Crypto founders will wire $500 to a KOL & call it marketing…

Here is what will usually buy with a 50k-follower account at typical engagement: ~1.5 new holders.

That's $333 each. A 0.15x ROI. 😬

Block AI built a free calculator just for this.

So you can run these numbers before you decide to pay, not find out after.

Fee, followers, engagement, conversion it spits out cost per holder & projected ROI.

No sign-up.

𝗔𝗜 𝗙𝗼𝘂𝗻𝗱 𝗮𝗻 𝗘𝘁𝗵𝗲𝗿𝗲𝘂𝗺 𝗕𝘂𝗴. 𝗛𝘂𝗺𝗮𝗻𝘀 𝗦𝘁𝗶𝗹𝗹 𝗛𝗮𝗱 𝘁𝗼 𝗣𝗿𝗼𝘃𝗲 𝗜𝘁.

The Ethereum Foundation pointed coordinated AI agents at validator client code and got a remotely triggerable crash out of it. But it also got a pile of confident, well-written reports that were completely wrong.

This is the real story nobody's discussing: AI is now good enough to find genuine zero-days in consensus-layer software, but it's also good enough to fabricate plausible-sounding vulnerabilities that waste human review time. The signal-to-noise ratio is the bottleneck, not the capability.

We run 70+ custom AI algorithms for on-chain analysis. The pattern is identical. Raw AI output without human validation is noise dressed up as insight. The teams that win are the ones building hybrid systems where AI flags and humans confirm.

The Ethereum Foundation got this right. The question is whether smaller chains and DeFi protocols with thinner engineering teams can afford the same approach. If your protocol relies on 3 devs reviewing AI-generated audit findings, are you actually more secure or just more confident?

𝗬𝗼𝘂𝗿 𝗣𝘂𝗺𝗽 𝗙𝘂𝗻 𝗟𝗮𝘂𝗻𝗰𝗵 𝗗𝗶𝗲𝗱 𝗶𝗻 𝟳 𝗠𝗶𝗻𝘂𝘁𝗲𝘀

I tracked 83 Pump Fun launches last month. The ones that graduated the bonding curve with real momentum had one thing in common: coordinated early buying from 25+ wallets, not 3 dev wallets panic-buying their own supply.

Block AI runs Pump Fun launches with 25+ pre-warmed wallets buying through the bonding curve phase, followed by manual scoops once bonding completes. The wallets have aged history and varied on-chain behaviour. It looks like genuine early demand because it behaves like genuine early demand.

The difference between a token that flatlines at 12% bonding and one that graduates and holds is almost always what happens in the first few minutes.

How many of your past launches actually made it past the bonding curve?

Available through @Block_AIBot

𝗕𝗶𝘁𝗰𝗼𝗶𝗻'𝘀 𝗠𝗼𝗼𝗻𝘀𝗵𝗼𝘁 𝗘𝗿𝗮 𝗜𝘀 𝗢𝘃𝗲𝗿. 𝗧𝗵𝗮𝘁'𝘀 𝗔𝗰𝘁𝘂𝗮𝗹𝗹𝘆 𝗕𝘂𝗹𝗹𝗶𝘀𝗵.

Every cycle since 2018, the same pattern: analysts extrapolate the previous cycle's returns onto a larger base. $300K-$500K by 2029 requires BTC to absorb trillions in new capital at a rate it's never sustained post-halving. The maths doesn't work when your market cap already rivals silver.

But here's what the "$300K is impossible" crowd misses: diminishing percentage returns don't mean diminishing opportunity. They mean the market is maturing. And mature markets need real infrastructure, not hype cycles. The money now flows to projects with actual liquidity depth, proper market making, and sustainable order books rather than leveraged moonshot narratives.

We've run market making through three full cycles. The shift from "number go up" speculation to institutional-grade liquidity is the most significant structural change since 2020. BTC doesn't need to 5x to be the best risk-adjusted asset in the room.

So which matters more for the next cycle: peak price targets, or whether the liquidity behind those prices is real?

𝗧𝗵𝗲 𝗨𝗞 𝗗𝗶𝗱𝗻'𝘁 𝗚𝗲𝘁 𝗦𝗲𝗿𝗶𝗼𝘂𝘀. 𝗜𝘁 𝗚𝗼𝘁 𝗦𝗰𝗮𝗿𝗲𝗱.

The UK isn't embracing crypto because of some grand vision. It watched Dubai, Singapore, and Abu Dhabi hoover up every serious crypto firm from 2022 to 2025, and finally recognised the tax revenue walking out the door.

Regulatory clarity is welcome, but frameworks without infrastructure are just paperwork. A token listed on a UK-regulated exchange still needs proper market making, tight spreads, and real depth on day one. We've onboarded projects across 120+ exchanges since 2018, and the pattern is always the same: regulation gets the headline, liquidity gets the listing to survive past week one.

The real question is whether UK regulators will treat market makers as partners in building orderly markets, or as adversaries to be compliance-bludgeoned into irrelevance. Singapore got this right. Has the FCA learned anything from watching?

Apple suing OpenAI for alleged iPhone trade secrets theft is the clearest signal yet that the AI arms race has moved from model benchmarks into talent and IP. A former Apple engineer named Chang Liu quit in January 2026, kept his Apple-issued laptop instead of returning it, then reportedly used a bug to log back into Apple's private systems. The accusation: a coordinated campaign to steal information about upcoming products, timed to accelerate OpenAI's push into consumer hardware.

The structural read here is not unique to big tech. We see the exact same failure mode in crypto infrastructure. When organisations scale aggressively into new verticals by copying rather than building, the controls rarely keep pace with the ambition. The cracks appear at scale, not at launch, and by then the damage is already done.

If your project is integrating third-party AI tooling or onboarding engineers from competing teams, what does your IP and access audit actually look like before they touch production systems?

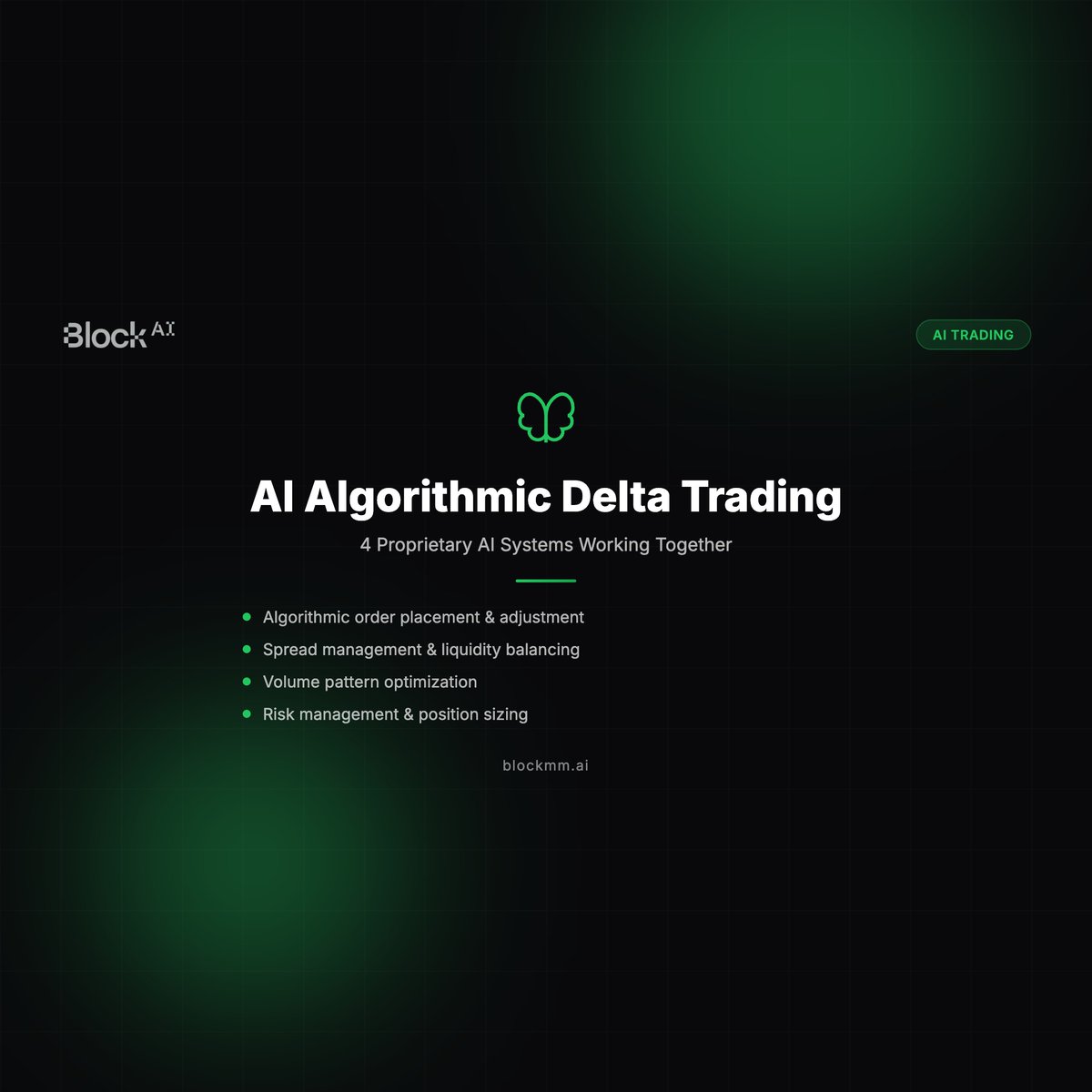

𝗬𝗼𝘂𝗿 𝗧𝗿𝗲𝗮𝘀𝘂𝗿𝘆 𝗜𝘀 𝗦𝗶𝘁𝘁𝗶𝗻𝗴 𝗜𝗱𝗹𝗲

Most project treasuries lose value between milestones. Slowly, quietly, predictably.

Block AI's Delta Trading system puts idle treasury to work through 4 proprietary AI layers: order placement, spread management, volume optimisation, and risk management. All running 24/7 across 120+ exchanges.

The model is simple: no profit, no fee. If the algorithms don't generate returns, you pay nothing.

This isn't a replacement for your market making. It sits alongside it as a separate revenue layer, building treasury value from activity that's already happening in your order books.

▪️ 70+ custom AI algorithms

▪️ 15+ experienced traders managing oversight

▪️ 300+ projects served since 2018

▪️ Zero upfront cost

Available through @Block_AIBot on Telegram.

Honest question for founders: if your treasury isn't actively generating yield between raises, what's the actual justification for holding it on-chain vs converting to stables?

$147M bled out of bitcoin and ether ETFs Thursday, while both assets rallied. Flows and price just diverged. When institutional pipes drain but spot keeps lifting, the bid is coming from somewhere else. Is it sticky capital or leveraged longs front-running a MACD flip?

𝗕𝗶𝘁𝗰𝗼𝗶𝗻 𝗧𝗿𝗲𝗮𝘀𝘂𝗿𝘆 𝗙𝗶𝗿𝗺𝘀 𝗔𝗿𝗲𝗻'𝘁 𝗪𝗵𝗮𝘁 𝗬𝗼𝘂 𝗧𝗵𝗶𝗻𝗸

Empery Digital sold 1,400 BTC since May to fund an AI data centre deal, legal bills, and general expenses. That's nearly half their holdings, $87M out the door.

This is the quiet problem with the "Bitcoin treasury" model every Nasdaq shell is copying from MicroStrategy. When you hold BTC as a corporate asset but your actual business burns cash, every quarter becomes a potential liquidation event. The market reads "Bitcoin company" and prices in upside exposure. What it actually gets is a leveraged position with operational bleed underneath.

The tell is always the same: you don't sell half your treasury in a bull market unless something off-balance-sheet is forcing your hand. Legal costs and "other expenses" is the kind of line item that hides a lot.

We've watched this pattern since 2020. The firms that survive cycles aren't the ones with the biggest BTC stack. They're the ones with revenue that doesn't depend on selling their own holdings to keep the lights on.

How many of the current crop of Bitcoin treasury firms will still hold their full position by Q1 2026?

307 days inside a $10K band, Bitcoin's third longest consolidation in history. Most see boredom. Market makers see a coiling spring. The liquidity stacked on both sides of $60K-$70K dwarfs every pre-breakout setup since 2020. When it snaps, the first 4 hours will matter more than the last 10 months. Is your infrastructure built for the release or just the range?

Circle didn't just get a bank charter, it rewrote stablecoin counterparty risk. USDC reserves under federal supervision changes settlement math for every desk routing through it. When the issuer becomes a bank, does it start competing with the market makers it serves?

𝗠𝗲𝘁𝗮 𝗝𝘂𝘀𝘁 𝗦𝗮𝗶𝗱 𝘁𝗵𝗲 𝗤𝘂𝗶𝗲𝘁 𝗣𝗮𝗿𝘁 𝗢𝘂𝘁

Meta's Chief Data Officer says stablecoins are "assumed" inside Meta now. Not piloted. Not explored. Assumed.

That's a company with 3.3 billion monthly users treating stable digital dollars as default infrastructure. The bottleneck isn't adoption at Meta's scale. It's that most of crypto still can't handle the settlement, bridging, and liquidity demands that come when a platform that size actually plugs in.

We've been building cross-chain bridge infrastructure across 12 chains for exactly this reason. When TradFi and Big Tech treat stablecoins as plumbing, the projects that survive are the ones with real liquidity depth and proper market making on both sides of the bridge.

Here's the question worth asking: if Meta routes even 1% of commerce through stablecoins, which L1 or L2 actually has the order book depth to absorb that volume without spreads blowing out?

Crypto founders will wire $500 to a KOL & call it marketing…

Here is what will usually buy with a 50k-follower account at typical engagement: ~1.5 new holders.

That's $333 each. A 0.15x ROI. 😬

Block AI built a free calculator just for this.

So you can run these numbers before you decide to pay, not find out after.

Fee, followers, engagement, conversion it spits out cost per holder & projected ROI.

No sign-up.

Bitcoin up 4.2% through an oil shock, a bond selloff, and U.S. strikes on Iran, in seven days. Correlation models said dump. Markets said no.

The real tell wasn't price. It was which desks held tight spreads through 72 hours of Strait of Hormuz chaos versus who widened 3x and called it "risk management." Crypto's settlement layer didn't pause for geopolitics, but plenty of liquidity providers did.

Did your market maker hold spread through the vol, or just quote it in calm?

Your AI agent's next hallucination won't be a wrong answer, it'll be a backdoor. Researchers proved agents can be tricked into installing malicious code via fabricated package names. For any firm running autonomous agents near order flow or wallet infrastructure, this is the attack surface nobody's stress-testing. What can your agents install without human sign-off?

$7.2B just moved from LayerZero to Chainlink CCIP. Kelp, Lombard, Solv, Virtuals, Mantle, gone. This is the bridge layer's "exchange consolidation" moment. Settlement reliability beats ecosystem loyalty every time. At what remaining volume does staying on LayerZero start looking like a counterparty risk signal?

Your market maker clocks out at 5pm EST. Asia opens three hours later. That gap is where liquidity quietly bleeds.

Block AI runs 24-hour market making, rotating human traders with full AI backing. $3,500/day. Built for prelaunch or $500k+ daily volume projects. ~6% token allocation.

If your order book thins out every night, is that market making or just market suggesting?

B3 listed options on BTC, ETH, and SOL futures, zero token custody required. Latin America's largest exchange didn't build a crypto desk. They routed derivatives through existing clearing rails. Which matters more for adoption: another spot ETF, or infrastructure that lets brokerages offer crypto without retooling?

$568M in week-one onchain volume from Robinhood. Most of it memecoins. Arbitrum jumps 19%. But here's the part nobody's discussing: one TradFi integration just outpaced most L2s' quarterly volume. The chain didn't matter, the liquidity infrastructure underneath did.

If Coinbase or Schwab flipped the same switch tomorrow, which L2 actually has the market making depth to handle it?

Senator Lummis calling the Clarity Act "our last chance to get real legislation for digital assets on the books before 2030" is the kind of statement that should land differently for anyone building serious infrastructure. The CFTC Chair added "we're so close" and "it's absolutely critical that we have a federal standard for crypto assets." The alignment is there. The hold-up is politics, not conviction.

What this actually means for builders: securities versus commodities classification changes everything downstream. Custody requirements, exchange listing eligibility, how you structure a token launch, how market makers manage inventory risk across venues. Projects running on ambiguity right now are making structural bets whether they acknowledge it or not.

If the Clarity Act fails, the U.S. doesn't get a pause. As Lummis put it, another country writes the rules, and America spends the next decade catching up to a framework built without its input.

Is your token architecture designed for the framework that passes, or the grey zone you're operating in today?