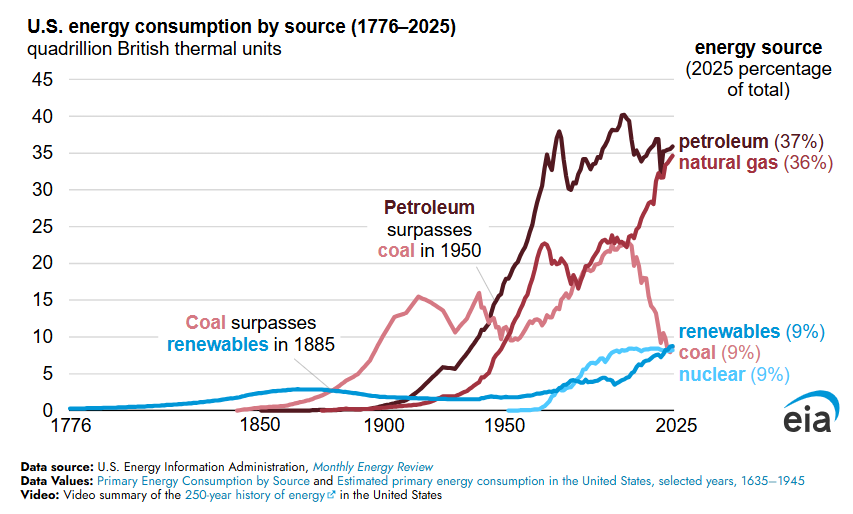

"The acquisition of fire and language made our ancestors fully human.

The adoption of agriculture laid the basis for cities, civilizations, and states.

The adoption of fossil fuels made us modern."

McNeill

🛢️The Exxon led consortium currently keeps 75% of Guyana's oil production to recover exploration and development costs.

Guyana takes 12.5% of profit oil.

Exxon expects to fully recover those costs this year.

When that happens, Guyana's profit oil share jumps from 12.5% to 50%.

At $100/barrel, that's roughly $4.3 billion in 2026 oil revenue 67% higher than last year.

Just from the price move.

The cost recovery flip adds further upside.

And the strategic position is structurally different from every other major producer.

Liza crude went from $68.98/barrel on February 27 the day before the Iran conflict started to a high of $120. Break-even cost: $25–35/barrel.💰

Guyana has direct Atlantic access.

In a world repricing geopolitical risk into every barrel, that's a structural premium that doesn't disappear when the ceasefire comes.

"The war may end next month, but it will be a changed world."

900,000 barrels per day from a country of 1 million people that was one of the poorest in South America in 2019.

GDP quadrupled to $27.5 billion between first oil and 2024.

The pace of development had no recent precedent.

But Oil and gas accounts for 75%+ of GDP.

Guyana imports all its refined products... no domestic refinery. ⚠️

So higher crude prices mean higher import costs for gasoline, diesel, fertilizer, food.

The structural bull case for Guyana is intact and strengthening.

The macro risk is the same one that has destroyed resource economies for decades: the politics of distribution when the money arrives faster than the institutions to manage it.

Full analysis on oil and infaltion in my latest article.

Link in the comments 👇

Qatar's LNG is offline for 3-5 years

The US was already building the replacement

North America's LNG export capacity could more than double by 2029.

This chart was drawn before the war.

Now it looks like a strategic masterplan ♟️

Projects coming online 2026-2029:

🇺🇸 Plaquemines — already ramping

🇺🇸 Corpus Christi Stage III — coming

🇺🇸 Golden Pass — Exxon/QatarEnergy joint venture

🇨🇦 LNG Canada — first Canadian exports

🇺🇸 Port Arthur — major capacity

🇺🇸 Rio Grande — massive scale

🇺🇸 CP2 Phase 1 — next wave

🇺🇸 Woodside Louisiana LNG — 2029

From 11 bcf/day today to 28+ bcf/day by 2029.

Ras Laffan produced 10 bcf/day.

Now offline for 3-5 years minimum.

The gap is enormous.

The US filling it is inevitable.

Every desperate LNG buyer (China, Japan, Korea, India, Europe ) now has one supplier capable of scaling at this speed.

🇺🇸 America.

Iran accidentally handed the US permanent LNG dominance.

This chart is the proof🛢️⚡

⚠️the issue:🇺🇸🇪🇺Europe Needs American LNG

In my latest article, I break down the 8 stocks best positioned for this trade name by name, mechanism by mechanism and explain exactly how each one gets paid as the next cargoes head to Europe.

the full analysis is in the below comments👇

El cambio climático afecta algunas regiones más rápido que a otras, con importantes implicaciones para la seguridad energética y el bienestar social. Lee el artículo de Vicente Germán-Soto (@UAdeC) y Ruth A. Bordallo (@ElColegiodeTam): https://t.co/VSbrO9KpPD, en el que examinan los patrones del consumo de electricidad en México, en respuesta a cambios de temperatura y desarrollo económico durante 2003Q1–2019Q4.

Consulta en #AccesoAbierto los textos de la revista @EstudiosEconom y recuerda que todas las revistas de investigación de El Colegio de México cuentan con un menú de accesibilidad en la parte inferior izquierda de su sitio web, donde podrás personalizar aspectos visuales como el contraste, interlineado, tamaño del cursor, texto y más.

The Middle East refines 13 million barrels of products every day.

The war just disrupted them.

2026 output (mbd):

→ Saudi Arabia: 5,350

→ Iran: 2,350 ← at war

→ UAE: 1,535

→ Kuwait: 1,496

→ Qatar: 626 ← LNG infrastructure damaged

→ Iraq: 769

This isn't just crude.

It's the products the world runs on:

→ Diesel: 2,381 mbd global freight

→ LPG: 2,609 mbd cooking, petrochemicals

→ Jet Fuel: 793 mbd aviation

→ Naphtha: 1,244 mbd Asian crackers

Saudi Arabia at 5,350 mbd is the only producer with scale to absorb the disruption.

It's already running hard.

Markets track crude.

The real stress is in refined products diesel cracks, jet fuel margins, naphtha spreads.