My latest video for @AlphaBetaSoup_ explores the current state of the economy, and how bad data doesn't seem to matter because the top 20% of earners are doing so well.

Give it a watch, subscribe to my channel, etc. YT link in the retweet below. Appreciate the engagement!

Have a great weekend

Something that got missed in the noise last week: Coinbase got approved to offer true global crypto perps in the US. This took many years of work, and we're the first to offer this global liquidity to US users.

Backstory: For many years crypto trading has been moving offshore because the US didn't have clear rules, and perpetual futures were a superior product that traders wanted but it wasn't allowed in the US.

If we're being honest, probably ~half of all perpetual futures volume was Americans using offshore products via VPN with loose KYC controls (an open secret in the industry). Penalties for this were rarely, if ever, enforced, which as you can imagine, was frustrating for us as an American company following the rules. Others set up offshore entities and found ways around it.

After dozens of personal visits to DC, and many more from our policy team, I'm really proud we finally got approval to give US users access to true, global perpetual futures. This is important because we'll now see pooled global liquidity in perpetual futures, with the US and international markets being connected instead of fragmented.

Coinbase is strongest in the US, and the US is the largest market for trading, so there is now a chance to build a global network effect around liquidity. And US traders can now use these products in a compliant way with a US company, which hopefully provides greater customer protection.

Major credit to Chair Selig and Atkins on recognizing the importance of this for US capital markets. And we will keep working to update the system in a compliant way, and to be the best place you can trade.

Look guys, it's actually really straightforward, a bunch of people staked their ETH on the Ethereum blockchain to earn yield, except they didn't want their capital to be locked up, so they actually staked with a liquid staking protocol called Lido who provided them a liquid staking receipt token called stETH, except they decided to juice their yield further by depositing their stETH receipt tokens into a restaking protocol called Eigenlayer, except they didn't want to lock up their capital, so they actually restaked with a liquid restaking protocol called KelpDAO who provided them with a liquid restaking receipt token called rsETH, except they decided to juice their yield further by depositing their rsETH tokens into a lending protocol called Aave so that they could open a leveraged looping position that borrows ETH against the rsETH collateral and restakes the ETH into rsETH which is then deposited as collateral, except it turns out rsETH used a cross-chain bridge called LayerZero that was hacked by north koreans causing rsETH to become undercollateralized and now these looping positions are stuck and unprofitable, and everyone is pointing fingers at each other, and also DeFi is a very serious industry

“The ability to exercise collateral value on your assets makes DeFi instantly more productive.”

@calilyliu, President of the @SolanaFndn explains why programmable collateral is DeFi’s real edge.

When we eventually get into a bear market (not yet btw) I expect to see the first chain mergers. Consolidation will allow smaller chains to survive and come out stronger instead of grinding to oblivion.

First Ken Griffin screwed over Constitution DAO

Now he's coming for DeFi, asking the SEC to treat software developers of decentralized protocols like centralized intermediaries

Bet Citadel has been lobbying behind closed doors on this for years

Okay thats all pretty bad, but the actual nerve for one of their arguments to be that there is no way for DeFi protocols to provide "fair access" of all things lmao

Makes sense the king of shady tradfi market makers doesn't like open source, peer-to-peer tech that can lower the barrier to liquidity creation

https://t.co/nnlQAKx7bF

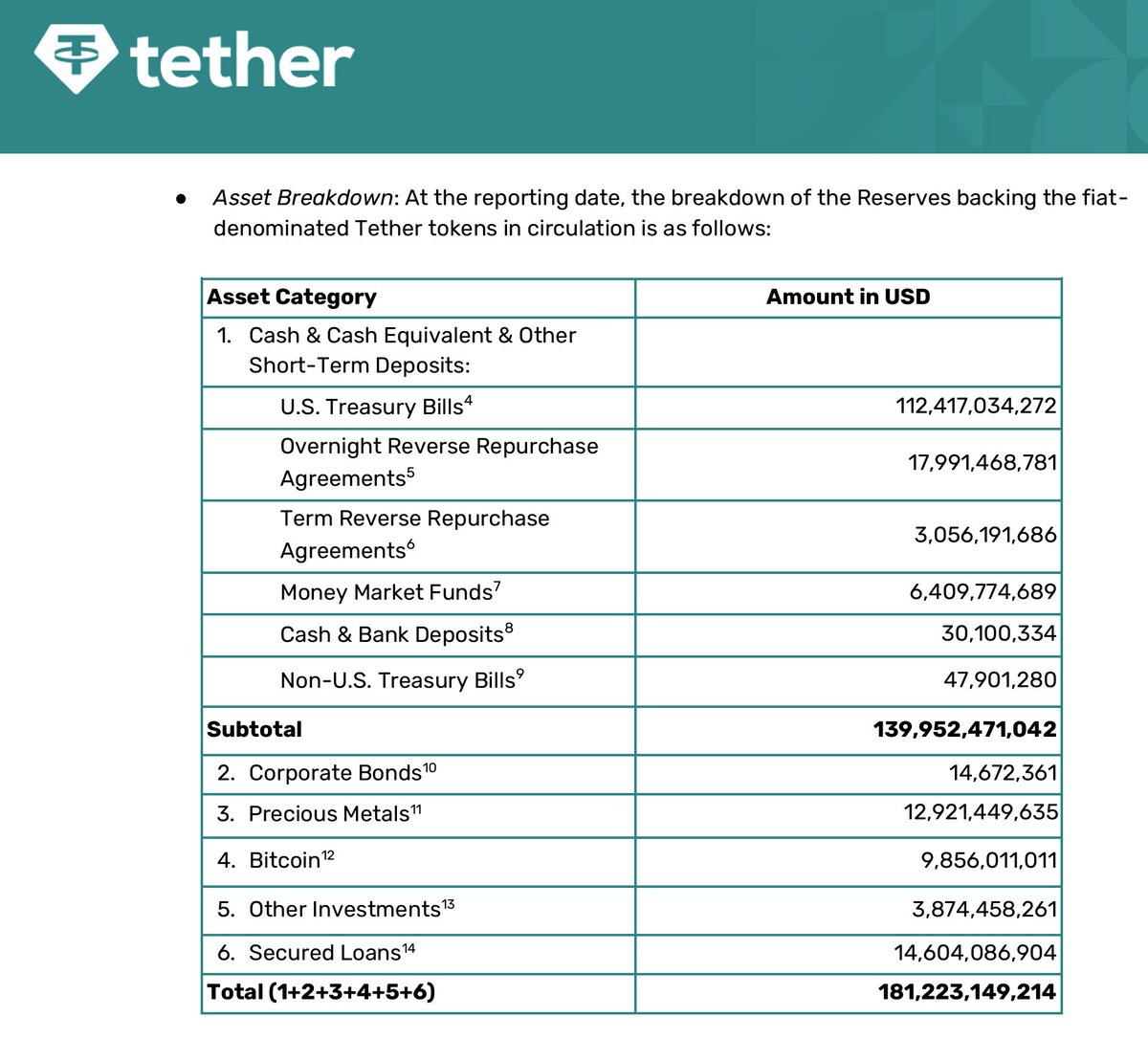

The Tether folks are in the early innings of running a massive interest rate trade. How I read this audit is they think the Fed will cut rates which crushes their interest income. In response, they are buying gold and $BTC that should in theory moon as the price of money falls.

A roughly 30% decline in the gold + $BTC position would wipe out their equity, and then USDT would be in theory insolvent. I'm sure some large holders and exchanges will demand a real-time view of their B/S so they can assess the solvency risk of Tether. Get out your popcorn, I expect the MSM to run wild with this, especially all the editors with TDS who want to shit on Lutnick and Cantor for backing this stablecoin.

Why Tether’s Gold & Bitcoin Bets May Be the Only Real Hedge Against the GENIUS Act’s “Reverse-Yield” Risk

This week, S&P downgraded its stability assessment of Tether’s USDT from “constrained” to “weak”—the lowest score on S&P’s five-point stablecoin stability scale. S&P cited Tether’s increased reliance on gold and Bitcoin reserves.

Tether is now the largest non-state holder of physical gold in the world, and approximately 13% of USDT reserves are backed by gold and Bitcoin. Under the GENIUS Act, Tether’s U.S.-issued stablecoin, USA₮, is mandated to hold 1:1 short-term U.S. Treasury bills.

For its offshore stablecoin, USDT, Tether is relying more heavily on gold and Bitcoin as reserve assets. This move may well be a strategic hedge against a mass U.S. stablecoin liquidation event.

In such an event, Tether would not be forced to shore up reserves by liquidating short-term T-bills at a loss. It would have the option to meet redemptions by liquidating its gold and Bitcoin reserves instead. The more Tether’s reserves rely on gold and BTC—instead of exclusively on short-term T-bills—the less its overall balance sheet is exposed to a reverse-yield liquidation crisis.

As noted in Shanaka’s article, the GENIUS Act forces U.S.-regulated stablecoins into one of the safest assets on earth: short-term U.S. Treasury bills. While that’s great for reducing Terra/Luna-style risks and for lowering U.S. borrowing costs, it does come with a structural problem: when stablecoins grow, they gently push yields down; when they contract, they can violently push yields up.

This is the convexity trap. A few billion dollars entering stablecoins barely moves yields—but a few billion dollars leaving stablecoins can spike yields two to three times harder.

If Tether held exclusively short-term T-bills, then in a redemption crisis, it would be forced to dump T-bills into a stressed market—further accelerating a T-bill yield spike—or take mark-to-market losses on its remaining T-bill holdings.

In that scenario, Tether gets hit twice, right when confidence in stablecoins is already fragile. That’s the “reverse-yield” problem.

A stablecoin built entirely on U.S. Treasuries therefore becomes brittle at the exact moment the system needs stability most. Here’s where Tether’s controversial reserve mix makes more sense than critics admit.

Gold & Bitcoin Break the Convexity Loop

By holding a meaningful slice of reserves in gold and Bitcoin, Tether gives itself something almost no other issuer—including Circle—has:

🚫 Assets it can liquidate during redemptions without dumping T-bills.

🚫 Assets that aren’t mechanically tied to short-term rates.

🚫 Assets—like gold and Bitcoin—that may rise or stay stable in the exact macro scenarios that crush Treasuries.

As a consequence:

➕Gold reduces Tether’s exposure to interest-rate convexity.

➕Bitcoin hedges the tail-risk of a U.S. sovereign credibility event.

Together, they give Tether something a 100% T-bill model cannot: the ability to meet redemptions without feeding the very crisis that threatens its peg.

Do these assets introduce volatility? Absolutely.

But they also break the one-way valve the GENIUS Act accidentally created. This is why Tether’s diversification looks reckless to regulators—but smart to anyone who understands convexity.

In a world where every GENIUS-compliant stablecoin becomes a leveraged bet on the short-end of the U.S. curve, Tether is quietly building the only balance sheet not fully dependent on the thing everyone else assumes will never break.

My favorite thing about this chart is that the median homebuyer age rose from 39 in 2005 to 59 in 2025

20 years over 20 years

It’s literally the same people buying the homes two decades later