There were only two times in the last thirty years that investors had an incredible opportunity to hedge.

As seen as a fraction of Currency in Circulation, today's cost to hedge is even cheaper.

$QQQ $TLT $SPY

Howard Marks has been writing investment memos for 30 years that Warren Buffett says he reads first thing every time.

In 36 minutes he explains why every bull market ends the same way - and where he thinks we are right now.

36-min. Oaktree. TBPN.

Bookmark & watch - the clearest market cycle read you'll find in 2026

A privately-rated BBB defaults like a publicly-rated BB+ or BB, according to a CBS study

US life insurers hold $481bn of this paper, up from 2% to 12% of portfolios since ‘18.

The rating is the product.

Charlie Munger: "The director's table in the Heinz Corporation cost $600,000. The director's table at Costco cost about $300. They are different places [with] different ethos."

"If you get fat like that, somebody like 3G comes along and says, 'I want to buy you and cut you back to normal.'"

"Of course, it's possible to over-cut — but my guess is there's a lot of fat in our successful places."

(Daily Journal AGM || 2022)

Did you know Peter Thiel's Macro LLC liquidated his entire stock portfolio valued at $210 million.

As of Q1 2026 he owns zero stocks outside of Palantir.

I wonder what he knows that we don't?

Warren Buffett on why chasing yield on cash is a mistake:

A Berkshire shareholder, Ed Schmidt, asks where all the sidelined money is being held, pointing out that every option looks bad:

Banks paying nothing, risky corporate bonds, and government bonds that "seem less and less sound as each day passes."

Buffett agrees the choices are poor, but says it doesn't matter, because Berkshire treats short-term money completely differently from most investors.

"He's certainly right that all the choices are lousy for short-term money now, but we don't play around with short-term money."

He explains that in 2008, before the crisis hit, Berkshire owned no commercial paper and no money market funds.

The big money stayed in treasuries, earning almost nothing, and Buffett is blunt that the temptation to reach for a little more is exactly the trap to avoid:

"The last thing in the world we would do at Berkshire is to try and get five or 10 or 20 or 30 basis points more by going into some other things with our short-term money."

His framing for why is simple:

"It is a parking place. It's an unattractive parking place, but it's a parking place where we know we'll get our car back when we want it."

The reason that matters became clear in September 2008. Berkshire had committed $6.5 billion to the Mars-Wrigley deal months earlier, long before anyone knew what that autumn would bring.

When the date arrived, the form of the money was everything:

"I had to show up with $6.5 billion. I couldn't show up with a money market fund or some commercial paper or anything of the sort. I had to show up with cash."

That's why his conviction lands where it does:

"Virtually the only thing I feel good about in terms of having large amounts of ready cash is treasury bills."

Charlie Munger puts it more sharply, reframing the whole question as a discipline issue rather than a yield issue:

"I think it's really stupid to try and maximize returns on short-term money if you're an opportunistic game the way we are, where we want to suddenly deploy money."

He points to pipelines that came up for sale on a Saturday and had to close by Monday.

There was no room to be stuck in "some dubious instrument" when the cash was suddenly needed.

Buffett adds his own version of the same story, a pipeline whose seller feared bankruptcy the following week and needed the money immediately, with regulatory clearance still pending. Berkshire offered to close early and let the regulators review everything afterward, even unwind the deal if required. The point being that readiness, not return, is what closes deals:

"Our ability to come up with cash when people need it, and when the rest of the world is petrified for some reason, has enabled several deals to get done."

And that is the entire logic behind holding tens of billions in treasuries earning almost nothing:

"When somebody comes to us and they say we need a deal right now, we can do it, and they know we can do it, and it can be big. It just has to be attractive."

"The $TWO Board has been clear in what it requires: all cash, to all stockholders, no stock component. Fully committed financing to cover the entire $12.50 per share in cash," the REIT said.

By @NMNBrad

https://t.co/5wQG84HjJ5

The key question is not whether AI is important or useful.

The key question is whether the economic value created by AI ultimately exceeds the extraordinary amount of capital currently being invested.

Will the return justify the investment?

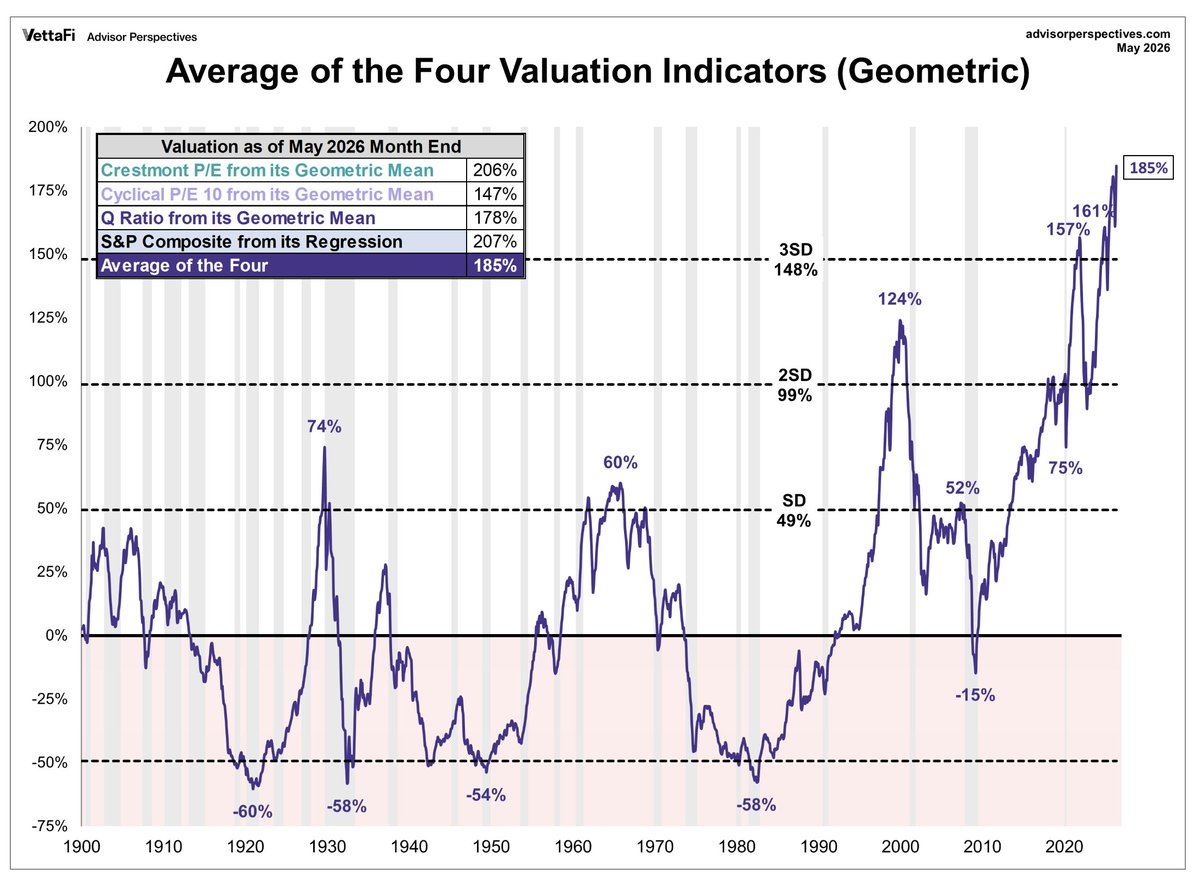

The current reading of 185% above historical fair value is the highest in the entire data series going back to 1900.

The purple line is the average of four long-term valuation measures, each expressed as a percentage above or below its historical geometric mean:

* Crestmont P/E

* Cyclically Adjusted P/E (CAPE/Shiller P/E)

* Tobin's Q Ratio

* S&P Composite Regression Model

Historically, when broad U.S. indexes reached extreme valuations, future leadership often came from:

* Small caps

* Value stocks

* International markets

* Commodity-related businesses

* Asset-heavy cyclical sectors

This is one reason many value investors today focus on areas trading at single-digit EBIT multiples while the major indexes trade at historically rich valuations.

Some of the best periods for value strategies occurred when the broad market was near valuation extremes and the valuation spread between glamour and neglected businesses was unusually wide.

@waterboystocks Something seems to be off with value line's bargain basement stocks screen. Their price to net working capital seems to be including issues with very high numbers. P/B's are low, which makes sense

The latest @FortuneMagazine data confirms a major shift in corporate America.

Texas is now home to MORE Fortune 500 companies than California.

Lower-tax, business-friendly states are attracting companies. Who would have thought?

Auction June 8-10 Current Bid $1 Industrial Warehouse

1015 West Jefferson Street Vandalia, Ilinois

26,947 SF Built 1951 0% Occupancy

-rimarketplace

#commercialrealestate