I believe $BRUN is a screaming buy on a ridiculous sell-off AH. I believe it is the second best Neocloud investment behind $NBIS. I have added to my position.

Why the sell off?

A post was made on X by @saso_capital reporting ~54 million insider shares will become eligible to sell next Monday. Including 29.5 million Class B shares held by CEO Andrew Karos.

A few different financial influencers found out about this information and sold after-hours, notifying their followers. This created enormous selling pressure during an illiquid after-hours on a stock with an already extremely low float.

I don’t judge anyone’s decision to buy or hold a company. There is a potential risk of selling pressure lowering the stock price short term.

At the same time however, this is a unicorn neocloud stock with jaw-dropping growth metrics:

$BRUN ARR tripled from $30M to $96M in 4 months. Contracted backlog went from $120M to $1.45 billion as of June 1st. 1,233% year over year ARR growth. Free cash flow positive. $NVDA Preferred Cloud Partner. One of only 8 companies globally with Exemplar Cloud status. FY2026 ARR guidance of $400M+.

Karos owns 48% of this company. He built it. The pipeline keeps converting. The numbers keep accelerating. That is not someone who listed to dump.

The growth is real. The overhang is real. Both things are true. Likewise with my $IREN thesis, compute demand is insatiable, and a company as well-ran as Boost Run will likely explode in growth, and stock price.

Not financial advice. Do your own research.

I woke up to a lot of messages regarding this. And most of what is written here is plain wrong. Here are the facts:

The Lock-up period is correct. BUT the total shares that will be released to the float is NOT 54M. The tradeable float is also not 7M like implied in the earlier post. A lot of what is written here looks like something that A.I vomited out.

Let's get the easy part out of the way, the tradeable float is 12.65M and it's derived from the $WLAC public float. Easy.

Now the lock-up shares:

From the S4:

"

for any 20 trading days within any 30-trading day period commencing after the Business Combination or (iii) subsequent to a Business Combination, the date on which the Pubco consummates a subsequent liquidation, merger, share exchange or other similar transaction which results in all of the Company’s shareholders having the right to exchange their shares for cash, securities or other property (each of (i), (ii) and (iii), as the case may be, the “Lock-up Period”); provided, however, that the Lock-Up Period shall not apply to 10% of the shares of Pubco Common Stock issued upon conversion of the Founder Shares pursuant to the Business Combination.

"

> This means not ALL get released as soon as we clear the conditions above

Here's what actually happens:

The Sponsor holds 4,628,674 founder shares. These are locked up for 6 months after closing. BUT 10% of these shares (~462,867) get released early if BRUN closes ≥ $12.00 for any 20 trading days within a 30-day period commencing AFTER closing.

The Boost Run sellers' 44.15M shares have the same structure: 6 months locked, with 10% (~4.42M shares) released early on the same $12 condition.

So that means from the Sponsor and Sellers, only 4.9M shares get released.

For earn out shares:

Up to 7,875,000 shares across three tiers for Andrew (CEO)

The Sponsor + SPV (a separate vehicle that bought some of the Sponsor's stake) get a separate earnout block of 3,093,750 shares on the same tiered structure.

Total contingent share issuance: 10,968,750 new shares.

The implication for float and outstanding:

The shares outstanding (excluding warrants) simply go from ~61M to ~72M from the earnouts whereas the float goes from 12.65M to 29M. Not 54M getting released like Saso has stated here.

Also bold of you to assume that they will sell all of their shares like some kind of armageddon event. This is not a shitco like $XNDU.

Details here: https://t.co/FFJqfCQoR3

Final thoughts:

The float mechanics are arguably complicated, and it takes awhile to understand, this is why I wrote up the post linked directly above when it first de-SPACed. But it's extremely unfortunate that details can be dumbed down and taken out of context like what Saso has written. I hope this helps.

-Leki

It's September 2026, stocks I bought under $20 and they exploded 1000%

1. $KEEL – Former Bitfarms. 2.2 GW pipeline. Hyperscaler leases incoming. Cheapest GW-scale AI land play (Leopold call)

2. $SATL – Satellite imagery feeds AI training + defense targeting. Fresh DoD contract proves the demand is real. $SPCX SPACEX play

3. $LAES – Every AI agent needs quantum-proof identity. SEALSQ embeds PQC in silicon. The security layer AI can't run without.

4. $POET – Optical Interposer replaces copper in AI clusters. Light moves data faster at half the energy. 800G design wins at record pace.

5. $ONDS – Wireless OS for AI-driven industrial drones. Defense + logistics demand exploding. First-mover advantage. (Trump call)

6. $CIFR – Massive power assets pivoting to HPC. Market repricing it as AI infrastructure owner, not just a crypto miner. Same as $IREN $CRWV $NBIS

7. $BTDR – AI cloud ARR up 60% MoM. 92% GPU utilization. 3 GW global capacity. Own-chip design cuts cost to near zero.

8. $CLSK – Situational Awareness fund loaded 12M+ shares. Massive power footprint waiting to flip into AI colocation. (Leopold bought)

9. $HIVE.TO – Canada's largest AI gigafactory incoming. 100K GPU build-out on 100% renewable power. $225M ARR target.

10. $NOK – Restructuring entirely around AI data center networking. $4B US bet. Optical division feeding hyperscalers directly.

♻️ RESHARE this post and write 1 comment, I'll DM you my favorite 1000% play for this week.

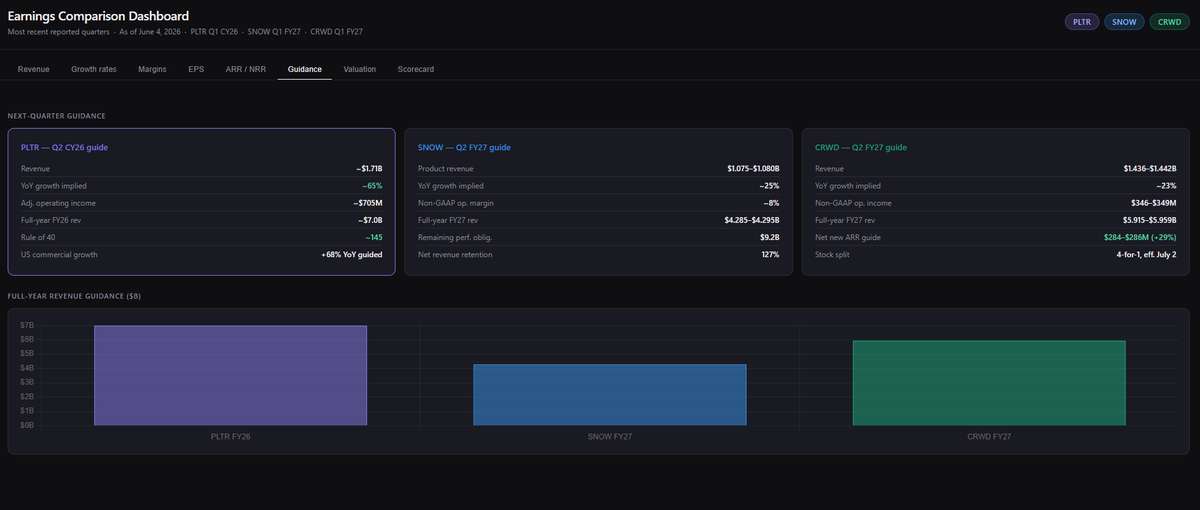

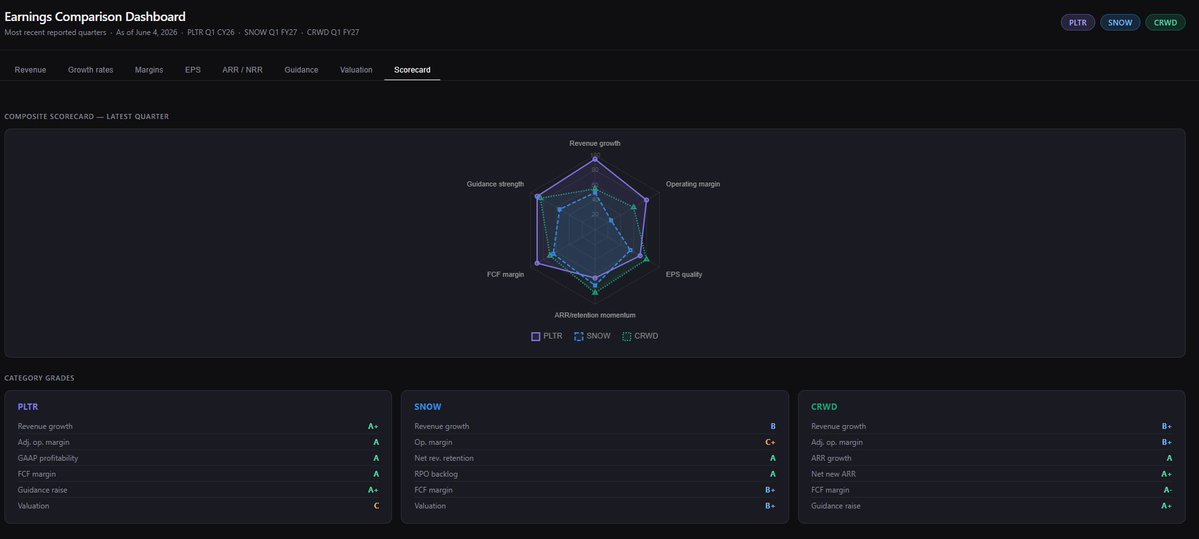

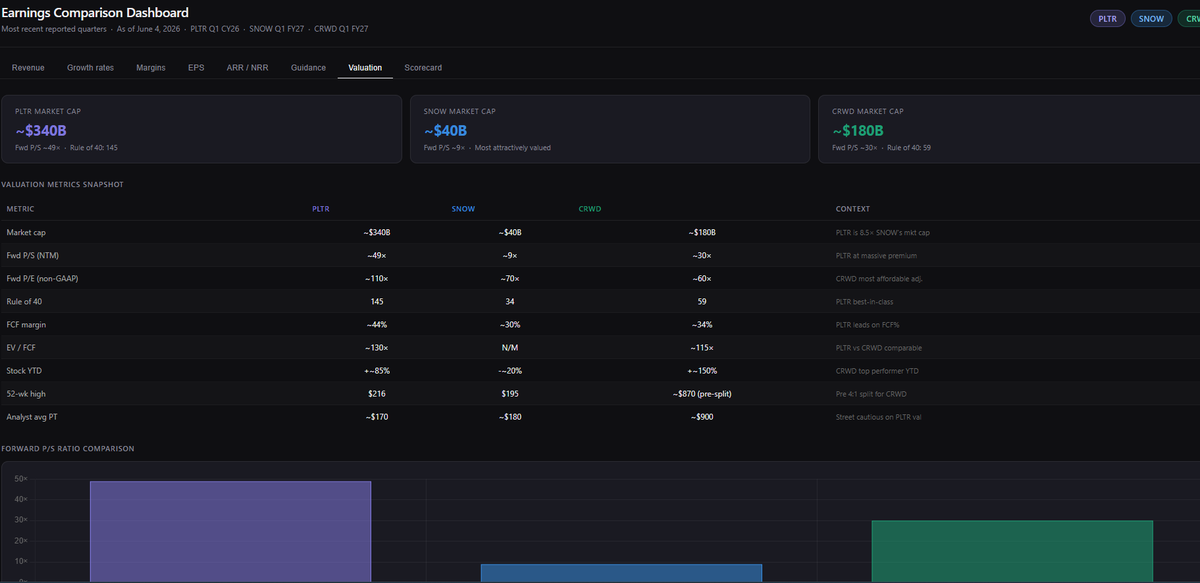

$PLTR

The biggest concern around Palantir over the past 2 years has been its valuation.

That concern should not be that relevant anymore.

If we are looking at other companies in Software, $SNOW and $CRWD are trading at HIGHER multiples on a NTM EV/EBITDA yet they are growing 2x LESS than Palantir and at 2x WORSE margins, as shown in the chart below by Arny.

You want to know what’s even worse?

The TTM GAAP profits for all 3:

Palantir did $2.28B in GAAP net income, actual profit coming down to the bottom line.

Snowflake LOST $1.33B and Crowdstrike LOST $162M!

$SNOW and $CRWD can’t produce a GAAP profit, have significantly worse margins and have significantly less growth but are getting a HIGHER multiple.

This is not to say that Snowflake or Crowdstrike are overvalued or don’t deserve the premium they are getting, but it is to say there is a massive valuation disconnect and anyone screaming that Palantir is expensive cannot make that argument relative to every other company in SaaS.

Better margins, faster growth, profitable…and basically guided to 100% topline growth next year.

This is obvious.

If the market is willing to continue giving these premiums to software companies as the “AI destroying software” narrative goes away, Palantir should continue to gain momentum.

2 years ago, I called out $ASTS at $2. Its up 6500% so far at $130.

My target at least $200+ when $SPCX IPOs.

Right now, $ORCL is the most obvious play. Its earnings is on June 10 then $MU on June 24.

This year, I explained these would 10x-20x:

$INTC — $AAPL chip deal + foundry turnaround tripled the stock in months (Trump)

$DELL — Pentagon contract + AI server orders created a multi-catalyst monster (Trump)

$MU — HBM memory sold out through 2026, AI supercycle just getting started (Trump)

$NOW — Enterprise AI agents replacing entire IT workflows, 22% revenue growth accelerating (Trump)

$PLTR — Government + commercial AI contracts exploding, revenue up 56% in 2025 (Trump call)

$TE — nuclear power is the only answer to AI's insatiable electricity demand (Leopold call)

♻️ RESHARE this post and write 1 comment, I'll DM you my exact 1000% play for $ORCL