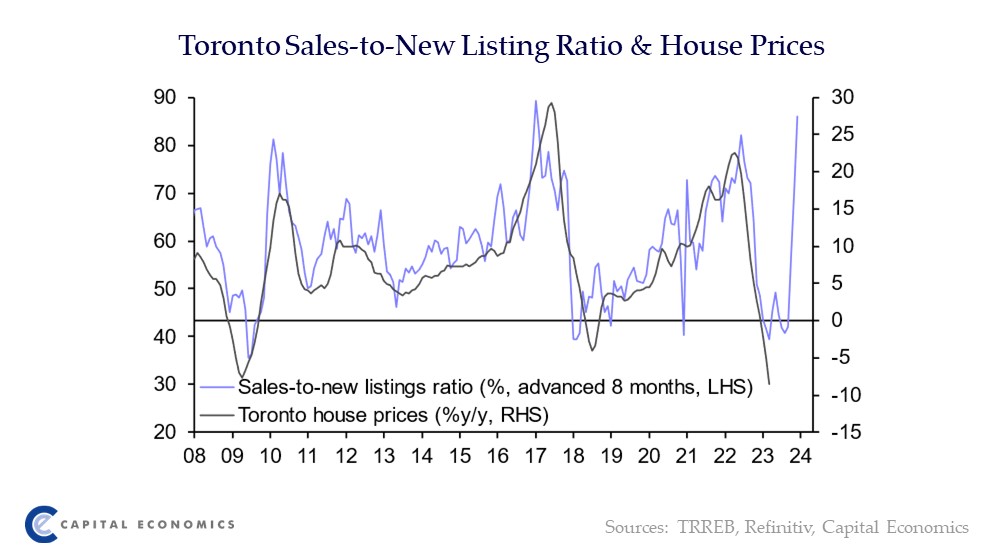

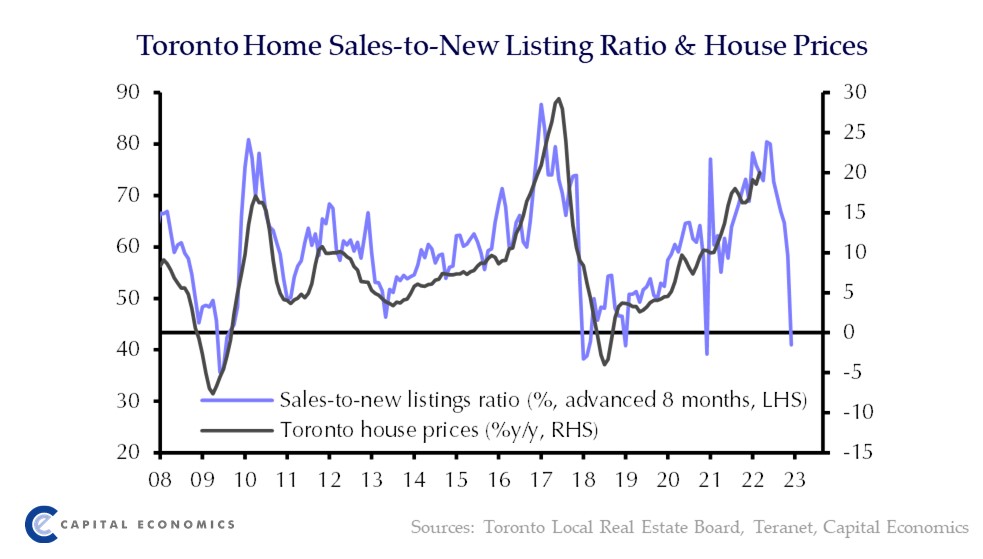

The Toronto home sales-to-new listing ratio, a balance between demand and supply, has surged rapidly above its pandemic peak. This time its about a lack of supply rather than elevated demand, but the direction for prices is clear

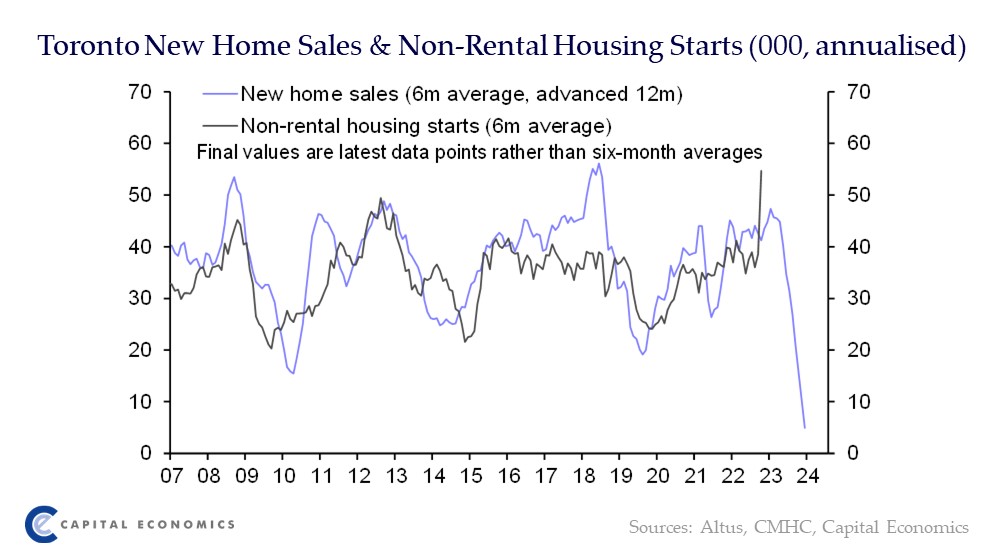

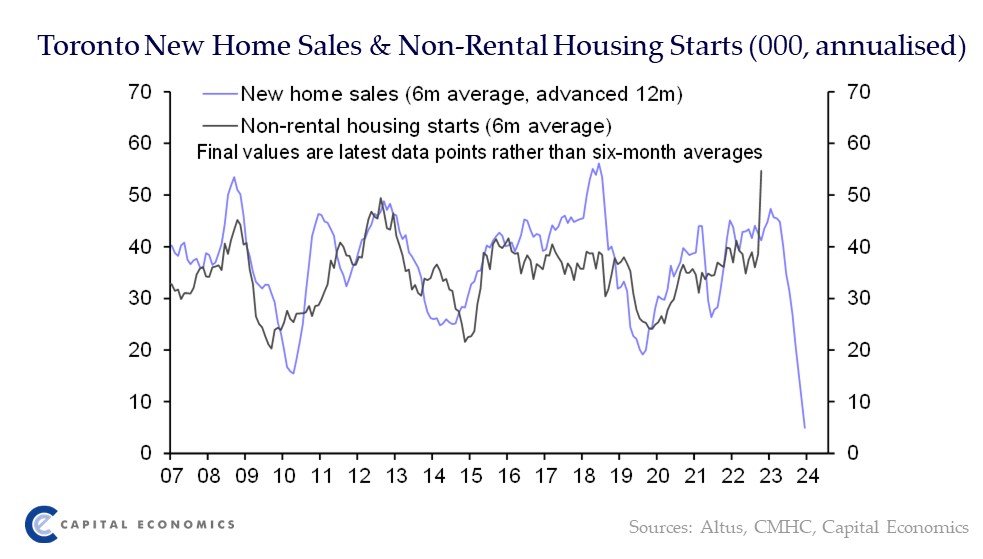

New home sales in Toronto are now weaker than during both the global financial crisis and the pandemic, pointing to a sharp downturn in construction activity in 2023

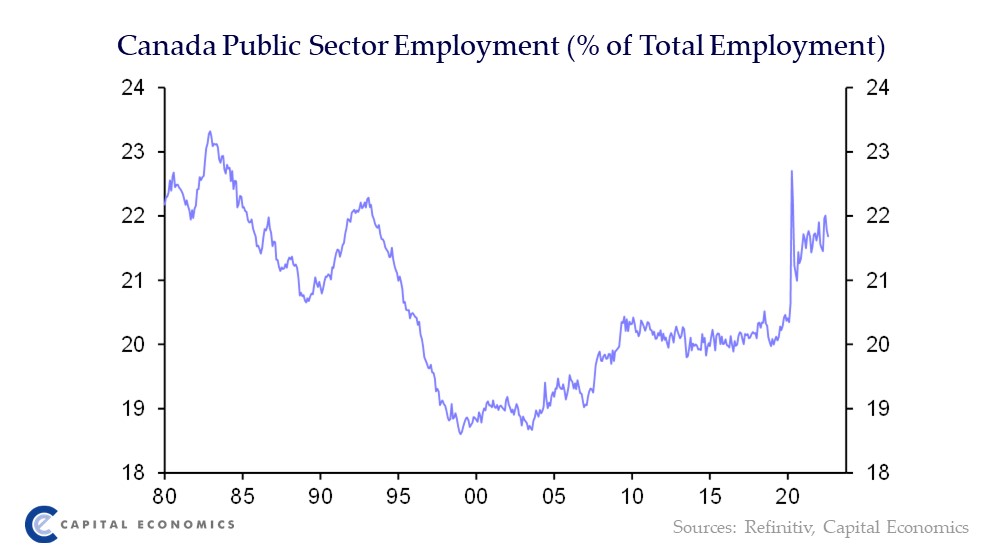

The weakness of employment since June is largely due to a drop in public sector employment, although it still accounts for a far larger share of total employment than before the pandemic

@Michaelseanpor1@RobMcLister This month they change the weight of each item in the CPI basket based on spending patterns in 2021, previously 2020. Gasoline will have a larger weight, so the sharp rise in gasoline prices since April will have a larger upward impact on overall inflation in May and June

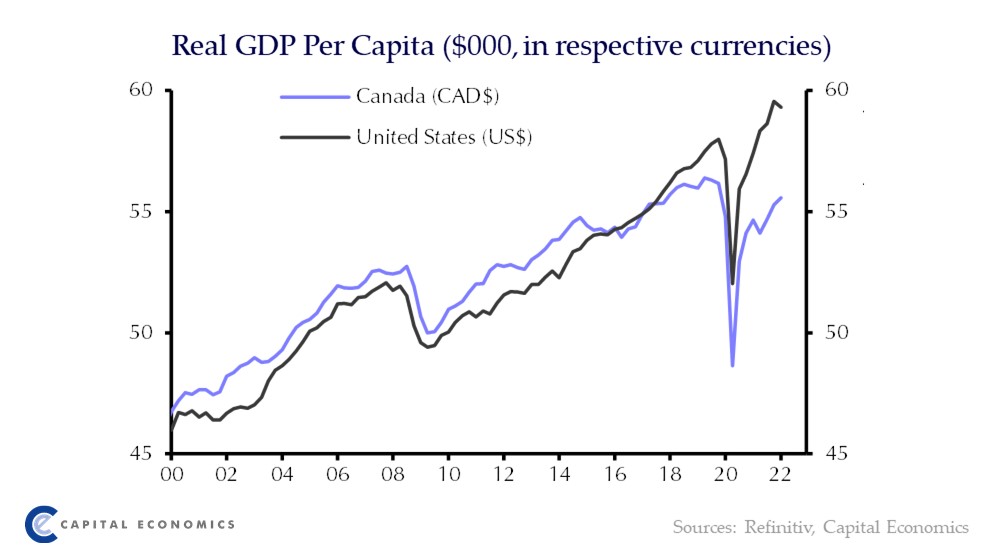

@hank_moody12 Yes mainly that - Canadian consumption 1% higher than pre-pandemic, so down on a per capita basis. US consumption 5% higher than pre-pandemic

While Canada's labour market recovery has been impressive, GDP per capita is still more than 1% below the pre-pandemic level, in sharp contrast to the US where it is more than 2% higher

@mikalskuterud@dima_nomad@StatCan_eng Questions for the CFIB to answer - they only cover small businesses, but their surveys have proved very informative during the pandemic

@mikalskuterud@dima_nomad@StatCan_eng Ok, maybe some modest improvement then, although CFIB survey still suggests it might be reversed in the Mar & Apr vacancy data. The CFIB monthly survey data are all available here: https://t.co/kwitbBNVIZ Excel file link has the full data set

@dima_nomad@mikalskuterud Problem with the vacancy data is they are not seasonally adjusted, and hard to do that given gap in collection during pandemic. Vacancies normally lower in the winter, and rebound in CFIB labour shortages in the April survey (out this morning) suggests no real improvement lately

@francesdonald This speech was a sign the BoC is more concerned about full employment than in the past https://t.co/qJFWGnLD6L, although we also know that, until the latest restrictions least, the labour market recovery was running well ahead of that in the US

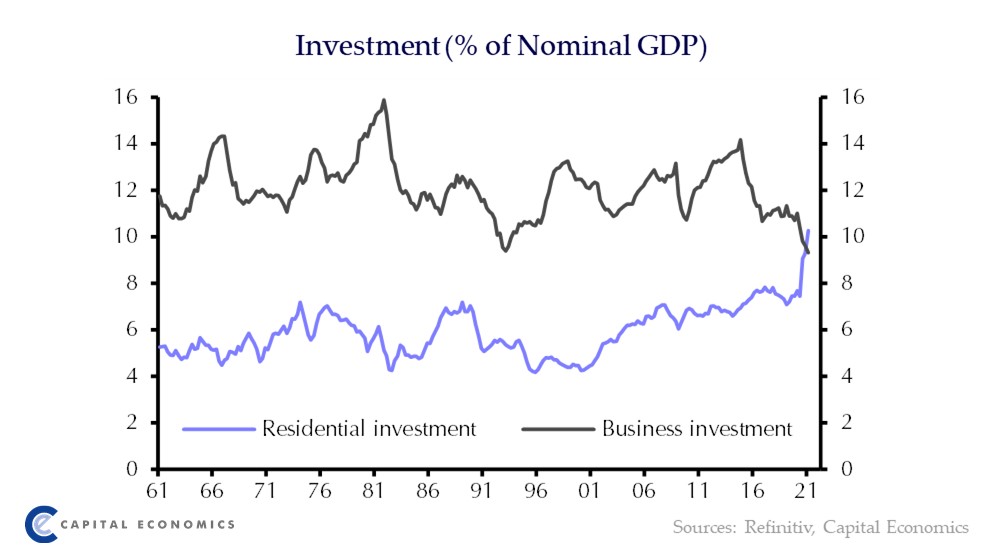

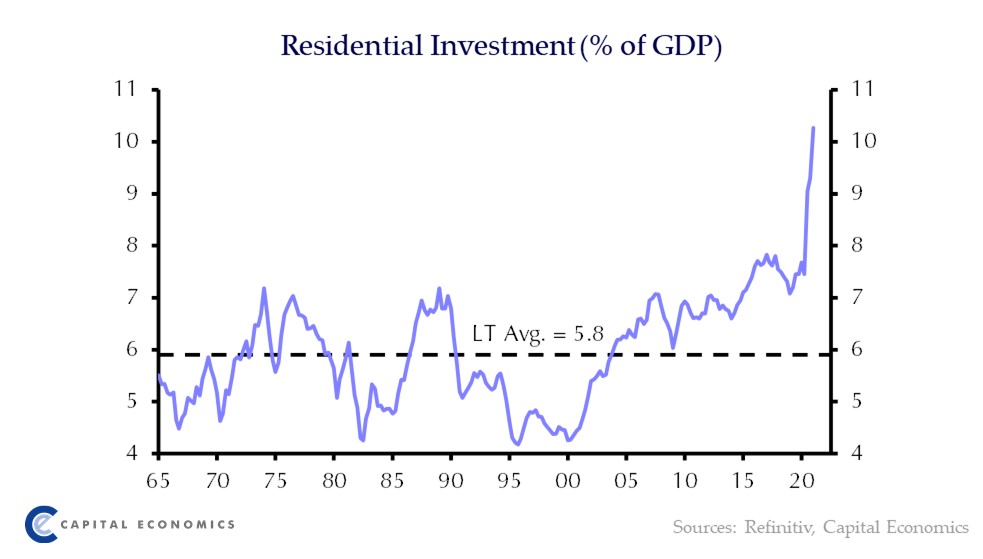

But is the stage already set for the next downturn? The further 43% annualised surge in residential investment means it now accounts for an extraordinarily high 10.3% of nominal GDP, making the economy vulnerable to a future correction (2/2)

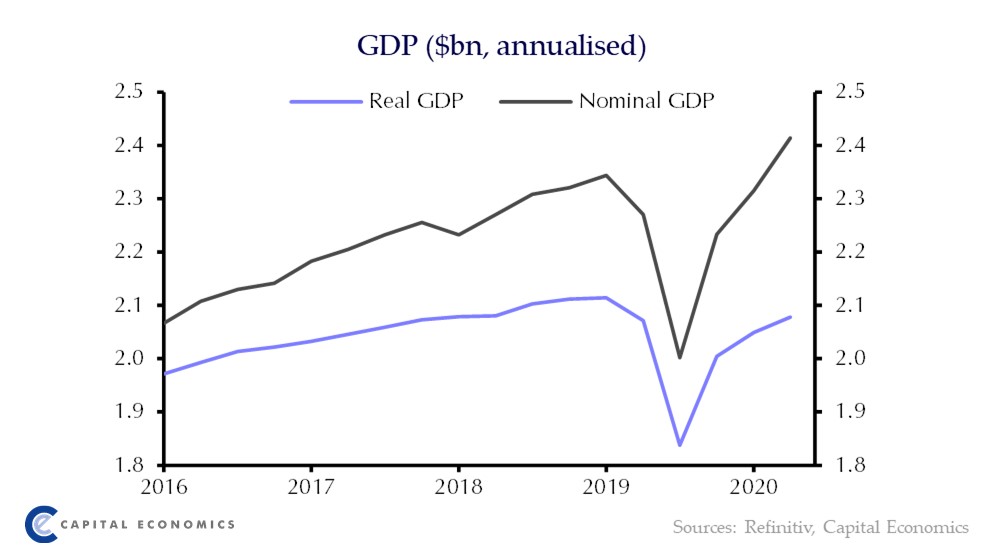

A couple of interesting points to highlight from the Q1 GDP data. First, while real GDP remains 1.7% below its pre-pandemic level, nominal GDP is now 3% higher thanks to strong gains in commodity prices in particular (1/2)

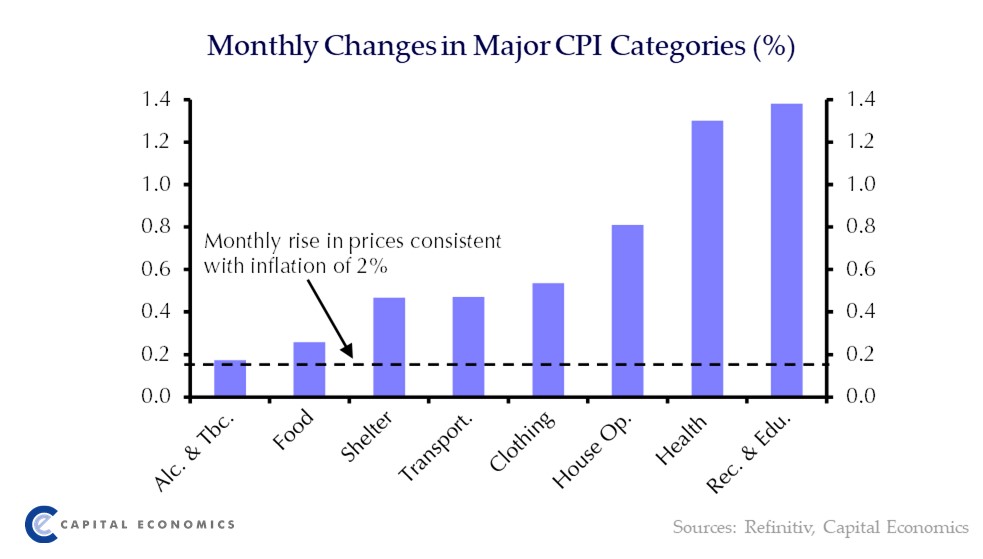

A jump in energy inflation explained most of the rise in headline inflation to 3.4% in April, but inflationary pressures are emerging elsewhere as well. In fact, the m/m% rises in every category in April were consistent with annual inflation of more than 2% #cdnecon