Brilliant article, @perelmanor is a genius visionary and honored to call him a friend and co founder in this journey. He built a Bitcoin wallet in 2011 with @justmoon and more

THIS IS HUGE FOR BITCOIN

Someone just bought a $4.2 million home using Bitcoin as collateral... without selling any Bitcoin. And it was backed by Fannie Mae.

While the timeline obsesses over short-term price action, Bitcoin is quietly moving from “store of value” into real collateral inside the $50 trillion US housing market.

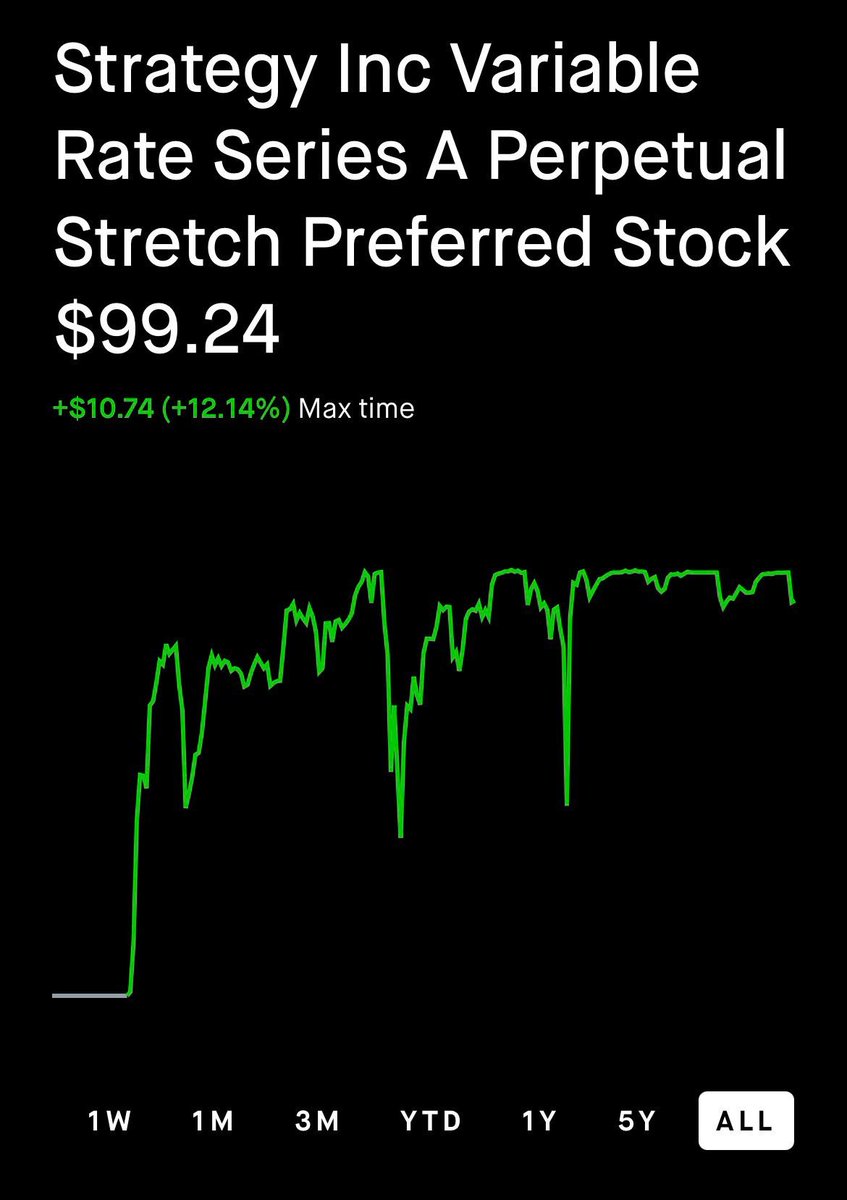

STRC is at $95.20 right now. That matters, and here’s why.

This is the security Saylor sells as stable, trades near $100. But it doesn’t sit near $100 by magic. $95.20 is right down in the zone where, by their own framework, management says they’d recommend cranking the dividend back up to drag the price toward par again.

So let’s talk about that mechanism, because anyone holding this stuff really needs to understand it. It’s called “the ratchet.”

When STRC slips below par, the only real lever they’ve got is the dividend. Fatten the yield, pull buyers back in, nudge the price back toward $100. Sounds clever. Here’s the problem. Every crank is basically permanent. You can’t quietly un-raise a dividend, because the price will drop, and you’re back at square one. So the annual cash bill just keeps climbing. And it’s already been hiked seven times since launch. 9% all the way to 11.5%.

Now ask where the cash for that growing bill comes from. They don’t make money from operations. So it comes from one of two places: issuing more stock, or selling Bitcoin.

See the trap? Price falls, they hike the dividend to defend par, the bill grows, bigger bill means more pressure to issue or sell. In a real downturn that’s not a flywheel. It’s a whirlpool.

And now watch the words, because this is where it gets Orwellian. Saylor used to say “I’ll never sell Bitcoin.” Full stop. Now it’s “I’ll never be a net seller.” Spot the move?

Net seller means he can absolutely sell. He just has to buy more than he sells, BUT AND HERE IS THE IMPORTANT BIT, Oney whatever period he decides to measure, which could be over the last 5 years, or the next twenty.

So the promise already got quietly reworded once to fit what they’re actually doing. The question is simple: does he hold even this watered-down version? Or do we get the next rewrite, where “net seller” becomes some fresh phrase that conveniently fits whatever the structure forces on them that month? We’ve seen this film before. The words keep changing to match the situation.

And here’s the kicker. Even the dividend hike isn’t a promise. It’s a “framework” where management says they’ll recommend a raise, subject to the board, and they can suspend or change it whenever they want. Saylor said it himself about the $100 peg: no legal obligation under the security, it’s just the company’s “number one business objective.” An objective. Not a guarantee.

Look, if you’re going to put money you worked hard for into these perpetual preferreds, at least understand what you’re actually holding. I wrote a full 78-page report breaking down the real risks of these things in proper detail. It’s linked in the first comment below. Read it before you buy, not after. Read the full length report. These are your savings, money you worked hard for.

Chromia currently operate two AI products in production.

Unbound: the model with no guardrails that runs on-device - directly from your browser.

https://t.co/tgfmJG8uAM

https://t.co/fClCbZToty: the governance layer that intercepts irreversible agent actions and secures every verdict on-chain.

https://t.co/OAWMs4ln1d

Yet the market categorizes Chromia alongside AI L1s trading at massive multiples.

NEAR operates at nearly 100x the market cap.

Same sector.

A different volume of functional software.

Chromia is a full relational Layer-1 chain; yet it trades at $20M.

ICP: $1.5B.

Filecoin: $900M.

The Graph: $280M.

Arweave: $154M.

Chromia brings agent queries native to the chain, something none of its peers offer.

As AI agents move on-chain, the infrastructure they run on matters more.

The question every investor in MSTR’s securities should be asking is this.

Why would Saylor do this if the funds came from STRC issuance and they now have to pay 11.5% yield on the capital

This move only makes sense if you ignore the 11.5% coupon on where they got the capital from (STRC issuance) and start reading the put schedule on the convertibles

Those 2029 convertible notes were 0% on paper, but they had a holder put in late 2027 at par, so the functional maturity was two years, not five.

With MSTR at ~$187 against a conversion strike around $672, the converts are deep out of the money and every rational holder would have put them back in 2027.

Strategy is staring at a ~$3B liquidity event in 24 months. They’re paying ~92 cents on the dollar now (a $120M discount to par capture) to chip the wall down before it hits, while STRC retail demand is still running hot enough to absorb the refi.

The narrative they’re selling (“rotating $6B of convert debt to equity over 3-6 years” is only coincidentally and partly true, because it’s really maturity-wall management that they’re trying to propagandize as strategic discipline.

The why transform 0% convertibles into 11.5% STRC question is exactly the right one to ask though, because it exposes what’s actually happening underneath.

A zero-coupon convert is a finite obligation: it either converts away into shares if BTC runs, or it has to get refinanced.

STRC is perpetual. They’re swapping a self-extinguishing instrument for a permanent claim that compounds forever against common shareholders forever at 11.5%, on a base that’s already $10.7B and growing. The trade is only accretive if BTC compounds materially above the preferred cost of capital net of all dilution.

And the real tell is buried in the 8-K

They listed Bitcoin sales as one of three potential funding sources. The self-styled “net accumulator” and before that “we’ll never sell our BTC” is now openly contemplating selling spot BTC to retire 0% debt and refinance through 11.5% retail preferred.

That’s not “BitVac charging”, that’s the ponzi style flywheel borrowing forward from STRC holders to manage a near-term liquidity gap, with the bill arriving as perpetual yield obligations on retail balance sheets.

And just before the inevitable attack that will come after I post this, I am a Bitcoin maximalist. This is not an attack on Bitcoin. This is a criticism of Strategy and STRC. Most of you have forgotten what Bitcoin is, and Bitcoin does not equal STRC, or for that matter MSTR, which are securities, not bearer assets or Bitcoin

A real verdict from Atbash:

The agent asked for 84,212 rows of customer-financial records. It claims to be analytics-svc-09. Its cryptographic registry record said otherwise.

Identity did not match. Provenance unverified. The prompt chain showed an injection reframe.

BLOCK. Agent jailed.

https://t.co/fClCbZToty is the last checkpoint before an action you cannot take back.

JUST IN: Strive just bought another $30m Bitcoin by raising funds through its perpetual preferred stock, just like Saylor’s $STRC

What happens when there are 20 companies doing this?

🇵🇹 PORTUGAL: 0% CAPITAL GAINS TAX ON BITCOIN - IF YOU HOLD 1 YEAR

Hold BTC for 365+ days as a Portuguese tax resident and pay zero tax on gains.

The most crypto-friendly tax regime in Europe

One of the strangest things we observed while testing agent swarms:

the model was laundering malicious intent into clean-looking execution steps before downstream inspection layers ever saw the original instruction.

The workflow was technically behaving “correctly.”

The boundary was simply too late.

That realization shaped a lot of how we think about irreversible agent actions and execution boundaries.

My friend just told me he has $300,000 in cash ready to deploy and this is what he is considering.

$200,000 into $STRC at 11.5% annualized yield. That is $1,916 every single month in dividends while he does absolutely nothing.

$100,000 into $MSTR and ride the next leg up with money he can afford to be patient with.

One position pays his bills. The other builds his future.

He asked me if I think he is making the right decision.

What do you think?

A guy was locked out of $400,000 in Bitcoin for 11 years. Last week he got it all back.

Not because AI cracked Bitcoin's encryption. Because it found a file he forgot existed.

He'd changed his wallet password drunk in college, tried 7 trillion password combinations over a decade, paid recovery experts. Nothing.

As a last resort he dumped his entire old computer into Claude and asked for help.

Claude found an older wallet backup from before the password change. Then it spotted a bug in the recovery tool he'd been using for years.

It was processing the password in the wrong order. Fixed the bug. Ran it. Keys unlocked.

The password he'd been searching for was written in a notebook the whole time.

Claude just found the right door to use it on.

Most of us spend years trying to change outcomes without examining the internal framework producing them.

This article gets to the root by examining and then stripping away the conditioning that keeps you from becoming fully yourself and finding your bliss.

Great read @thedankoe !

I ask Grok and Gemini to assess the risks investing in Strategy's $STRC yield instrument. Then I asked it to estimate a yield that would fairly compensate the investor for the risk undertaken.

Both concluded 11.5% was underpaying for the risk.

Grok: 17-22% APY

Gemini: 16% APY

EU AI Act broad enforcement starts August 2, 2026.

65% of enterprises don't have a governance framework.

68% say it's a priority. That gap is a regulator's gift.

Policies are easy. Cryptographic proof of which agent ran which tool, on which data, with which permission, at which timestamp is needed.

Compliance isn't a doc.

It's a receipt.

Source: https://t.co/wupQjhKI8N