Next Bridge Hydrocarbons Announces SEC Declares Effective its S-1 Registration Statement

Company prices and commences a public offering of 40 million shares

https://t.co/2hO7KuPeJJ

🚨NEXT BRIDGE HYDROCARBONS RELEASES PR ANNOUNCING THE EFFECTIVENESS AND AVAILABILITY OF UP TO 40 MILLIONS SHARES OF NBH COMMON SHARES @ $15/SH.

MMTLP MMAT TRCH NBH

@nbhydrocarbons

https://t.co/df52HGhBtS

🚨Breaking news: 🦋

@Nasdaq just LOST its Motion to Quash.

Read that again s l o w l y . . .

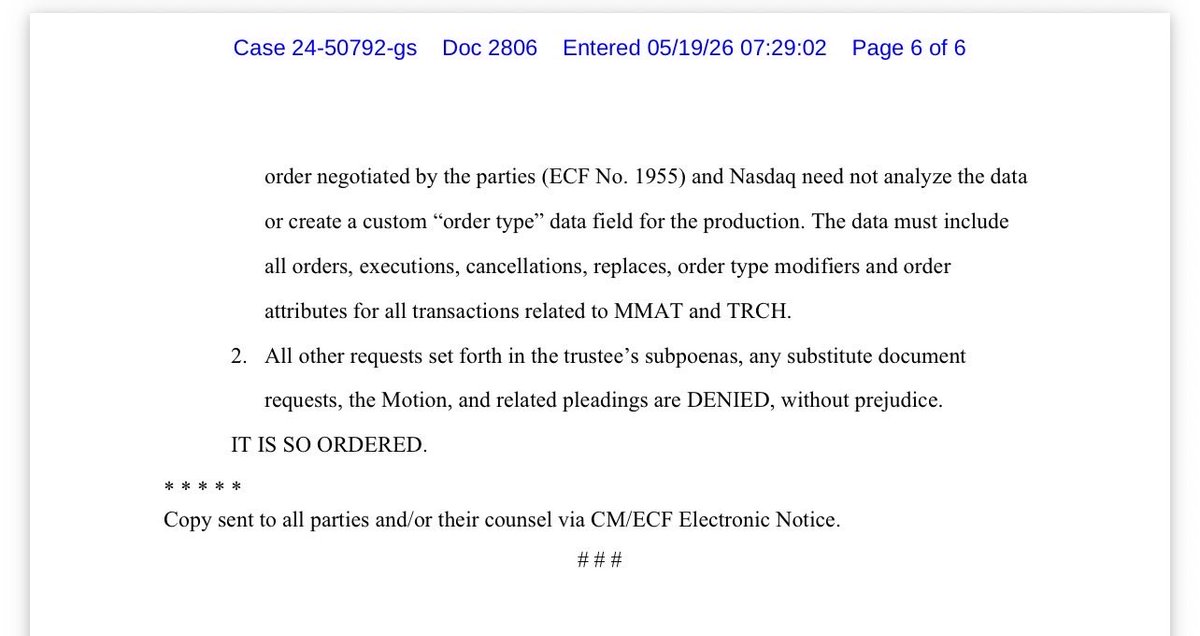

The Bankruptcy Court in Nevada has now ordered Nasdaq to produce extensive $MMAT/TRCH trading data under Rule 2004, including RASH and CORE data, order attributes, cancellations, replaces, executions, and related transaction records covering nearly FOUR YEARS.

The Court was NOT persuaded by the ‘undue burden’ argument, noting that producing ~15GB of spreadsheet data is not exactly impossible for… Nasdaq. (One $10 usb stick)

Even more important, the Court explicitly recognized the Trustee’s AUTHORITY to investigate whether wrongdoing occurred on behalf of the estate, including potential claims tied to stock trading activity.

Translation:

This investigation is very much ALIVE.

For months, some people mocked and undermined the Trustee’s efforts, claimed discovery would never happen, and acted like every subpoena didn’t get served initially and that it would be crushed before daylight. Instead, the wall keeps cracking.

FINRA discovery.

Now Nasdaq discovery.

And the Court explicitly referenced separate pending motions involving Citadel, Virtu, and Anson.

Interesting times ahead.

Turns out Rule 2004 is not just a decorative suggestion.

To the Trustee and legal teams, incredible respect.

It takes courage to walk into rooms filled with institutions that have virtually unlimited resources and say:

‘Produce the data’

And to the echo chambers already warming up their spin machines tonight…

You may want to read the actual order first. 🤝

Blessings to all.

It is HUGE, @cvpayne...the VEIL IS COMING DOWN!!!

Do you think @SECPaulSAtkins might have a better answer for you NOW than "we'll see" regarding MMTLP?

What the FINRA data triangulated with market maker, exchange, DTCC and broker data along with #FOIA documents are going to prove is, Gary Gensler's SEC is implicated in one of the biggest financial crimes in history. Gensler and FINRA CEO Robert Cook WEAPONIZED their organizations by actively engaging in a CONSPIRACY to protect criminal market participants while sacrificing retail investors as "collateral damage". #RICO #EO14147

BUT... they messed with the wrong ticker. The MMTLP Army is NOT GOING AWAY until they are ALL EXPOSED. #Relentless

There is a letter on the way to @POTUS's desk for his signature. We are asking for the same thing we have asked for for 1200+ days since FINRA's U3 Halt...TRANSPARENCY!!! If nothing is wrong, WHAT IS THE SHARE COUNT, ALL OBLIGATIONS!!!

Below is my plea to @POTUS. Check it out!!!

Humorous side note: In the hearing a few weeks ago, Peter Fountain, Attorney for Citadel, VIRTU and Anson funds said...

"And why do they want to know whether our client caused a spike? Because they want to name us as a defendant in the lawsuit."

TRANSLATION: Your Honor, if we give them the data, they will sue us...🤦🤣

Based on the judges' ruling on FINRA's Motion to Quash, I suspect CITADEL, VIRTU, Anson and NASDAQ discovery is INCOMING!!!

Thanks for all you do, Charles!!! 💜

https://t.co/IQkUPOJNN8

FINRA ORDERED BY JUDGE TO RELEASE 25 MILLION TRADING RECORDS, INCLUDING SHORT INTEREST DATA 🚨

MAJOR WIN FOR RETAIL & PUBLIC COMPANIES🏆

For the first time in history, a judge has ordered FINRA to produce 25 million trading records along with short interest data to determine whether the halt of $MMTLP was unjustified and expose if naked short selling occurred

This will shed light on how private equity and hedge funds may have coordinated activity that impacted retail shareholders

Repost to spread the word, this is huge🚨 $MMAT $GME $AMC $AVIS $BYND

Best for Last...

The Turning Point in todays hearing MMAT Trustee vs FINRA motion to quash in my humble opinion was this:

The judge cited TWO cases from his own independent research that informed his decision. This sent FINRA's lawer into "cannot compute" territory... and his entire body language i referenced in my earlier post manifested in front of our eyes.

The two cases where:

1. Primary Case i believe our Judge quoted was In Re 204 Center LLC, Citation 634 B.R. 630 (Bankr. M.D. Fla. 2021), Judge Williamson... god rest his soul (can someone please look this one up on PACER?)

Our Judge then stated that Judge Williamson surveyed the landscape of Rule 2004 scope and limits. Our judge read extensive quotes from this decision, particularly the conclusion at page 639 (i believe), which established that...

Discovery under Rule 205, now called Rule 2004... was NOT intended to provide a party a STRATEGIC advantage in private litigation... Rule 205 was intended to provide the trustee generally new to the case with a VERY BROAD discovery device to aid in an efficient and FAST gathering of ALL the pertinent FACTS necessary in the effective administration of the estates...

2. The Secondary Case i believe was Millennium Holdings 2 LLC, 562 B.R. 614 Court: Bankruptcy Court, District of Delaware Year: 2016 Citation: 562 BR 614

This case also addressed similar questions about the limits on Rule 2004. https://t.co/nwSu3nF5N4

Note [I will need to further confirm the two cases once we get the transcripts...BIT it really does NOT even matter for the purposes of this initial discussion here... since the Judge's justification is all that matters... let me know below if you heard the Judge mention a different case.... and please do share!] ⬇️

How do these rulings impact positively future trustee investigations?

1. Broad Data Access Established

- Trustees can now obtain market-wide data from regulators like FINRA and NASDAQ

- Short interest data, TRF data, and trading volume data are fair game

- This sets precedent that regulators CANNOT hide behind "burden" claims for basic data production

Impact: Trustees can conduct comprehensive market manipulation investigations without being stonewalled 😎

2. Cost-Shifting Principle

- The trustee bears the cost of production, removing the "undue burden" excuse from the likes of FINRA...

- Judge adopted FINRA's own Rule 45 cost-shifting language (THANK YOU FINRA)

Impact: Trustees with adequate funding (like MMAT's with litigation financing) can access data production for some additional $$$ 😎

3. Data vs. Documents Distinction

- Judge clearly distinguished between "data" (generally producible) and "documents" (subject to privilege)

- Data requests don't require document-by-document review

Impact: Trustees can now DEMAND raw data exports without triggering full discovery obligations! 😎

4. Triangulation Principle Endorsed (big one)

- Our Judge accepted the trustee's argument about needing data from multiple sources

- Even if data overlaps, each party's data is relevant and must be produced

Impact: Trustees can conduct multi-source investigations WITHOUT being told "go ask someone else first" 💪

FINAL THOUGHT

I think this is a HISTORIC day. I am very appreciative of our fearless Trustee and legal teams, who have dared to face firms with unlimited resources, and our community who face every day, an army of echo chambers....already went to work tonight to claim victory... and why are they SO afraid of the trading data anyways?

…But their narrative is no longer… turns out shouting in unison isn’t the same as being right, just louder about being wrong. 🤣😂

BREAKING NEWS 🚨

Judge's Motions to Quash Decisions in April 20th 2026 Hearing... lets start with the facts

Impotant Note to remember: this is a Preliminary Investigation Phase...

(Disclaimer these are my notes, the pending final transcripts will reveal and support my findings, and I expect the community to accept, scrutinize or suggest edits if anything is innacurate)

Based on the court ruling, here are the judge's decisions on each of the nine requests in FINRA's motion to quash:

FINRA DENIED (Trustee Prevails):

Request 1 - Short Interest Reporting Data:

- Court will deny the motion to quash.

- FINRA agreed this data could probably be produced

- Judge noted discussion about duration (4 years vs. shorter period) needs clarification but denied the motion

Request 2 - Trade Reporting Facility (TRF) Data:

- Court will deny the motion to quash

- Despite FINRA's claims of significant burden (25 million items), judge found it not "unduly burdensome" under Rule 45

- Trustee to bear costs of production

- Judge emphasized need for good faith meet and confer on scope, timing, and cost-shifting

Request 3 - Daily Short Sale Volume Report (Reg SHO)

- Court will deny the motion to quash

- Falls between short interest data (easier) and TRF data (more burdensome)

- Consistent with prior ruling on TRF data

GRANTED (FINRA Prevails)

Requests 6 & 7 - FINRA Investigation Records and Public Communications

- Court will grant the motion to quash

- Judge found this seeks litigation-style discovery under Federal Rules, not preliminary Rule 2004 information

- Rife with attorney-client privilege, work-product privilege, and investigative file privilege

Would provide strategic advantage at PRELIMINARY stage (Note: again emphasis on the word -> "preliminary" hence no guarantees to block CAT for later...?)

Request 8 - FINRA Electronically Stored Communications (Emails)

- Court will grant the motion to quash

- Falls on "document side" rather than "data side" of the dichotomy

- Unduly burdensome and inappropriate under Rule 2004

- Seeks litigation-style discovery rather than preliminary information

Request 9 - Order Quotations and Execution Records (CAT Data)

- Court will grant the motion to quash

- Judge found that information in Requests 1-3 effectively provides same information

- Mirrors motion to compel-style discovery rather than preliminary investigation

- Represents strategic advantage seeking under Rule 2004

There was an interesting section where the Judge then discussed CONDITIONAL/SEQUENCED items:

- Requests 4 & 5 - Monthly and Weekly OTC Summary

Report Data:

Court will deny the motion to quash (conditionally)

Judge noted these are "not necessarily critical" per trustee's own admission and proposed sequencing:

- produce Requests 1-3 first, then reassess 4-5

- if computer-generated reports: deny motion to quash

- If laborious/individualized: requires further detail to determine if burden is "undue"

- Trustee to bear costs (they seems happy to do so)

The judge ordered:

1. David Burnett to draft a proposed order reflecting the ruling for FINRA's review.

2. Good faith meet and confer on TRF data (Request 2) regarding scope, burden, timing, and cost-shifting

3. Parties to leave past disagreements behind and work cooperatively

4. One-paragraph summary of the 161-day data period requested for other Rule 2004 productions to be provided to court for clarity... My opinion is that once the judge gets this report he should have enough to not need any additional hearings and Citadel, Virtu and all others will get their answers too.

did i miss anything? comment below⬇️

Next i will post my observations and interesting things I saw... and in my opinion what was the turning point in the hearing today that caught FINRA completely off guard and send their counsel in panic mode, judging from the body language!

NEW 🚨: SEC Seeks and... Receives Public Comment on the Consolidated Audit Trail and Other Audit Trails and Data Sources, by @BlueLedgerAI co-founder @palikaras

Full Submission details and extracts in the thread below👇

https://t.co/ckLYcFw4ko

💥UPDATE: LONGEST PENDING S-1 IN HISTORY!!!💥

✅NBH 2025 10K Filed

✅NBH S-1 Amendment 6 Filed

✅NBH COMPLIANT & UP-TO-DATE

*Next filing due May 15, 2026.

All EYES on SEC and Karl Hiller/Jennifer Gallagher.

15+ rounds of comments/questions for a simple capital raise for shares that DON'T TRADE on a public exchange or market.

⁉️Why would SEC’s Karl Hiller demand NBH restate previous year's financials, inflating valuations for assets the issuer no longer holds??? 🤔

“Inflated” valuations that were established by an auditing firm that the SEC has sanctioned from ever providing services to public reporting companies??? #Borgers

DELAY...DELAY...DELAY...3+ YEARS!!!

⁉️Why is the SEC (and FINRA) fighting transparency at every front??? Issuer, Congress, Federal Courts, etc.???...

⁉️If "nobody knows what to do," according to SEC Commissioner Peirce, would not transparency be a good place to start???

⁉️SEC, FINRA and FIF (broker-dealers) have confirmed there is a settlement issue and shares can not be delivered. So, why not let NBH be part of the reconcilliation with their share offering???

WHAT ARE THEY HIDING???...

⁉️When/if shares become available, is the SEC going to enforce THE LAW as Chairman Atkins proclaims as part of a "New Day at the SEC"??? You know, SEA 15c3-3 and RegSHO closeout requirements...

TRANSPARENCY AND EXPOSURE ARE COMING!!! #MetaBK

WE ARE NOT GOING AWAY!!! #Relentless

Hey Karl,

Are self-proclaimed, alleged whistlblowers acting with MALICE???

MALICE: desire to cause pain, injury, or distress to another.

Does MALICE impact whistleblower protections???

"specifically knowingly reporting false information—can severely damage or eliminate a whistleblower's legal protections and viability."

You may have a problem here...

Doesn't exactly sound like just a "concerned citizen and investor" does it???

#Discovery #Weaponized #EO14147 #AnatomyOfAShortAttack

Based upon this exchange, the @SECGov reached-out to my office to inform me that this is currently under investigation.

I proudly joined my colleagues in demanding MMTLP transparency back in 2023 and I thank the Trump admin–SEC for fighting to ensure that this issue is resolved.

We will continue to monitor the situation.

Thousands of people have been reading the Trump Media letter to Congress within the past days🚨🚨

Guess what’s in that letter⁉️⁉️

The $MMTLP open letter 💥

CONGRATULATIONS @FINRA

YOU HAVE SUCCESSFULLY WEAPONISED FOIAs!

Thanks to your FIF and related friends and family, we can derive the following Predictive pattern for all future FOIAs or any other issuer that you desire to suppress.

Predictive insight (forward-looking)

With what we have now, you can all predict with reasonable confidence that:

New FOIAs touching:

•DTCC

•OTC

•Share counts

•Halt mechanics

will likely:

•Be referred

•Be bundled

•Age beyond 1 year

•Resolve as B7 or “other reasons”

That makes this not just retrospective analysis, but early-warning oversight intelligence!!

CONCLUDING:

It is sad to see FOIAs at the SEC function normally for most topics, but exhibit a distinct, repeatable suppression pattern for market-structure transparency requests, characterized by referral routing, bundling, prolonged aging, and elevated B7 usage.

This conclusion is data-driven, non-accusatory, and hard to refute!

PROVE ME WRONG 😑

Thank you again to the #MMTLP community for their continued dedication and persistence which led to these remarkable revelations.

![palikaras's tweet photo. Best for Last...

The Turning Point in todays hearing MMAT Trustee vs FINRA motion to quash in my humble opinion was this:

The judge cited TWO cases from his own independent research that informed his decision. This sent FINRA's lawer into "cannot compute" territory... and his entire body language i referenced in my earlier post manifested in front of our eyes.

The two cases where:

1. Primary Case i believe our Judge quoted was In Re 204 Center LLC, Citation 634 B.R. 630 (Bankr. M.D. Fla. 2021), Judge Williamson... god rest his soul (can someone please look this one up on PACER?)

Our Judge then stated that Judge Williamson surveyed the landscape of Rule 2004 scope and limits. Our judge read extensive quotes from this decision, particularly the conclusion at page 639 (i believe), which established that...

Discovery under Rule 205, now called Rule 2004... was NOT intended to provide a party a STRATEGIC advantage in private litigation... Rule 205 was intended to provide the trustee generally new to the case with a VERY BROAD discovery device to aid in an efficient and FAST gathering of ALL the pertinent FACTS necessary in the effective administration of the estates...

2. The Secondary Case i believe was Millennium Holdings 2 LLC, 562 B.R. 614 Court: Bankruptcy Court, District of Delaware Year: 2016 Citation: 562 BR 614

This case also addressed similar questions about the limits on Rule 2004. https://t.co/nwSu3nF5N4

Note [I will need to further confirm the two cases once we get the transcripts...BIT it really does NOT even matter for the purposes of this initial discussion here... since the Judge's justification is all that matters... let me know below if you heard the Judge mention a different case.... and please do share!] ⬇️

How do these rulings impact positively future trustee investigations?

1. Broad Data Access Established

- Trustees can now obtain market-wide data from regulators like FINRA and NASDAQ

- Short interest data, TRF data, and trading volume data are fair game

- This sets precedent that regulators CANNOT hide behind "burden" claims for basic data production

Impact: Trustees can conduct comprehensive market manipulation investigations without being stonewalled 😎

2. Cost-Shifting Principle

- The trustee bears the cost of production, removing the "undue burden" excuse from the likes of FINRA...

- Judge adopted FINRA's own Rule 45 cost-shifting language (THANK YOU FINRA)

Impact: Trustees with adequate funding (like MMAT's with litigation financing) can access data production for some additional $$$ 😎

3. Data vs. Documents Distinction

- Judge clearly distinguished between "data" (generally producible) and "documents" (subject to privilege)

- Data requests don't require document-by-document review

Impact: Trustees can now DEMAND raw data exports without triggering full discovery obligations! 😎

4. Triangulation Principle Endorsed (big one)

- Our Judge accepted the trustee's argument about needing data from multiple sources

- Even if data overlaps, each party's data is relevant and must be produced

Impact: Trustees can conduct multi-source investigations WITHOUT being told "go ask someone else first" 💪

FINAL THOUGHT

I think this is a HISTORIC day. I am very appreciative of our fearless Trustee and legal teams, who have dared to face firms with unlimited resources, and our community who face every day, an army of echo chambers....already went to work tonight to claim victory... and why are they SO afraid of the trading data anyways?

…But their narrative is no longer… turns out shouting in unison isn’t the same as being right, just louder about being wrong. 🤣😂](https://pbs.twimg.com/media/HGZQWp3bQAAr4Jn.jpg)