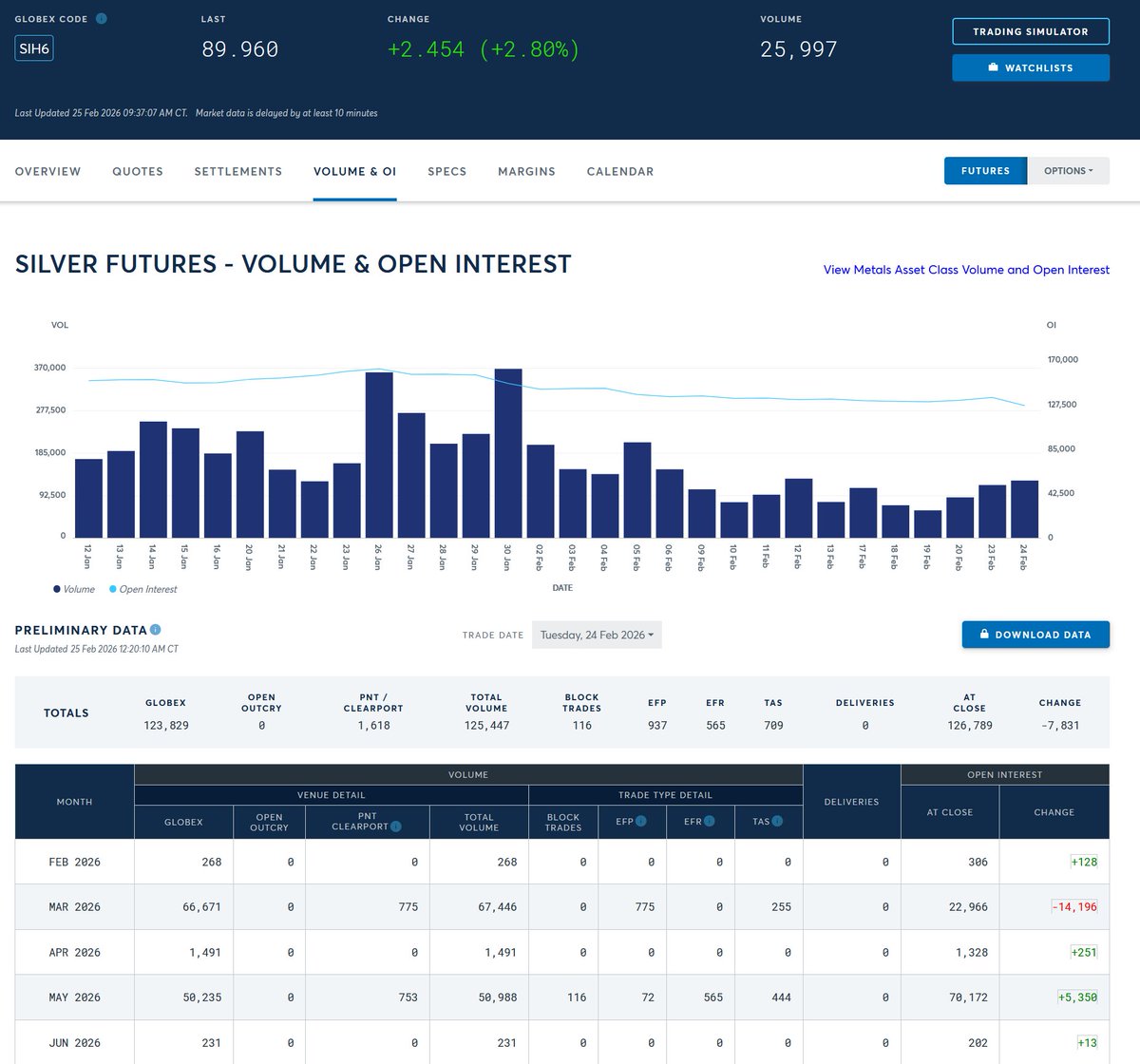

Silver open interest and March deliveries.

Social media has become a sea of confusion, misinformation, and speculation involving silver futures and the March delivery month.

The fact is, the Comex is not going to default and March contracts are being liquidated or rolled in an orderly fashion.

We just saw a decline of 14,196 March contracts yesterday, which equates to almost 71 million ounces. This is happening with volatility declining.

It appears the market is strengthening under the surface with less participation. Not seeing the crowded conditions we saw in January.

𝗧𝗵𝗲 𝗜𝗘𝗘𝗣𝗔 𝗧𝗮𝗿𝗶𝗳𝗳 𝗥𝗲𝘃𝗲𝗿𝘀𝗮𝗹: 𝗟𝗲𝗴𝗮𝗹 𝗥𝗼𝘁𝗮𝘁𝗶𝗼𝗻 𝗼𝗿 𝗣𝗼𝗹𝗶𝗰𝘆 𝗦𝗵𝗶𝗳𝘁?

The US Supreme Court has struck down the administration’s emergency tariff regime forcing Customs and Border Protection to abruptly halt collections.

However beneath the surface of this “legal defeat” lies a swift policy rotation that will keep the structural trade barriers completely intact…

🗝️ 𝗞𝗲𝘆 𝗧𝗮𝗸𝗲𝗮𝘄𝗮𝘆𝘀

• 𝗖𝗕𝗣 𝗔𝗰𝘁𝗶𝗼𝗻: Collections of IEEPA tariffs officially cease at 𝟭𝟮:𝟬𝟭 𝗮.𝗺. 𝗘𝗦𝗧 on 𝗙𝗲𝗯𝗿𝘂𝗮𝗿𝘆 𝟮𝟰.

• 𝗥𝗲𝗳𝘂𝗻𝗱 𝗥𝗶𝘀𝗸: Over 𝟭𝟳𝟱 𝗯𝗶𝗹𝗹𝗶𝗼𝗻 in collected revenues are now legally eligible for complex refund claims.

• 𝗥𝗲𝗽𝗹𝗮𝗰𝗲𝗺𝗲𝗻𝘁: A new 𝟭𝟱% global tariff immediately replaces the void, utilizing a different legal framework.

• The mechanism has changed, but the restrictive trade environment remains fully anchored.

📉 𝗖𝗕𝗣 𝗛𝗮𝗹𝘁𝘀 𝗖𝗼𝗹𝗹𝗲𝗰𝘁𝗶𝗼𝗻𝘀 𝗮𝘀 𝟭𝟳𝟱 𝗕𝗶𝗹𝗹𝗶𝗼𝗻 𝗶𝗻 𝗥𝗲𝗳𝘂𝗻𝗱𝘀 𝗟𝗼𝗼𝗺

Following the Supreme Court ruling Customs and Border Protection is deactivating all tariff codes associated with the International Emergency Economic Powers Act (IEEPA).

This creates an immediate fiscal vacuum, as these tariffs were generating over 𝟱𝟬𝟬 𝗺𝗶𝗹𝗹𝗶𝗼𝗻 per day in gross revenue.

More importantly, it exposes the US Treasury to massive liability, with economists estimating that more than 𝟭𝟳𝟱 𝗯𝗶𝗹𝗹𝗶𝗼𝗻 in illegally collected duties are now subject to potential corporate refunds.

⚖️ 𝗟𝗲𝗴𝗮𝗹 𝗣𝗶𝘃𝗼𝘁 𝗥𝗮𝘁𝗵𝗲𝗿 𝗧𝗵𝗮𝗻 𝗮 𝗣𝗼𝗹𝗶𝗰𝘆 𝗥𝗲𝘃𝗲𝗿𝘀𝗮𝗹

To interpret this as a return to free trade would be a severe miscalculation!

The Trump administration is not abandoning its protectionist stance it is merely rotating its legal authority.

As the IEEPA duties fall away, a new 𝟭𝟱% global tariff is being simultaneously imposed under Section 122 of the Trade Act of 1974.

Furthermore, the targeted Section 232 and Section 301 tariffs remain completely untouched!

🏭 𝗠𝗮𝗰𝗿𝗼 𝗜𝗺𝗽𝗮𝗰𝘁 𝗥𝗲𝗺𝗮𝗶𝗻𝘀 𝗦𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗮𝗹𝗹𝘆 𝗜𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻𝗮𝗿𝘆

This is a structural continuation of the current trade regime disguised as a cyclical disruption!

The refund process will be deeply protracted and litigious, meaning a sudden 𝟭𝟳𝟱 𝗯𝗶𝗹𝗹𝗶𝗼𝗻 liquidity injection for US importers is highly improbable in the near term.

Meanwhile, the rapid replacement of the tariffs guarantees that supply chains will continue to face elevated costs and persistent inflationary pressures.

Legal volatility. Structural protectionism.

#Trump #Trade #Tariffs

THE SILVER-EQUITY NEXUS 🔗

The historical divergence between precious metals and risk assets is temporarily breaking down as we can observe in the chart below.

Cross-asset linkages seem to be tightening, for the time being silver is increasingly trading as a high-beta proxy for broader equity liquidity rather than an isolated monetary metal.

▪️ STRONG POSITIVE CORRELATION EMERGES 📊

Equities and silver are exhibiting a surprisingly strong positive correlation in recent times.

They are currently moving largely in tandem, overriding traditional safe-haven dynamics.

This tightening relationship means risk transmission is bleeding directly across asset classes.

▪️ EQUITY LIQUIDITY IS DICTATING METALS PRICING 📉

At present the broader macro tone remains cautiously bearish.

If a sustained equity selloff materializes it is highly likely to exert direct downside pressure on silver.

Conversely if equities can absorb the current selling pressure and stabilize, silver is positioned for rapid upward momentum.

▪️RISK TRANSMISSIONS Trumps Isolated Fundamentals 🔄

This implies a cyclical liquidity adjustment rather than a structural change in silver’s core thesis.

When cross-asset correlations approach one, it signals a macro environment driven by broad de-risking or re-risking rather than idiosyncratic value.

Confirmation from price action across both markets is now critical before sizing positions.

🗝️ KEY INTERMARKET SIGNALS TO MONITOR 📝

• Correlation Window: Positive tandem movement

• Downside Risk: Equity capitulation will drag silver lower.

• Upside Catalyst: Equity stabilization provides a springboard for metals.

• Tactical View: Watch the S&P for leading indicators on silver entry points.

➡️ Cyclical correlation. Structural patience.

#Silver #spx #silversqueeze

These AI-generated videos circulating on Chinese social media are getting wilder and wilder… here in this video 🇨🇳 Unitree humanoid robot soldiers in that “CMG 2026 Spring Festival Gala” outfit are defeating the US military à la The Avengers..

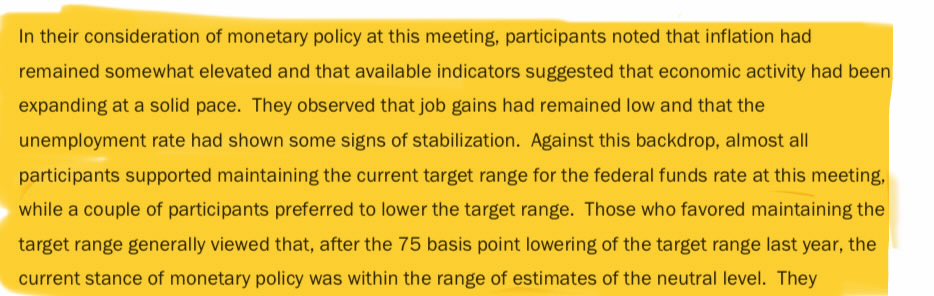

𝗙𝗢𝗠𝗖 𝗠𝗶𝗻𝘂𝘁𝗲𝘀: 𝗧𝗵𝗲 𝗛𝗮𝘄𝗸𝗶𝘀𝗵 𝗥𝗲𝗮𝗹𝗶𝘁𝘆 𝗼𝗳 𝟮𝟬𝟮𝟲 🦅

Reading FOMC minutes (𝑟𝑒𝑙𝑒𝑎𝑠𝑒𝑑 𝐹𝑒𝑏 18 𝑓𝑜𝑟 𝑡ℎ𝑒 𝐽𝑎𝑛 27-28 𝑚𝑒𝑒𝑡𝑖𝑛𝑔) reveals a challenging environment for risk assets in the coming year.

The FED is signaling that meaningful monetary easing is unlikely! This is anchoring us in a regime of restrictive policy and structural uncertainty.

🗝️ 𝗞𝗲𝘆 𝗧𝗮𝗸𝗲𝗮𝘄𝗮𝘆𝘀

• 𝗘𝗰𝗼𝗻𝗼𝗺𝗶𝗰 𝗚𝗿𝗼𝘄𝘁𝗵: GDP revised up and labor market stable.

• 𝗣𝗼𝗹𝗶𝗰𝘆 𝗣𝗮𝘁𝗵: Neutral stance.

only 𝟭–𝟮 𝗰𝘂𝘁𝘀 expected in 𝟮𝟬𝟮𝟲.

• 𝗜𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗗𝗿𝗶𝘃𝗲𝗿𝘀: Tariffs boosting core goods, late-2025 data skewed by shutdown.

• 𝗦𝘆𝘀𝘁𝗲𝗺𝗶𝗰 𝗥𝗶𝘀𝗸: High hedge fund leverage + mortgage refi market frozen by high rates despite Fannie/Freddie MBS purchases.

Hawkish baseline. Structural repricing of risk.

📊 𝗥𝗮𝘁𝗲𝘀 𝗦𝘁𝗮𝘆 𝗛𝗶𝗴𝗵𝗲𝗿 𝗳𝗼𝗿 𝗟𝗼𝗻𝗴𝗲𝗿

The Fed has revised GDP forecasts upward, signaling a surprisingly resilient economy.

Projections now indicate only 𝟭 𝗼𝗿 𝟮 𝗿𝗮𝘁𝗲 𝗰𝘂𝘁𝘀 for the entirety of 𝟮𝟬𝟮𝟲,

keeping the policy range at what officials currently consider "neutral."

Inflation is expected to stabilize but remain elevated with official forecasts ticking higher after a gov shutdown artificially understated November and December prints.

(we will see if Truflation proves more accurate)

📉 𝗬𝗶𝗲𝗹𝗱 𝗖𝘂𝗿𝘃𝗲 𝗦𝘁𝗲𝗲𝗽𝗲𝗻𝗶𝗻𝗴 𝗮𝗻𝗱 𝗦𝘆𝘀𝘁𝗲𝗺𝗶𝗰 𝗙𝗿𝗶𝗰𝘁𝗶𝗼𝗻

The spread between long and short-term rates is visibly widening… with long-term Treasuries climbing while the short end remains flat!

This dynamic highlights deep Fed concerns over debt sustainability and longer-term terminal inflation.

Meanwhile the labor market is stabilizing after a cooling period giving the committee cover to hold rates steady while continuing to roll over maturing Treasuries and purchase T-bills.

🧱 𝗔 𝗦𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗮𝗹 𝗛𝗲𝗮𝗱𝘄𝗶𝗻𝗱 𝗳𝗼𝗿 𝗥𝗶𝘀𝗸

This is not a temporary pause it is a structural adjustment to sticky inflation driven by core goods and Trump administration tariffs, even as housing services finally cool.

The Fed is acutely aware of financial vulnerabilities… specifically flagging the dangerous buildup of leverage among hedge funds and life insurance companies!

Short-term rate cuts are highly improbable absent a severe macroeconomic shock.

This is leaving Bitcoin and risk assets fighting a persistent liquidity headwind amid deep geopolitical uncertainty!

#Macro #FOMC #Fed

𝗕𝗜𝗧𝗖𝗢𝗜𝗡 𝗨𝗣𝗗𝗔𝗧𝗘 : 𝗦𝘂𝗿𝘃𝗶𝘃𝗶𝗻𝗴 𝘁𝗵𝗲 𝗕𝗼𝗿𝗲𝗱𝗼𝗺 𝘁𝗼 𝗕𝘂𝘆 𝘁𝗵𝗲 𝗕𝗼𝘁𝘁𝗼𝗺

🐻

We are in a confirmed Bear Market nothing new….

The primary driver of losses right now is not price collapse, but boredom.

Retail are forcing capital into a statistically negative environment simply to feel active… donating liquidity in a zone designed to chop them up. 🪚

🚫 𝗧𝗵𝗲 "𝗡𝗼-𝗚𝗼 𝗭𝗼𝗻𝗲" 𝗶𝘀 𝗮 𝗧𝗿𝗮𝗽 𝗳𝗼𝗿 𝗧𝗼𝘂𝗿𝗶𝘀𝘁𝘀

Trading above 𝟲𝟬𝗸 is currently negative EV.

This range is a volatility vacuum, designed to bleed impatient capital through chop and fake-outs.

Most participants are losing money here because they lack the discipline to do nothing.

This is the time to be strategic, to be patient and letting the tourists fight over scraps while the chart paints a clear roadmap for the next 𝟮 𝘆𝗲𝗮𝗿𝘀.

🎯 𝗧𝗵𝗲 𝗦𝗻𝗶𝗽𝗲𝗿 𝗘𝗻𝘁𝗿𝘆: 𝗧𝗮𝗰𝘁𝗶𝗰𝗮𝗹 𝗕𝗼𝘂𝗻𝗰𝗲 𝗣𝗹𝗮𝘆

Entry at 𝟱𝟵𝗸 is strictly a 𝘁𝗲𝗰𝗵𝗻𝗶𝗰𝗮𝗹 𝘁𝗿𝗮𝗱𝗲, not a marriage.

It is highly lucrative if timed correctly, but it is a swing trade, not a lifestyle. Risk management here must be tight.

🏦 𝗧𝗵𝗲 𝗩𝗮𝘂𝗹𝘁 𝗘𝗻𝘁𝗿𝘆: 𝗧𝗵𝗲 𝗖𝘆𝗰𝗹𝗶𝗰𝗮𝗹 𝗕𝗼𝘁𝘁𝗼𝗺

The real opportunity lies around the 𝟱𝟬𝗸 𝗥𝗲𝗴𝗶𝗼𝗻. (Maybe even below but let’s not be too greedy!)

This is the macro target where I intend to deploy 𝘀𝗲𝗿𝗶𝗼𝘂𝘀 𝘀𝗶𝘇𝗲 for the next bull cycle.

This is not a trade it is long-term positioning for a multi-year horizon.

⏳ 𝗣𝗮𝘁𝗶𝗲𝗻𝗰𝗲 𝗶𝘀 𝘁𝗵𝗲 𝗢𝗻𝗹𝘆 𝗥𝗲𝗺𝗮𝗶𝗻𝗶𝗻𝗴 𝗘𝗱𝗴𝗲

The market will likely give us these prices, but not before it makes you wait until you are disgusted.

The algorithm of a bear market is designed to exhaust your patience before it fills your bids.

The question is not if the price will get there, but whether you will still have capital left to deploy when it does…

𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝘆: Have a clear plan and do nothing until the price meets your plan.

➡️ Discipline over activity. Execution over emotion.

Two months ago at $89k everyone was screaming for a Supercycle. I warned it was a liquidity trap.

We are currently sitting at $66k

Entering in the "Next Support Zone" I outlined in my December post.

The macro damage looks worst than anticipated in December, we are dropping faster than I could have expected.

I believe the cycle bottom is lower but right now I’m looking at $59k

Despite the bearish structure, the Risk:Reward for a rebound at $59k is now heavily in favor of the bulls.

Not calling a bottom but calling a bounce hard to ignore.

NFA

#bitcoin #btc

𝗖𝗲𝗻𝘁𝗿𝗮𝗹 𝗕𝗮𝗻𝗸 𝗚𝗼𝗹𝗱 𝗗𝗲𝗺𝗮𝗻𝗱: 𝗦𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗮𝗹 𝗦𝗵𝗶𝗳𝘁 𝗼𝗿 𝗖𝘆𝗰𝗹𝗶𝗰𝗮𝗹 𝗦𝗼𝗳𝘁𝗲𝗻𝗶𝗻𝗴? 🏦

The 2025 data regarding official sector gold accumulation has arrived. While headline volumes have retreated from record highs, a longer-term view reveals a fundamental change in the baseline demand function for sovereign reserves.

🔵 𝗣𝗿𝗲𝗹𝗶𝗺𝗶𝗻𝗮𝗿𝘆 𝟮𝟬𝟮𝟱 𝗗𝗮𝘁𝗮 𝗦𝗵𝗼𝘄𝘀 𝟴𝟲𝟯.𝟮 𝗧𝗼𝗻𝗻𝗲𝘀 𝗼𝗳 𝗗𝗲𝗺𝗮𝗻𝗱 📉

World Gold Council estimates central bank demand reached 𝟴𝟲𝟯.𝟮 tonnes in 2025.

This figure represents a 𝟮𝟭% decline from the 𝟮𝟬𝟮𝟰 record of 𝟭,𝟬𝟵𝟮.𝟰 tonnes.

While this data is preliminary and likely to be revised upward as lagging institutions report, it currently sits below the psychological 𝟭,𝟬𝟬𝟬-tonne threshold.

🔵 𝗖𝘂𝗿𝗿𝗲𝗻𝘁 𝗕𝘂𝘆𝗶𝗻𝗴 𝗥𝗲𝗺𝗮𝗶𝗻𝘀 𝗗𝗼𝘂𝗯𝗹𝗲 𝘁𝗵𝗲 𝗣𝗿𝗲-𝟮𝟬𝟮𝟮 𝗔𝘃𝗲𝗿𝗮𝗴𝗲 ⚖️

To determine if this is a bearish signal, we must compare the current run rate to historical averages.

Between 𝟮𝟬𝟭𝟬 and 𝟮𝟬𝟮𝟭, central bank demand averaged 𝟰𝟳𝟯 tonnes per year.

Since 𝟮𝟬𝟮𝟮, a new regime has emerged. The four-year average (including 2025) now sits near 𝟭,𝟬𝟮𝟭 tonnes.

Even with the year-over-year decline, 𝟮𝟬𝟮𝟱 demand remains nearly double the pre-2022 average.

This marks the 𝟭𝟲𝘁𝗵 consecutive year of net buying from the official sector.

The market impact remains evident, with gold appreciating +𝟰𝟲% against the Euro over the same period.

🔵 𝗦𝗼𝘃𝗲𝗿𝗲𝗶𝗴𝗻 𝗥𝗲𝘀𝗲𝗿𝘃𝗲𝘀 𝗔𝗿𝗲 𝗨𝗻𝗱𝗲𝗿𝗴𝗼𝗶𝗻𝗴 𝗮 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗥𝗲𝗽𝗿𝗶𝗰𝗶𝗻𝗴 🌍

The data suggests we are witnessing a structural repricing of sovereign reserves rather than a fleeting trend.

The failure to break the 𝟮𝟬𝟮𝟰 record is a cyclical normalization, not a reversal of the thesis.

We have moved from a decade of tactical allocation (averaging <𝟱𝟬𝟬 tonnes) to a strategic era of accumulation (averaging >𝟴𝟱𝟬 tonnes).

This creates a persistent, non-price-sensitive bid underneath the market.

The "floor" for central bank demand has effectively shifted upward, driven by geopolitical fragmentation and a desire for neutral reserve assets.

🔵 𝟭𝟲 𝗬𝗲𝗮𝗿𝘀 𝗼𝗳 𝗔𝗰𝗰𝘂𝗺𝘂𝗹𝗮𝘁𝗶𝗼𝗻 𝗖𝗼𝗻𝗳𝗶𝗿𝗺𝘀 𝘁𝗵𝗲 𝗦𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗮𝗹 𝗙𝗹𝗼𝗼𝗿 🧱

• 𝟮𝟬𝟮𝟱 𝗗𝗲𝗺𝗮𝗻𝗱: 𝟴𝟲𝟯.𝟮 tonnes (preliminary).

• 𝟮𝟬𝟮𝟰 𝗥𝗲𝗰𝗼𝗿𝗱: 𝟭,𝟬𝟵𝟮.𝟰 tonnes.

• 𝗣𝗿𝗲-𝟮𝟬𝟮𝟮 𝗔𝘃𝗲𝗿𝗮𝗴𝗲: 𝟰𝟳𝟯 tonnes.

• 𝗣𝗼𝘀𝘁-𝟮𝟬𝟮𝟮 𝗔𝘃𝗲𝗿𝗮𝗴𝗲: 𝟭,𝟬𝟮𝟭 tonnes.

• 𝗦𝘁𝗿𝗲𝗮𝗸: 𝟭𝟲 years of net accumulation.

➡️ Cyclical variance. Structural accumulation.

#Gold #CentralBanks #GoldDemand

🇨🇳 𝗠𝗔𝗥𝗞𝗘𝗧 𝗔𝗟𝗘𝗥𝗧: 𝗧𝗵𝗲 "𝗖𝗵𝗶𝗻𝗮 𝗣𝘂𝘁" 𝗶𝘀 𝗩𝗮𝗻𝗶𝘀𝗵𝗶𝗻𝗴 𝗳𝗼𝗿 𝟳 𝗗𝗮𝘆𝘀

The Shanghai Gold Exchange (SGE) goes dark for Lunar New Year. Here is why this matters for your positions:

🗓️ 𝗗𝗮𝘁𝗲𝘀: Feb 15 – Feb 23, 2026

🔓 𝗦𝘁𝗮𝘁𝘂𝘀: Market resumes Feb 24.

𝗥𝗶𝘀𝗸: 📉

For one full week, the world's largest physical buyer leaves the building. We are moving from a bilateral market (Physical + Paper) to a unilateral Western paper market.

𝗪𝗵𝗮𝘁 𝘁𝗼 𝗲𝘅𝗽𝗲𝗰𝘁:

1️⃣ 𝗟𝗕𝗠𝗔 & 𝗖𝗢𝗠𝗘𝗫 𝘁𝗮𝗸𝗲𝗼𝘃𝗲𝗿: Without the SGE arbitrage bid, price discovery happens entirely in London & NY.

2️⃣ 𝗟𝗼𝘄𝗲𝗿 𝗥𝗲𝘀𝗶𝘀𝘁𝗮𝗻𝗰𝗲: Western shorts face no threat of physical delivery from the East.

3️⃣ 𝗩𝗼𝗹𝗮𝘁𝗶𝗹𝗶𝘁𝘆: Expect "Stop-hunts" and downside pressure in thin liquidity.

𝗢𝗽𝗽𝗼𝗿𝘁𝘂𝗻𝗶𝘁𝘆: 🐂

History suggests this is a seasonal liquidity gap, not a structural break.

• 𝗦𝗲𝘁𝘂𝗽: Price softness during NY/London overlap.

• 𝗣𝗹𝗮𝘆: Watch for the "Holiday Discount" before Chinese desks reopen and the structural bid returns.

Seasonal silence. Tactical noise.

#Gold #XAUUSD #SGE

𝗧𝗵𝗲 𝗦𝗶𝗹𝘃𝗲𝗿 𝗗𝗶𝘀𝗰𝗼𝗻𝗻𝗲𝗰𝘁: 𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗮𝗹 𝗗𝗲𝗺𝗮𝗻𝗱 𝘃𝘀. 𝗡𝘂𝗺𝗶𝘀𝗺𝗮𝘁𝗶𝗰 𝗟𝗶𝗾𝘂𝗶𝗱𝗶𝘁𝘆 🪙

Silver prices are pushing toward multi-decade highs but the physical market is exhibiting a structural dislocation.

The divergence between rising spot prices and collapsing premiums suggests a fundamental shift in how the metal is being monetized.

🔵 𝗦𝗽𝗼𝘁 𝗣𝗿𝗶𝗰𝗲𝘀 𝗦𝘂𝗿𝗴𝗲 𝗪𝗵𝗶𝗹𝗲 𝗣𝗵𝘆𝘀𝗶𝗰𝗮𝗹 𝗣𝗿𝗲𝗺𝗶𝘂𝗺𝘀 𝗖𝗼𝗹𝗹𝗮𝗽𝘀𝗲 📉

Silver has experienced significant appreciation driven by 𝗶𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗮𝗹 𝗱𝗲𝗺𝗮𝗻𝗱 (specifically solar and electronics) and inflationary hedging.

Paradoxically while the spot price is rising, 𝗱𝗲𝗮𝗹𝗲𝗿 𝗽𝗿𝗲𝗺𝗶𝘂𝗺𝘀 have collapsed.

In a rare market inversion, common-date silver coins are frequently trading 𝗮𝘁 𝗼𝗿 𝗲𝘃𝗲𝗻 𝗯𝗲𝗹𝗼𝘄 𝘁𝗵𝗲𝗶𝗿 𝗺𝗲𝗹𝘁 𝘃𝗮𝗹𝘂𝗲.

The velocity of the price rise has outpaced buyer demand, compressing the spread between the paper price and the physical product.

🔵 𝗜𝗻𝘁𝗿𝗶𝗻𝘀𝗶𝗰 𝗠𝗲𝘁𝗮𝗹 𝗩𝗮𝗹𝘂𝗲 𝗜𝘀 𝗢𝘃𝗲𝗿𝘁𝗮𝗸𝗶𝗻𝗴 𝗖𝗼𝗹𝗹𝗲𝗰𝘁𝗼𝗿 𝗣𝗿𝗲𝗺𝗶𝘂𝗺 🏭

We are witnessing a "Melt Value Flip."

The intrinsic metal value of common silver coins now exceeds their numismatic (collector) value.

This creates immediate "𝗺𝗲𝗹𝘁𝗶𝗻𝗴 𝗽𝗿𝗲𝘀𝘀𝘂𝗿𝗲."

Historic coins are being diverted from the collector market to refiners to be melted down for industrial use.

This permanently removes supply from the numismatic ecosystem, converting history into industrial feedstock.

🔵 𝗠𝗮𝗿𝗸𝗲𝘁 𝗦𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲 𝗜𝘀 𝗦𝗵𝗶𝗳𝘁𝗶𝗻𝗴 𝗳𝗿𝗼𝗺 𝗛𝗼𝗯𝗯𝘆𝗶𝘀𝘁 𝘁𝗼 𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗮𝗹 🔄

Dealers are facing liquidity squeezes and effectively widening spreads to manage volatility risk.

Many are bidding 𝗯𝗲𝗹𝗼𝘄 𝗺𝗲𝗹𝘁 𝘃𝗮𝗹𝘂𝗲 to protect against sudden drawdowns.

Simultaneously, the entry price for hobbyists has shifted from accessible levels (𝟮𝟬–𝟯𝟬) to restrictive highs (~𝟭𝟬𝟬).

This creates a high barrier to entry, forcing a transition toward a "new normal" of 𝗵𝗶𝗴𝗵𝗲𝗿-𝘃𝗮𝗹𝘂𝗲, 𝗹𝗼𝘄𝗲𝗿-𝘃𝗼𝗹𝘂𝗺𝗲 trading.

🔵 𝗛𝗶𝘀𝘁𝗼𝗿𝗶𝗰𝗮𝗹 𝗣𝗮𝗿𝗮𝗹𝗹𝗲𝗹𝘀 𝗦𝘂𝗴𝗴𝗲𝘀𝘁 𝗮 𝗥𝗼𝘁𝗮𝘁𝗶𝗼𝗻 𝗶𝗻𝘁𝗼 𝗥𝗮𝗿𝗶𝘁𝗶𝗲𝘀 ⏳

Analysts note strong parallels to the 𝟭𝟵𝟴𝟬 silver boom.

Historically, profits from a massive run-up in bullion eventually rotate back into 𝗿𝗮𝗿𝗲, 𝗵𝗶𝗴𝗵-𝗴𝗿𝗮𝗱𝗲 𝗰𝗼𝗶𝗻𝘀.

These numismatic assets have remained relatively stagnant during the spot surge.

If history repeats, the stabilization of the bullion market could trigger a repricing of rare numismatics as capital seeks value in scarcity rather than just weight.

🔵 𝗞𝗲𝘆 𝗜𝗺𝗽𝗹𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀 𝗳𝗼𝗿 𝗣𝗵𝘆𝘀𝗶𝗰𝗮𝗹 𝗔𝗹𝗹𝗼𝗰𝗮𝘁𝗼𝗿𝘀 📝

• 𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗮𝗹 𝗗𝗲𝗺𝗮𝗻𝗱: Driving spot price, not retail speculation.

• 𝗦𝘂𝗽𝗽𝗹𝘆 𝗗𝗲𝘀𝘁𝗿𝘂𝗰𝘁𝗶𝗼𝗻: Historic inventory is being melted.

• 𝗟𝗶𝗾𝘂𝗶𝗱𝗶𝘁𝘆: Dealer spreads are widening to manage risk.

• 𝗖𝘆𝗰𝗹𝗲 𝗪𝗮𝘁𝗰𝗵: Watch for capital rotation from bullion into rare numismatics.

➡️Short-term dislocation. Long-term rotation.

#Silver #SilverSqueeze #Macro

𝗖𝗲𝗻𝘁𝗿𝗮𝗹 𝗕𝗮𝗻𝗸 𝗚𝗼𝗹𝗱 𝗗𝗲𝗺𝗮𝗻𝗱: 𝗦𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗮𝗹 𝗦𝗵𝗶𝗳𝘁 𝗼𝗿 𝗖𝘆𝗰𝗹𝗶𝗰𝗮𝗹 𝗦𝗼𝗳𝘁𝗲𝗻𝗶𝗻𝗴? 🏦

The 2025 data regarding official sector gold accumulation has arrived. While headline volumes have retreated from record highs, a longer-term view reveals a fundamental change in the baseline demand function for sovereign reserves.

🔵 𝗣𝗿𝗲𝗹𝗶𝗺𝗶𝗻𝗮𝗿𝘆 𝟮𝟬𝟮𝟱 𝗗𝗮𝘁𝗮 𝗦𝗵𝗼𝘄𝘀 𝟴𝟲𝟯.𝟮 𝗧𝗼𝗻𝗻𝗲𝘀 𝗼𝗳 𝗗𝗲𝗺𝗮𝗻𝗱 📉

World Gold Council estimates central bank demand reached 𝟴𝟲𝟯.𝟮 tonnes in 2025.

This figure represents a 𝟮𝟭% decline from the 𝟮𝟬𝟮𝟰 record of 𝟭,𝟬𝟵𝟮.𝟰 tonnes.

While this data is preliminary and likely to be revised upward as lagging institutions report, it currently sits below the psychological 𝟭,𝟬𝟬𝟬-tonne threshold.

🔵 𝗖𝘂𝗿𝗿𝗲𝗻𝘁 𝗕𝘂𝘆𝗶𝗻𝗴 𝗥𝗲𝗺𝗮𝗶𝗻𝘀 𝗗𝗼𝘂𝗯𝗹𝗲 𝘁𝗵𝗲 𝗣𝗿𝗲-𝟮𝟬𝟮𝟮 𝗔𝘃𝗲𝗿𝗮𝗴𝗲 ⚖️

To determine if this is a bearish signal, we must compare the current run rate to historical averages.

Between 𝟮𝟬𝟭𝟬 and 𝟮𝟬𝟮𝟭, central bank demand averaged 𝟰𝟳𝟯 tonnes per year.

Since 𝟮𝟬𝟮𝟮, a new regime has emerged. The four-year average (including 2025) now sits near 𝟭,𝟬𝟮𝟭 tonnes.

Even with the year-over-year decline, 𝟮𝟬𝟮𝟱 demand remains nearly double the pre-2022 average.

This marks the 𝟭𝟲𝘁𝗵 consecutive year of net buying from the official sector.

The market impact remains evident, with gold appreciating +𝟰𝟲% against the Euro over the same period.

🔵 𝗦𝗼𝘃𝗲𝗿𝗲𝗶𝗴𝗻 𝗥𝗲𝘀𝗲𝗿𝘃𝗲𝘀 𝗔𝗿𝗲 𝗨𝗻𝗱𝗲𝗿𝗴𝗼𝗶𝗻𝗴 𝗮 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗥𝗲𝗽𝗿𝗶𝗰𝗶𝗻𝗴 🌍

The data suggests we are witnessing a structural repricing of sovereign reserves rather than a fleeting trend.

The failure to break the 𝟮𝟬𝟮𝟰 record is a cyclical normalization, not a reversal of the thesis.

We have moved from a decade of tactical allocation (averaging <𝟱𝟬𝟬 tonnes) to a strategic era of accumulation (averaging >𝟴𝟱𝟬 tonnes).

This creates a persistent, non-price-sensitive bid underneath the market.

The "floor" for central bank demand has effectively shifted upward, driven by geopolitical fragmentation and a desire for neutral reserve assets.

🔵 𝟭𝟲 𝗬𝗲𝗮𝗿𝘀 𝗼𝗳 𝗔𝗰𝗰𝘂𝗺𝘂𝗹𝗮𝘁𝗶𝗼𝗻 𝗖𝗼𝗻𝗳𝗶𝗿𝗺𝘀 𝘁𝗵𝗲 𝗦𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗮𝗹 𝗙𝗹𝗼𝗼𝗿 🧱

• 𝟮𝟬𝟮𝟱 𝗗𝗲𝗺𝗮𝗻𝗱: 𝟴𝟲𝟯.𝟮 tonnes (preliminary).

• 𝟮𝟬𝟮𝟰 𝗥𝗲𝗰𝗼𝗿𝗱: 𝟭,𝟬𝟵𝟮.𝟰 tonnes.

• 𝗣𝗿𝗲-𝟮𝟬𝟮𝟮 𝗔𝘃𝗲𝗿𝗮𝗴𝗲: 𝟰𝟳𝟯 tonnes.

• 𝗣𝗼𝘀𝘁-𝟮𝟬𝟮𝟮 𝗔𝘃𝗲𝗿𝗮𝗴𝗲: 𝟭,𝟬𝟮𝟭 tonnes.

• 𝗦𝘁𝗿𝗲𝗮𝗸: 𝟭𝟲 years of net accumulation.

➡️ Cyclical variance. Structural accumulation.

#Gold #CentralBanks #GoldDemand

@KobeissiLetter People get too distracted by a misquoted soundbite while ignoring the mechanical reality of the "Warsh Vacuum" and what it implies.

https://t.co/S7cCFtUANy

⚔️ 𝐁𝐈𝐓𝐂𝐎𝐈𝐍 𝐔𝐏𝐃𝐀𝐓𝐄: “𝐖𝐚𝐫 𝐨𝐟 𝐓𝐰𝐨 𝐊𝐞𝐯𝐢𝐧𝐬” 𝐎𝐯𝐞𝐫 — 𝐇𝐞𝐫𝐞’𝐬 𝐖𝐡𝐚𝐭 𝐈𝐭 𝐌𝐞𝐚𝐧𝐬 𝐟𝐨𝐫 𝐁𝐢𝐭𝐜𝐨𝐢𝐧

Most of you did.. or did not … pay attention to who replaced Powell.

Before the K. Warsh announcement, the market assumed: “New Chair = Fresh Pump.”

That missed the point.

This appointment is the single most important monetary policy shift since 2008.

Kevin Hassett (𝐓𝐡𝐞 𝐏𝐫𝐢𝐧𝐭𝐞𝐫) was traded for

Kevin Warsh (𝐓𝐡𝐞 𝐕𝐚𝐜𝐮𝐮𝐦).

🔵 𝐓𝐡𝐞 𝐓𝐡𝐞𝐬𝐢𝐬 𝐭𝐡𝐞 𝐌𝐚𝐫𝐤𝐞𝐭 𝐁𝐨𝐮𝐠𝐡𝐭 💸

Before the announcement, markets priced in Hassett.

He represented technological optimism, a continuation of the credit cycle where stablecoins and cheap debt keep the wheels turning.

Under that regime, liquidity expands… and Bitcoin flies.

🔵 𝐓𝐡𝐞 𝐑𝐞𝐚𝐥𝐢𝐭𝐲 𝐖𝐞’𝐫𝐞 𝐆𝐞𝐭𝐭𝐢𝐧𝐠 🧊

Warsh is different. He’s a disciple of sound money.

He doesn’t believe the Fed’s job is to keep the S&P 500 at all-time highs.

He believes the Fed’s $𝟔.𝟓𝐓 balance sheet is a systemic risk that needs to be cut.

🔵 𝐓𝐡𝐞 𝐌𝐞𝐜𝐡𝐚𝐧𝐢𝐬𝐦 𝐨𝐟 𝐭𝐡𝐞 𝐁𝐓𝐂 𝐂𝐫𝐚𝐬𝐡 💥

Why does this matter for your bags?

Bitcoin has a 0.43 correlation with Global M2.

It is a liquidity sponge.

• Hassett would have turned the tap ON

• Warsh is here to turn the tap OFF

Warsh appears focused on extracting ~$𝟏𝐓 from the banking system to restore Dollar credibility versus the Yuan and Gold.

You cannot have a shrinking money supply and a parabolic crypto market at the same time.

The math does not work.

🔵 𝐓𝐡𝐞 𝐖𝐚𝐫𝐬𝐡 𝐏𝐚𝐫𝐚𝐝𝐨𝐱 ⚖️

Here’s the nuance most are missing: Warsh is not anti-Bitcoin.

He sees Bitcoin as a thermometer: a warning signal when government spending runs hot.

But here’s the problem:

A thermometer doesn’t heat the house.

By fixing the Dollar and halting debasement, Warsh lowers the temperature.

He makes the Dollar attractive again.

A stronger Dollar is kryptonite for asset prices… at least in the short term.

🔵 𝐁𝐓𝐂 𝐂𝐡𝐨𝐩 𝐢𝐬 𝐖𝐡𝐚𝐭 𝐂𝐨𝐦𝐞𝐬 𝐍𝐞𝐱𝐭 🪚

A chop is forming between $𝟓𝟗𝐤 – $𝟕𝟑𝐤

(upper wicks could stretch all the way toward ~$𝟖𝟒𝐤).

Big money is distributing to retail that still believes the “Fed Put” is coming.

It isn’t.

Warsh will likely chose Austerity over Debasement.

➡️ 𝐌𝐲 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲 🎯

I respect the mechanism. I’m not fighting the Fed.

A range is forming where patience will be tested and leverage will be punished possibly for weeks or months!

After the chop, the liquidity drain likely pushes price through the current floor ($𝟓𝟗𝐤).

I have some bids near 59, but I’m waiting for repricing in the $𝟒𝟖𝐤 – $𝟓𝟒𝐤 zone before deploying serious capital

#bitcoin #fed #warsh

𝙳𝚒𝚜𝚌𝚕𝚊𝚒𝚖𝚎𝚛: 𝙽𝚘 𝚏𝚒𝚗𝚊𝚗𝚌𝚒𝚊𝚕 𝚊𝚍𝚟𝚒𝚌𝚎. 𝙹𝚞𝚜𝚝𝚎 𝚜𝚑𝚊𝚛𝚒𝚗𝚐 𝚖𝚢 𝚊𝚗𝚊𝚕𝚢𝚜𝚒𝚜. 𝙳𝚘 𝚢𝚘𝚞𝚛 𝚘𝚠𝚗 𝚍𝚞𝚎 𝚍𝚒𝚕𝚒𝚐𝚎𝚗𝚌𝚎.