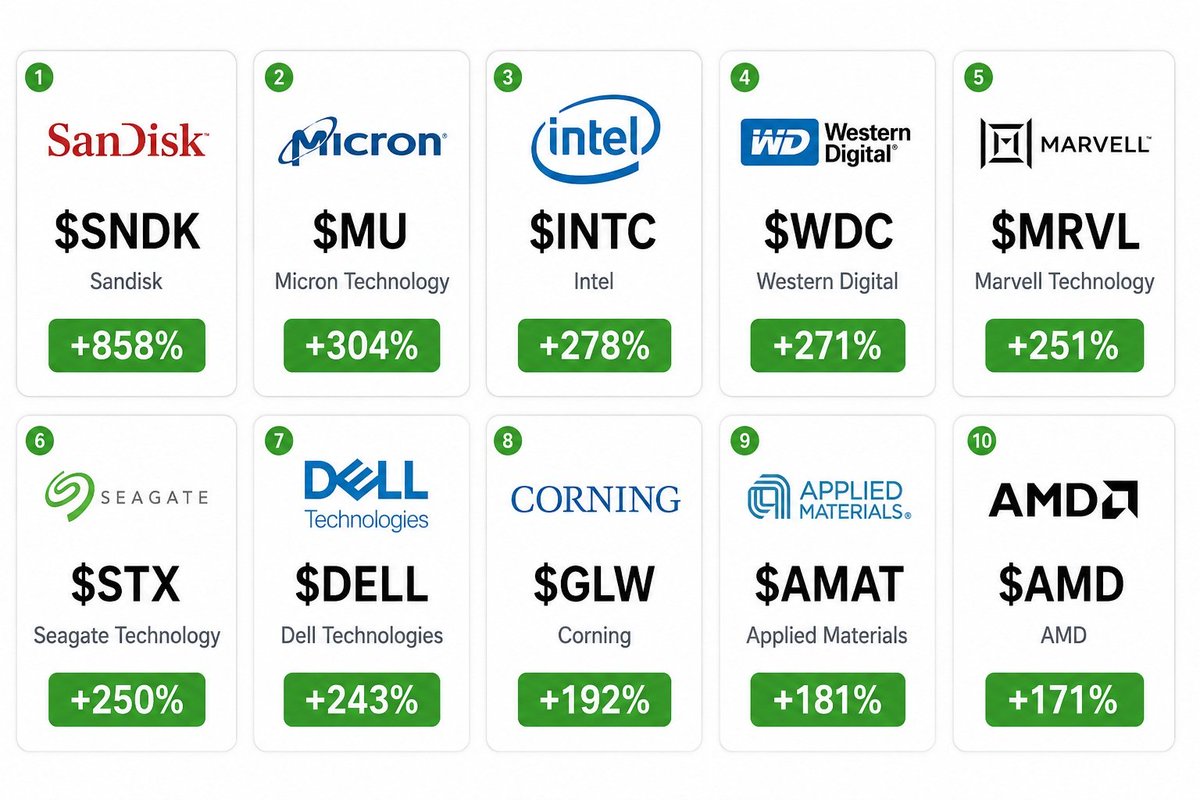

Best performing stocks in the S&P 500 halfway through 2026:

1. Sandisk $SNDK: 858%

2. Micron $MU: 304%

3. Intel $INTC: 278%

4. Western Digital $WDC: 271%

5. Marvell $MRVL: 251%

6. Seagate $STX: 250%

7. Dell $DELL: 243%

8. Corning $GLW: 192%

9. Applied Materials $AMAT: 181%

10. AMD $AMD: 171%

Are we still in the early stages of the cycle, or has the market already overheated?

Blue Origin reportedly raising $10B at a $130B valuation per NYT.

That’s a strong valuation signal for the space sector.

At the same time, Morgan Stanley reiterated $RKLB at Overweight, kept its $105 PT, and raised its bull case to $293.

If SpaceX and Blue Origin can command these kinds of valuations, public space names like $RKLB and $ASTS may still have room to rerate.

10 High-quality stocks trading near 52-week lows

1. Microsoft $MSFT: -29%

2. Netflix $NFLX: -41%

3. Mastercard $MA: -12%

4. SoFi Technologies $SOFI: -43%

5. Palantir $PLTR: -36%

6. ServiceNow $NOW: -48%

7. Oracle $ORCL: -56%

8. Meta Platforms $META: -24%

9. Adobe $ADBE: -43%

10. CoreWeave $CRWV: -46%

If you are interested in seeing my high-conviction stock picks, my full portfolio, and every trade I make, click "Follow" and leave me a message.

$LITE isn't dead.

It simply rose too fast.

The AI optics theme remains strong, but after such a significant rally, the stock needs a pullback to shake out some of the less prudent investors.

The $700–$715 level is the initial support zone.

If it holds this area, the pullback could turn into a reset.

If it drops below $700, you'll need to wait for a deeper bottom to form.

In the long run, this is a strong theme.

But patience is key.

🔥 $MU is pulling back hard.

But the AI memory story is not over.

This looks more like profit-taking after a massive rally than a broken thesis.

HBM demand is still strong.

Memory supply is still tight.

AI data centers still need more DRAM and NAND.

The key level now: $965–$980.

Hold that zone, and $MU could reset for another move.

Lose it, and the stock may need more time to cool down.

Power Semiconductors: The Next Price-Hike Cycle May Be Starting ⚡

Power semiconductors may be entering a new upcycle.

The signal is not coming from hype.

It is coming from price increases.

Recently, several power semiconductor suppliers have started or reportedly prepared new rounds of price hikes. In China, Yangjie Technology announced that it will raise prices across its product lines by 10%–15%, with the new pricing taking effect from July 1, 2026. This is reported as its second price adjustment this year.

That matters because price hikes usually do not happen when demand is weak.

They usually mean three things:

1. Demand is recovering

Power devices are used in EVs, industrial automation, AI servers, energy storage, robotics, consumer electronics, and grid infrastructure.

When downstream demand improves, distributors and OEMs begin restocking.

2. Supply is getting tighter

Power semiconductors rely heavily on mature-node capacity, 8-inch wafers, packaging, and upstream materials. These areas are not as glamorous as GPUs, but they are critical to the entire electronics supply chain.

When capacity becomes tight, pricing power returns.

3. Costs are being passed downstream

Yangjie cited upstream wafer, bulk metal, and packaging material cost pressure as reasons for the adjustment. The key point is not just rising costs — it is that suppliers are confident enough to pass those costs to customers.

This is why the price hike is important.

It may signal that the sector is moving from a weak pricing environment into a margin recovery cycle.

Watchlist:

$ON $STM $IFNNY $VSH $WOLF $POWI $DIOD $TXN

China just turned antimony into a strategic weapon.

Most investors still don’t understand how big this supply gap could become.

Global annual production is only around 110,000 tons, while the supply gap may already be 10,000–40,000 tons.

This is no longer just a metal story. It is a defense, battery, flame-retardant, and critical-mineral story.

Watch: $UAMY $PPTA $SSMR