The hidden Japan layer of the AI buildout, and how it flows to Korea, Taiwan and US tickers. An operator's read, not a desk. 20 yrs in JP hardware. NFA, DYOR

Why this account.

20 years building hardware and running factories across Korea, Japan, China and Vietnam.

Worked on a global tech giant's strategy (joint programs with Japanese and US tech leaders). 7 years on a Japanese board, building EV powertrain and power-electronics test systems. Ran factories and overseas units from Shenzhen to Europe. 5+ years running a global tech giant's tier-1 supplier in Vietnam. I still research motor efficiency.

Here is what those 20 years taught me.

AI didn't make atoms obsolete. It made them the bottleneck.

The buildout runs on things you have to manufacture: memory, power, substrates, motors, cooling. So the AI era quietly rewards the makers, the nations and firms with real manufacturing depth. Japan, Korea, Taiwan, and whoever else can actually build.

That is the moat I track: the hidden Japanese layer of the AI supply chain, and how it flows to Korea, Taiwan and US tickers.

Why I post here. I used X for years to learn. Now I want to give back what I see, and keep learning in the open. The sharpest reply beats silence.

My view, not financial advice. I will be wrong sometimes, and I will say so.

If you believe the AI era belongs to the makers, let's think out loud together.

Murata (6981.T) just filed its annual report, and it has one line it would rather you skipped.

Its "visible" half, the smartphone RF business everyone pictures when they hear "Japanese components," lost ¥26.5B this year.

The half nobody photographs, MLCC and capacitors, earned ¥315.1B in operating profit at a 26.8% margin. It is carrying the entire company.

And it is accelerating. Murata guides FY26 data-center capacitor sales +85 to 90% YoY, group operating profit +34.8% to ¥380B, on the back of an AI-server MLCC price hike.

Here is where it crosses the border. AI-server MLCC is not a Japanese monopoly, it is a Japan-Korea duopoly:

- Murata (6981.T) ~45%, the scale player

- Samsung Electro-Mechanics (009150.KS) ~40%, closing the gap (FY25 revenue ₩11.3T, +10%)

And the purest Japanese leverage is not Murata. It is Taiyo Yuden (6976.T): MLCC is ~70% of revenue, and FY25 net profit rose ~6.4x on AI-server demand, with a capacitor book-to-bill of 1.31. Highest concentration, highest beta.

But highest beta cuts both ways, and here is the part the hype skips. Taiyo Yuden is up ~357% YTD, ~7x off its low, near 157x earnings. Murata is up ~223%, ~5x off its low, near 84x. The leverage is real, and so is the fact that the market has already found all of it.

So the honest read is not "buy the cheap one." There is no cheap one. It is a map: scale plus the biggest profit inflection (Murata 6981.T, OP +34.8%, ~84x), the purest beta already pricing the whole cycle (Taiyo Yuden 6976.T, ~157x), and the Korean name closing the AI-server gap (SEMCO 009150.KS). Sizing, not discovery.

If you want actual discovery and not just sizing, it is not in the capacitor. It is one layer down: the dielectric powder and nickel electrode paste every one of these makers has to buy, a layer Japan quietly dominates, where the single purest name is not even listed. That is where the valuation gap still lives.

I am digging into that layer next.

메모리 테제(thesis)의 변화가 시작됨!

즉, 데이터센터(AIDC)--------> Physical AI로 ~

마이크론($MU)이 이번에 제대로 짚은 두 번째 곡선은 Physical AI. 한 번 파도 치고 끝나는 게 아니라, 수십 년 우상향하는 완전히 다른 구조입니다.

마이크론 CEO는 로보틱스를 "20년 성장 벡터"로 봅니다. 그 아래 실제 메모리 수요를 보면:

- 스마트폰 → 이미 16GB가 표준 (온디바이스 7B 모델)

- 전기차 → L4급 되면 차량당 수백GB까지 (자율 레벨을 따라 증가)

- 휴머노이드 로봇 → 고성능 L4 자율주행차 수준, 기존 차량의 약 10배

이 시장은 수억에서 십억 대 단위로 분산돼 있고, 하드웨어 세대가 올라갈 때마다 디바이스당 메모리가 계속 늘어납니다. 단순 반복이 아니라 복리로 쌓이는 구조죠. 데이터센터가 소수 구매자의 한 번짜리 capex 파도라면, 이쪽은 분산되고 교체 때마다 바닥이 높아집니다.

직접 수혜는 메모리 빅3(삼성전자·SK하이닉스·마이크론). 그 아래로 일본 로봇/모션/센서 레이어까지 연결됩니다.

지금 중요한 건 숫자 맞추기가 아니라, 이 두 번째 곡선이 데이터센터와 완전히 다른 모양이라는 걸 이해하는 겁니다. 단, 전망 편차가 크고 일부는 이미 가격에 반영돼 있습니다.

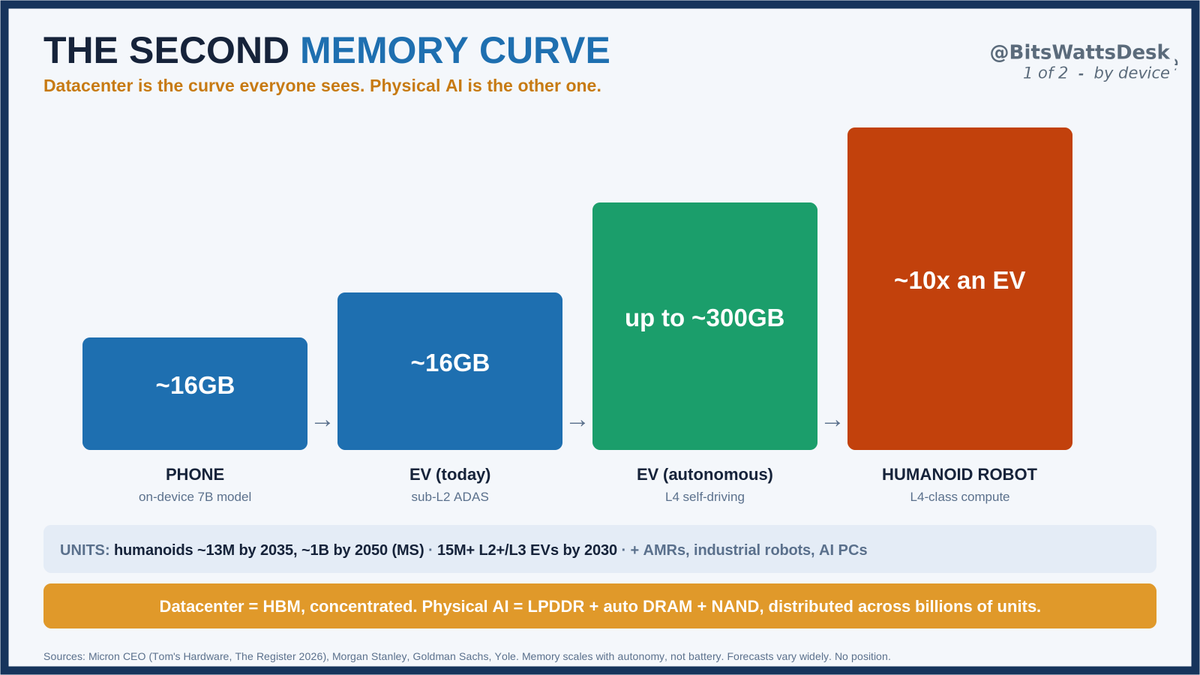

Everyone's memory thesis stops at the AIDC. The second curve, the one Micron just flagged, is Physical AI, and it is more distributed and longer-dated.

Micron's CEO calls robotics a 20-year growth vector and expects it to become one of the largest categories in tech. Here is the ladder underneath that.

Memory per device, today to the end of the decade:

- Smartphone: ~16GB is becoming standard, enough to run a 7B-parameter model on-device.

- EV: ~16GB today at sub-L2, and the memory scales with autonomy, not the battery. L3 needs 8 to 16GB, L4 needs 32GB and up, and a fully autonomous car can reach ~300GB of RAM.

Total memory content per vehicle goes from ~90GB in 2025 to ~278GB on average in 2026, and multi-TB on high-end by 2030.

- Humanoid robot: Micron says its compute rivals a high-end L4 car, roughly 10x the memory of an L2+ vehicle.

Now the units. Morgan Stanley sees ~13M humanoids in service by 2035 and ~1B by 2050, a $5T market.

Goldman sees $38B and ~1.4M units by 2035. The bull case is steeper: Tesla targets ~1M Optimus a year around 2030, and Musk's own aspiration runs to ~100M humanoids a year if volumes compound about 5x annually. On the road, 15M+ vehicles at L2+/L3 by 2030. Add AMRs, industrial robots and AI PCs on top.

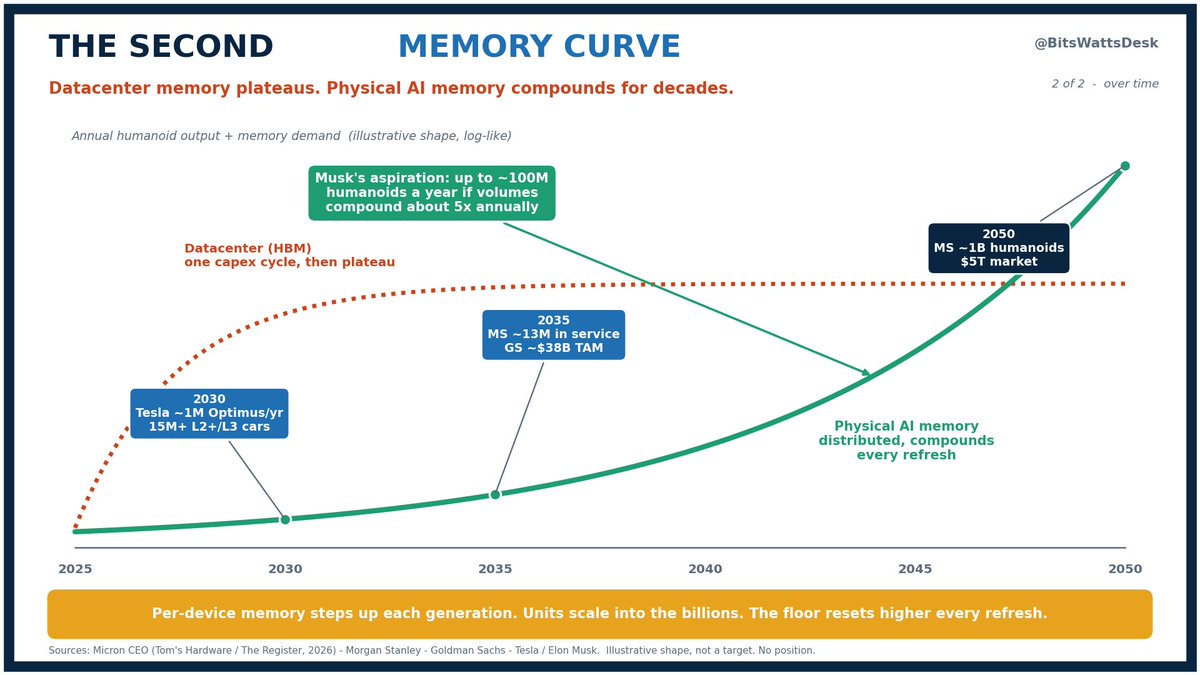

Why this is a different curve from the AIDC: the datacenter is one concentrated capex cycle, HBM bought in waves by a handful of buyers. This one is distributed across billions of units, built on LPDDR and automotive-grade DRAM and NAND, not only HBM. And the content per device steps up with every hardware generation, so it does not just repeat, it compounds, each refresh resetting the floor higher.

One curve is a wave. The other slopes up for decades.

Where it flows: the memory Big 3 capture it directly, SK Hynix (000660.KS), Samsung (005930.KS), Micron ($MU).

But underneath, the same Japan materials and equipment floor makes all of it, and Japan owns much of the robot body and motion layer, FANUC (6954.T), Yaskawa (6506.T), Harmonic Drive (6324.T), plus auto sensors at Sony (6758.T).

The discipline: humanoid forecasts for 2035 run from under $10B to over $250B, so timing and scale are genuinely uncertain, and a lot of the memory cycle is already in prices. The constraint now is valuation, not awareness. The point is the shape of the second curve, not a target.

Tickers, by market. KR: 000660.KS, 005930.KS. US: $MU. JP: 6954.T, 6506.T, 6324.T, 6758.T.

My read, not advice.

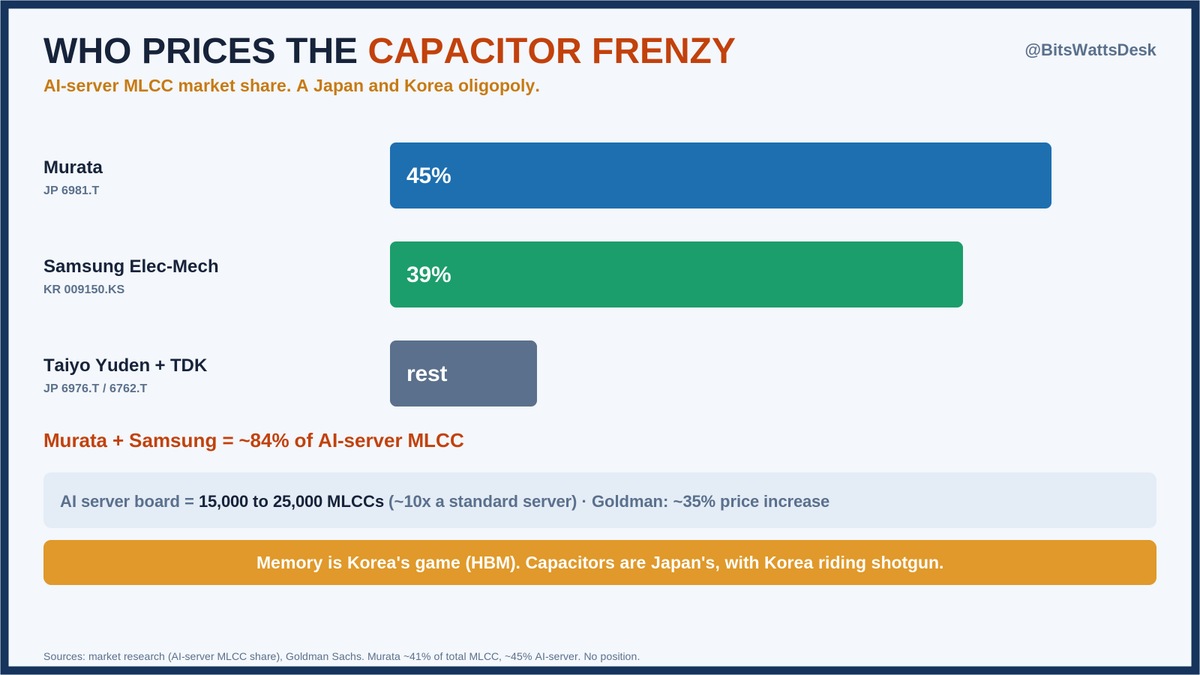

If capacitors are the next bottleneck, the name to know is Murata (6981.T), Japan's quiet #1 in passive components.

Murata holds about 41% of the world MLCC market, and around 45% of the AI-server MLCC segment specifically. An AI server board carries 15,000 to 25,000 of these, roughly 10x a standard server. That is the demand Goldman is flagging, and their actual number is about a 35% price increase, a memory-style move.

The rest of the stack is Japan and Korea. Taiyo Yuden (6976.T) and TDK (6762.T) in Japan, Samsung Electro-Mechanics (009150.KS) in Korea. With Murata, those four are about 84% of the AI-server MLCC market.

So the capacitor frenzy is really a Japan and Korea oligopoly repricing. Memory is Korea's game with HBM. Capacitors are Japan's, with Korea riding shotgun.

Tickers, by market. JP: 6981.T, 6976.T, 6762.T · KR: 009150.KS.

If MLCCs reprice, the real question is who holds the pricing power. It is an 84% JP/KR duopoly: Murata (6981.T) at ~45% of the AI-server MLCC market and Samsung Electro-Mechanics (009150.KS) at ~39%, with Taiyo Yuden (6976.T) and TDK (6762.T) behind.

The demand side is real. An AI server board uses roughly 15,000 to 25,000 MLCCs, about 10x a standard server.

On the number, Goldman's actual figure is around a 35% price increase, a memory-style surge, so 5-10x is the hot version. But tight supply plus 10x content plus an 84% duopoly is where the durable pricing power sits~

$GLW is the US side of this. Japan's mirror is AGC, the former Asahi Glass (5201.T), the other century-old glass giant in the AI buildout.

Corning connects the chips, fiber and now CPO. AGC helps print them: it makes over half the world's EUV mask blanks, around 59%, and with Hoya (7741.T) that is roughly 93% of the market.

Every leading-edge chip is patterned through a mask on their glass.

Two old glass houses, two different chokepoints.

현재 기준 가장 아름다운 ETF를 고른다면,

DRAM Memory ETF~

구성종목은 메모리 3대장이 71.96% 점유

- 마이크론 $MU: 28.05%

- SK 하이닉스: 27.64%

- 삼성전자: 16.27%

라운드힐 인베스트먼츠 (Roundhill Investments)가 발행한

$DRAM

JX Advanced Metals(JX金属, 5016.T)

6월 24일, 프로브카드용 로듐 도금액 생산능력을 FY2028까지 2배 이상 확대한다고 발표했습니다.

AI 검사 수요증가 때문임(공식 릴리스, https://t.co/uNmJ8u26lP).

작은 로듐 도금 라인 하나가 AI 검사 공급망의 구조를 보여줬습니다.

프로브카드 한 장에 수천 개의 프로브핀이 들어가고, 그 핀 끝을 로듐으로 도금해야 웨이퍼를 수없이 찍어도 버팁니다. AI로 검사 물량이 늘수록 이 소모품 수요도 같이 커지는 구조예요.

여서 더 큰 그림은?

같은 JX Advanced Metals가 지금 뜨거운 CPO광엔진 안에도 한 층 아래 들어가 있다는 점입니다.광엔진 주요 소재 공급망(레이어별):

- InP 기판: JX Advanced Metals(5016.T), 스미토모전기(5802.T)

- 커넥터·연마: Seikoh Giken(精工技研, 6834.T), 커넥터 연마 세계 시장 선도(약 60% 수준)

- 변조기·LTCC: Murata(6981.T)

- 수광소자(PD): Dexerials(4980.T)

- EML 레이저(한국): OE Solutions(138080.KQ)

테스터 시장에서는 Advantest(6857.T)가 Teradyne·FormFactor와 경쟁하고 있지만, 실제 재료 바닥은 테스터 소모품이든 검사 대상 기기든 일본이 압도적으로 강하고, 레이저만 한국이 들어와 있습니다.

광 인터커넥트는 단일 종목이 아니라 일·한·미 공급망 전체임.

이미 상당 부분은 리레이팅됐습니다.

Seikoh Giken은 연말 대비 큰 폭으로 올랐고, Advantest도 마찬가지죠.

이제 중요한 건 인지가 아니라 가격입니다. 히든 레이어는 분명히 았죠.

티커

JP: 5016.T, 5802.T/ 6834T/ 6981.T / 4980.T /6857.T

KR: 138080.KQ

US: $TER · $FORM

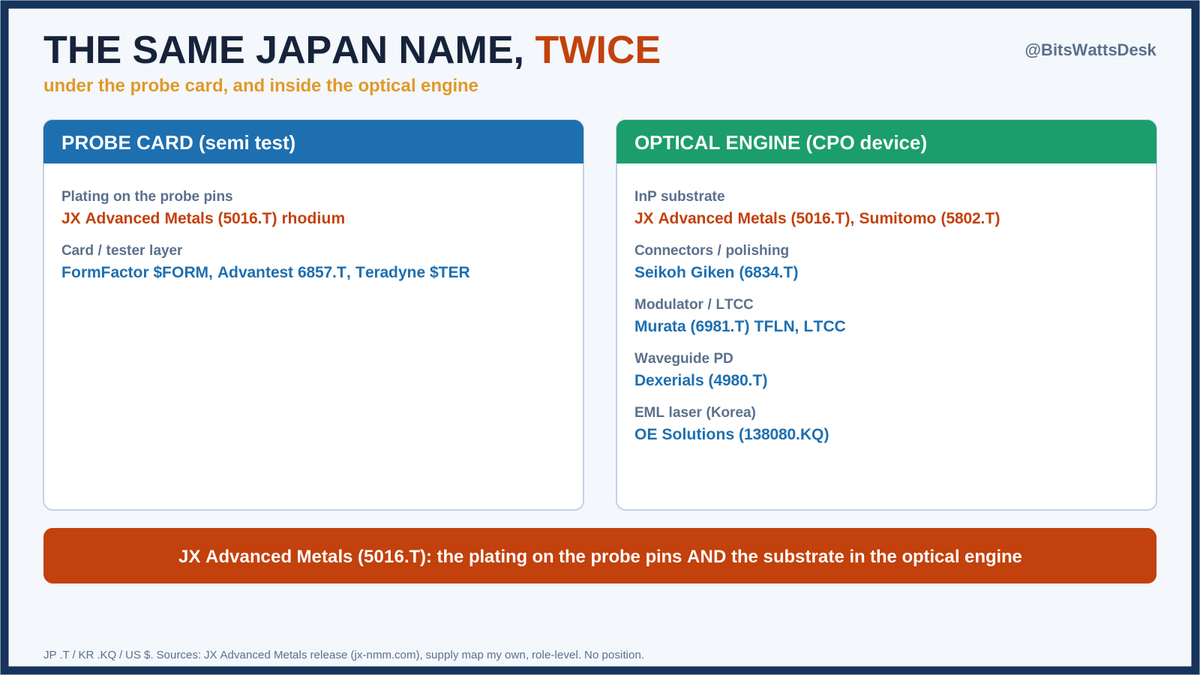

A tiny rhodium plating line just told you how the AI test buildout is wired.

JX Advanced Metals (JX金属, 5016.T) said this week it will more than double capacity for the rhodium plating solution used on probe cards by FY2028, on AI-driven test demand (its own release, https://t.co/puRjCYLCsm).

A probe card carries thousands of probe pins, and that plating is what lets them touch a wafer over and over. As AI pushes more silicon through test, that consumable scales with it.

Here is the part that fits a bigger pattern. The same name shows up one layer down in the optical engine, the device the whole co-packaged optics race is being built to test.

The optical engine BOM, by layer:

InP substrate: JX Advanced Metals (5016.T), Sumitomo Electric (5802.T)

Connectors and polishing: Seikoh Giken (6834.T), around 60% of connector polishing

Modulator and LTCC: Murata (6981.T), TFLN and LTCC

Waveguide PD: Dexerials (4980.T)

EML laser, Korea: OE Solutions (138080.KQ)

So the visible fight is in the testers, Advantest (6857.T, JP) against Teradyne and FormFactor (US).

But the material floor, under both the tester's consumables and the device being tested, skews Japanese, with Korea on the laser side.

Optical interconnect is a JP/KR/US supply chain before it is any single ticker.

The discipline: much of this has already re-rated. Seikoh Giken is up roughly 2.7x off the end-2025 base, Advantest re-rated hard. The slept-on part is no longer awareness, it is valuation. The hidden layer is real, you still pick your price.

Tickers — JP: 5016.T, 5802.T, 6834.T, 6981.T, 4980.T, 6857.T · KR: 138080.KQ · US: $TER, $FORM.

My read, not advice.

Nikkei ran a full feature this morning, framing Ajinomoto as a semiconductor stock.

The part I'd add is pricing power ~

ABF is under 0.1% of the selling price of an NVIDIA chip, yet without it that chip does not get built. An activist, Palliser, is pushing for 30%+ price hikes, and Omdia agrees there is room. The monopoly has barely started pricing like one.

Ajinomoto itself prefers raising price through higher-value products over blanket hikes, so this plays out slowly. But the asymmetry is the point: 0.1% of the bill, 100% of the dependency......

(via Nikkei, 6/25)

Going to work through Japan's quiet world #1s in the AI supply chain, materials then components then equipment, one at a time. Starting with materials.

The company that makes the insulation film inside almost every AI GPU and CPU package is a seasoning company.

Ajinomoto (味の素, 2802.T). Yes, the MSG company. Its Ajinomoto Build-up Film (ABF) holds >95% of the world market for the film that insulates the layers of FC-BGA packaging substrates, the board that carries the chip. Sekisui (Japan) has the low-end few percent. For ~30 years ABF has been the de facto standard.

It came out of amino-acid chemistry. The MSG business and the film inside your GPU share a lab heritage.

Who's trying to break it is the interesting part, and it's mostly Korean: Dongjin Semichem (reportedly at parity with ABF on the key metrics, CTE and Df), H&S High Tech (2028 mass-production target), and LG Chem (in customer qualification), plus US startup Thintronics, all pushed by Samsung's drive to dual-source. But all of them are still in qualification, and matching the chemistry is not the same as winning a socket that can't fail inside a $30,000 GPU.

Ajinomoto's real moat is 30 years of proven reliability, not just the formula. A late-decade story, if it happens.

Why it matters now: AI packaging is the demand driver. Ajinomoto's functional-materials business (ABF) did ¥100.7B revenue in FY25 at a ~54% business-profit margin, up from ~30% a decade ago, and it keeps growing as AI boards move to 11-13 layers (more ABF per board). They are building a third plant, operating from FY2032, on that bet.

The cross-border thread: ABF goes into the substrate makers (Ibiden, Shinko, Unimicron, Samsung Electro-Mechanics) who build FC-BGA for NVIDIA, AMD, Intel. Ajinomoto sits one layer below the substrate, which itself sits one layer below the chip. A chokepoint under a chokepoint.

The honest part: ABF is only ~6-7% of Ajinomoto's revenue, but it is ~30% of group profit. A food giant with a hidden, ~54%-margin monopoly inside, not a pure ABF play, and the stock is not cheap, around 40x trailing and low-30s forward, expensive if you only price it as a food name. This is about understanding the chokepoint, not a stock call.

Tickers, by market. JP: Ajinomoto 2802.T. KR challengers: Dongjin 005290.KQ, H&S 044990.KQ, LG Chem 051910.KS.

My read, not advice.

닛케이가 오늘 아침 이걸 특집으로 다뤘네요~. 아지노모토를 "반도체 종목"으로 !

제가 덧붙일 건 가격결정력입니다.

ABF는 NVIDIA 칩 판매가의 0.1%도 안 되는데, 그게 없으면 그 칩이 안 만들어집니다. 행동주의 펀드 파리사(Palliser)는 30%+ 인상을 요구 중이고, 옴디아도 인상 여력이 있다고 보고 있습니다. 이 독점은 아직 독점처럼 가격을 매기지도 않았습니다.

단, 아지노모토는 일괄 인상보다 고부가 제품으로 단가를 올리는 쪽이라 천천히 갑니다.

그래도 핵심은 비대칭입니다. 이것이 핵심 포인트죠~

청구서의 0.1%, 의존도의 100%.

투자권유 아님.

(닛케이 보도 6/25)

AI 공급망에서 일본이 조용히 세계 1위를 장악한 소부장(소재·부품·장비) 길목을 하나씩 뜯어보려 합니다. 오늘은 소재~

거의 모든 AI GPU·CPU 패키지 안에 들어가는 절연 필름을 만드는 회사는, 아이러니하게도 조미료 회사입니다.

味の素(아지노모토, 2802.T). MSG 그 회사 맞습니다.

이 회사의 ABF(아지노모토 빌드업 필름)는 FC-BGA 패키지 기판의 층간 절연 필름을 세계에서 95% 이상 독점합니다. 나머지는 일본 세키스이가 저가 제품으로 소량 차지할 뿐이죠.

이 필름은 아미노산 화학에서 나왔습니다. MSG를 만드는 기술과, 지금 여러분이 쓰는 GPU 안에 들어가는 그 필름이 같은 연구실 뿌리를 공유해요. 약 30년 동안 사실상 표준(de facto standard) 자리를 지켜온 이유입니다.

그런데 이 독점을 깨려고 가장 적극적으로 움직이는 곳은 한국 기업들입니다 !

동진쎄미켐, 에이치엔에스하이텍(2028년 양산 목표), LG화학 등이죠. 동력은 삼성의 공급망 이원화 압력입니다. 하지만 아직 모두 인증 단계에 머물러 있어요.

화학 성능을 맞추는 것과, 수만 달러짜리 GPU 소켓에서 절대 실패하면 안 되는 자리를 실제로 차지하는 것은 완전히 다른 문제이기 때문입니다. 아지노모토의 진짜 해자는 레시피가 아니라 30년 동안 쌓인 검증된 신뢰성! 즉, 경쟁사가 생기더라도 2028년 이후가 될 가능성이 높습니다.

왜 지금일까요. AI 패키징 수요가 본격적으로 폭발하고 있기 때문입니다. AI 보드가 11~13층의 적층으로 두꺼워지면서 보드당 ABF 사용량이 계속 늘고 있어요.

아지노모토 기능성소재(ABF) 사업은 FY25 기준 매출 약 1,007억 엔, 사업이익률 약 54%까지 올라왔습니다(10년 전 약 30% 수준). 이 수요에 대응하려고 기후(Gifu) 3공장도 FY2032 가동을 목표로 건설하고 있습니다.

ABF는 기판 제조사(이비덴·신코·유니마이크론·삼성전기)로 공급되고, 이들이 다시 NVIDIA·AMD·인텔용 FC-BGA 기판을 만듭니다. 아지노모토는 기판의 한 층 아래, 기판은 칩의 한 층 아래. 길목 아래의 길목에 있습니다.

넹정하게 말하면, ABF는 아지노모토 전체 매출의 6~7%에 불과합니다. 하지만 전사 이익의 약 30%를 책임지는 사업이에요. 숨은 고마진(54%) 독점을 품은 식품 대기업이지 순수 ABF 플레이어가 아니라는 점을 기억해야 합니다. 주가는 PER 약 40배(포워드 30배 초반)로, 식품주 카테고리에서만 보면 상당히 비싼 수준입니다.

이 글은 AI 공급망 속 일본의 조용한 강점을 이해하기 위한 것입니다.

티커는 아지노모토(2802.T) / 동진쎄미켐(005290.KQ), 에이치엔에스하이텍(044990.KQ), LG화학(051910.KS).

제 관점이고, 투자 권유가 아닙니다.

@StockSavvyShay Yes~ The 10x is the tell. Datacenter HBM is the memory curve everyone sees.

Physical AI is the second one: more distributed, longer-dated, far more units. A humanoid near L4-class memory, EVs going from 16GB to multi-TB, every edge device running its own model.

@StockSavvyShay Not Japan entering the same race, but funding the parts it can win: physical AI, vertical AI, and the materials layer the US and China builds already run on ~

Less joining the trillion dollar race, more doubling down on what already routes through Japan.

DRAM is fungible at the chip level. The layer that makes it is not, and that is the part that holds.

CXMT taking commodity DRAM volume in Asia is plausible. But the part AI prices is HBM, and HBM is not commodity DRAM, it is TSV, stacking and bonding, so it leans far harder on the equipment and materials floor. Much of that litho, deposition, etch, photoresist and wafer base is Japanese or Western, and a lot of it is export-controlled.

Subsidies can buy commodity share, but the ladder up to leading edge, the litho and the key materials, sits past the control line and is hard to simply buy. So the call is right on the commodity tier and overstated on HBM, whose moat sits under the chip in the packaging and material floor.

The logo on the module can change, that layer changes slowly~