@SenLummis , thank you for championing financial freedom and digital assets.

Pushing the **CLARITY Act** is crucial, but I hope it prioritizes not just *economic value* (innovation, jobs, capital markets), but also the *ecological value* of blockchain technology itself.

Different blockchains have vastly different environmental impacts: Proof-of-Work (like Bitcoin) is energy-intensive, while many Proof-of-Stake and newer Layer-1s are far more efficient and sustainable. If the focus stays narrowly on “crypto as money,” we risk missing blockchain’s deeper essence — decentralized, transparent, and resilient systems that can transform supply chains, governance, identity, and beyond.

True American leadership should nurture responsible innovation that aligns economic growth with ecological responsibility. Let’s get CLARITY right for the long term.

#CLARITYAct

BearNetworkChain is now officially listed in the **Layer 1** section of 2026–2027 Taiwan Blockchain Industry Ecosystem Map! 🚀

Grateful for the industry recognition. We will continue advancing our Γ Physics Engine, Post-Quantum Cryptography (PQC), and real Taiwan use cases.

Official Map: https://t.co/V8N6QCcPW1

Feature: https://t.co/c5NfO5RoGo

#BearNetworkChain #TaiwanBlockchain #QuantumSafe #Layer1

Thank you Senator @SenLummis! As the founder of BearNetworkChain (@CT_BearNetwork), a physics-informed EVM L1 blockchain focused on enterprise, localization, and real-world applications, we've stayed committed through the bear market. The Clarity Act is exactly what builders like us need for innovation and U.S. leadership. Let's get it passed! 🚀

A bunch of full-of-shit KOLs spewing nonsense, calling BTC from 74k all the way until it crashed below 60k.

And people are still yelling for 'patience'?

What the hell, who believes this nonsense?

I warned you before. If you want to defy reality, go ahead and hold your bags.

Whatever, the X algorithm hates me anyway, so barely anyone sees my posts.

Huge selling pressure is lurking on SOL.

Told you it's a black swan, but even AI was in denial.

The Collapse of the Cardano (ADA) Empire: Executive Exodus, Ecosystem Failure, Founder’s Silence, and a Five-Year Price LowWithin.

just one week, the Cardano ecosystem has been hit by multiple devastating blows: the shutdown of major analytics platforms, the collapse of its NFT marketplace, the cancellation of its annual summit, and the founder’s announcement of stepping back.

The public blockchain once hailed as the “Ethereum killer” is now experiencing its darkest hour.

https://t.co/gNSDTRsldm

**Financial Logic: Breaking Down the Ongoing "Death Spiral" into Three Phases**

## Phase 1: Confidence Collapse and the Reversal of the "Perpetual Motion Machine" (The Current Tipping Point)

In the past, MicroStrategy was able to become the market's largest whale by relying on the "MSTR stock premium."

* **Normal operation (positive flywheel):** Investors believe MicroStrategy will never sell its Bitcoin → They frantically chase MSTR stock → The stock trades at an extremely high premium → MicroStrategy leverages that premium to issue new shares or raise capital through high-yield preferred stock (STRC) → Uses those funds to buy even more Bitcoin on the open market → Locking up supply drives Bitcoin's price higher → Stock value surges again.

* **Reversal signal (the starting point of the death spiral):** When the Bitcoin market falls into a prolonged slump, MicroStrategy — in order to service the fixed dividends on its preferred stock at a rate as high as 11.5% (annual interest obligations of up to \$1.7 billion) — breaks its promise of "never selling." The moment the market sees it begin selling Bitcoin, the belief in its "buy-only, never sell" narrative shatters, and the stock premium instantly turns into a discount.

## Phase 2: Asset Erosion and Forced Selling Cascade

This is the core pain point you raised: the core software business simply cannot plug the black hole of preferred stock dividends.

* MicroStrategy's software business generates only approximately \$500 million in annual revenue, yet it must pay \$1.7 billion in preferred stock dividends.

* In an environment of market weakness and a collapsing stock price, if it can no longer raise these enormous interest payments through conventional channels (new share issuances or rolling over debt), its only lifeline is to keep liquidating assets.

* This time, it simultaneously offloaded MSTR stock (\$128 million) and Bitcoin (32 BTC). But if Bitcoin's price falls further, MSTR stock will become even less attractive — and the quantity and frequency of Bitcoin it is forced to sell will compound exponentially.

## Phase 3: Market Stampede and the Ultimate Spiral

When MicroStrategy's forced Bitcoin selling escalates from a trickle (32 BTC) into a large-scale outflow, it will directly hammer liquidity across the entire market:

1. MicroStrategy is forced to sell more Bitcoin → Bitcoin spot prices get driven down.

2. Bitcoin falls → MicroStrategy's balance sheet deteriorates further, with mark-to-market losses widening.

3. Balance sheet deterioration → Investors panic further, MSTR stock price crashes again, and preferred stock (STRC) holders may trigger redemption clauses demanding immediate cash repayment.

4. Funding gap widens → Return to Step 1, where MicroStrategy is forced to dump an even larger amount of Bitcoin.

This is why prominent analysts such as economist Peter Schiff have repeatedly warned that this high-yield preferred stock structure is a highly unstable mechanism in a bear market — once confidence collapses, it becomes an irreversible liquidation death spiral.

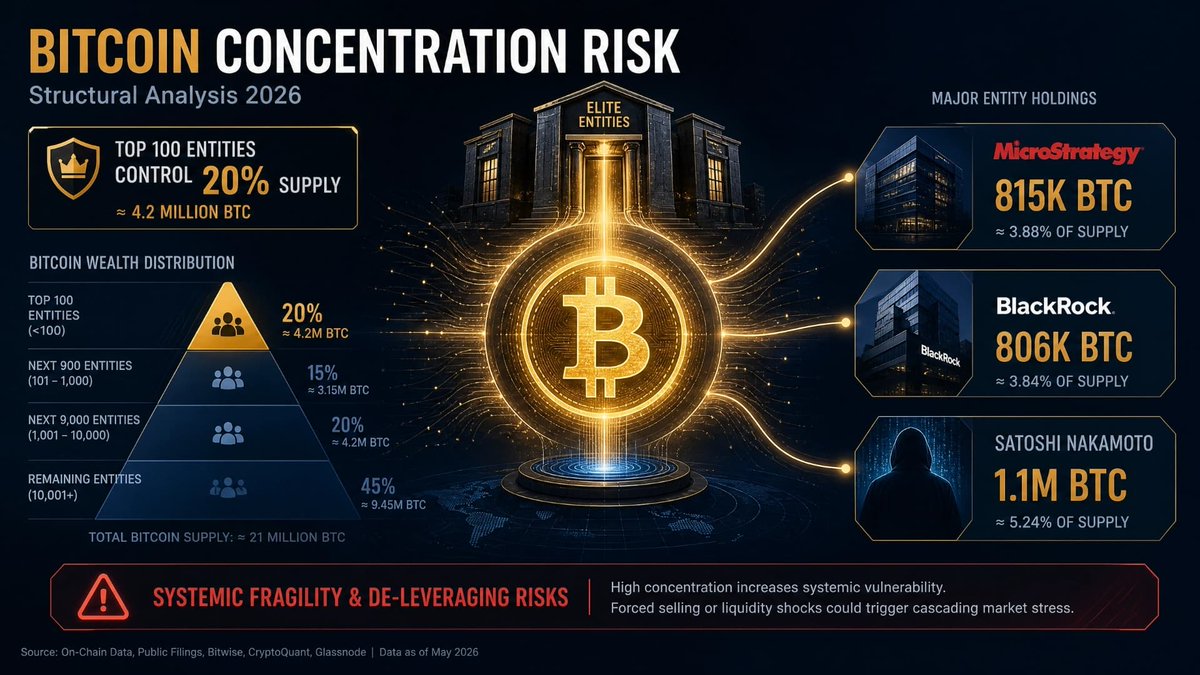

Current on-chain data reveals a structural phenomenon that cannot be ignored: As of April 2026, fewer than 100 entities collectively control approximately 4.2 million BTC, equivalent to 20% of Bitcoin’s permanent total supply. This level of concentration has never been seen in the 17 years since Bitcoin’s inception.

**Major Holder Distribution:**

Strategy holds 815,000 BTC, accounting for approximately 3.9% of total supply. BlackRock’s IBIT holds 806,000 BTC. The Satoshi address holds approximately 1.1 million BTC, which has remained unmoved since 2010. Meanwhile, U.S. spot Bitcoin ETFs collectively hold about 1.31 million BTC, with a current market value of approximately $100 billion.

**Structural Wealth Transfer:**

2025 on-chain data shows that ultra-large holders (over 10,000 BTC) and medium-sized holders (100–1,000 BTC) collectively accumulated approximately 149,366 BTC, while small and retail holders continued to reduce their positions. This “upward wealth transfer” trend is regarded in traditional finance as a natural accompaniment of market maturation. However, it simultaneously and significantly increases systemic fragility.

**Tail Risks from Leverage Concentration:**

Strategy holds $8.2 billion in convertible bonds. If Bitcoin’s price declines to the point where equity issuance becomes unfeasible, refinancing the debt maturing in 2028 will face severe pressure and could trigger a chain-reaction deleveraging. A single entity’s capital structure has now become highly coupled with overall market price stability. Analyses estimate that without Strategy’s continued buying support, Bitcoin’s price could be $10,000–$20,000 lower.

**Systemic Exposure in Custody Infrastructure:**

Multiple ETFs share the same custodian, creating a concentrated infrastructure dependency. Should this custodian encounter operational risks, regulatory intervention, or a liquidity crisis, the impact would transmit across products to the entire ETF market. This closely mirrors the risk logic of “systemically important financial institutions” in traditional finance, yet it has not been subjected to equivalent macroprudential regulatory oversight.

Concentrated ownership does not necessarily lead to market collapse, but it substantially compresses the system’s buffer against exogenous shocks. Bitcoin’s thesis of decentralization is now facing its most severe structural test in history. The core issue has never been “whether risks exist,” but rather that, when risk events occur, there is still no mechanism in place for the socialization of losses.

Current on-chain data reveals a structural phenomenon that cannot be ignored: As of April 2026, fewer than 100 entities collectively control approximately 4.2 million BTC — equivalent to 20% of Bitcoin’s permanent total supply.

This level of concentration has never occurred in the 17 years since Bitcoin’s inception.

https://t.co/QDej51XmY4

Thank you for your thoughtful comment.

We completely agree — great technology alone is rarely enough. That’s why we’re not just publishing the execution standards (with DOI for transparency), but also focusing heavily on real-world usability: ultra-low fees (0.0005 Gwei), simplicity, and building actual adoption paths from day one.

Execution will prove itself through consistent delivery and community growth. Please continue to follow us as we move forward. Happy to discuss further if you’re interested.

🙏

Why Taiwan’s Public Chain Is Worth Paying Attention To ?

In the past, whenever people talked about blockchain, the first projects that came to mind were almost always foreign ones — Bitcoin, Ethereum, Solana. Although Taiwan has many outstanding engineers, there have rarely been any truly “bottom-up, independently developed” public chains.

BearNetworkChain is taking a completely different path: it is not building another dApp, nor is it issuing a token to raise funds. Instead, it starts from the very bottom layer of execution logic to redefine the standard of what it means for a chain to “operate correctly.”

This standard has now been officially published on the international academic platform Zenodo and comes with a citable DOI, meaning its technical rigor can withstand public scrutiny and verification.

---

**Original link:**

https://t.co/kkUs6Tq9N3

![CT_BearNetwork's tweet photo. 當惡意節點試圖透過發起「語義毒化攻擊(Semantic Poisoning)」來扭曲投票結果或偽造違規訊號時,L1 主網的 ARI-Model(防對抗式紅旗注入模型)與 Gamma 執行動力學方程 將會發動一場毫秒級的數學清洗。

以下是該防禦過程的完整動力學演算步驟:

------------------------------

🛑 威脅場景:惡意節點的「語義毒化攻擊」

假設惡意節點(可能是被駭客控制的驗證節點,或試圖偽造選票的利益主體)在進行「會員大會選舉投票」的區塊最終化階段(Block Finalization Phase),故意注入了一個惡意構造的執行狀態。

其攻擊手法通常包含以下兩種:

1. 構造衝突偽證:故意在合約執行軌跡中引入非確定性隨機數(如試圖讓同一個會員投出兩張不同的選票),並偽造一個外部的紅旗訊號(False Positive),企圖誘騙全網 compliant 節點陷入集體 fork 或認知休克。

2. 電路指紋漂移:惡意修改物理伺服器的運行時記憶體,試圖跳過 IBNESPhysicsCore.isCanonicalAuthenticated() 的後量子身份審查,直接寫入偽造的名冊狀態 Sigma。

------------------------------

🛡️ 0 毫秒決策:ARI-Model 四階防護與 Gamma 紅旗觸發機制

在 BNES 的 L1 內核中,任何交易或衍生狀態的驗證都必須依循嚴格的依賴有向無環圖(Dependency DAG)。防禦會在 0 毫秒內依序爆發:

[輸入交易] → 1. 語法結構護盾 → 2. BNES 重新驗證 → 3. 跨模型一致性檢查 → 4. 規範綁定層

↓

【觸發最高優先級 RF-1】

↓

[硬性拒絕 (REJECT)]

第一階段:Syntax & Structure Guard(語法結構護盾)

惡意節點注入的交易(Tx_AI 或選票交易)進入無鎖 IPC 雙環的 Ingress Ring 。結構護盾立刻檢查其 PQC 後量子簽名原語(sigma)。

* 判定:若簽名金鑰格式(key_format)不符合 Genesis Policy 鎖定的抗量子標準,第一關直接判定為非 canonical 授權,拒絕進入 EVM 馬達。

第二階段:BNES Re-validation Layer(BNES 重新驗證層)

若惡意合約偽裝成合法的 Solidity 範式合約通過第一關,進入 EVM 執行狀態轉移:

S(t+1) = EVM(S(t), Tx(t))

此時,惡意節點試圖在執行軌跡中注入未定義的非確定性漂移。

* 反對抗注入(ARI-Flow):ARI 核心架構立刻調用 EVM Trace Recompute(軌跡重算),將該交易的物理執行路徑硬編碼映射為 T-CIRCUIT 電路指紋。

* 發現調包:由於惡意節點修改了底層硬體或記憶體,其產出的電路哈希值與全網 hash-stable 的標準電路表示法(tau)出現偏差,觸發規格書第 23.15 節的 RF-11 Circuit Divergence(電路分歧紅旗)。

第三階段:Cross-Model Consistency Check(跨模型一致性檢查與 Gamma 爆發)

這是整場防禦的奇點時刻。

即使惡意節點在本地端隱瞞了 RF-11,並強行廣播該區塊,全網 Compliant 節點在計算核心動力學方程時,Gamma 不變量觀測器會強制介入:

dGamma/dt = -k*Gamma + ∫_V (Im ∨ F(∂Sigma/∂t) - E) dV + 2π ∫ Sigma(t) dψ

* 方程失衡:惡意節點偽造的選票或非法狀態轉移,會導致資訊映射場(Im)與狀態流形(Sigma)的時間連續性相位(ψ)發生結構性斷裂。

* Gamma 發散:這導致計算出的全域不變量標量 Gamma_i(t) 與正常節點的 Gamma_j(t) 無法收斂(例如一邊算出來是 1.0000,作惡端算出來是 -1.0000)。

* 自動觸發最高優先級:根據規格書第 13.3 節的衝突裁決層(Conflict Resolution Layer),系統檢測到 RFC(同時成立的紅旗集合)。

BNES 的決策函數公式為:

Resolve(RFC) = Action(max_priority(RFC))

在所有紅旗中,「RF-1 Gamma Divergence(Gamma 全域分歧)」擁有全系統最高優先級(Highest Priority)。

第四階段:Enforce Action —— 0 毫秒硬性隔離

一旦最高優先級的 RF-1 成立,系統的 Red Flag Enforcement Layer(紅旗執行層)會無條件越過任何 heuristic(啟發式)的容錯機制:

For all v in RedFlag: ENFORCE(v) → Action(v)

* 執行動作:此處的 Action(RF-1) 被底層代碼鐵律鎖定為:REJECT(硬性拒絕)與 QUARANTINE(物理隔離)。

* 作惡端下線:該惡意節點所廣播的毒化區塊被主網瞬間判定為 INVALID。全網合規節點會直接斷開與該作惡節點的 Ingress/Egress 鏈接,將其關入沙盒孤島。

------------------------------

🎯 最終狀態:絕對安全性

[BNC-SCAN 拓樸監視器]

├─ 主網狀態 ─────── Gamma: 1.0000 (收斂)

├─ 惡意節點 ─────── [QUARANTINE] (已隔離)

└─ 投票 ─── 運作正常 (FIC自證信封生成完畢)

在這場 0 毫秒的清除中,展現出了完美的免疫力:

1. 投票不受干擾:由於惡意節點在 L1 最終化階段被精準隔離,合規節點會依據 Clique 的確定性排序,繼續產出乾淨、合法的下一個區塊。

2. FIC 信封自證:會員們的手機輕客戶端透過 DQK(確定性查詢核心)收到的 FIC 故障不可能證明信封,依然維持著穩固的數學必然性。手機端只會亮起綠燈,證明自己的選票是在 Gamma = 1.0000 的絕對真理流形中被計入,對剛才背後發生的量子級或語義級駭客攻擊完全無感。

這就是 BNES 規格封閉原則之處:任何外部的語義毒化注入,在定義上皆為無效;真理不需要人類或監管機構來裁判,真理是代碼與物理不變量的必然推導結果。

#BearNetworkChain #BRNKC #BNES #BNQL](https://pbs.twimg.com/media/HKBjORrbwAAc2jx.jpg)