Inversionista, trader y fundador de Traders Club. Comparto análisis, estrategias con opciones y el crecimiento real de mi portafolio DCA. ¡Crecemos juntos!

SpaceX hit $3 trillion market cap today.

This means Elon Musk made more money in the last 24 hours than Warren Buffett made in his entire lifetime.

Insane.

La historia más importante de $MSFT hoy

Hay dos líneas y la divergencia entre ellas es el punto central del análisis.

La línea naranja es el Fwd P/E normalizado. Media histórica de 10 años: 27.97x. Máximo: 36.98x. Mínimo: 17.49x. Valor actual: 21.81x — significativamente por debajo de la media histórica y acercándose al extremo inferior del rango.

La línea verde es el Market Cap / FCF . Media histórica: 30.79x. Máximo: 53.89x. Mínimo: 15.71x. Valor actual: 41.37x — por encima de la media histórica y en la mitad superior del rango.

Esa divergencia entre ambas líneas es inusual y merece análisis cuidadoso. Históricamente desde 2016 hasta 2022 ambas líneas se movían casi juntas — cuando el P/E subía, el P/FCF subía proporcionalmente. Desde 2023 se separaron y la brecha se amplió significativamente. Hoy están en extremos opuestos de sus rangos históricos respectivos.

Por qué existe esa divergencia, y qué significa:

La explicación es el capex masivo de AI. Microsoft está invirtiendo $80B anuales en infraestructura de AI — datacenters, chips, cables, todo. Ese capex sale del FCF antes de que genere el revenue correspondiente. La contabilidad GAAP distribuye ese gasto via depreciación en 10-15 años, entonces el P/E normalizado captura menos del impacto que el P/FCF que lo ve directamente en caja.

En otras palabras: el P/E en 21.81x parece barato porque la depreciación del capex de AI todavía no golpeó completamente el income statement.

El P/FCF en 41.37x parece caro porque el cash ya salió pero el revenue de Azure AI todavía no llegó completamente.

¿Cuál es el número más honesto? Los dos juntos. El P/E te dice lo que el negocio genera hoy en términos contables. El P/FCF te dice el costo real de construir el negocio del mañana. La verdad está en el medio.

El Fwd P/E en 21.81x : la señal más interesante

Este es el número que más me impacta del gráfico. $MSFT a 21.81x earnings normalizado está en el percentil más bajo de la última década — solo estuvo más barato en el crash de COVID de marzo 2020 y brevemente en el bear market de 2022. En ambos casos, quien compró en esos niveles generó retornos extraordinarios en los 12-24 meses siguientes.

Para contextualizar: en 2016-2017, cuando Nadella recién estaba ejecutando la transición a cloud y el negocio crecía al 10-12%, $MSFT cotizaba a 20-22x earnings. Hoy, con Azure creciendo al 31% YoY, Copilot con 15 millones de asientos pagos, margen operativo del 47%, ROIC mayor al 30%, y posicionamiento central en la infraestructura de AI global, cotiza al mismo múltiplo que en 2016. Eso no tiene sentido económico en el largo plazo.

El P/FCF en 41.37x: el argumento bajista que hay que tomar en serio

El contra-argumento también está en el gráfico. El P/FCF en 41.37x está por encima de la media histórica de 30.79x y muy lejos del mínimo de 15.71x. Quien dice que $MSFT es cara usa este número — y no está equivocado en señalarlo.

La pregunta correcta es si ese capex de $80B anuales va a generar el retorno que justifica el múltiplo. Si Azure AI crece al 35-40% en los próximos tres años y el capex empieza a moderarse desde 2027 en adelante — que es exactamente lo que el management guió — el FCF va a explotar al alza y el P/FCF va a colapsar hacia la media. Si el capex crece más de lo esperado o el revenue de AI decepciona, el P/FCF actual se mantiene elevado y la acción tiene presión.

El mercado hoy le está dando más peso al P/FCF elevado — de ahí la corrección. Pero el P/E en mínimos históricos dice que los earnings contables no justifican esa presión.

Mi lectura integrada:

El gráfico muestra una empresa en un punto de inflexión de valoración muy inusual. El P/E en 21.81x está en mínimos de una década para un negocio que objetivamente es mejor hoy que en cualquier momento de esa década. El P/FCF en 41.37x refleja el costo real de la apuesta de AI — una apuesta que el mercado está cuestionando en el corto plazo.

La historia de Microsoft desde 2014 es la historia de Nadella invirtiendo agresivamente adelante de la curva — en cloud cuando nadie creía, en Teams cuando todos usaban Slack, en OpenAI cuando el mundo no entendía GPT — y el FCF siguiendo siempre 18-24 meses después de que el capex pico. El patrón se repite.

Para un inversor de largo plazo, $MSFT a 21.81x NTM earnings con Azure creciendo al 31%, Copilot monetizándose, y márgenes del 47% es una de las entradas más atractivas de la última década en esta empresa. El P/FCF elevado es el precio que pagás por el optionality de AI — y dado el posicionamiento de $MSFT en esa carrera, parece un precio razonable.

Sigo invertido y sumando posición en $MSFT y este gráfico refuerza la convicción en lugar de debilitarla. El mercado te está ofreciendo la mejor empresa de software del mundo al múltiplo de earnings más bajo en diez años.

$BTC will return to its ATH

$ETH will return to its ATH

$SPY will return to its ATH

$AMZN will return to its ATH

$GOOG will return to its ATH

$NVDA will return to its ATH

$MSFT will return to its ATH

$META will return to its ATH

$TSLA will return to its ATH

$UNH will return to its ATH

‼️Market pressure on Trump to de-escalate the Iran War is at extreme levels:

The Trump Pain Point Index, or "TACO Index," just hit ~2 standard deviations above the mean for the first time ever.

This index combines inverse S&P 500 returns, 10-year Treasury yields, 30-year mortgage rates, gasoline futures, 1-year CPI swaps, and presidential approval ratings into a single measure of economic and political pain.

Every major spike in the index over the last 15 months has been followed by a policy reversal or pause from the White House.

The 90-day pause on tariffs came after the April 2025 spike, the government shutdown ended after the September spike, the Greenland threat was dropped after the December spike, and most recently, Trump backed down from threats on Iranian energy infrastructure.

The pattern is consistent. When Treasury yields spike too much alongside falling stocks, Trump intervenes.

At $373, $MSFT is now 33% off all time highs and trading at a 5 year low P/E.

There is no reason $MSFT will not make it's way back to ATH eventually. The fundamentals are too good.

> 16% revenue growth

> $77 billion free cash flow

> Backlog of $630 billion

> $89 billion in cash on the balance sheet

The risk reward here is undeniable.

THE NUMBER 1 REASON I CONTINUALLY BUY $META STOCK

I've been continually adding to my META stock position any time the stock goes under $600 over the last few weeks!

The reason - Mark Zuckerberg!

Every time the market buries him, he comes back with a company that’s even stronger. Just look at how he's managed to bounce back across the major controversies META has been through over the last 13 years!

1. 2012 IPO Collapse: The stock crashed -53%!

- They IPO'd at $38 - fell to ~$18, a -53% crash.

- The media called it a failed launch.

- Zuck pivots the entire company to mobile and builds one of the most profitable ad machines on earth. Stock recovers and then runs for a decade!

2. 2018 Cambridge Analytica Meltdown (-24% / -$134B in market cap lost)

- The privacy scandal explodes. “Delete Facebook” goes global!

- The stock drops -24% in days, wiping $134B off the market cap.

- Zuck responds, he tightens privacy controls, stabilizes the platform, and keeps driving growth. The stock recovers within months!

3. 2021–2022 Meta Crash (-76%)

- Apple kills ad tracking. The Metaverse investment is mocked by everyone!

- Meta collapses from the high $300's to $90 - a -76% crash, nearly $700B in market cap erased!

- Zuck responds by declaring the “Year of Efficiency,” cuts 21,000+ jobs, rebuilds ads around AI, scales Reels… and by 2024 the stock is up 500%+ and Meta is back over $1 TRILLION!

This is why I buy Meta.

Not because it avoids pain - but because every time it gets hit, Zuck uses the punch to build a stronger company.!

And the bull case going forward?

- Re-acceleration in ad monetization and AI-driven efficiency. Meta is squeezing more value out of every impression through AI optimization. Better targeting, greater yield leading to margin expansion and revenue acceleration.

- WhatsApp monetization is still in its infancy

The biggest messaging app on the planet is barely monetized in the West. Payments, business messaging, commerce, all have huge potential.

- AI infrastructure scale will give META massive leverage and new revenue lines.

Their compute stack is becoming a real differentiatior - lowering their unit costs and increasing their margins even further. Zuck has signalled they will continue to drive future opportunities in AI services, LLMs, agents, and on-device integration!

This combo of both Zuck as CEO and the key bull cases is why I keep buying. Zuck is coming into his prime, still only 41 years of age and he has no plan in stepping aside for at least another 20 years!

Meta isn’t just surviving - it’s a cash cow continually compounding.

I'm betting on ZUCK!

El rally del petróleo este fin de semana parece tener dos motores principales:

1.Riesgo geopolítico.

Las tensiones con Irán reavivaron el miedo a interrupciones en el Golfo Pérsico y el Estrecho de Hormuz (por donde pasa ~20% del petróleo mundial). Eso añade una prima de riesgo inmediata al crudo.

2.Short squeeze.

Muchos traders estaban posicionados en corto. Cuando el precio empezó a subir por las noticias, tuvieron que cubrir posiciones, amplificando el movimiento.

Cuando un rally viene de riesgo geopolítico + short covering, muchas veces termina siendo un pico de corto plazo.

La pregunta ahora es:

¿interrupción real de oferta… o solo prima de riesgo temporal?

Yo sigo bullish en el mediano/largo plazo.

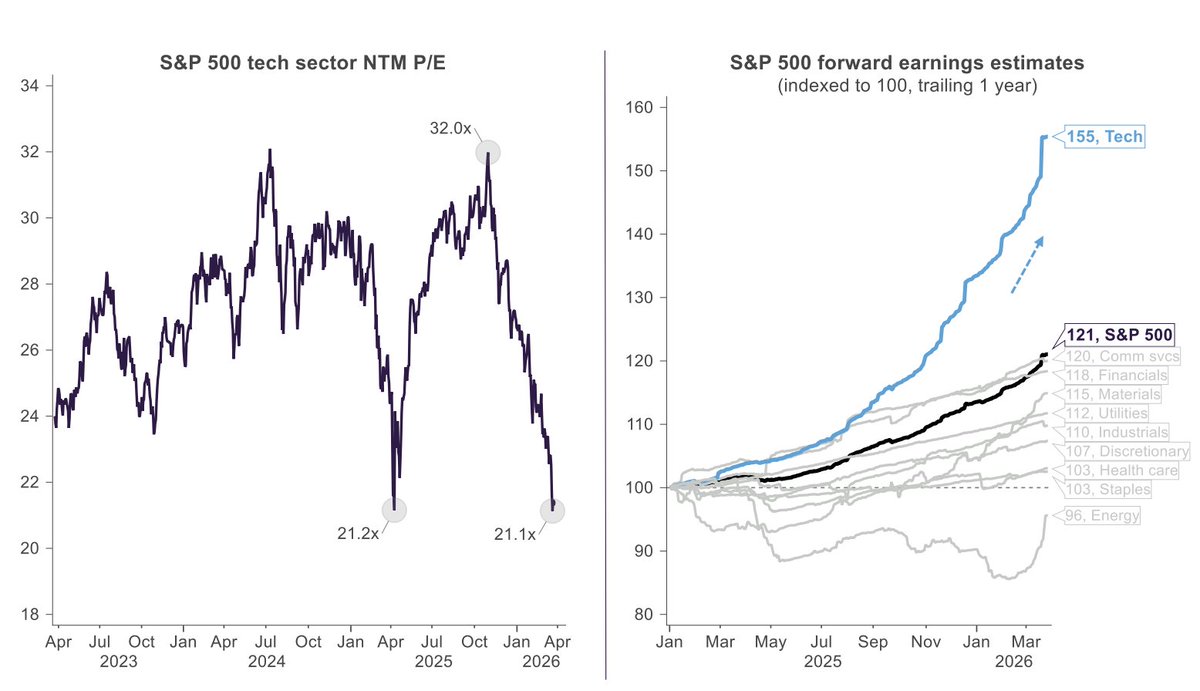

La rotación de Growth a Value se está poniendo ridicula cuando uno realmente evalua cómo están pensando los fondos.

Estoy revisando $DE (Deere).

Ventas +13% YoY.

Ingreso neto -25% YoY.

Operating profit -59% YoY.

La acción cotiza a un PE de 35x y está +42% YTD.

Uno de los argumentos que escuché:

“Empresas como Deere hacen cosas físicas que la IA no puede reemplazar.”

¿En serio?

¿Estamos pagando 35x por crecimiento negativo solo porque “hacen cosas tangibles”?

$DE es una gran empresa. Merece múltiplo.

Pero lo que estamos viendo ahora no es fundamental, es narrativa.

Hay tanto miedo a que la IA “comoditize” todo, que los fondos están rotando hacia compañías que hacen cosas físicas solo por no estar en el epicentro tecnológico.

Verizon, Coke, Deere… preferidas sobre $META, $GOOGL, $AMZN.

El mercado es cíclico.

Si la IA realmente va a comerse el mundo, entonces $NVDA debería valer mucho más de lo que vale hoy porque toda esa demanda termina concentrándose ahí.

Y si no va a destruir todos los sectores, entonces pagar múltiplos extremos por crecimiento negativo tampoco tiene sentido.

No sé cuándo, pero este trade eventualmente se va a dar vuelta.

La pregunta no es si.

Es cuándo.

BIG TECH EARNINGS OFFICIALLY START TOMORROW.

$META, $MSFT, and $TSLA kick us off.

The S&P is up +1.37% YTD but is being massively outperformed by international stocks and small caps.

High beta names have had an incredible year already.

Tomorrow, I think we need the large caps to remind the world why they are worth trillions of dollars. Maybe we start to see a rotation back into them which likely puts us at $SPX $7000.

$META —> Zucks needs to tell us what he’s doing with the capex besides making ads better, any guidance of $100B capex MUST have support over explaining ROI especially if Zucks is competing with GCP/AWS/Azure with “Meta Compute”

$MSFT —> Azure needs to keep scaling, CoPilot needs to show further penetration, Claude has now shown massive potential for enterprise adoption and Microsoft should be positioning their workflows as essential within the enterprise which should lead to increased monetization via AI

$TSLA —> Elon just needs to promise the robots will be here soon and the market needs to believe him 😂

Which of these 3 names are you long?

FOMC tomorrow as well, 2.8% chance of a rate cut but we will have the last of 4 meetings with Powell so we ought to cherish it.

THE GREATEST SHOW ON EARTH CONTINUES THIS WEEK.