"It's a great business to be in, Central Banking, where you print money and people believe it" - Adrian Orr

They're laughing at us.

LAUGHING.

"And people believe it". He's not wrong.

World central banks are incredibly bullish on gold:

45% of central banks said they plan to buy gold over the next 12 months, the highest reading on record, according to the World Gold Council survey of 74 central banks.

This percentage has more than doubled since 2020 and marks the 3rd consecutive annual increase.

Emerging market and developing economy central banks led the increase, with a record ~53% of this group planning to add gold, up from 48% last year.

Overall, 89% of central banks expect global gold reserves to increase over the next 12 months, the 2nd-highest reading on record.

Central banks are buying the gold dip.

On days like today, it is important to keep this chart in mind.

We are living through a global monetary reordering.

Do not let volatility discourage you. We cannot control it.

What we can control is how thoughtfully we respond when opportunities present themselves.

https://t.co/CDf4pgGYDj

Money supply is skyrocketing:

Global money supply is now up to a record $121.9 trillion.

Over the last 2 years, money supply has soared +$17.1 trillion, or +16%.

This also marks a +$27 trillion increase, or +28%, since the 2022 low.

This means that global money supply is surging +7% to +8% a year.

Meanwhile, US M2 money supply jumped +$1 trillion YoY, or +4.6%, to a record $22.7 trillion.

Money supply growth is accelerating.

BREAKING: Month-over-month US PPI Inflation officially rises +1.5% in April, marking the biggest monthly jump in inflation since March 2022.

All of the data is very clear: consumers are about to face another wave serious pressure on spending power.

BREAKING: April PPI Inflation surges to 6.0%, well above expectations of 4.9% and the highest level since January 2023.

Core PPI Inflation rose to 5.2%, above expectations of 4.3%.

Both CPI and PPI Inflation are now officially at 3+ year highs.

Odds of rate HIKES are rising.

In 1967, Indira Gandhi appealed to Indians: “Don’t buy Gold.”

The reason was that India’s foreign exchange position was under stress, imports were becoming difficult, and the currency system needed people to show “national discipline.”

But what followed?

One of the biggest Gold bull markets in history.

From the late 1960s to 1980, Gold exploded higher globally, and in rupee terms the move was even more brutal.

This is the real lesson:

When governments tell citizens not to buy Gold, they are usually not worried about your jewellery.

They are worried about pressure on the currency, pressure on reserves, and pressure on the financial system.

Gold doesn’t become important when everything is normal.

Gold becomes important when the system starts asking you not to buy it.

BREAKING: Global physical gold-backed ETFs posted +$6.6 billion in inflows in April.

European funds led, at +$3.7 billion, followed by Asia, at +$1.8 billion, and North America, at +$1.0 billion.

This marks a sharp recovery from -$12.0 billion in outflows in March, the largest monthly withdrawal on record.

Year-to-date, global gold ETFs have attracted +$19.0 billion in inflows.

This lifted total assets under management across global gold ETFs by +1% MoM, to $615 billion.

At the same time, gold holdings jumped +45 tonnes, to 4,137 tonnes, the 3rd-highest on record.

Global gold demand is rapidly recovering.

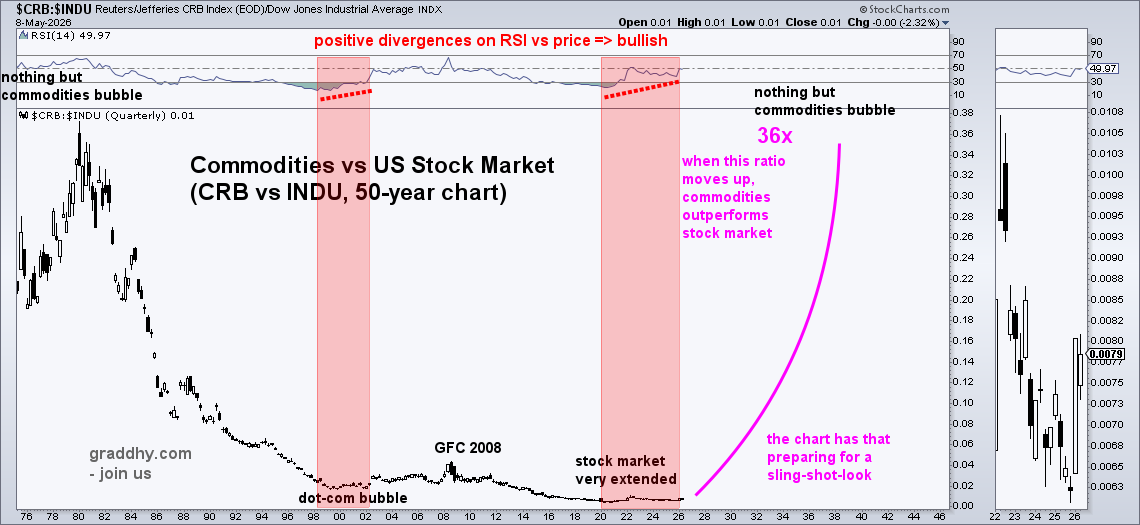

This chart shows hard assets vs paper assets.

And it has now broken out on lower time frames.

Commodities are extremely undervalued vs the stock market. A historical opportunity is underway, in the form of a global paradigm shift away from overvalued paper assets towards undervalued hard assets. It will be the largest global financial paradigm shift the world has ever seen. And therefore, one of the biggest opportunities there has ever been.

The pushed narrative is that big inflation is basicly done.

No, it surely is not. Not by a mile. Unfortunately.

The commodities bull market started 6 years ago, which we caught the start of. The biggest opportunity in our lifetime, and threat.

So, do not miss it, whatever you do. #joinus https://t.co/dZoc2yuE1z

Commodity inflation is surging:

The Bloomberg Commodity Index is up to 141 points, the highest since February 2013.

This index tracks 25 exchange-traded futures contracts across energy, metals, and agriculture.

Energy accounts for the largest weighting, at 39%, followed by agriculture, at 27%, precious metals, at 16%, and industrial metals, at 13%.

This index is now up +28% year-to-date and it has officially surpassed the 2022 energy crisis peak of 140 points.

As a result, commodity prices are now on track for their first annual increase in 4 years.

Inflation is back.

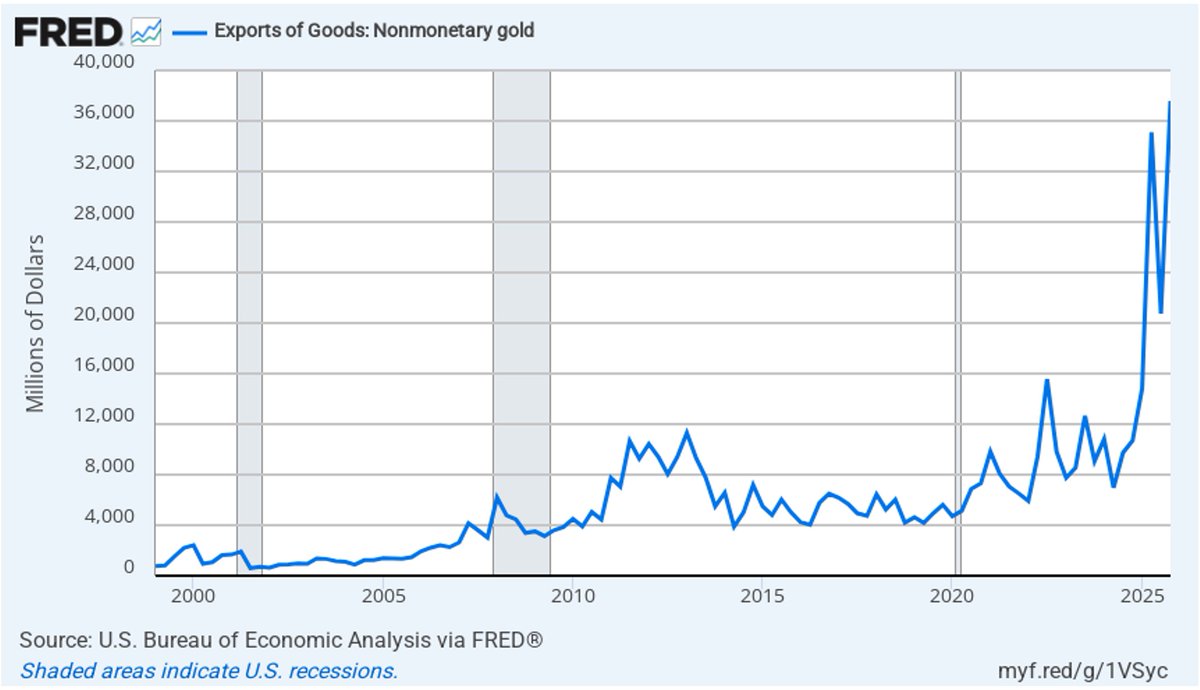

For the 5th month in the last 6, "Nonmonetary Gold" was again the single biggest export of the US in March.

US gold exports were 1.7x > oil; 2x > than Rx preparations, 2.5x > aircraft engines.

Biggest destination for US gold exports: China or Switzerland (& then on to China).

Two months ago no one thought there was any possible way metals could ever go down. Just the mention of a potential correction brought out hordes of trolls to tell me I was an idiot, that this time was different.

Now we have reached the opposite extreme. No one thinks there is any possible way metals can ever go back up.

Just like everyone was wrong 2 months ago they are wrong now as well.

The fundamentals haven't changed. This is just a very severe profit taking event that has convinced people that the metals are broken.

They are not broken. This is just another in a very long line of corrective counter trend moves in a long term secular bull market.

Central banks are sitting on massive stockpiles of gold after years of record purchases:

Global central banks now hold ~38,666 tons of gold, reflecting ~17% of all gold ever mined.

Still, the largest portion of gold remains in private hands, with ~97,645 tons held as jewelry, or ~43% of the total.

Investment-related holdings, including bars, coins, and ETFs are ~50,978 tons, making up 23% of the total.

The remaining ~32,602 tons, or 14%, fall into other categories, such as industrial use and private reserves.

Central banks are now major players in the global gold market.

China is experiencing historic demand for silver:

Chinese silver imports rose +78% MoM, to a record ~836 tonnes in March.

This is +173% above the 10-year seasonal average for March.

Year-to-date, silver imports are up to ~1,626 tonnes, the highest on record.

Surging demand was driven by retail investors purchasing small silver bars as a lower-cost alternative to gold, and solar manufacturers front-loading production ahead of the removal of export tax rebates on April 1st.

The global solar industry consumes ~20% of total annual silver supply, with the majority of activity concentrated in China.

China's demand for silver is exploding.

I almost bought apartment buildings instead of precious metals 4 years ago, but I went with metal.

Instead of dealing with cranky tenants, I’ve been doing yoga on the beach and playing with my kids.

Oh, and I 2.5x’d my portfolio while apartments lost 25% of their value. More of this trend to come.

This isn’t hard people. Gold’s crushed the S&P 500 the past quarter century and is gaining speed

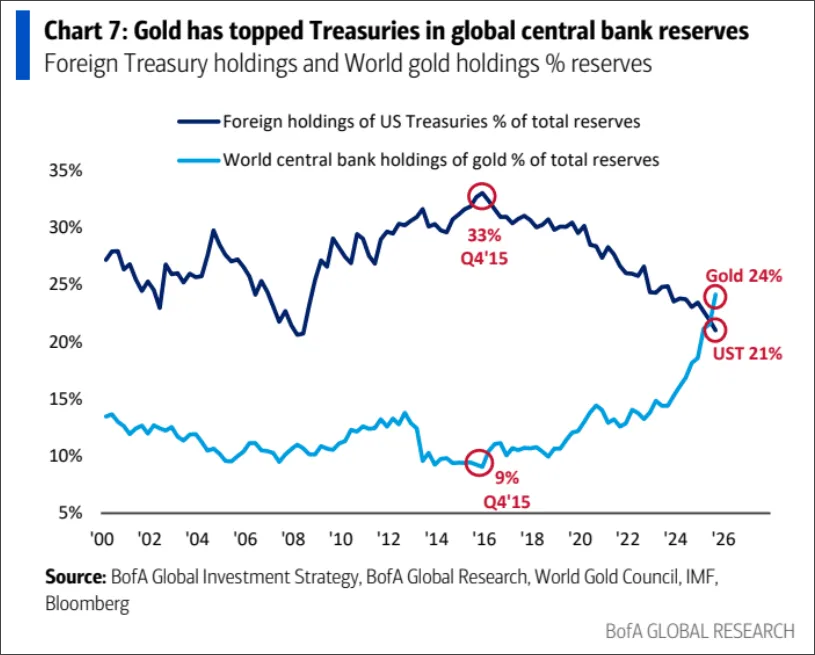

🔥Gold is making history:

Gold now makes up 24% of global central bank reserves, surpassing US Treasuries at 21% for the first time since the mid 1990s.

This is a complete reversal from Q4 2015, when Treasuries made up 33% of reserves and gold just 9%.

Gold as a % of central bank reserves has NEARLY tripled over the last decade, driven by both aggressive central bank purchases and surging gold prices.

At the same time, central banks have steadily reduced their exposure to US government debt, driven by China.

The shift signals a historic move away from Dollar-denominated assets as the global reserve system evolves.

Gold is no longer an alternative reserve asset; it is now a major reserve asset.

US gold reserves have never been this small relative to government debt:

Gold reserves now reflect just 3% of US federal debt, one of the lowest readings on record.

This comes despite the US holding 8,133.5 metric tons of gold, the largest stockpile in the world, and prices surging to record highs.

By comparison, the ratio was ~18% in 1980, or 6x higher.

At the same level of reserves, gold prices would have to rise +400%, to $26,000/oz, to match the 1980s peak.

Meanwhile, in the 1940s, gold reserves backed over 50% of federal debt.

To match the 1940s ratio, gold would need to surge +1,340% to ~$75,000/oz.

Gold reserves are highlighting just how astronomical US debt has become.

#gold is insurance

#silver is insurance + speculation

#platinum is speculation on steriods

If silver is at least a x6 from here, which I do think, imagine where platinum would be if this ratio goes back to ATHs, which is very likely. Same move happened 45 years ago; red arrows.

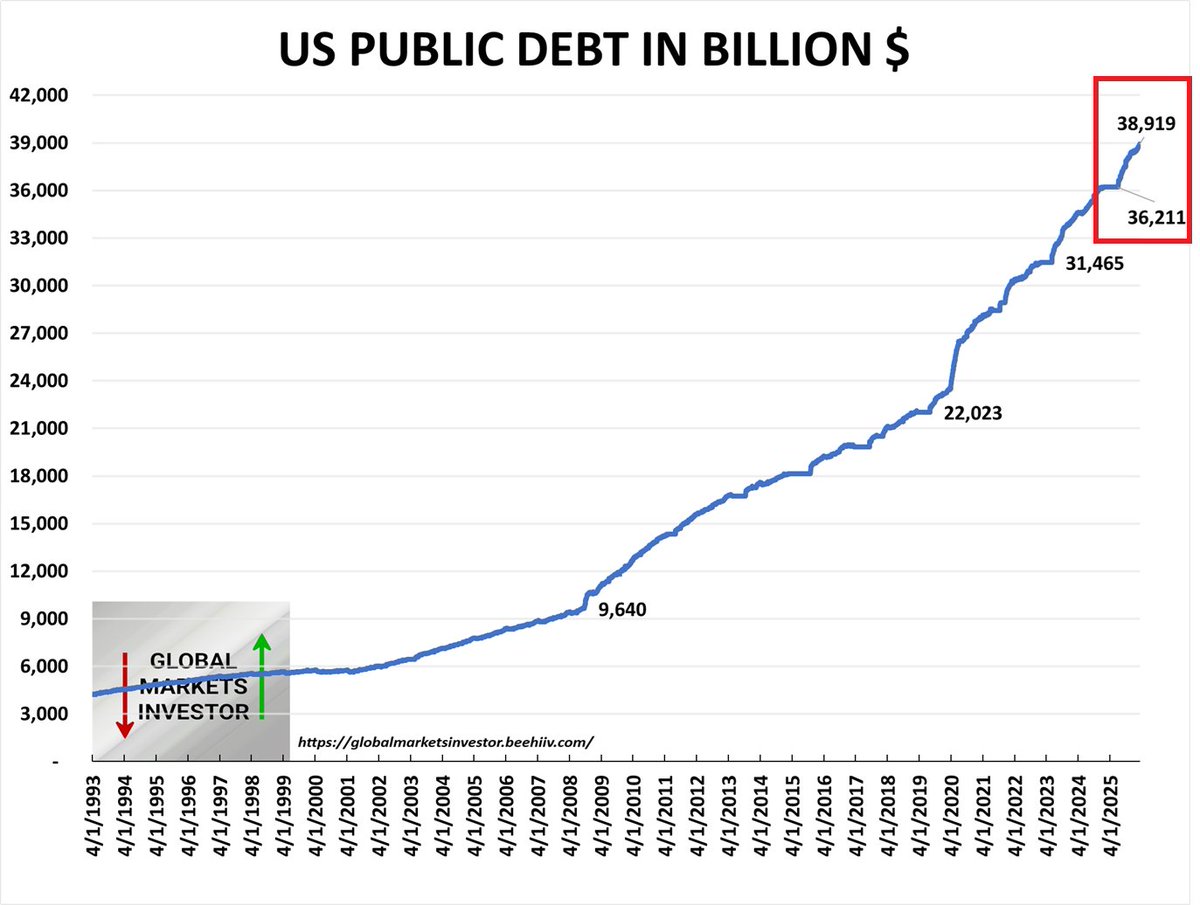

🚨The surge in US public debt is MIND-BOGGLING:

US federal debt hit a record $38.9 TRILLION at the beginning of March.

Since the start of 2026, the debt is up $400 billion.

Since 2020, the debt pile has surged nearly $7 trillion and is on track to hit $40 trillion as early as this year.

This is beyond comprehension.

The financial system is broken, and taxpayers are left holding the bill.

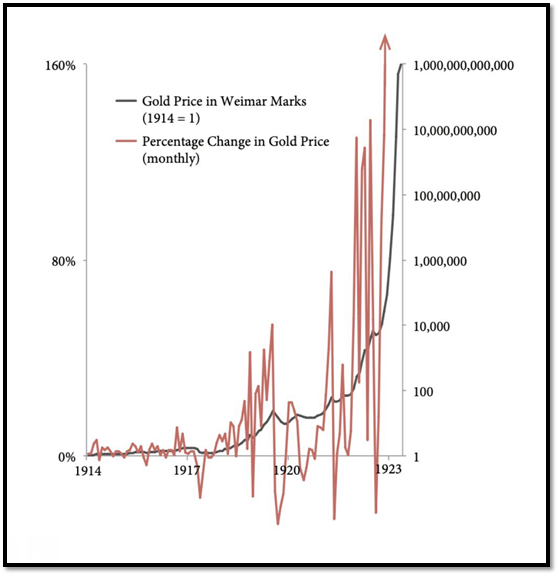

This is what real hyperinflation does to a stock market.

Early in the move, stock market moves outweigh inflation. Later in the move, stock market gains is no where near the rate of inflation. Many will be fooled by Western stock markets going up hugely when the time comes.

It is imperative to understand how things actually work.

Then also add resulting depression, plus CBDCs, bail ins, coming capital controls, bank closures, severe ownership issues, how long physical will be available etc etc, and it quickly gets complicated. It is vital to piece the puzzle together in order to understand what is coming, and in order to be prepared in detail in every way needed. https://t.co/dZoc2yuE1z