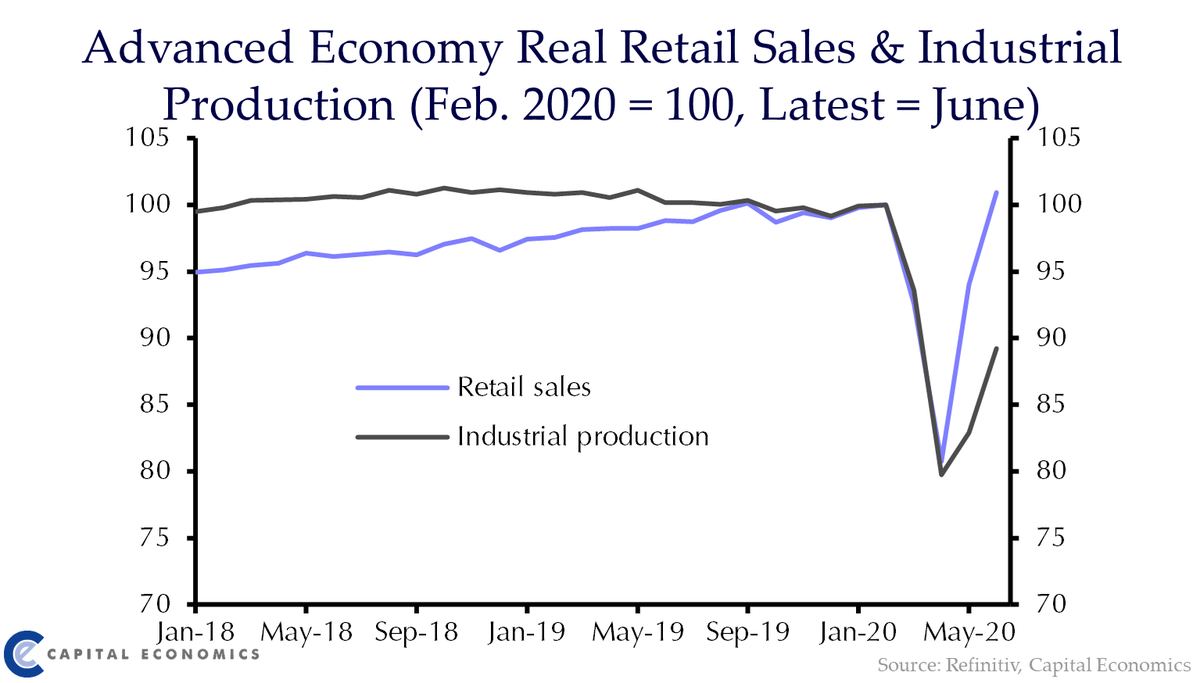

While the rebound in retail sales has been faster than that in IP in DMs, the opposite is true in China. This reflects the differing focus of policy and highlights the role of fiscal support in getting economies back on their feet.

Clients read more here: https://t.co/fAfiJgqP0V

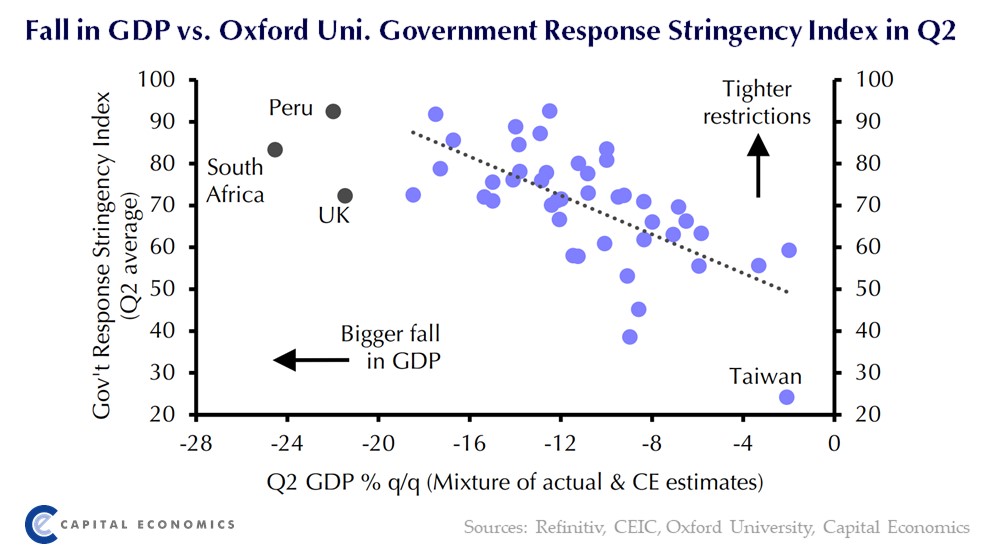

The relative declines in #GDP we are seeing between countries in Q2 are to a large extent a function of how strict #lockdowns were. See our Global Update: https://t.co/nEavW1oAhK

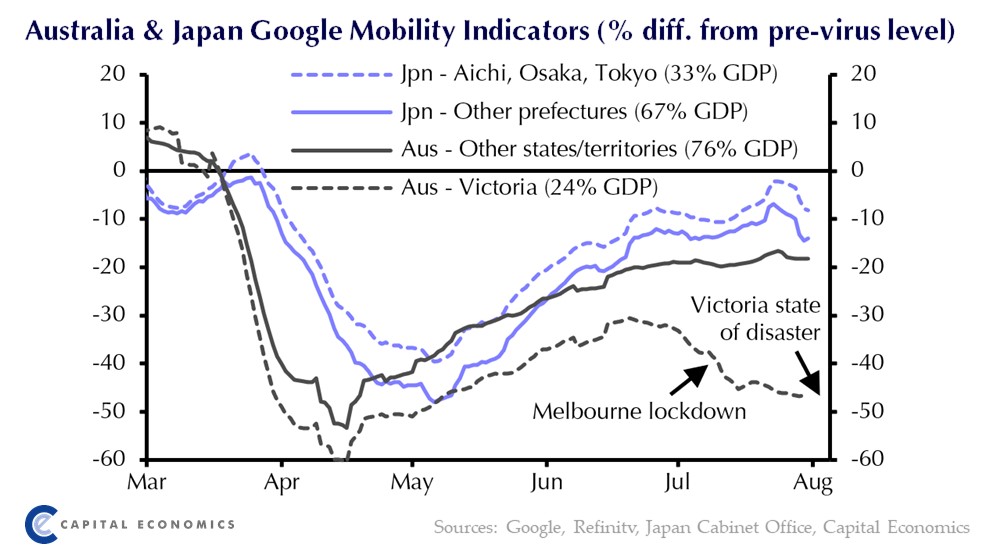

Just as conditions may be about to get better in the #USA, they are deteriorating in other developed countries. #SecondWave in Aus and Japan prompting renewed restrictions. Even before #victorialockdown the recovery in there had already gone into reverse. https://t.co/QpKUpmHu5Q

There isn't a whole lot we can say about the future of the #virus - it's a case of "fundamental uncertainty" (see our blog post https://t.co/53IcbcWjCd). One thing that is clear is that the pandemic has entered its fifth phase. See our Global Update. (https://t.co/yKAbxDI3av)

The rise in July's global manufacturing #PMI suggests that industry continued to recover. But some economies are recovering faster than others and with a resurgence in the virus likely, global industry will probably slow in the months ahead.

https://t.co/B2xF4FILQS

The #FederalReserve is not done cutting interest rates to cushion the blow from #COVID19. 25bps more to come.

See our US Economics Update: https://t.co/Ogbz4hQcof

World trade volumes rose in December in another sign that trade was stabilising at end of 2019. But

early evidence suggests #COVID19 has dealt heavy blow to trade in #EMs since. As disruption drags on, chance of full rebound in Q2 diminishes.

See here: https://t.co/HabSEtRkF5

Some think weak #productivitygrowth means technological progress has hit a wall. We disagree: weakness has been due to poor diffusion of best practices, not slower progress. An investment rebound will facilitate spread of #4thindustrialrevolution

See here: https://t.co/qieiHZu1uM

#Coronavirus outbreak strengthens case for further monetary policy loosening in EMs. But, assuming #covid19 is contained in coming weeks & China production resumes, we think market expectations of rate cuts in some DMs won't come to pass.

See here: https://t.co/mzpGxYCNKM

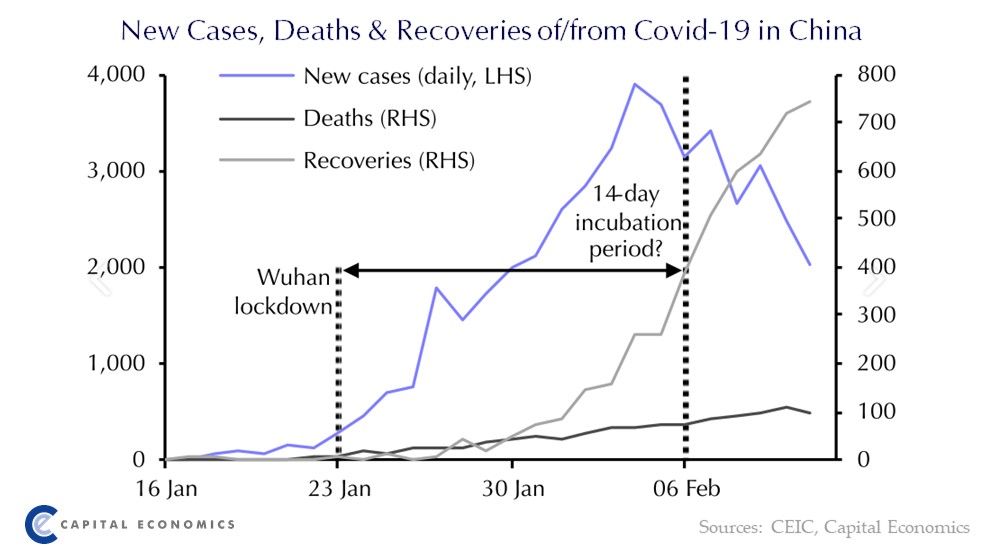

Our chart uses the original definition of new infections. The authorities have changed headline definition recently (now excludes mild cases) but downward trend in Hubei is apparent on either definition. But this is not to say that there is underreporting for other reasons.

@CapEconGlobal This is completely false. The numbers have only declined because China have stopped counting milder cases. So it looks like the new rates of infection have dropped but they have not.

Downward trend in new #COVID19 infections in China suggests containment measures are paying off. As long as they're further relaxed in coming weeks, output lost in Q1 should be made up in subsequent quarters.

See our dedicated #coronavirus website page: https://t.co/TmNlXCaKKx

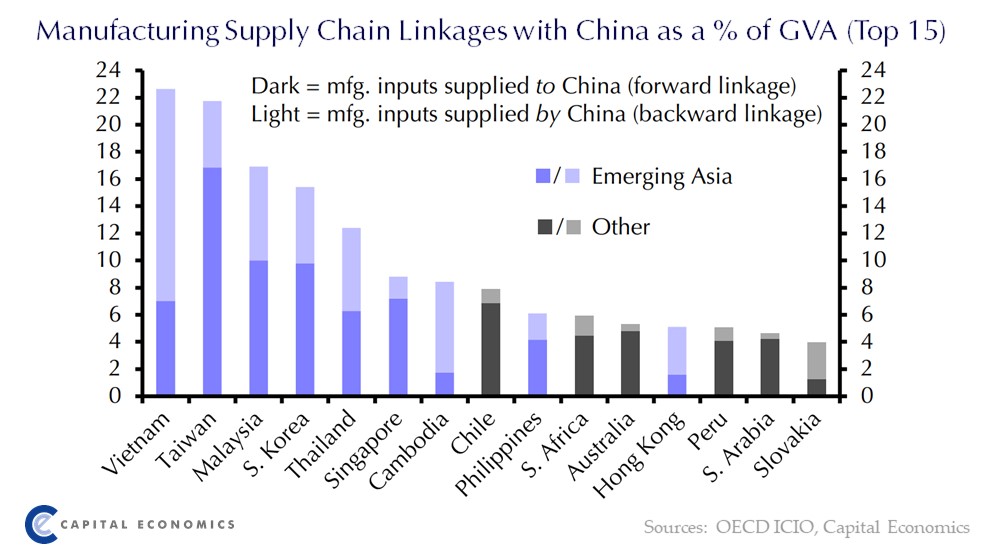

Sadly #coronavirus infections & fatalities continue to grow. Containment efforts mean that Em. Asia growth will slow sharply in Q1. Given China’s prominent position in supply chains there could be global fallout if factory closures extended further.

See: https://t.co/jrIR8n2Hfw

Reliable bellwethers of global activity have stabilised. And a range of data shows this is also true at the country level in the #G7. That said, the global recovery in 2020 will be slow and patchy, and could be derailed by #CoronavirusOutbreak.

See here: https://t.co/YJkgavzvVx

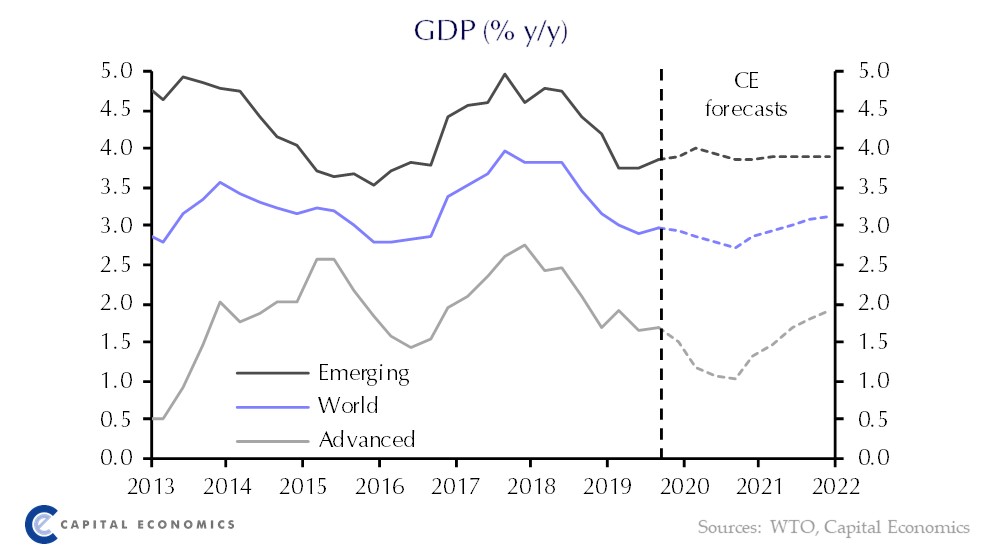

We think global growth is at or near a trough, with leading indicators stabilising or picking up around the world. Just to think that only six months ago markets were fretting about an imminent global recession...

See our Global Economic Outlook: https://t.co/VrE8MkEoMo

We suspect the #globalslowdown has reached a trough. There are signs that looser policy is boosting activity in the US and will do soon in several EMs. Some leading indicators of global activity suggest the turning point is near.

See our Global Chartbook: https://t.co/P7ygGPZY5D

3 Key Takeaways from our 2050 World #GDP Rankings: 1) China fails to overtake the US as the world's largest economy. 2) Indonesia, India & Philippines leap up the rankings. 3) Italy drops out of the top 10. #worldin2050

See our Long Term Global Outlook: https://t.co/iYhuaXsSSK

The global mfg #PMI fell in Dec, ending longest spell of increase since start of 2018. While consistent with a pick-up in IP growth, the PMI has been overstating growth lately. In any case, a material recovery remains elusive.

See our Global Update: https://t.co/l33RUxislT

We are nearing the trough in global growth. The pace of recovery will be slow and spread unevenly across regions, with the US leading the way among the advanced economies & India ahead of the pack in EMs.

See our recent Update: https://t.co/HLODrtGmKg

#FlashPMIs underwhelmed in December, suggesting that advanced economies lost further momentum in Q4. More forward-looking components of the PMI are yet to indicate that a rebound is around the corner.

See our Global Update: https://t.co/GLIAxGKFO9