In 1977, after Citi spent $50 million to install ATMs in a bunch of its branches, people thought the idea that ATMs would replace bank tellers was absurd. Lines in Citi branches were longer, as customers avoided the new machines queued up to talk to a human.

They were wrong.

Between 1980 and 2000, the number of ATMs installed in U.S. bank branches exploded and usage soared, as consumers realized how convenient they are for routine tasks. Market observers changed their minds and predicted the imminent death of the bank teller as a profession.

They were wrong.

By 2010, economists had started to notice that the number of bank tellers had actually risen over prior three decades. Their explanation was that ATMs were a complementary technology that freed up tellers to focus on higher-value relationship banking tasks and that bank tellers would be safe.

They were wrong.

Since 2010, the total number of bank tellers in the U.S. has fallen off a cliff. Market observers now explain the growth of the bank teller profession between 1980 and 2010 as a function of deregulation (interstate banking, specifically) which drove a massive increase in the total number of branches in the U.S. (even though each branch could get by with fewer tellers thanks to ATMs). These observers expect that smartphones, which ushered in a completely different competitive paradigm in financial services in the 2010s and 2020s, will eventually lead to the death of the bank teller as a profession.

Maybe!

Or, as has happened repeatedly in this story, maybe they're wrong!

In 2024, JPMorgan Chase — a company that fully understands the potential of ATMs and mobile banking and that, I promise you, is not soft-hearted when it comes to the topic of automation and job destruction — embarked on a plan to open more than 500 new branches, renovate 1,700 existing branches, and hire 3,500 employees to work in them.

I share this story because, at a time when everyone is rightly worried about the impact that AI will have on the job market, it's important to remember that old William Goldman line (which @DKThomp recently introduced into the AI/jobs debate): Nobody knows anything.

Step, the kids banking app recently acquired by MrBeast, made a series of videos coaching kids on how to manipulate their parents into letting them buy crypto.

The videos, referenced in a letter sent by Sen Elizabeth Warren yesterday, have all been deleted.

Breaking: there’s a new way to move money!

Today, we’re launching Payments, our integrated payment service provider (PSP) built to let teams move money easier than ever.

For too long, teams building payment products have had to juggle fragmented vendors, slow bank integrations, evolving regulations, and infrastructure that needs to be rebuilt every time a new rail appears.

Payments changes that.

With one API, teams can:

- Go live in days, not 6-12 months

- Move money across ACH, wires, cards, RTP, FedNow, and stablecoins as first-class rails

- Build with confidence, using built-in KYC/KYB and transaction monitoring

- Scale forever by starting with our PSP and plugging in more banking partners overtime, without re-integrating

All powered by the same orchestration, ledgering, and reconciliation software that’s already processed $400B+ in payments, with 99.99% uptime and 99% CSAT over the last six months.

Our goal is simple: to be the forever payments platform for teams of all sizes, wherever they are on their journey.

Ready to build payments products faster and scale without limits? Visit https://t.co/cmo2JhP5Mz to get started.

FinCEN announced new Bank Secrecy Act regulatory relief regarding the Customer Due Diligence regulation. Learn more about the Exceptive Order and what it means for your #CreditUnion: https://t.co/tdhMwmiWh3

Your AI conversations aren't privileged. Yesterday, Judge Jed Rakoff ruled that 31 documents a defendant generated using an AI tool and later shared with his defense attorneys are not protected by attorney-client privilege or work product doctrine.

The logic is simple: an AI tool is not an attorney. It has no law license, owes no duty of loyalty, and its terms of service explicitly disclaim any attorney-client relationship. Sharing case details with an AI platform is legally no different from talking through your legal situation with a friend (which is not privileged).

You can't fix it after the fact, either. Sending unprivileged documents to your lawyer doesn't retroactively make them privileged. That's been settled law for years. It just hadn't been tested with AI until now.

And here's what really hurt the defendant: the AI provider's privacy policy (Claude), in effect when he used the tool, expressly permits disclosure of user prompts and outputs to governmental authorities. There was no reasonable expectation of confidentiality.

The core problem is the gap between how people experience AI and what's actually happening. The conversational interface feels private. It feels like talking to an advisor. But unless you negotiate for an enterprise agreement that says otherwise, you're inputting information into a third-party commercial platform that retains your data and reserves broad rights to disclose it.

Judge Rakoff also flagged an interesting wrinkle: the defendant reportedly fed information from his attorneys into the AI tool. If prosecutors try to use these documents at trial, defense counsel could become a fact witness, potentially forcing a mistrial. Winning on privilege doesn't make the evidentiary picture simple.

For anyone advising clients or managing legal risk, this is a wake-up call. AI tools are not a safe space for clients to process their counsel's advice and to regurgitate their legal strategy. Every prompt is a potential disclosure. Every output is a potentially discoverable document.

So what do we do about it?

First, attorneys need to be proactive. Advise clients explicitly that anything they put into an AI tool may be discoverable and is almost certainly not privileged. Put it in your engagement letters. Make it part of onboarding. Don't assume clients understand this, because most don't.

Second, if clients want to use AI to help process legal issues (and they clearly will, increasingly), then let's give them a way to do it inside the privilege. Collaborative AI workspaces shared between attorney and client, where the AI interaction happens under counsel's direction and within the attorney-client relationship, can change the analysis entirely. I'm excited to be planning this kind of approach, and I think it's where the industry needs to head.

https://t.co/NFqsznVdXh

Washington appears to be the first state to enact a new specific tax tied to credit union bank purchases. We plan to track whether other states will follow Washington's lead. https://t.co/0RBByg6qoM #creditunions#taxes#Washington

WOW! 🚨 Nubank just got OCC conditional approval for a US bank charter.

Huge for the US market

—

Monzo tried. Failed. Is trying again.

Bunq waited 301 days. Withdrew. Now trying again.

N26 abandoned the US entirely.

Revolut still doesn't have one.

Nubank applied September 30. Approved January 29.

121 days.

—

The difference? They showed up profitable.

$4.2B quarterly revenue. 31% ROE. $783M net income last quarter.

127 million customers. $0.90 cost to serve per month.

Traditional banks spend $5+.

—

This is the world's most valuable LatAm financial institution ($77B market cap) proving its thesis works outside home turf.

60% of Brazilian adults bank with Nubank.

1 in 4 banked Mexicans use Nubank.

Now they're bringing the full stack to the US — deposits, credit cards, lending, digital asset custody.

—

The board tells you everything:

Roberto Campos Neto (former Brazilian Central Bank president) as chair.

Brian Brooks (former acting OCC Comptroller) as director.

Cristina Junqueira running the US operation.

—

Timeline: 12 months to capitalize. 18 months to open. Still needs FDIC and Fed approval.

Target market? "Consumers that know the brand" — read: the 65M+ Hispanic Americans, 92% of whom already use fintechs.

—

Every US neobank is watching.

Every European challenger that couldn't crack the OCC is watching.

If Nubank replicates even a fraction of their LatAm playbook here, the competitive math changes for everyone.

Today marks a new chapter for @AmericasCUs. Scott Simpson takes the helm as President/CEO, ready to strengthen our unified voice in Washington and showcase how essential #CreditUnions are to our nation. https://t.co/vgPCtiiGRu

"Because The Fed Made Their Stress Tests Easier US banks Can Hide Troubled Loans"

🔺🔺🔺

That would be a more appropriate FT headline,

but the actual Financial Times doesn't point fingers

"US banks could hide troubled loans under new reporting rules"

Under the easier stress tests rules banks now only have to report loans that were modified in the last 12 months to help borrowers avoid missing payments

Sl there is no longer a way to tell how many modified loans a bank has, which makes it easier for banks to hide the health of their loan portfolios.

That changes upended a rule in place since the 70's that required banks to report all modified loans.

___________

"..I believe this is enough to prove without a shadow of a doubt how today’s FED is complicit in hiding banks’ problems rather than doing its job to fix them beforehand and avoid a financial catastrophe that at this point is just a matter of when it’s going to happen, not if it’s going to happen.." @DarioCpx

TD bank plead guilty to laundering $675 million to cartels and other criminal organizations. The TD bank, between 2019-2023 did not report transactions that made up the $675 million. Employees of the various branches set up accounts to help launder money while another employee in the anti-fraud department was selling customers personal information. The bank will pay a penalty of $3 billion. They plead guilty to conspiracy to commit money laundering which is the first in U.S. history.

‘Check washing’ is now costing Americans over $1 billion each year, says USPIS — how to spot the threat and protect yourself from becoming a statistic #checks#fraud https://t.co/MLJZgNnsQR

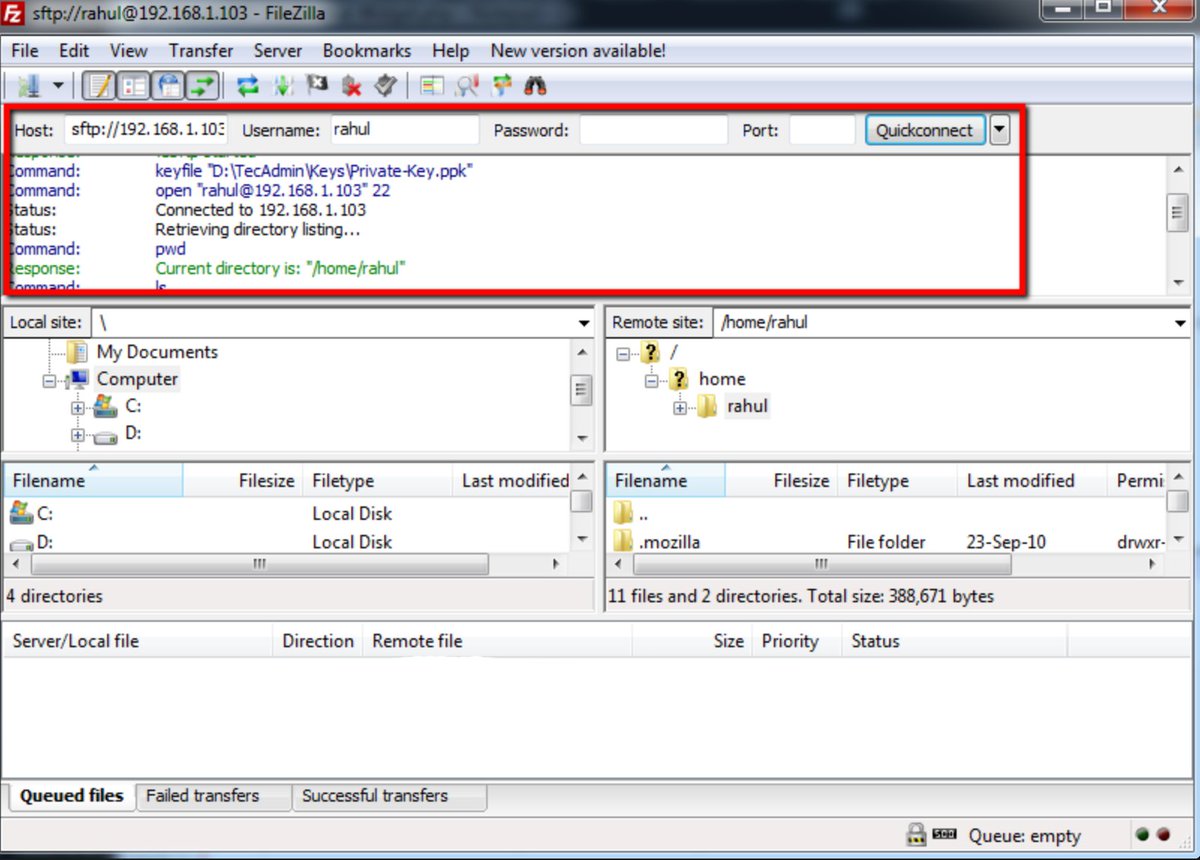

When you make a Bank ACH transaction, it’s literally just an SFTP upload.

Sent as a NACHA file, it's 940 bytes of ASCII text.

Bank-to-Bank transactions cost ~0.2 cents. As long as it travels via encrypted tunnel; it’s compliant!

Here’s how the quirky system works:

Big congratulations to Senator Blaise Ingoglia (@GovGoneWild) on being sworn in as Florida’s new Chief Financial Officer!

A true champion of the credit union movement, CFO Ingoglia has been a strong advocate for public deposits and was honored as our 2023 Lawmaker of the Year.