I do not think $HHH will be taken private. The process of taking a real estate centric asset base and rolling that into an insurance operation will take years. To the extent there remains a wide discount to intrinsic value as this process is underway, I have been an advocate of aggressive share purchases to maximize the per share benefit of the book multiple re-rating.

There is a bit more to it than just “charging fees”. For starters, $PS injected equity capital into the firm at $100 a share, which was a meaningful premium to the market pricing at the time. That enabled $HHH to buy Vantage at 1.5x book, which likely gaps to 2x+ book over time. They also arranged additional financing for the Vantage transaction from $PSH at compelling terms. Those two things alone create substantial value which make them feel more like partners vs. using $HHH as a fee machine for the GP.

There is an even wider discount to intrinsic value with $HHH. Is $HHH restricted in its ability to authorize a share purchase program because of Pershing’s ownership % restrictions? If so, can you please update us on if you intend to seek to remove this restriction and initiate a buyback program?

Possibly, but that would be quite an opportunity… The long-term IRR of share repurchases at current price levels is quite a substantial hurdle rate.

If there is a structural limitation of their ability to execute a share purchase program because of Pershing’s agreement to not increase their ownership past a certain percentage, that needs to be corrected as no holding company like this should have that tool taken away.

$ACGL buying in stock at ~150% p/b last quarter…surely $HHH could see the value of buying in stock at ~61% p/b prior to the cash transition from HHC to Vantage (which should command a ~180%+ p/b valuation) @BillAckman if there are limitations around Pershing and affiliates increasing ownership past current ownership levels which is the reason share repurchases cannot happen, could you please let us know if you are open to revisiting this dynamic with the $HHH Board?

Considering the 5-year plan and associated share price economics, would $HHH consider instituting an aggressive share repurchase program in lieu of early-retiring the $PSH preferred equity investment?

Buying $HHH common at a meaningful discount to intrinsic value is materially more accretive per share than redeeming $PSH preferred at par or at the 1.5x book / 4% compounded floor.

At current $HHH pricing, the per-share CAGR is 25%+ if you hit your 5-year target, which seems like a great use of capital as cash rolls off from the CRE business in addition to allocating capital to Vantage.

If you are prohibited from instituting a share repurchase plan because of the impact that would have on Pershing’s effective ownership %, I would suggest immediately going to the Board to change that effective ceiling restriction. This structural capital allocation restriction could actually be partly why the discount to NAV exists… you should be entitled to use any and all tools to create shareholder value for $HHH.

.@BillAckman (follow up) thanks for the presentation. Considering the 5-year plan and associated share price economics, would $HHH consider instituting an aggressive share repurchase program in lieu of early-retiring the $PSH preferred equity investment?

Buying $HHH common at a meaningful discount to intrinsic value is materially more accretive per share than redeeming $PSH preferred at par or at the 1.5x book / 4% compounded floor.

At current $HHH pricing, the per-share CAGR is 25%+ if you hit your 5-year target, which seems like a great use of capital as cash rolls off from the CRE business in addition to allocating capital to Vantage.

If you are prohibited from instituting a share repurchase plan because of the impact that would have on Pershing’s effective ownership %, I would suggest immediately going to the Board to change that effective ceiling restriction. This structural capital allocation restriction could actually be partly why the discount to NAV exists… you should be entitled to use any and all tools to create shareholder value for $HHH.

I think there is significant value in both. I am preferential to $HHH because I think their insurance operation can grow significantly faster than the underlying fee pools which $PS would be entitled to. That, and you are buying a $1 for 60 cents now with $HHH, whereas $PS to me doesn’t have that type of current margin of safety at current pricing.

@BillAckman As an $HHH shareholder, I have three questions on capital allocation that I believe compound on each other to drive the share price toward intrinsic value:

1) Is $PSUS, as a distinct vehicle, able to purchase $HHH common stock directly in the open market? Or do any such purchases count toward the existing 47% beneficial / 40% voting cap that applies to the broader Pershing fund complex?

2) Would $HHH consider instituting an aggressive share repurchase program in lieu of early-retiring the $PSH preferred equity investment? Buying common at a meaningful discount to intrinsic value is materially more accretive per share than redeeming preferred at par or at the 1.5x book / 4% compounded floor.

3) When will $HHH begin publishing formal NAV, even on a periodic basis? Without that disclosure, the market cannot reliably distinguish operating performance from valuation drift, and the discount persists by default.

These compound. The 47% cap already mechanically removes ~28M shares from tradeable float. Layer in a $PSUS buying channel (if available outside the cap), buybacks executed below NAV, and published asset values: effective free float shrinks further, pushing price toward intrinsic value rather than allowing the discount to calcify around an unmeasured number.

@BillAckman thanks for the presentation. Considering the 5-year plan and associated share price economics, would $HHH consider instituting an aggressive share repurchase program in lieu of early-retiring the $PSH preferred equity investment?

Buying common at a meaningful discount to intrinsic value is materially more accretive per share than redeeming preferred at par or at the 1.5x book / 4% compounded floor. The per-share CAGR is 25%+ if you hit your 5-year target, which seems like a great use of capital as cash rolls off from the CRE business in addition to allocating capital to Vantage.

If you are prohibited from instituting a share repurchase plan because of the impact that would have on Pershing’s effective ownership %, I would suggest immediately going to the Board to change that effective ceiling restriction.

@BillAckman As an $HHH shareholder, I have three questions on capital allocation that I believe compound on each other to drive the share price toward intrinsic value:

1) Is $PSUS, as a distinct vehicle, able to purchase $HHH common stock directly in the open market? Or do any such purchases count toward the existing 47% beneficial / 40% voting cap that applies to the broader Pershing fund complex?

2) Would $HHH consider instituting an aggressive share repurchase program in lieu of early-retiring the $PSH preferred equity investment? Buying common at a meaningful discount to intrinsic value is materially more accretive per share than redeeming preferred at par or at the 1.5x book / 4% compounded floor.

3) When will $HHH begin publishing formal NAV, even on a periodic basis? Without that disclosure, the market cannot reliably distinguish operating performance from valuation drift, and the discount persists by default.

These compound. The 47% cap already mechanically removes ~28M shares from tradeable float. Layer in a $PSUS buying channel (if available outside the cap), buybacks executed below NAV, and published asset values: effective free float shrinks further, pushing price toward intrinsic value rather than allowing the discount to calcify around an unmeasured number.

Good morning Bill and Ryan,

I attempted to ask the following about HHH, but was cut off due to technical issues with Spaces.

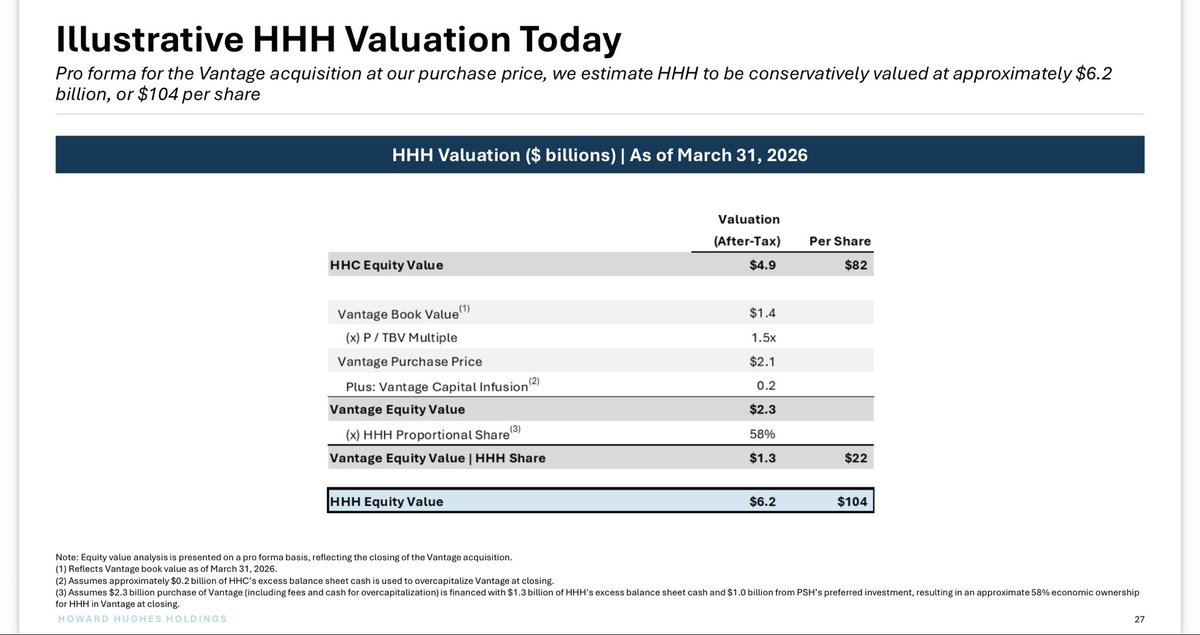

I also find HHH’s discount to intrinsic value at this moment to be quite wide; I actually think it is even wider than you indicated as the NAV of HHH seems to be well in excess of $100.

Post-closing of Vantage, would you consider allocating a portion of HHH’s free cash flow toward a HHH common stock repurchase program rather than directing incremental capital toward early retirement (prior to 7 year schedule) of the PSH preferred?

Also, is PSUS able to buy HHH stock, or were there restrictions around effective ownership totals after PS invested $900M?

@BillAckman Arch posted ~79% combined ratio ex cat and prior year activity…very impressive. Looking forward to Marc adding value as a Board member. Well done @BillAckman.