@christianvctrs Umumny urusan agen sm penjual.

Pembeli boleh aja kasi bonus(kalau bs neken harga sesuai kemauan pembeli)

Yg ttd perjanjian komisi sm kantor agen kan penjual & si agen 😂. Kecuali dr awal transaksi dicantumkan dan diinfokan komisi pembeli yang tanggung.

Valuation-wise, Indonesia is arguably one of the cheapest equity markets in Asia today. Many well-known blue-chip companies are trading at what can only be described as crisis-like multiples despite maintaining healthy balance sheets, dominant market positions, and attractive dividend yields.

BBCA trades at roughly 11x forward earnings and 2.6x book value. Bank Mandiri trades at around 6x forward earnings and 1.2x book value. BRI trades at approximately 7x forward earnings and 1.3x book value. Astra sits at 6x forward earnings. Kalbe trades at 9x forward earnings. Amman trades at roughly 10x forward earnings. The list goes on.

Many of these companies also offer high single-digit dividend yields, with some names approaching double-digit yields. On paper, this should attract significant investor interest. Yet share prices continue to drift lower.

The obvious question is: where are the buyers? Where are all the investors who have spent years believing Indonesia’s long-term potential? Indonesia’s weight in MSCI Emerging Markets remains only around 0.5-0.6%, remarkably small relative to the size of its economy, population, and long-term growth aspirations.

More importantly, where is Danantara? It was presented as a potential new source of domestic capital and a stabilizing force for Indonesian financial markets. If the local market is trading at distressed valuations, this should be the type of environment where a large domestic institutional investor helps establish confidence.

The problem, however, is that cheap valuation alone is rarely enough. Markets ultimately pay for growth.

Indonesia’s core challenge today is not valuation. It is earnings growth. Aggregate earnings growth for the market has slowed materially, with many sectors struggling to generate meaningful expansion. Compare that with South Korea and Taiwan, where investors are being offered direct exposure to AI, semiconductors, advanced manufacturing, memory, and high-performance computing. Foreign investors are naturally willing to pay higher multiples for companies whose earnings are compounding rapidly.

Currency concerns add another layer of complexity. Investors are not simply underwriting Indonesian corporate earnings. They are also underwriting the rupiah. If currency depreciation continues to offset equity returns, valuation discounts can persist far longer than expected.

There is also a credibility issue that should not be ignored. For years, many foreign investors have complained that parts of the Indonesian market function primarily as distribution channels rather than genuine capital formation venues. Domestic equity sales teams routinely promote names that later become exit liquidity for local institutions seeking to reduce exposure. Over time, repeated experiences like this erode trust.

The persistent allegations of wash trading, questions around effective free float, concentrated ownership structures, and concerns over genuine liquidity have further damaged confidence. Investors do not simply buy low valuations. They buy governance, transparency, liquidity, and confidence in future earnings.

This is why cheap markets can remain cheap for years. A stock trading at 6x earnings can still fall to 5x. Valuation itself is not a catalyst.

The harsh reality is that Indonesia does not have a valuation problem. It has a growth and confidence problem.

Until investors see stronger earnings growth, more credible policy execution, better market governance, improved liquidity, and a clearer path for capital to generate attractive real returns, low multiples alone will not be enough to attract meaningful foreign capital back into the market.

Cheap without growth is a value trap. Cheap with deteriorating confidence is even worse.

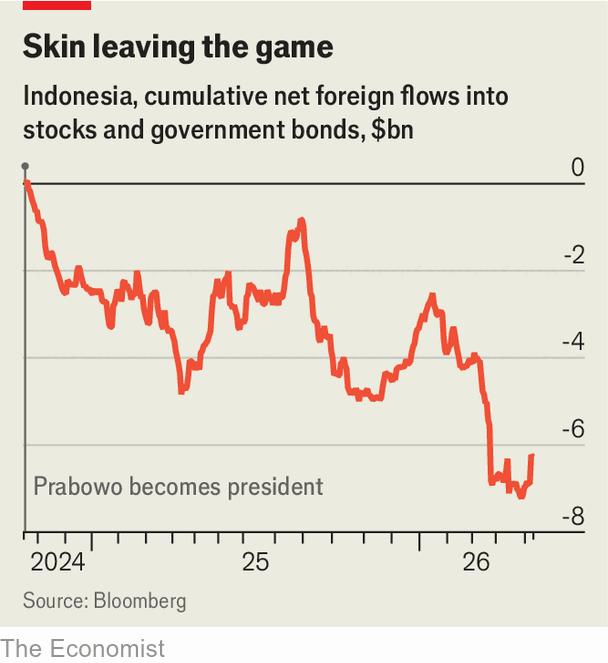

🧵 Prabowo Subianto is chipping away at the political and economic settlements that have been the foundation of Indonesia's hard-won stability since the Asian financial crisis.

In @TheEconomist's Briefing this week, @EthanYWu and I take in the first 18 months of his presidency.

For years back then, Erwan and Kartika did wash trading for CIMB, creating fake trades to lure people so that broker generated more commission. In my Christian faith, I declare whoever gives trade to BNI Sekuritas before Erwan is fired will be cursed by my God. Whatever you do may suck. Evil will own you. It is time for him to retire. Same goes to ones whom give institutional trade to Indopremier, evil will own you and be burned in hell.

To the ones not in my blast, it means you have been an ass hole buy side. This curses still apply to you as well regardless of you not receiving it.

“The eyes of the LORD are everywhere, keeping watch on the wicked and the good.” (Proverbs 15:3)

We are not just dealing with a weaker rupiah. We are watching a feedback loop that is getting harder to break.

Start with refinancing. Around Rp833.96T of debt matures in 2026. This has to be rolled over in a risk-off environment, with the rupiah already under pressure. To clear the market, the government must offer higher yields. That pushes the interest bill, already about Rp599T per year or roughly 22% of tax revenue, even higher.

From there the dynamics compound. Higher interest costs compress fiscal space. Productive spending gets crowded out. Growth slows. And once growth slows, the core justification for continued fiscal expansion weakens. Investors reassess, and capital outflows accelerate.

Now add oil. A rising oil price worsens the picture for a net importer. Import bills increase, the current account deteriorates, and inflation pressures build. If fuel subsidies are maintained, the fiscal burden rises further. If prices are passed through, household purchasing power weakens. Either path tightens financial conditions.

The risk is not any single variable. It is the alignment of all variables in the same direction. A weaker rupiah inflates the burden of foreign currency debt. Higher oil prices widen external and fiscal deficits. A larger debt burden tightens fiscal flexibility. Limited fiscal room reduces the ability to defend the currency. That, in turn, reinforces pressure on the rupiah.

All of this is happening under the constraint of the policy trilemma. With open capital flows, markets will price fiscal credibility in real time. Any hesitation or inconsistency is immediately reflected in yields and the currency.

Foreign exchange reserves provide a buffer, but not an unlimited one in a sustained outflow scenario.

There is no crisis today. But the preconditions are in place. Without a credible shift in policy direction, today’s exchange rate risks looking benign in hindsight.

@KemenperinRI Shopee, tiktok, serupa jugaa. 21% + 1250 + blm termasuk ads. Bulan mei mau naik pula..

Jual barang 100ribu, kalau itung bersih gross masuk kantong paling 70-76rb..

Blm ongkir retur pembeli kita yg tanggung.

Some of my wealthiest friends and relatives don’t follow markets at all. No charts, no thesis, no screener. But they own BBCA. And their strategy is almost embarrassingly simple: if it drops more than 10% from their average, they buy more. That’s it. No stop loss, no scenario analysis, no ikut ikutan kelas.

And honestly? For them, it works. Because BBCA is a small slice of a much larger picture. Their real wealth sits in property, business equity, private credit. The stock portfolio is almost recreational. So the psychological math is completely different. A 30% drawdown on something that represents 3% of your capital is not the same animal as a 30% drawdown on something that represents 60% of your liquid savings.

Position sizing changes everything about what the right behavior is.

The “jangan cut loss, company bagus akan balik” logic is not universally wrong. It’s wrong when the position is too big relative to your total capital and your ability to stay solvent, patient, and rational while it bleeds. For someone with deep pockets and a 5% stock allocation, averaging down on BBCA is a completely reasonable strategy. For someone with 80% of their savings in one or two names, the same behavior is a slow liquidation of their financial future.

And this is one of the most common mistakes traders and investors make. They watch a conglomerate, a family office, or a big institution hold through a 40% drawdown without flinching, and they think “okay, that’s the move.” What they don’t see is that the conglomerate is only deploying 1 to 2% of their total capital into listed equities. The rest is in operating businesses, hard assets, and private structures that don’t mark to market daily. They’re not being brave. They’re just playing with money that genuinely doesn’t hurt if it disappears. Copying the behavior without copying the balance sheet is one of the most expensive mistakes in investing. You’re mimicking the surface. Not the structure. (example : orang X liat #NETV diakum di 120-150 lalu junam ke 70)

This is why copying the behavior of wealthy investors without copying their balance sheet construction is dangerous. You see the action. You don’t see the context that makes the action safe.

The real lesson here isn’t “cut loss always” or “hold always.” It’s: know what role each position plays in your total picture, then decide the rules accordingly. Most people skip that step entirely. They just react.

Mereka yang tajir tadi bukan gak ngerti risk. Mereka ngerti banget. They’ve just structured their life so that one position going wrong doesn’t change anything. That’s the actual edge. Bukan strategi-nya. The architecture underneath it.

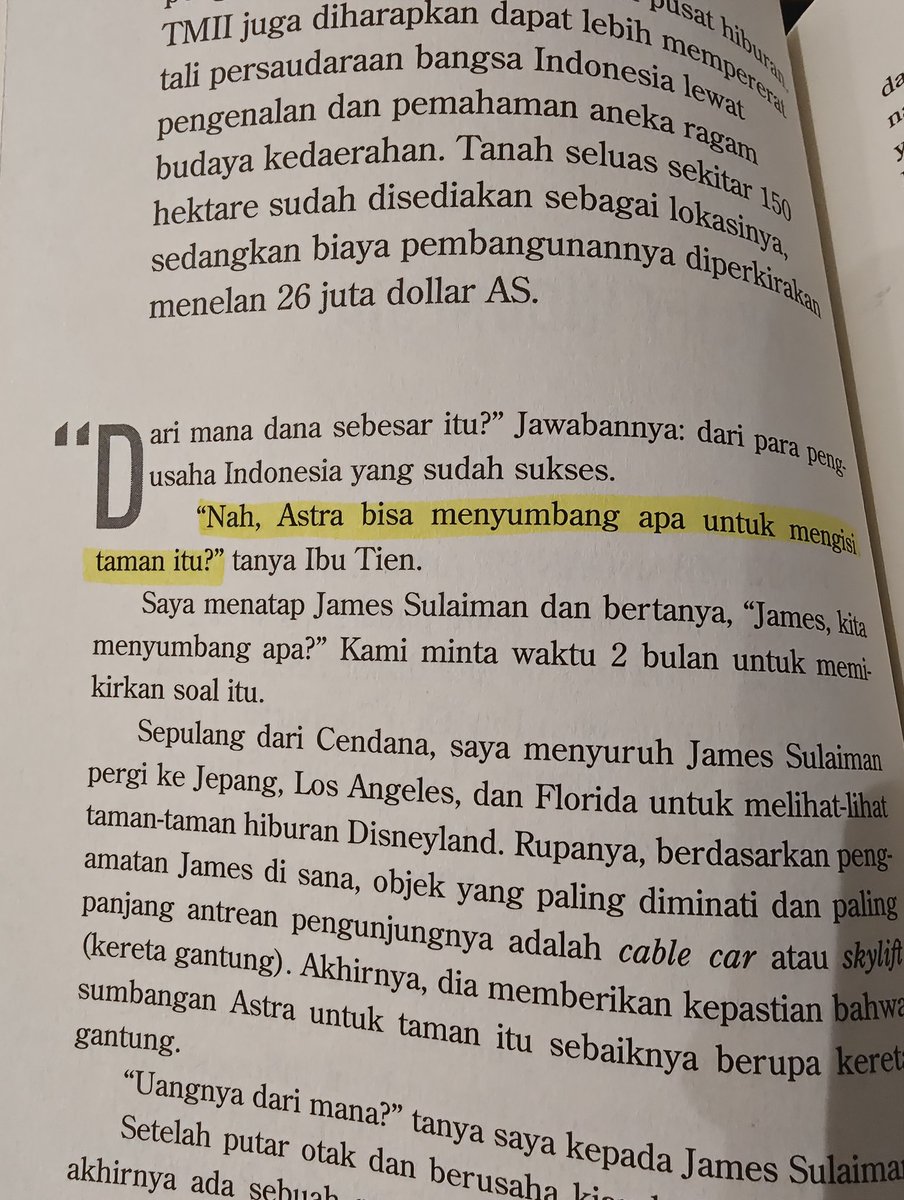

@hendrifisnaeni Banyak cerita yang tidak keluar terutama bagaimana cara "malak" di era itu. Contohny gondola TMII hasil malak astra. Jadi yg kreatif atau pintar bukan penggagasnya melainkan hasrat yg dipalak untuk harus memuaskan penguasa. Memoar Om William

@rzfjri@idfc_______@chrs_al@O5Bravo Karena commodity boom selesai diawal periode jokowi. dari peak jaman SBY coal turun -40% , sawit -50%, crude oil -50% di 1 tahun jkw.

SBY pro banget ekspor jadi pas commodity boom pertumbuhannya tentu mantap.

Cuma periode 2 jkw pakai uangnya ugal-ugalan sangat disayangkan

@neollexador Simply mereka ga pernah kepikiran aja, safety netnya lebar. Mereka juga ga tau rasanya mulai dari titik 0 atau minus.

Apalagi kalau spendingnya kenceng, ga bkl bs turun lifestyle. Gengsi is real.