It's official.

MicroStrategy, $MSTR, is now facing its biggest unrealized loss in history, at -$10.8 billion.

In other words, after 6 years of buying Bitcoin, the company is now down -17% on its position.

By comparison, the S&P 500 is up +116% over this same timeframe.

Since MicroStrategy sold 32 Bitcoin at $77,135 per coin, their positions has lost -$11.8 billion in value.

This puts MicroStrategy's stock, $MSTR, down -77% since its record high.

Bear market is an understatement.

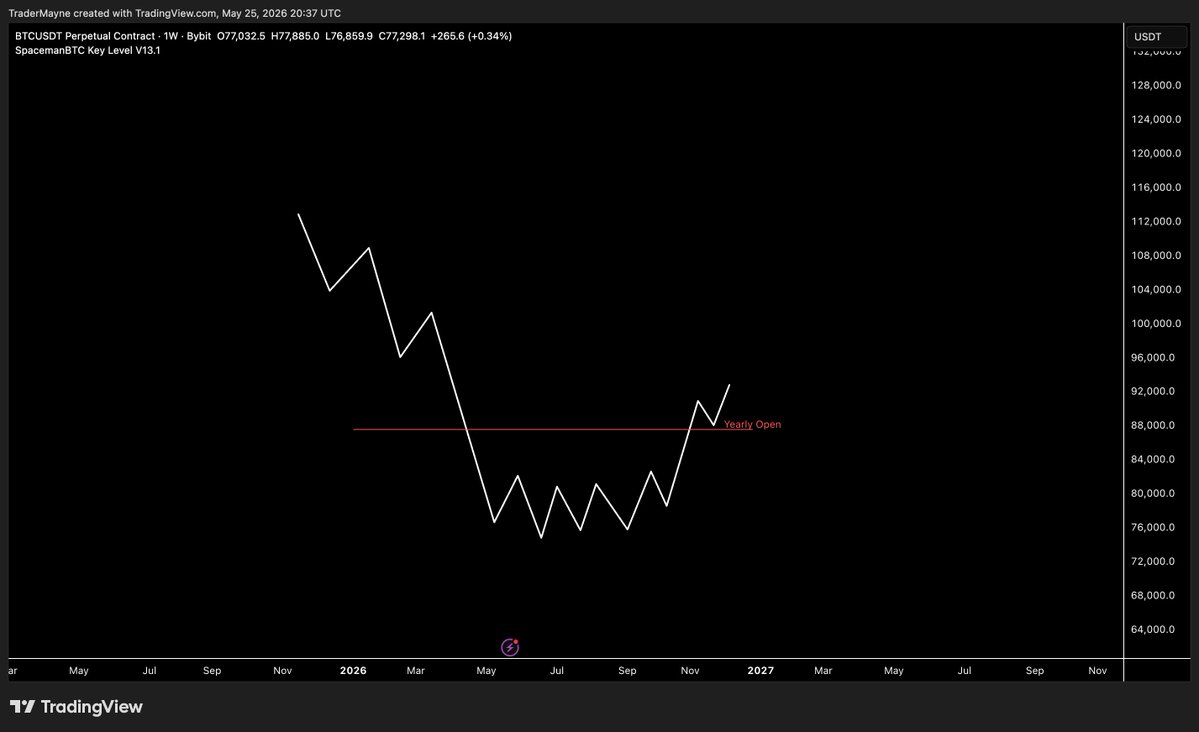

Plausible path:

Bitcoin forms a low in June (like it did in June 2018 and June 2022).

BTC rallies in July

SPX correction later in year which allows Bitcoin to finally bottom (most likely October)

Four year cycle wins again

Buy $10K of BTC in 2019 and hold: ~$181K today.

Do the exact same thing but skip every Thursday (out at the open, back in Friday, no fees): ~$687K.

One day off a week. 3.8x the money.

Thursdays simply suck. Ima buy the dip on Friday. See you guys when my Claude credits reset.

There have been a few key changes in crypto market structure.

I've written about this topic before but I found myself carrying some stale epistemological baggage about how the market used to be versus what it is at the moment, so thought I'd share.

1. More coins than ever before and the barrier to creating new coins has never been lower.

2. More competition for the hot ball of money (AI, semis, tech, even commodities) and instruments like 0DTE options - all of which are very attractive to normies.

3. Change in participant type and sophistication - ETFs, more tradfi shops, suits etc.

4. Normie flows that used to concentrate around a few CEXes and a limited token set have been fragmented by the infinite listings and existence of the trenches.

There are fewer normie flows, they're spread too thin, and it's difficult to come back to the casino if you get dumped on for holding longer than 15 seconds.

The main attractor to crypto used to be outsized, long-lasting, and well-distributed trend and momentum effects that were easy to access because there weren't that many venues or coins.

That's basically up only/alt season i.e. multi-month periods that were responsible for a disproportionate amount of a crypto trader's lifetime P&L.

A rising tide lifting all boats is an overused but appropriate analogy - it didn't really matter what coins you bought.

If you got the broader market conditions right, you'd enjoy significant uplift and basically get bailed out even if you made bad picks.

In the current paradigm you can't afford to make bad picks.

To be precise: in previous cycles if you got the conditions right but the assets wrong, you'd still make money but underperform. In the current cycle (even from the most recent BTC run) if you got conditions right but the assets wrong, you got shafted.

So asset selection went from a nice-to-have enhancer to one of the main drivers of returns, even if BTC is going up.

That's a pretty significant departure from what we've dealt with in the past

This type of dispersion is a symptom of the market maturing.

I think that's a net good thing and is likely to incentivise more intelligent token design, less ghost chain VC slop etc.

But that's a forward-looking view, and at the moment we're trapped in this awkward transition phase where the old rules don't really apply but we haven't figured out a new framework yet e.g. top N coins by market cap are still mostly shit vs quality.

Maybe I'm wrong and everything changes and we go back to the market-wide altseason paradigm when conditions are right. This could all be cyclical, but I think that's less compelling than before given the dispersion we saw on the way up too vs just to the downside.

I think it's a good time (especially with other markets and asset classes going crazy) to revisit where crypto sits in the speculative stack and how to approach it as the market is changing.

Cheers.

Even though I do think the stock market is a little out of touch with reality I think that it can still go higher.

“Large cap technology stocks are merely getting cheaper as they go up”

Our most frequently asked question right now:

"If oil prices are above $100/barrel and the Iran War isn't over, why are stocks at record highs?"

The answer to this question is simple.

The AI Revolution has simply become so large, that investors are viewing everything else as "noise."

Over the last few months, as large cap technology stocks traded flat then sharply lower amid the Iran War, the AI narrative only grew.

The Magnificent 7 companies are set to invest over $600 BILLION in AI this year alone.

And, as broader markets swept tech giants like Nvidia and Alphabet lower, these stocks reached their cheapest Forward P/E levels since 2019.

At the March 30th bottom, the S&P 500 Information Technology index was trading at just a 4% Forward P/E premium to the S&P 500, the lowest since January 2019.

Tech stocks became cheaper than the average S&P 500 stock for the first time since 2017.

Nvidia, for example, is now trading at just a ~26x Forward P/E multiple, even as it is back at record highs. Walmart? 43x. Costco? 46x.

The reality is that many large cap technology stocks are merely getting cheaper as they go up. And when they go down, they become remarkably cheap.

We are in the biggest technological revolution in modern history, and even $100 oil, a 4.40% 10Y Yield, and rate cuts priced out until 2027 are unable to derail the train.

Asset owners will continue to win.

Absolutely incredible:

The US 20Y Note Yield is now above 5.00%.

At the current pace, we will have 7% mortgages and $4.00 gas prices this week.

Talk about a turn of events.