In our Future of Property research, we identified important post-pandemic shifts in most real estate sectors. We think it is premature to declare the death of cities, but the built environment is likely to change significantly over the coming decades.

https://t.co/TAegfrfsWs

“The closer we look at Sweden the worse things seem to appear,” said James McMorrow, Europe commercial property economist at @CapEconProperty

Article by Rui Soares,FAM Frankfurt Asset Management , via @FTAlphaville https://t.co/dSuqrS7V4y

The exceptionally strong rebound in commercial property returns has been clear from the middle of last year. While this came earlier than most expected, we think it reflected special conditions and won’t last. https://t.co/v6eifBhspd

Our estimates of the size of the risks in the transition to net zero for commercial property markets suggest that, at less than 8% of current capital values, the costs are significant but not insurmountable. https://t.co/P5OAOAQ5LU

While we expect the US to comfortably outperform the UK and EZ in 2022, we forecast similar returns everywhere thereafter. But with interest rate rises likely to impact US valuations sooner, we think the US will underperform by 1.5%-2% pts p.a. in 2024-26. https://t.co/gf0LFYKwAi

Omicron poses downside risk to an already soft economic outlook. However, with inflation set to fall back, lower interest rates should support the property upturn, albeit the recovery in offices and retail will be held back by structural changes. https://t.co/iPP8QOdYot

The outlook for rents remains fragile, while we are close to the peak of capital value growth. Within this, industrial remains the standout, while London offices have the weakest returns https://t.co/3mxWcwPG0b

We are proud to announce that our research on the natural vacancy rate in European office markets won the SPR's Under 30s Research Prize. Clients can revisit the piece here:

https://t.co/9nzhiHEtRz

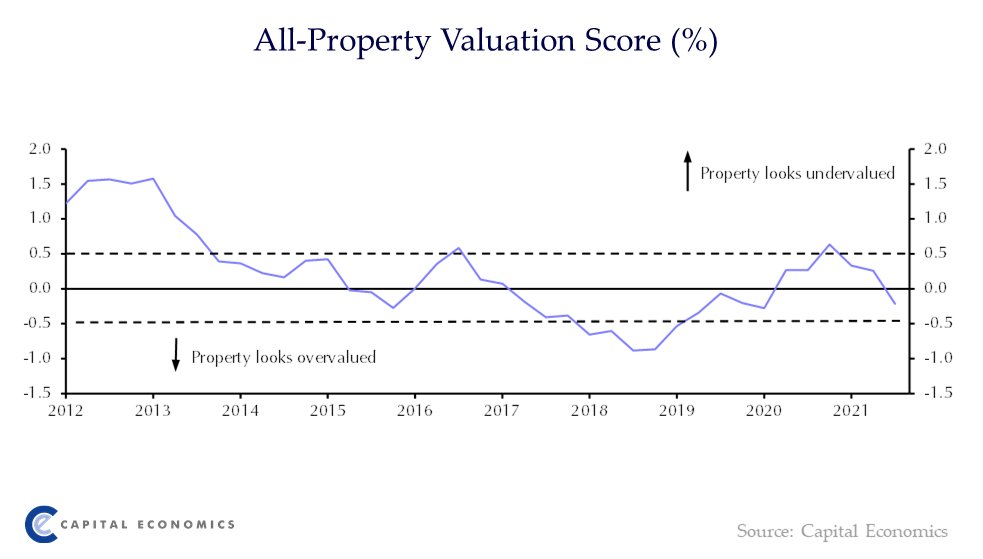

Compared to bonds and equities, property valuations deteriorated further in Q3. This was due to a fall in property yields and a rise in both bond and equity yields. Although we expect a less dramatic fall in Q4, the risks to yields lie on the downside. https://t.co/gSvWy0C7iH

While weaker demand for office and retail will weigh on performance in European cities dependent on these assets, prospects are better for cities that are attractive to more than just workers and therefore can fill the gap with other property.

https://t.co/r53b7uYGYt

US #NCREIF data for Q3 showed a 5.2% quarterly return, taking year-to-date all property rtns above 10%. #Industrial still best game in town, seeing supersized returns of over 10% q/q and on course for well over 30% for the year! Reflects strong demand from investors and lenders

Our webinar on the Future of US Cities said:

- Americans are returning to cities, but still limited signs of return to the office

- Southern metros will be the big winners

- Largest US metros will be slow to recover and second tier cities will outperform

https://t.co/rJNPrp1H3J

While the UK has seen house prices boom over the past year, central London has not joined in as more remote working led buyers to shun the capital for more space elsewhere. But demand indicators show that it is far too early to call time on city living. https://t.co/8dnb9tKQuZ

Our property team this week briefed clients on the future of cities in light of pandemic-driven changes. Among the big questions they tackled was the outlook for office demand and what we're expecting among major European city markets. https://t.co/6YENNQpjsQ

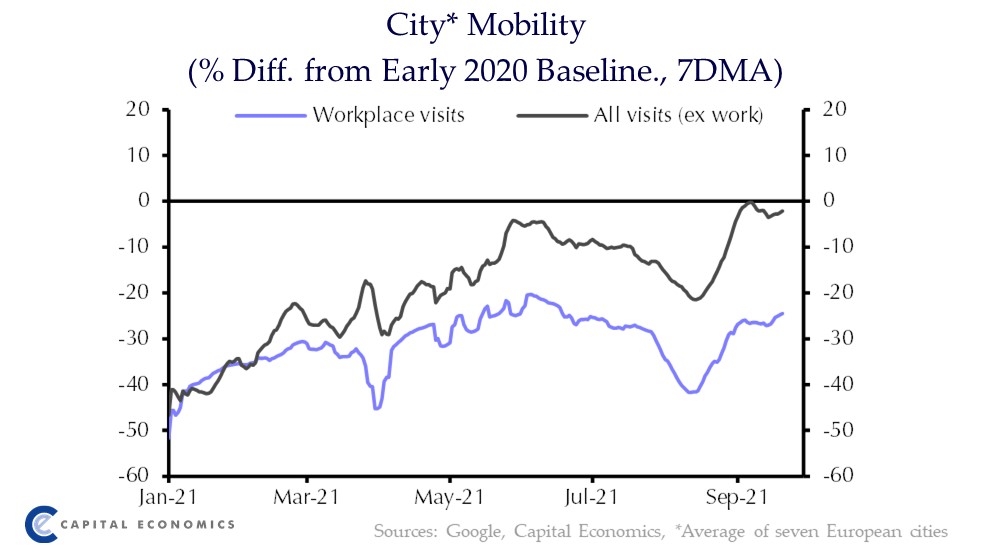

The pandemic and use of remote working appeared to entice some Europeans to leave cities in 2020. However, the recent improvement in city mobility supports our view that this would prove short-lived, as cities remain attractive for a range of reasons. https://t.co/3sm2ZaU3ge

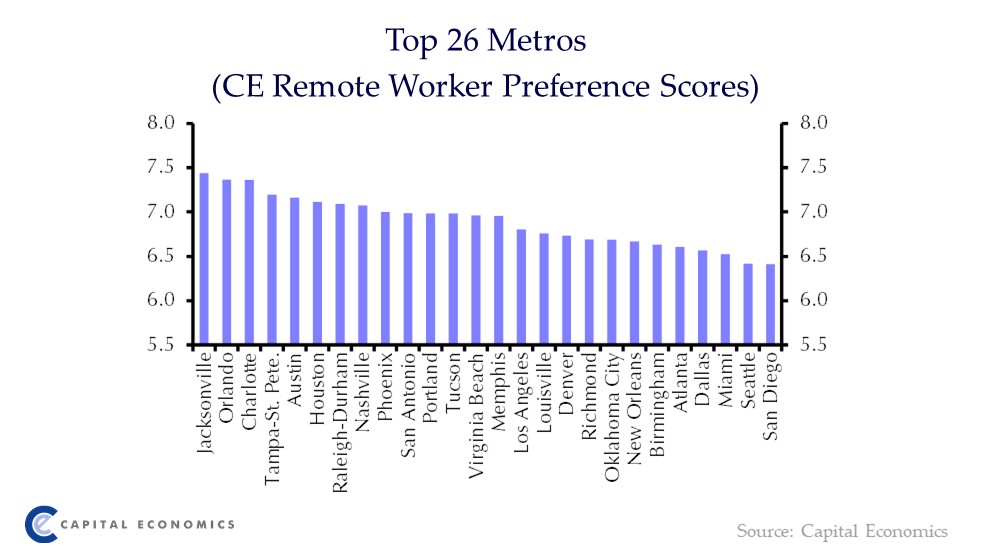

The pandemic's newly footloose 1mn workers will prioritise cost of living, a metro's desirability and its climate over the job opportunities it offers. The biggest winners from this trend will be a number of metros in Florida, Texas and North Carolina. https://t.co/plLpMl7e6K

The Evergrande crisis has made waves in financial markets this week. But, while the developed property markets we cover may see some short-term upheaval, we think the impacts outside of China are unlikely to be severe or lasting. https://t.co/QNWWnL7RSf

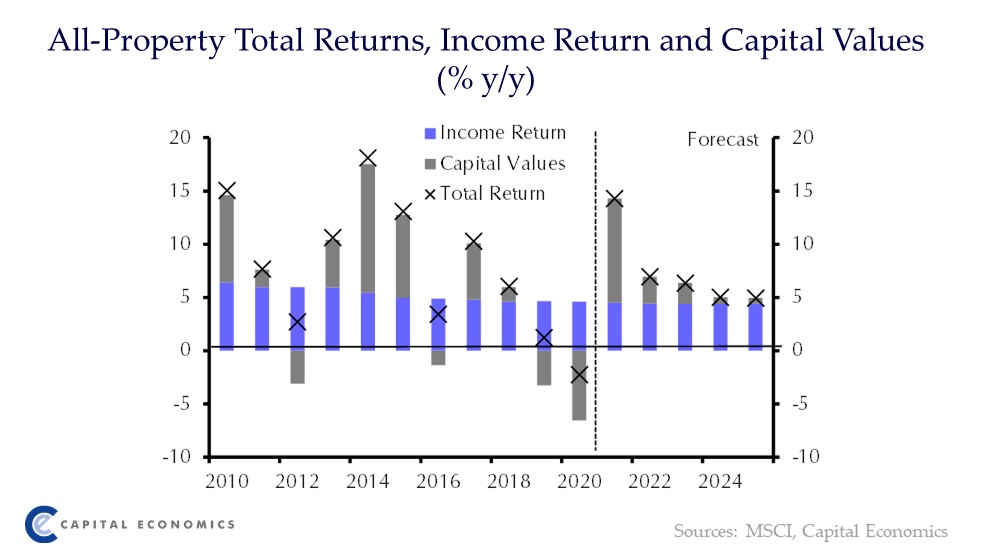

The economic recovery will support the property market upturn, but structural changes will limit the rental rebound in offices and retail. Industrial is set to outperform over 2021-22, but stronger value growth after 2022 will allow retail to overtake. https://t.co/jkms5wf9A1

Recent data have been surprisingly upbeat and suggest that there is a risk that the recovery is stronger than expected. But we think investors may have run ahead of themselves and this trend is unlikely to be sustained given the weak rental outlook. https://t.co/XrrZ5hJzs5

We expect more hybrid working to lead to a flight to quality space. But while we think CBD office rents will hold up better than other submarkets after COVID-19, we don't expect this to mark the start of a dramatic divergence, similar to the past. https://t.co/vFhEOpCnb2