Q: “How did you go bankrupt?”

A: “Two ways. Gradually, then suddenly.” Ernest Hemingway, The Sun Also Rises

The chart below shows the prices of BSL and DL loans one year before default vs. default date. By the default date, direct lending loan recoveries fall below 50 cents, from prices above 80 just one year earlier. Broadly syndicated loans show a similar pattern, declining from the high 70s to just above 50 cents during the same period. The lesson is simple: the longer you wait, the more it costs.

Bottom line: deal with problems early, and the outcome is likely to be better.

The real damage occurs long before the bankruptcy filing. A deteriorating business model, covenant breaches that are not adequately addressed, bad PIK that digs a deeper hole for the issuer, cash burn, and more. Just as Hemingway’s bankrupt character did not wake up broke overnight, companies rarely arrive at distress without warning signs. Deteriorating earnings, shrinking liquidity, customer concentration, margin pressure, management turnover, and excessive leverage are just a few of the key signals that are usually visible well before an out-of-court restructuring or bankruptcy filing.

Proactive, forward-looking asset management plays a critical role in monitoring performance, identifying trends early, and having the discipline and experience to maximize outcomes. Every day, month, and quarter spent ignoring those signals increases the probability of default and decreases recovery value for existing lenders. What could have been a manageable problem may become a much bigger one. For companies that are on plan or ahead of plan, lenders should allow management to operate and let their winners win. But for companies that are falling behind, lenders are well served to have constructive conversations with borrowers and sponsors and take initiatives to help them get back on the right path.

Takeaway #1: Address problems early. The earlier a problem is confronted, the more value can be preserved.

Takeaway #2: Sell before default, if possible.

Takeaway #3: Covenants are important because they force meaningful conversations with the borrower.

Takeaway #4: BSL is liquid credit. Direct lending offers considerably less liquidity, so it is important to be ultra conservative, lending to non-cyclical businesses owned by strong sponsors, with healthy operating margins and cash flow, and the right capital structure.

Takeaway #5: Covenants are rare in BSL, however DL should never give up key covenant protection as this would render asset management somewhat ineffective prior to default.

The Great Software Divide: Code that once took teams of engineers can now be replicated by AI in minutes, destroying the moat around legacy software companies. The weight of this gravity will be defied by AI-first software companies, the same force becomes creates a multiplier effect. Cube the legacy base by its AI coefficient and you will notice that the AI-native software companies gain mass exponentially and soar, while legacy implodes under its own weight. Winners and losers with little middle ground that defines outcomes.

What's in your Red Box?

Highly leveraged software companies represent the largest sector concentration within private credit, comprising ~26% of NAV for leading BDCs and ~23% of direct lending funds. Managers with less than 10% software exposure are well positioned; those with significantly greater exposure have a tough road ahead. By its very nature, credit risk is idiosyncratic, and many software names will perform well, while others will not transition in the era of AI. There are varying opinions on this topic, and that is what makes markets, yet I maintain my stance that the AI induced SaaS Apocalypse will leave an indelible mark. The die is cast; as the saying goes “you've made your bed, so you must lie in it" as there is limited secondary liquidity options in private credit, outside the Top 50 PC loans.

Leading Wall Street investment banks have begun to address the pending software default cycle. Barclays just published a report entitled "When Tides Turn" that draws parallels to the TMT crisis post the dot-com bubble 25 years ago as they argue AI has created a similar paradigm shift for the software industry. Barclay's highlights the maturity wall for highly leveraged software companies that will bear down in the next three years. Questions arise about whether sponsors and lenders will provide ongoing support when loans come due. The report questions if recovery rates on defaulted software credits will be far lower compared to other industry sectors, noting the collapse of the high yield energy credits a decade ago stating: "Defaulted software assets, in our view, do not have much salvageable value, particularly in the age of agentic AI." OUCH!

Claude Code, Codex, and Cursor now replicate in hours what took days, months, and years to build. The competitive moats protecting these businesses have been structurally compromised. Public software companies with strong unit economics and Rule of 40 (revenue growth + profit margin ≥ 40) will likely prove undervalued as they transition to a AI-first world, create significant enterprise value along the way. Private credit borrowers with 6x to 10x leverage, whose growth curve has flattened and enjoy little free cash flow after debt service, is of concern.

The chart below shows the Red Box with cumulative default rates of 30% to 40% and recovery rates of just 30% to 50% for leveraged software companies. While I believe that the recovery rate range in Barclays Red Box is a good estimate, I believe the loss rates due to default will prove to be more severe. My Red Box is centered around 15% to 20 % recovery rates.

Where do you draw the red lines for software?

The High Yield bond market is very different than the 'Junk Bond' market of yesteryear. Today's High Yield contains much stronger credit quality than historically had been the case. Within the $1.5 trillion marketplace for HY bonds, BB-rated bonds now represent a greater share of the index than B and CCC-rated bonds combined (see graph below). For the first time this century, CCC-rated bonds account for less than 10% of the HY index weighting. The High Yield market size has remained the same size for the past decade, with aggregate face value of circa $1.5 trillion. Software names comprise a mere 3% of the HY bond index, likely leading to the HY market to perform well as higher likely defaults within the software sector is well contained, allowing investors to comfortably allocate to HY as capital allocators have greater confidence to add incremental yield to their global fixed income and credit portfolio.

This Rising Star is the GOAT

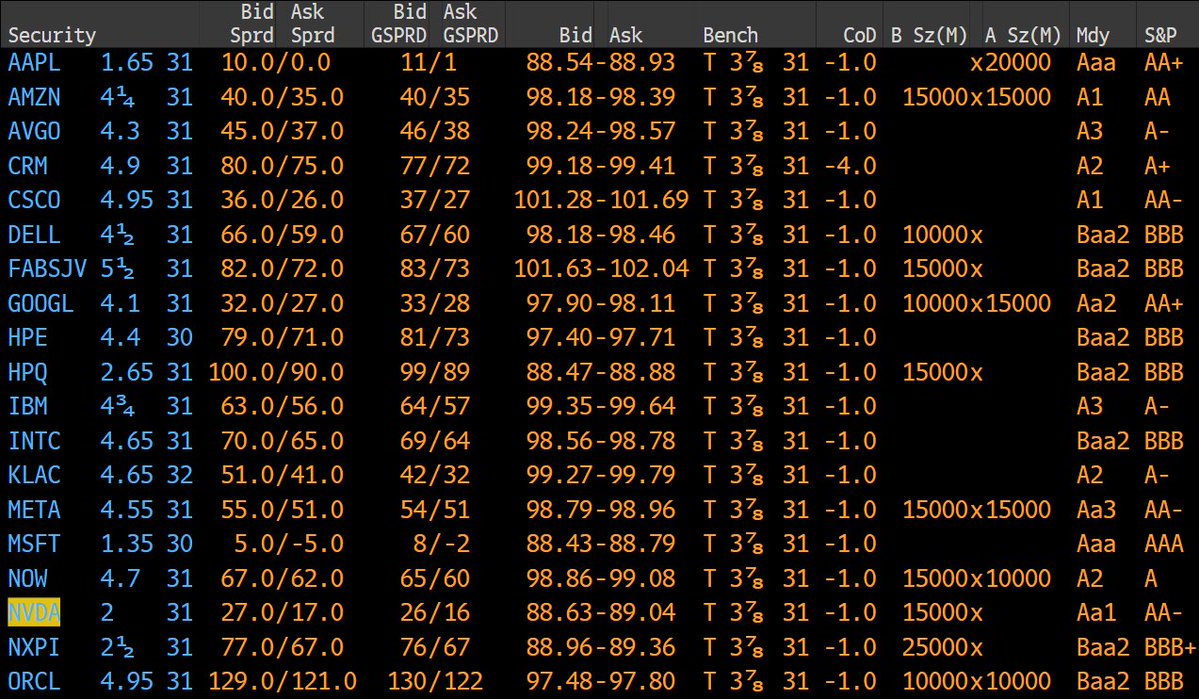

Rising Star: the reference to a credit that migrates from High Yield to Investment Grade. The biggest leap is SpaceX, securing a $20 billion loan from Goldman Sachs, BofA, Citi, JPMorgan, and Morgan Stanley at a spread of roughly SOFR +100 bp (a mid-4% coupon) not too dissimilar to the borrowing costs of IG-rated companies such as Meta, Dell and Google (see table below for comparison vs. other IG tech companies). This is remarkable since this $20 billion loan refinances $17.5B of debt of which some yields 12%+, as the debt stack of the company held a range of +500 to 800 bps over SOFR. This saves SpaceX ~$1 billion debt service costs annually. BBB- rating, however, the rating agencies are notoriously conservative and would likely make a mistake rating SpaceX debt BB+.

Perspective 1: Currently SpaceX is non-rated currently, however, is priced as B- credit or CCC+. Looking forward, SpaceX should be able to secure a BBB- rating, however, if the rating agencies take a conservative approach, they may rate SpaceX debt BB+.

Perspective 2: Major bank lenders/investment banks have committed to underwrite next month's IPO of SpaceX IPO and based upon the expected market value of ~$2 trillion, $20 billion in debt is relatively inconsequential as it represents a mere ~1% of market cap. Further, SpaceX will have ~$80 billion in cash post-IPO on its balance sheet, so net-debt becomes negative. Just last year (June 2025), xAI 12.5% secured notes were priced at a slight discount to par, one of the five debt facilities that is being refinanced with the new bank facility.

GOAT: The largest U.S. IPO was Facebook in 2012 at a $104 billion valuation. SpaceX is the GOAT with a valuation that is likely to be priced at ~$2 trillion. A unicorn is a venture funded startup that is privately held with greater than $1 billion valuation, and when the term was first assigned on this basis it was a rare occurrence, thus the name. There have been over 2,000 unicorns created, but SpaceX is the first $1 trillion-plus company, which is indeed a generational event for both credit and equity markets. The June 12 listing on Nasdaq (SPCX) will be a momentous day, and there will be much more for us to discuss.

Public Credit Markets are vibrant with the rally in risk assets well appreciated, in sharp contrast to the recent performance of 'risk-free" assets (UST).

With the exception of software credits and wrong-way idiosyncratic situations, investors recognize the inherent value in the private and public credit markets which is highly encouraging.

Credit selection is critical; the payoff is well-worth the work.

Stay invested and enjoy the long holiday weekend.

Below is BofA's Daily Credit Run.

The LP Prisoner's Dilemma

Game theory is playing out in real time across private credit. Investors with capital tied up in open ended structures who have submitted redemption requests, or are contemplating whether to remain invested, may want to consider the dynamics of the prisoner's dilemma. For investors who decide to redeem, game theory is to get out before the fund level gate (~5% per quarter) is imposed. If too many LPs cut at the same time, not everyone will be able to redeem in full. Those who are not fully paid out must remain patient as their next distribution tranche is deferred to following quarters, leaving their remaining capital at risk inside the fund. If more than 95% of LP capital holds, this is a non-issue, as the fund manager most certainly has sufficient liquidity to meet quarterly redemptions below the 5% threshold.

Open-ended funds are constructed to handle redemptions. Despite the headlines, gates are not a bug, they are a well-designed structural feature, carefully constructed to allow each LP to redeem in an orderly fashion, while protecting the remaining investors. The single most important factor is the quality of the actual investments, as the structure itself is sound.

Over time, NAV and redemptions should stabilize, but this depends entirely on the quality of the underlying assets. If the manager has done a solid job investing, the LP will likely enjoy healthy returns, as Direct Lending should present attractive IRRs. However, if the fund has heavy exposure to highly levered software companies or have made other poorly performing loans, the investor in an open-ended fund will likely face a classic prisoner's dilemma: each LP's rational move is to redeem early.

Some Investors have begun to question marks. When credit markets and loan performance are strong, there is little variance in marks, as performing loans mature at par. However, when covenants are breached, loans extended/amended or PIK'ed, and default rates rise, then serious questions emerge about valuations, including whether the fund is marked to model vs. third party mark to market? Regrettably, for those managers who are saddled with risky loans and heavy software exposure, there are more questions than answers at this juncture.

The second order effect is equally important. When a fund sells its best, most liquid loans meet redemptions and use available cash to pay out departing investors; adverse selection becomes the defining risk. The remaining LPs are left holding a concentrated book of weaker credits. Further, in this case, the manager has diminished reinvestment capacity, worse liquidity. Staying becomes less rational precisely because others choose to leave.

Takeaways: 1) corrections are healthy, create a better playing field going forward, 2) know what's in the portfolio, insist on transparency as it truly matters at times like this, and 3) the best managers, those with the highest quality books will emerge from this cycle stronger than ever.

The UK suffered a shocking 100k job loss in one month—the largest in over a decade outside the peak COVID period. Surging gilt yields, heavy energy import dependence, and political uncertainty add to the pressure, painting a turbulent picture.

When opportunity knocks: Invest in the UK during turbulence, you’ll be rewarded, “buy when it goes on sale” is a motto for savvy credit investors. UK will always be the United Kingdom!

Credit Risk trumps Duration Risk

While Treasury bonds have delivered poor returns (30-yr UST yield has risen from ~1% to over 5% since 2020), falling 20 points since earlier this year. A well-constructed credit portfolio has compounded returns, clipping coupons that continue to generate an attractive absolute return. That is the asymmetry investors are taking note of. The 30-year bond has a 17-years of duration risk, with a yield less than 1/3 of this price risk (100bps move). Given higher inflation, a rising R*, the harsh fiscal backdrop with soaring deficits; bond vigilantes are on the hunt, until the Strait re-opens (inflationary pressure resides). When rates move like they have recently, equity markets may also respond (see UBS chart below).

The 30-year Treasury trades at 5.18%, its highest yield since July 2007. The 10-year hit 4.69%, a one year high, 2-year at 4.13%, as the markets price the potential for the Fed to tighten next year. April CPI printed 3.8%. Brent crude is above $100 on the Iran conflict dragging on. A Bank of America survey just released shows 62% of global fund managers expect the 30-year to reach 6%. The 30-year UK gilt sits at its highest level since 1998, while JGB 30-year just hit a record high yield, as its long bond is down 60 points from when it was issued 5 years ago. This is a coordinated global repricing of term premium, not just a domestic U.S. rate story.

My view is to invest with the best, maintain discipline in your Credit book wins, it has the potential to deliver absolute returns and selectively hire investment managers who will design and actively manage a well-constructed private credit portfolio that captures SOFR plus wide spreads, avoiding duration risk and generating consistent cash flow every quarter/year.

Green, Black, or Blue, but never Red:

When I was a young, up and coming trader on Wall Street, I believed in FILO (first in, last out), not for face time, but to learn every element about what makes the markets tick. As part of my daily routine, I marked the trading book at the close of business daily, which usually took 1 hour, to make sure every line item was accurate, and the P&L was perfectly stated, without exception. I was taught at a very early age that integrity is everything; your word is your honor. I learned this in my household growing up as a young boy as my loving parents always stressed these values, which were reinforced when I arrived on Wall Street.

In these early years of my career, I sat immediately to the left of the Head Trader, a big, boisterous fellow who had the tendency to yell when he wanted to teach lessons, which I was on the receiving side from time to time. These episodes taught me to have thick skin and never to give into pressure, a trait that came naturally. He would often slam his fist or break the phone receiver when slamming that into his trading desk, usually when markets went against him. Not exactly my style, but I was a young professional just starting out, reporting directly to him, so you suck it up. There was never a day that I did not learn, so I cherished every day, every minute, including the uncomfortable moments like this.

One evening as I marked the book, he grabbed the pen out of my hand, broke it in half, threw it in the trash and said, "Don't ever write with a red pen on my desk! Red means losses. Write in green, black or blue, but never red." I laughed inside as I nodded in agreement, and kept my mouth shut. I have never been superstitious about such silly things as the color of a pen and found this somewhat humorous.

This episode taught me the lessons I carry to this day. There are 261 business days in a year. You will have up days and down days. Do not get too high on the wins and do not let the losses consume you. Learn from your mistakes, recalibrate, and perfect your game. Do not be emotional. Make smart decisions by taking all vectors of information into account, knowing what is most relevant that will drive the outcome. If you are talented, and I never doubted myself, and you work exceptionally hard, you have edge as the credit markets offer exceptional opportunity to prosper.

Create your own luck. That does not come from the color of your pen. It comes from preparation, from knowing your markets, the risk factors working when nobody is there watching.

Know how to take a loss and move on. The great ones in this business are not the ones who never lose. They are the ones who build bigger wins that offset manageable losses, who stay disciplined when markets are volatile or dislocated, with a talent to understand relative value and credit selection.

"Luck is what happens when preparation meets opportunity." by famous Roman philosopher

Japan’s Yield Curve Control Trap:

For years, the BoJ aggressively enforced yield curve control by purchasing massive quantities of JGBs to suppress yields, pushing yields to record lows (negative), given deflation and weak growth, which artificially propped up JGBs, creating a dangerous distortion.

The 0.70% JGB maturing March 2061, that was trading at par, has since collapsed to 39 cents on the dollar over the past five years as the BOJ loosened yield controls and let the market determine JGB rates. Banks, pension funds, and local savers in Japan, are now burdened with heavy losses in their JGB holdings.

Buyer Beware: When CBs manipulate their govenrmnet bond market, reality and normalization can lead to a brutal awakening.

Bond Vigilantes are Back!

Global rates are moving higher around the globe, given the recent surge in inflation, persistent fiscal deficits (U.S: 6%+). Bond investors market now demand more compensation for taking on duration risk as seen. The most extreme move is the JGB which traded as low as 0.02% (near zero) and now trades at 4% resulting in a 45-point price decline with a nominal 0.1% coupon that does nothing to dull the pain of the decline.

Bond vigilantes are back when they take large levered short positions to punish government bonds when inflation, deficits, and issuance surge. Inflation (CPI, PPI) has recently been driven by the surge in energy costs and clearly the catalyst for this move. Even when central banks keep the front end tethered to official rates, longer term treasury borrowing costs can surge sharply as was the case in the U.K., Japan, U.S. and elsewhere (see Bloomberg table below; Friday closing price/yield). The 10-year is the most widely followed benchmark; however, the CBs have even less control of 30-year treasuries, unless if they re-start QT and buy outright; which Kevin Warsh has stated he will not do.

Central banks have been the critical determent rates; however, Bond Vigilantes are watching closely to see if CBs will allow market forces to now set the tone.

Fundamentals led the move, and now technicals are catching up, driving further weakness in price and higher yields. As the R* is moving higher (neutral rate assumption is being reset upward), long-duration assets.

Rates can rip the other way too, but it will likely take real progress towards reopening of the Strait, bringing down the cost of energy, which is a supply shock CBs can do nothing to control.

Takeaway 1: The good news is that fixed income and credit investors are being paid a higher absolute yield for taking on risk (nominal, not real).

Takeaway 2: The economy is growing above trend with a positive outlook for GDP growth, especially for those countries with positive net exports of energy (oil, gas).

Takeaway 3: Credit spreads perform well in this environment, unless the economy is to slow materially, which is not my base case.

Takeaway 4: HALO performs extremely well in this environment (both debt and equity).

Q: Is this repricing a temporary spike, or the beginning of a longer reset in global rates? If it is a longer reset, will policymakers tolerate higher long-end yields, or step in before markets force their hand?

The Friendly Skies

Aircraft leasing is one of the most compelling corners of ABL. Single aisle Boeing and Airbus commercial aircraft are mission critical assets for any airline. Today, roughly 53% of the global commercial fleet is leased (47% owned). Airbus and Boeing order backlog stands at approximately 15,500 aircraft, or roughly 8 years of production/back-order wait list time to take delivery. Given this dynamic, there is extraordinarily valuable in aircraft ABL, generating significant MOIC relative to other segments of ABL. Yet, there are risks.

Earlier this month, Spirit Airlines made the painful decision to cease operations and liquidate its fleet of aircraft. In bankruptcy, airlines have 60 days to affirm or reject aircraft leases under Section 1110, and they almost always affirm, since the vast majority of airlines that file for BK continue to operate as a going concern. Since 2000, the 3 major airlines used Chapter 11 to restructure (American, United, Delta all did) with exceptionally strong operating businesses today.

Spirit Airlines is the exception; it's the first U.S. airline with 100+ planes to not emerge from BK. The last liquidation of an U.S. based airline flying 100+ aircraft was Eastern Airlines, when it shuttered in 1991. Spirit ceased operations with 173 planes.

Under Section 1110 of the Bankruptcy Code, airlines have 60 days to affirm or reject aircraft leases in the event of default. Aircraft is mission critical for any airlines, except for an airline that liquidates. If a BB-rated airline have a ~5% probability of default during the next 5-years, and in the event of default, a ~90% probability that the lease will be reaffirmed, which is typically the case for newer aircraft, then there is less than 1% chance that they aircraft will be repossessed. When things go south like the recent case with Spirit, the lessor will likely call the the repo man

Inflation is your friend because aircraft values hold value relative to depreciation schedules.

Three big questions that ABL investors may want to know are: 1) COVID- how did the aircraft portfolio perform during this period when few people were flying during the 1-year COVID lock-down?, 2) Russia- did my ABL manager lose any of its aircraft portfolio when Russia took possession of ~550 commercial airplanes in 2022 when it surprisingly invaded Ukraine?, 3) how many aircraft investments have resulted in loss due to counterpart risk?

The math is compelling: mission-critical assets, inflation-protected values, a multi-year production backlog, and structural demand that only grows. For experienced ABL managers with dedicated and highly experienced aviation teams, the skies are indeed very friendly.

Macro Monday Themes:

1. New Fed Chair arrives this week, yet old Fed Chair stays on, which will create intrigue, drama, frustration, divided Fed and lots of headlines.

2. Jobs remain steady with +115k job growth in April, despite aging population and net-loss of immigration.

3. Inflationary data this week (CPI tomorrow, PPI on Wednesday), likely to prove worrisome, given the impact from higher energy prices; will we get a 4% PPI print?

4. Fed is on hold for foreseeable future with strength of economy and firmer inflation; Divided Fed Board, dispersion between hawks/doves, results in neutral policy stance most likely outcome, Powell remains a voting member if he stays on.

5. AI is inflationary, AI is deflationary are both argued in the press; my take is AI is slightly inflationary in the short-run for PPI, and significant more deflationary in the long-run for CPI.

6. AI build-out (data centers, chips, compute power) revised upward to $800B in 2026, over $1T in 2027 will be a huge driver for GDP growth requiring significant investment and debt financing.

7. President Trump will meet Chinese President Xi in Beijing on Thursday/Friday, first US president to visit China since Trump’s last visit in 2017. Trade, tariffs, rare earths, Taiwan, Iran discussions-negotiations.

8. S&P 500 Q1 earnings rose +27% y-o-y, with 84% beating estimates (90% reported), a stunning improvement as tech, financials and materials led the way.

9. Earnings strength coming through supported by +2% GDP gain in Q1, remain constructive since Q2 GDP forecasted to grow 3.7% (GDPNow), and Q2 corporate earnings forecasted to grow 15- 20%.

10. IPO market is re-opened for business with equities ATH.

11. IPO Unicorn?: never has a U.S. company with $1T market cap ever IPO'ed, the new unicorn benchmark since this has never occurred; In the coming year, expect three IPO Unicorns (SpaceX, Anthropic, OpenAI).

12. India's equities are down 10% y-t-d led by -25% in software/IT Services sector vs. South Korea's KOSPI +76% y-t-d, led by SK's leading semiconductor stocks up +140%.

13. AI & Chip valuations continue to surge, representing the biggest market advance in 2026.

14. Credit spreads back toward tight end (ex-software) in non-IG market (+300 high yield spread), as demand and credit conditions remain constructive.

Money Movers

Great to be on CNBC with Sara and Carl today (full interview clip below), where we discussed opportunities in private credit, rising interest in AI, and more.

8 Key Takeaways:

- Best vintage for opportunistic credit since the GFC: Turbulence in DL and credit markets, impact from higher oil prices leads to dislocation, while the strong growth/CapEx environment requires capital solutions

- America’s AI buildout: is enormous driving demand for financing.

- Europe: My meetings with 50+ institutional investors, insurance companies and private wealth bank platforms in Europe last week were hugely encouraging as investors are strategically allocating new capital to DL, ABL and Opportunistic Credit. Credit markets are strong, vibrant with the exception of software names, noting European credit market has materially lower software exposure vs. U.S.

- DL: The last 2 vintages may be troublesome for U.S. DL managers due to heavy software exposure, but next vintage will be strong as managers now have their eyes wide open and won’t be making the same mistakes in software.

- ABL: The total fund AUM for ABL is just $500B vs. $1.8T for DL; investors have 1/3 to 1/4 of the capital allocation to ABL than they do to DL, most are actively looking to rebalance by adding ABL.

- CBs: Hiking rates would be a policy error as current inflation pressures are largely energy-driven rather than demand-driven; rate hikes from the Fed and ECB would slow economic growth without meaningfully reducing inflation.

- AI is fueling markets: huge financing needs, with $750B spend in 2026; the math to build 1 gigawatt is: land cost for 500 acres and the data center box = $3 billion plus what goes in that box costs around $40 billion including chips, racks, wiring, power systems and cooling infrastructure.

- Software: Winner and Losers as this will be a tale of two cities; many highly leveraged private software companies funded by DL won’t make the AI transition to an AI-first software company. Hardware (semis and chips) leads to software costs coming down as hardware is used for coding, that has knock on impact of hurting many software companies, so "hardware eats software" is the new concept as coding becomes a commodity.

https://t.co/8z7IfRNCD4

Marathon Asset Management CEO @Bruce_Markets thinks we're approaching the best vintage for opportunistic credit since the Great Financial Crisis – here's why:

https://t.co/eUIWlOJcjg

Blockchain: The Infrastructure that Banks and Investors Should Not Ignore

Recent fraud allegations that MFS (U.K.) and Tri-Color double pledged collateral across multiple lenders is nothing short of alarming. This is not a new risk. It is a structural flaw tied to fragmented systems, delayed verification, paper and e-mail trail with a reliance on representations rather than real time fact-based truth.

Every loan could carry a single, immutable record of origination, ownership, lien status, and payment history. Title, servicing activity, and collateral pledges would be visible to authorized participants in real time. A loan cannot be pledged twice if the system of record enforces uniqueness at the asset level.

Blockchain eliminates this vulnerability entirely. This is not theoretical; the technology exists today.

Every origination event, title transfer, lien, warehouse pledge, repo, securitization and payment is recorded as an immutable, timestamped hash on a public or permissioned ledger. The record cannot be altered. Every counterparty sees it in real time. Double pledging becomes structurally impossible when a single authoritative registry marks each asset as encumbered at the moment of pledge.

Warehouse lines reflect the precise collateral position at all times. Principal, interest and tax payments are logged instantaneously on the ledger. If the loan moves to repo or securitization, that event is captured sequentially, in chronological order, with zero latency and no paperwork. Investor can examine the chain of ownership and evaluate the complete payment history.

The same process extends beyond loans as it is as easily applied to the securities and futures markets. Every securities transaction, repo, sale and purchase agreement benefit from instantaneous, immutable settlement as does home loans, auto loans, CRE loans, corporate loans.

Jamie Dimon wrote in his April 2026 shareholders letter that JPMorgan needs to roll out its own blockchain, as Tricolor and MFS blew up from the exact fraud blockchain would have prevented. Given recent events, the cost of inaction is becoming clearer; Jamie knows this and so do the regulators. In 2026, the age of technological change, the question is not whether blockchain belongs in the credit infrastructure; the question is why it has not been widely adopted. As often is the case, Jamie is spot on in his belief.

Complexity Risk rewards in the Public Credit Markets:

Structured Finance represents a highly complex and inefficient marketplace. Experienced and highly skilled investment managers can extract significant alpha in the ABL, ABF, and public securitization markets. Today's focus is on the public securitization market.

There are more than 50,000 unique and separate CUSIP securities that comprise the securitization market (ABS, RMBS, CMBS, CLO). By comparison, the U.S. listed equity market has approximately 5,500 stocks. The securitization market is vast and complex, covering a diverse range of assets across a wide-ranging ecosystem.

Pricing is not uniform; within residential mortgages, commercial real estate properties, auto loans, for instance, every trust is comprised of unique loans.

Documentation is critical. Trust indentures, pooling and servicing agreements (PSAs), credit support annexes, and offering memoranda span hundreds of pages, with jurisdictional variations across states adding further complexity.

Securitizations are inherently complex when it comes to structure, with varying rules for distribution of cash flow defining the waterfall of interest and principal. For example, the CMBS market alone has approximately 1,600 separate securitizations backed by thousands of different property loans with more than 9,000 unique tranches, as the average transaction carries seven tranches, each with its own rating and liquidity profile.

Originators, underwriters, servicers, trustees, rating agencies, credit enhancers, payment agents, and custodians all play a critical role in this marketplace and must be evaluated accordingly.

Loan-level data on the underlying credit quality drives performance, yet this data is siloed and difficult to access for those without entry to the critical portals. Quantitative methods that overlay AI and machine learning techniques on carefully curated data sets can drive alpha.

Rating agencies play a central role in assigning credit ratings to each tranche, and while they do a fantastic job, their financial models tend to be backward-looking. As a result, individual loan analysis and forward-looking forecasting models are essential.

The secondary market is inefficient, and as credit characteristics evolve from origination and initial offering, price discovery can become highly dislocated.

Investment managers who are expert in this space can generate significant alpha through credit selection, relative value analysis, and active management.

This $4 trillion market is large, highly complex, and offers tremendous value as illustrated in the chart below.

Getting paid for complexity is one of the core attractions of structured credit.

Takeaway: +200bp pick-up for IG rated structured securities vs IG corporates (BBB- rating), is a significant yield premium in the public markets. The reward to generate alpha in a market where fewer investors travel is worth exploring.

M&A activity shows significant advancement in 2026, with record $1.6T in Q1 2026.

IPO potential is even bigger. Three $1 Trillion+ companies want to list in the coming year.

First is SpaceX, followed by Anthropic, and Open AI, with the later two raising a new round with post money valuation of ~$900 Billion; their potential up round IPO likely exceeds $1 Trillion.

Let’s see if the IPO window remains open.

No U.S. company has ever IPO’d at $1 Trillion, however, several companies are now valued in the $3T to $5T range.

Q: Is this a bubble or we have now entered escape velocity for Space and AI?

I think “not”, these are generational/exceptional companies operating in a domain that is transformational in its early stage.