@Adonis_Stergiou They’ve grown those shade tobacco leaves here for years…some of the big fields are now massive Amazon warehouses but it’s cool to see the old barns with the leaves drying.

Today was the worst day on SPX this year, the worst day in 164 trading days, and the 2nd worst day in the past year. It was the 8th worst day in the past decade.

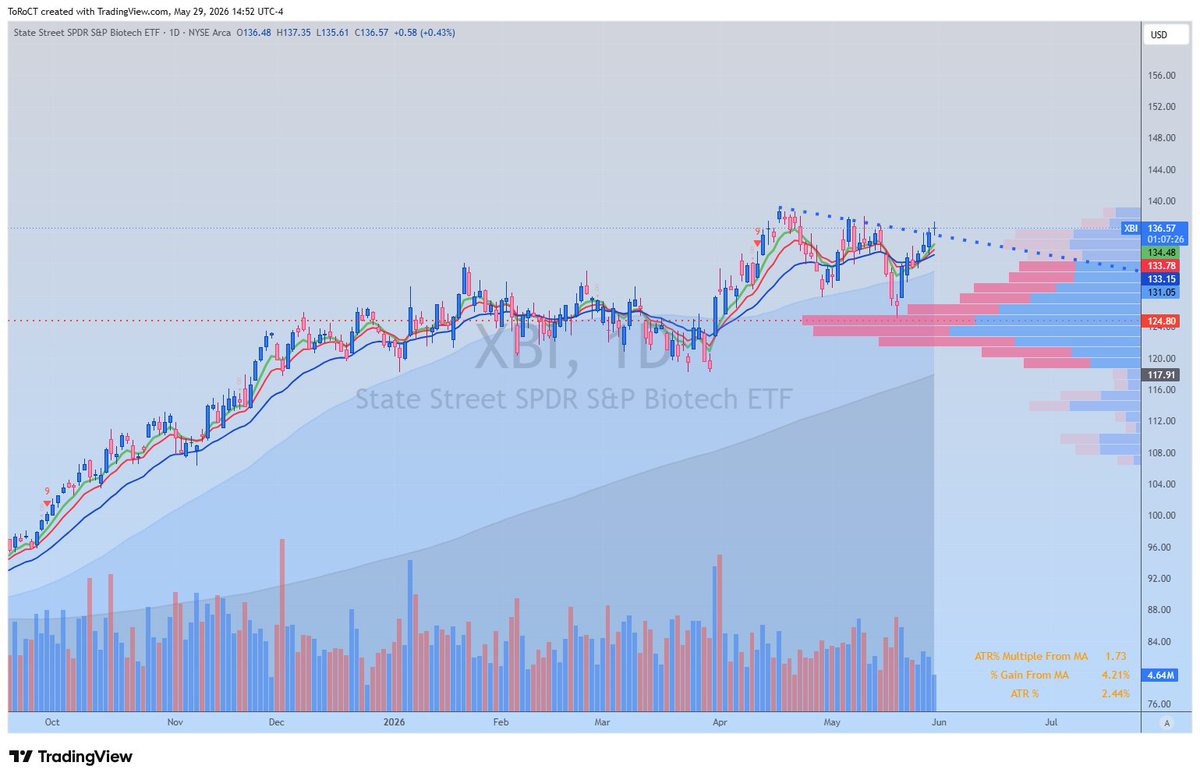

Quick update on the general market...

1. This is one of the more impressive lockout rallies I've seen, at least when looking at the Nasdaq.

2. Sentiment has remained very contained, almost impressively so and still very constructive.

3. Almost no distribution, and no meaningful distribution (heavy volume selling days where NYSE or Nasdaq close down >1%)

4. Breadth. While many are saying breadth is terrible it is pretty consistent with what we've seen over the last number of years, namely that the environment is more selective. NYSE A/D line looks like it wants to confirm upon a breakout and the NYSE Comp is tracing out a pretty nice consolidation.

Conclusion: 'Well, this is a bull market, you know!'

-Mr Partridge aka 'Old Turkey'

(Reminiscences of a Stock Operator)

Food for thought.

This is what super cycle looks like!

Dell’s earnings confirm a super cycle and the market is still mispricing its consequences.

The $ 8B revenue beat, the 25 per cent increase to full-year earnings guidance, and the 40 per cent surge in the share price are surface-level reactions.

The real signal is structural: customers are committing to 3, 4, and 5 yr AI infrastructure buildouts.

This is not a spending cycle. It is a capital regime shift.

Capital expenditure is no longer cyclical or discretionary. It is being locked in years ahead, redirected toward AI compute, storage, and networking, and secured through multi-year commitments. Dell’s backlog is not a cushion, it is a forward map of demand that has already been decided.

That is the mechanism of a supercycle. Demand is pulled forward, supply is constrained, and time collapses. What would have been sequential, phased investment is now concurrent and global. The buildout is happening everywhere, all at once.

This has direct implications for earnings. When capacity is pre-booked and utilization is structurally high, revenue visibility extends and operating leverage compounds. Margins expand not through efficiency, but through scarcity. The result is not incremental earnings growth, but step-change acceleration.

The market is still anchoring to a world where earnings mean-revert and multiples compress under higher rates. That framework no longer holds. A supercycle driven by productivity-enhancing infrastructure lifts both the numerator and the denominator: earnings expand while multiples re-rate to reflect durability and visibility.

Dell’s customers are making that case explicit. They are underwriting years of demand today because AI is not optional capex, it is core infrastructure.

That shift propagates through the entire stack: semiconductors, networking, power, and systems integration. It ultimately resolves at the index level.

S&P 500 earnings at $400 for 2027 are not optimistic. They are mechanical. The path to $600 is not speculative. It is already being contracted.

The market continues to treat AI as a theme. Dell’s order book shows it is an economic foundation.

Supercycles are only obvious in hindsight. This one is being booked in advance.

Ignore the noise. Doomers and MSM called the end of the cycle last September. They are living in a world that no longer exists.

Have a nice day.

i have my next trade idea for tomorrow and it’s gonna be a banger if it works

play small bc it’s a lotto but could pay huge

similar setup we traded in the past

i’ll tell you all about it one of these days

LAST DAY OF THE MONTH TOMORROW

STAY NIMBLE