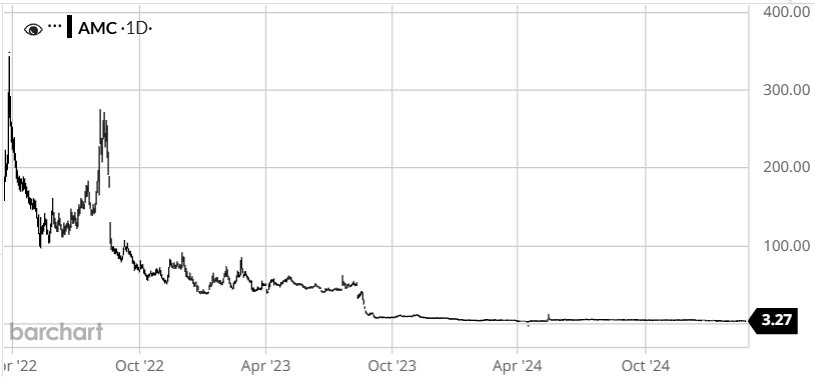

So amusing. Narrow-minded call our Hycroft investment… “stupid”…“idiotic.” AMC so understands how to raise cash and stretch out debt. Eric Sprott understands gold & silver. Add in a very low price for our shares/warrants. Tons of crow eating ahead, and it won’t be by me! #HaHa

$RAAQ

- warrants trading at $3.55 👀

- just upsized $10 PIPE to $146 million

- pro forma $2 billion EV = big discount to peers

- $QNT IPO this week good for sector

- downside protection to $10.41 NAV

- likely July close

- options coming?

Interesting from Wedbush:

“A successful Quantinuum debut would, in our view, validate the category rather than simply the single name,” Legault added. “We expect Quantinuum's valuation and early share-price action to set the tone in the first day or two of trading and to ripple across listed peers, particularly in light of the strong cross correlation of quantum asset prices.”

$QNT $IONQ $RGTI $INFQ $XNDU $RAAQ $BBCQ $AXIN

@spacanpanman In the last month, shorts got the Rakuten share sale pressure, the Blue Origin 2nd stage failure, the Q1 earnings sell off, and the New Glenn test explosion. What an incredible set of negative catalysts. At this point any shorts left are either hedging something or are idiots

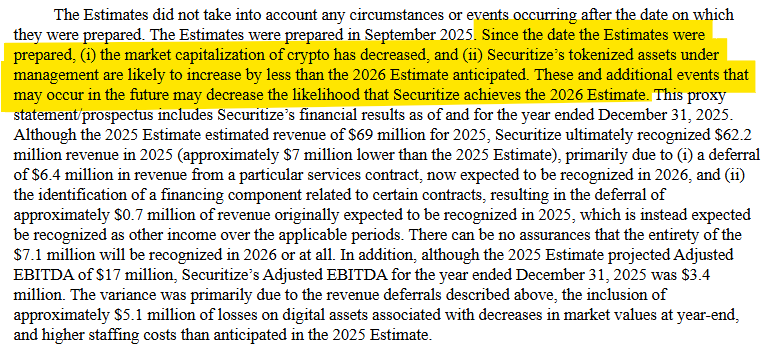

$CEPT filed an amended S-4 with full year '25 financials. Not great. Full-yr rev $62mn was a big miss vs. projected $69mn. Implies Q4 was $7mn vs. projected $13mn. Full-yr EBITDA $3mn vs. projected $17mn. Starting to walk back '26 projections. Abrupt loss of momentum does not match the narrative.

Starting to get excited about $CEPT. S-4 filed tonight shows 9 months rev +842% y/y to $56 million with 87.3% gross margin. Company is already EBITDA positive w/ $25 million YTD. And the YTD numbers imply the full year rev/EBITDA projections are sandbagged. Unless there is some weird seasonality that didn't exist last year, actual '25 rev and EBITDA should be well above the projected $69 million and $17 million. My guess is $85 million and $40 million.

Of the $110mn of projected '26 rev, $85 million is already on contract and recurring. Should be lots of upside in '26 also.

Aligned with a great theme, huge topline growth, 85-90% gross margins. $1.7bn pro forma EV looks pretty good to me. Think it will run.

https://t.co/aWxlYYaV7O

$ASTS, New Glenn launch failure yesterday was unfortunately very bad news for ASTS, potentially setting back the launch schedule by 6+ months and significantly increasing the cost of launching if you go by Kevin's expected scheduling and assume they are able to source some replacement launches:

> New Glenn pad damaged or destroyed, could take 6-18 months to rebuild depending on level of damage, see SpaceX prior pad destroyed and rebuilt in ~15 months (Falcon 9 SLC-40, Sept 2016 → Dec 2017).

> Blue Origin has no alternative pads available. LC-11 is at paperwork stage, Vandenberg SLC-14 is a greenfield with no construction commenced as of April 2026. Solving the failure root cause could also take some time but the long lead item is almost certainly pad replacement.

> Forces $ASTS to rely on SpaceX Falcon 9, currently fully booked on rideshare through end of 2027 and on dedicated manifests through 2028. ASTS would have to displace existing customers or wait. Falcon 9 list price c.$74m per launch and carries 3 BlueBirds per Kevin's schedule, vs New Glenn at c.$68m per launch carrying 4 and then 6 (long term targeting 8). Substituting F9 for the seven planned NG launches (Jul 26 — Feb 27) would roughly double the launch bill for that portion of the constellation deployment.

> Alternative options exist in Vulcan, but they've only flown twice in the last 12 months (USSF-106, USSF-87), have an 80+ mission backlog (NSSL Phase 2 + Kuiper) and are effectively fully booked through 2027. ISRO can only carry 1 satellite and is very expensive.

> Neutron expected to come to market late 2026 (could be delayed) and Eclipse to market early 2027 (will probably be delayed). Neither is a near-term solution.

Could see some negative price action on $ASTS beyond the current 10% drop as a result. The bigger overhang is the timing risk to continuous coverage milestones and the MNO commercial ramp, every month of slip is a month of Starlink D2C running uncontested.

This is positive news for $RKLB and $FLY as Blue Origin is a major competitor in launch, and any forced re-manifesting onto Neutron/Eclipse later in the decade lands in their lap.

The Blue Origin failure is unequivocally bad for $ASTS. There is now zero chance of hitting the targeted 45 satellites in orbit this year. It is dead money for a while. (That said, for the record, I am willing to wait and won’t be selling the news.)