Next Bridge Hydrocarbons Announces SEC Declares Effective its S-1 Registration Statement

Company prices and commences a public offering of 40 million shares

https://t.co/2hO7KuPeJJ

#MMTLP / #NBH Update: Interesting conversation with TD WebBroker yesterday. In the process of moving my remaining shares to AST, the representative mistakenly revealed that they are holding a single bulk certificate of 2+ million shares representing over 100 individual shareholders at TD.

They immediately realized they shouldn't have disclosed that structural info to a retail client. It clearly highlights the massive pooled "box certificates" brokers are sitting on and why forcing a manual extraction to AST takes weeks. Documenting everything...

$MMTLP

MMTLPfiasco Day 1261

Day 5 since @FINRA opened their trap after a 400+ day hiatus, now with a block on comments.😅

Unfortunately for them, we can still quote post that post. This is 100% social media advice.

You should consider doing that.

They have one of three options:

1) They could lock down their account, preventing RPs.

This is unlikely because then seniors wouldn't be able to see their content about how to avoid frauds and scams.

So you know they won't opt for that.🤡😎

2) They start blocking people.

I highly doubt they would go that far. It's easier to just remove comments, and you know the moment FINRA pulls that trigger, they'll never hear the end of it.

3) My favourite -- They accept their fate, (That one is for a special someone who thinks you spell ACCEPT, E-X-C-E-P-T.🐕🦺) and face public scrutiny for destroying the lives of hundreds of thousands of families -- The MMTLPARMY.

The #1A owns you.

Welcome back to the town square, MFers!

🚨Breaking news: 🦋

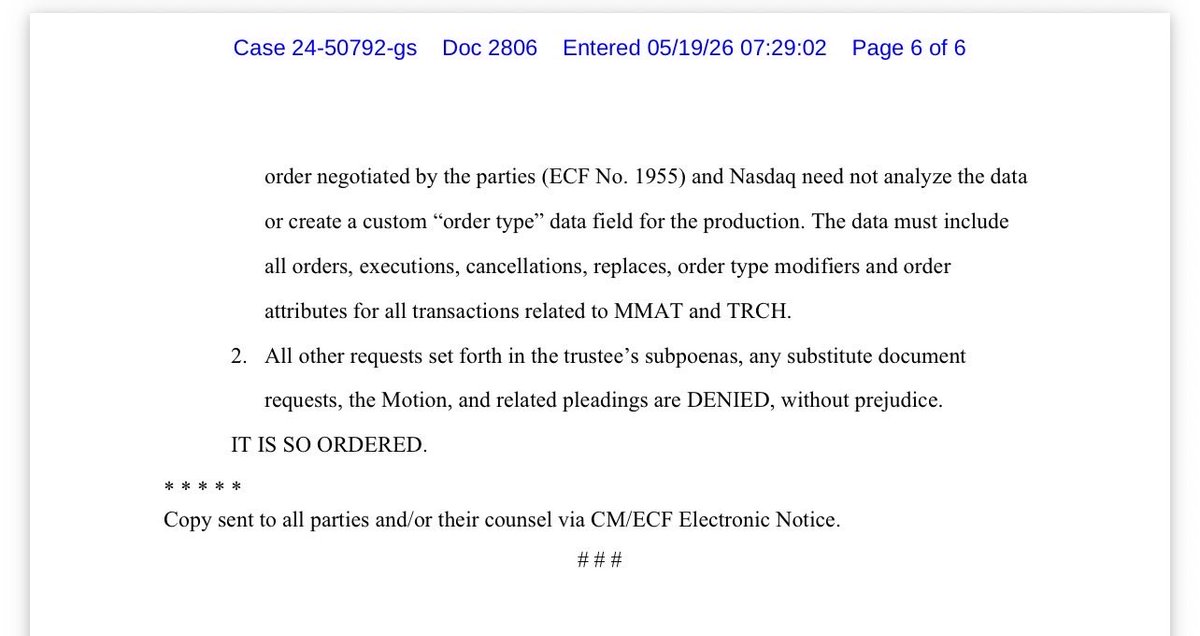

@Nasdaq just LOST its Motion to Quash.

Read that again s l o w l y . . .

The Bankruptcy Court in Nevada has now ordered Nasdaq to produce extensive $MMAT/TRCH trading data under Rule 2004, including RASH and CORE data, order attributes, cancellations, replaces, executions, and related transaction records covering nearly FOUR YEARS.

The Court was NOT persuaded by the ‘undue burden’ argument, noting that producing ~15GB of spreadsheet data is not exactly impossible for… Nasdaq. (One $10 usb stick)

Even more important, the Court explicitly recognized the Trustee’s AUTHORITY to investigate whether wrongdoing occurred on behalf of the estate, including potential claims tied to stock trading activity.

Translation:

This investigation is very much ALIVE.

For months, some people mocked and undermined the Trustee’s efforts, claimed discovery would never happen, and acted like every subpoena didn’t get served initially and that it would be crushed before daylight. Instead, the wall keeps cracking.

FINRA discovery.

Now Nasdaq discovery.

And the Court explicitly referenced separate pending motions involving Citadel, Virtu, and Anson.

Interesting times ahead.

Turns out Rule 2004 is not just a decorative suggestion.

To the Trustee and legal teams, incredible respect.

It takes courage to walk into rooms filled with institutions that have virtually unlimited resources and say:

‘Produce the data’

And to the echo chambers already warming up their spin machines tonight…

You may want to read the actual order first. 🤝

Blessings to all.

@udontknowjack99 Just want to say thank you to everyone of you relentless MMTLP warriors who keep fighting for justice for over 3 years! Things seem to be heating up 🔥🔥🔥 LFG!

The $MMAT trustee isn’t messing around

“…These filings look like the trustee broadening the financial investigation from market/trading discovery into the company’s banking records.

Translation:

The trustee isn’t just asking “What happened in the market?” anymore. She’s also asking “What happened to the company’s money?” 💸 ❓…”

- @kimkep4796

Former Meta Materials CEO George Palikaras knows too much… and refuses to go away quietly.

He knows the truth - and he’s proven he can’t be bought

That’s a big problem for regulators.

“..I had a choice.

I could have taken the Board’s severance offer, roughly $700K, signed a two-year gag order, sold my shares ahead of the 100:1 reverse split, and walked away quietly with a few million in hand.

That would have been the easy path.

But I chose not to take it. And so did my family and my other co-founders Paul and Themos.

For me, integrity is not for sale. It never has been, and it never will be….”

- @palikaras

TRCH MMAT MMTLP

Thinking back to 2023, from the day I was removed in mid-October to the December AGM vote, the company went through two CEOs, lost over 70% of its market value, and saw major contracts and deals either collapse or stall.

No business plan. No strategy shared.

Instead, highly dilutive capital was raised from sources that many in the market would recognize immediately as bad actors, despite multiple better alternatives being available.

I stayed publicly silent during that period. But privately, I was actively engaging, providing feedback, and making recommendations directly to the company.

At the same time, the Board, clearly in panic mode, made their position very clear to me.

I had a choice.

I could have taken the Board’s severance offer, roughly $700K, signed a two-year gag order, sold my shares ahead of the 100:1 reverse split, and walked away quietly with a few million in hand.

That would have been the easy path.

But I chose not to take it. And so did my family and my other co-founders Paul and Themos.

For me, integrity is not for sale. It never has been, and it never will be.

Others can decide what theirs is worth. $650K, $100K…or less. They know who they are starting with Mrs Spears.

For the record, at the 2023 time going into 2024 I was represented by three law firms across Nevada, Canada, and Nova Scotia, all paid personally, not by shareholders. Multiple demand letters were sent to address false statements and omissions. That is documented and in the trustees hands.

Also for the record, I have no NDA with the Trustee or any shareholder. I am not aligned to anyone’s agenda. I speak independently, and I act based on what I believe moves the truth forward. I am also a recognized creditor in the estate not trying to become one after the fact.

Had I taken the Board’s deal, this community would likely have received little to no information, and matters with the SEC could have been very quietly resolved.

Instead, I chose to fight for myself and for those who believe in me, because the underlying facts conflict with the narratives being pushed.

I am now building software designed to expose market structure and “plumbing” failures in cases like MMAT/MMTLP, so that what happened here does not happen to others again.

In the meantime, as both a major shareholder and a creditor, I would ask that those without standing stop consuming estate resources unnecessarily. If there are other motivations at play, it would be more honest to disclose them before they get revealed in a court of law.

And if the noise continues, people should start asking a very SIMPLE question:

who benefits from the DELAYS, and who is being paid to create them?

Integrity doesn’t get louder under pressure. It gets clearer.

My son turned 9 yesterday, thank you for all those who send wishes, have a blessed weekend, Monday is a big day and I may go live tomorrow to share some thoughts on the next few weeks ahead.

Latest $GNS news - The 30.1 Million Shares from the Company’s ERL Share Count Exercise and ICC Arbitration Win is equivalent to 25.8% of the Company’s Public Float.

SINGAPORE, April 23, 2026 (GLOBE NEWSWIRE) -- Genius Group Limited (NYSE American: GNS) (“Genius Group” or the “Company”), a leading AI-powered education group, today announced that further to completion of its ERL Share Count Exercise and the Company’s recently announced ICC Arbitration Win, it has identified a combined 30.1 million shares of Company common stock that it plans to move into trust or treasury, with the intention to permanently retire and remove them from its public float.

All 30.1 million shares are currently held by its transfer agent, VStock Transfer LLC (“VStock”).

The 30.1 million shares comprise 17.3 million unclaimed shares from the Company’s Asset Purchase Agreement with Entrepreneur Resorts Ltd (“ERL”) currently held at VStock, 5.5 million GNS shares payable to Genius Group for its prior shareholding in ERL to be returned to the Company’s treasury, and 7.4 million shares awarded to the Company by the International Chamber of Commerce (“ICC”) in its arbitration proceeding against LZG International, Inc, to be released from Vstock to the Company’s treasury pending final agreement between parties or court order.

The Company intends to retire and remove the 30.1 Million Shares from the Company’s public float, with the intention to eventually move all shares to treasury and subsequently to be cancelled as soon as practical, which will result in significantly reducing the Company’s public float and total shares outstanding, benefiting existing shareholders.

Whilst the final amount to be retired and removed may change, based on whether any further claimants of unclaimed ERL shares are identified or whether the shares from the ICC arbitration win are subject to appeal by opposing parties and remain in escrow until resolved, the Company currently believes any future change to this number will not be material.

Excluding the 30.1 million abovementioned shares and excluding 30.4 million shares owned by insiders and held as restricted book entry form at VStock, and including the shares issued pursuant to the investment led by American Ventures LLC on April 16, 2026, the Company’s remaining Public Float is 116.7 million shares.

The 30.1 million shares is equivalent to 25.8% of the Company’s public float.

Roger James Hamilton, Founder and CEO of Genius Group, commented “The completion of our ERL Share Count Exercise and our ICC arbitration win represent significant milestones in our ongoing efforts to protect shareholder interests and strengthen our share structure. Our plan to retire and remove these 30.1 million shares will meaningfully reduce our total shares outstanding and public float, for the benefit of our shareholders.”

Full PR - https://t.co/FrnxAsLtqf

@annvandersteel@TheRobbCarter If the media and experts were to look at this objectively the Headline tomorrow would be something like this:

"Unprecedented: Judge Denies FINRA Motion to Quash, Grants MMAT Trustee Rule 2004 Access to TRF Data"

To the best of my knowledge (plz correct me if i am wrong) THIS is the FIRST and only time in FINRA's history where ANY company, person or organisation have been granted 2004 (broad) access to TRF data.

Key Aspects of FINRA's TRF Data:

1. Reporting Mechanism: TRFs allow broker-dealers to report trades, typically within 10 SECONDS of execution, for equity securities. EVERY one... has so far been working off 5min data.

to explain the significance of 10sec vs 5min in a market‑microstructure or litigation context:

- Any path‑dependent metric (slippage, realized spread, adverse selection, queue dynamics, spoofing patterns) is fundamentally tied to HIGH‑frequency data.

example1 : “The market was distorted over this 30‑minute interval; VWAP was pulled away from fundamentals” → 10‑sec window is often more than enough to show patterns.

example 2: “This market maker placed and canceled orders in a way that spoofed the market at the millisecond level” → 10‑sec is not enough... you need order‑level data... seems like a dead end?? NO PROBLEM...

The path: from 10 sec to ms is achievable for the Trustee.

Step 1 – the 10‑second TRF data:

- Show an anomaly or pattern that should not exist under normal trading.

- Example: price/volume bursts, repeated ramps and fades, abnormal VWAP slippage, or patterns that line up suspiciously with specific counterparties or news windows.

- This would be good cause / proportionality basis for the Trustee: something is off in a way that can be seen even at coarse resolution.

Step 2 – Millisecond / order‑level data:

- The trustee at this step would be compelled by their findings to argue that to understand how the anomaly happened, and who did what, you need the higher‑resolution record (full order book, message timestamps).

- This is standard digital‑forensics logic: coarse timestamps show a suspicious interval; fine timestamps reconstruct the actual event sequence.

So 10‑second data is the screening and prima facie evidence. Millisecond or order‑level data is the mechanism and attribution evidence.

In 2004, the exchange / broker’s systems already recorded events with sub‑second resolution internally (for matching, risk, and audit), even if what was sold to clients later as historical data was coarser.

Today, forensic practice recognizes that higher timestamp resolution is necessary to determine execution order and causality when multiple events occur inside a single second.

Once the Trustee discovers that “something non‑random is happening” at 10‑second resolution, it becomes PROPORTIONATE to request the finer‑grained logs that can clarify sequence and intent.

In other words: you are not asking for a fishing expedition; you are asking for the obvious next layer of the same record after you have located the suspicious windows.

Oh no!... i predict some bad actors at this very moment are getting very sweaty...

Active TRFs:

There are three active TRFs operated in partnership with exchanges:

1. FINRA/Nasdaq TRF Carteret,

2. FINRA/Nasdaq TRF Chicago, and F

3. INRA/NYSE TRF.

OTC Transparency Data: FINRA publishes OTC trading information on a delayed basis for ATS and member firms with reporting obligations.

Daily Short Sale Volume Files: These files provide aggregated volume by security for short sale trades reported to a TRF, with daily files released for each facility by 6:00 PM ET.

Did you know? Vendor Information: Organizations wanting real-time TRACE data must enter a Vendor Agreement with FINRA... aka the gag order?

SO... as you can now appreciate based on the above...

The Undisputable Winner is.... The Trustee

Based on the court's rulings, the trustee (Mr Burnett) is the clear big winner on this day.

Why the Trustee Won

Granted Requests (3 out of 9):

- Short interest reporting data

- TRF (Trade Reporting Facility) data - the most critical and burdensome request

- Daily short sale volume report data

BUT ALSO...Conditionally Granted (2 out of 9):

- OTC summary report data (Requests 4 & 5) - pending sequencing

That's 5 out of 9 requests granted - the trustee got the core data it needed for its investigation...

A reminder: that the Trustee has already 9 out of 9 wins on sending subpoenas, with every opposing party that tried to take the case away from Nevada (e.g. FINRA in DC, Nasdaq in NYC) all getting defeated again and again and returning back.

Why the TRF Data Victory matters:

- If you go and read the docket all responses from the start, this was the most hotly CONTESTED request.

- FINRA claimed it would take weeks/months and cost hundreds of thousands of dollars.

- The judge said: produce it anyway, and the trustee will pay for it. This is huge for the trustee's investigation.

Judge's Tone - The judge was clearly frustrated with FINRA's approach and sympathetic to the trustee's position.

Advantage - The judge rejected FINRA's broader claims about investigative privilege and work product for the data requests, finding those protections apply mainly to DOCUMENTS (Requests 6-8), not DATA (keep this in mind for future reference).

The Judge made it clear he expects FINRA to cooperate in good faith going forward and warned against stall tactics

FINRA's Losses:

FINRA only won on Requests 6, 7, 8, and 9 (documents and CAT data) - the items it was most protective of anyway, and the trustee seems to not really care about it given the triangulation strategy they seem to be on... but the trustee's core investigative needs were GRANTED.

Do you agree with my analysis and opinion above? Would love to hear your feedback, edits, corrections etc...

In you made it this far (thank you for your patience)... next is the key turning point in today's call that caught FINRA by surprise... stand by. #MMAT #MMTLP

BREAKING NEWS 🚨

Judge's Motions to Quash Decisions in April 20th 2026 Hearing... lets start with the facts

Impotant Note to remember: this is a Preliminary Investigation Phase...

(Disclaimer these are my notes, the pending final transcripts will reveal and support my findings, and I expect the community to accept, scrutinize or suggest edits if anything is innacurate)

Based on the court ruling, here are the judge's decisions on each of the nine requests in FINRA's motion to quash:

FINRA DENIED (Trustee Prevails):

Request 1 - Short Interest Reporting Data:

- Court will deny the motion to quash.

- FINRA agreed this data could probably be produced

- Judge noted discussion about duration (4 years vs. shorter period) needs clarification but denied the motion

Request 2 - Trade Reporting Facility (TRF) Data:

- Court will deny the motion to quash

- Despite FINRA's claims of significant burden (25 million items), judge found it not "unduly burdensome" under Rule 45

- Trustee to bear costs of production

- Judge emphasized need for good faith meet and confer on scope, timing, and cost-shifting

Request 3 - Daily Short Sale Volume Report (Reg SHO)

- Court will deny the motion to quash

- Falls between short interest data (easier) and TRF data (more burdensome)

- Consistent with prior ruling on TRF data

GRANTED (FINRA Prevails)

Requests 6 & 7 - FINRA Investigation Records and Public Communications

- Court will grant the motion to quash

- Judge found this seeks litigation-style discovery under Federal Rules, not preliminary Rule 2004 information

- Rife with attorney-client privilege, work-product privilege, and investigative file privilege

Would provide strategic advantage at PRELIMINARY stage (Note: again emphasis on the word -> "preliminary" hence no guarantees to block CAT for later...?)

Request 8 - FINRA Electronically Stored Communications (Emails)

- Court will grant the motion to quash

- Falls on "document side" rather than "data side" of the dichotomy

- Unduly burdensome and inappropriate under Rule 2004

- Seeks litigation-style discovery rather than preliminary information

Request 9 - Order Quotations and Execution Records (CAT Data)

- Court will grant the motion to quash

- Judge found that information in Requests 1-3 effectively provides same information

- Mirrors motion to compel-style discovery rather than preliminary investigation

- Represents strategic advantage seeking under Rule 2004

There was an interesting section where the Judge then discussed CONDITIONAL/SEQUENCED items:

- Requests 4 & 5 - Monthly and Weekly OTC Summary

Report Data:

Court will deny the motion to quash (conditionally)

Judge noted these are "not necessarily critical" per trustee's own admission and proposed sequencing:

- produce Requests 1-3 first, then reassess 4-5

- if computer-generated reports: deny motion to quash

- If laborious/individualized: requires further detail to determine if burden is "undue"

- Trustee to bear costs (they seems happy to do so)

The judge ordered:

1. David Burnett to draft a proposed order reflecting the ruling for FINRA's review.

2. Good faith meet and confer on TRF data (Request 2) regarding scope, burden, timing, and cost-shifting

3. Parties to leave past disagreements behind and work cooperatively

4. One-paragraph summary of the 161-day data period requested for other Rule 2004 productions to be provided to court for clarity... My opinion is that once the judge gets this report he should have enough to not need any additional hearings and Citadel, Virtu and all others will get their answers too.

did i miss anything? comment below⬇️

Next i will post my observations and interesting things I saw... and in my opinion what was the turning point in the hearing today that caught FINRA completely off guard and send their counsel in panic mode, judging from the body language!

Drumroll please... Loading my report within the hour with a FACT-based analysis on today's major court rule 2004 decisions and what was the key turning point in my opinion... stand by.

After over a year by FINRA and others playing hide and seek shamelessly with the a United States Trustee, their time is finally up. #MMAT #MMTLP #Discovery #Rule2004

Major Update: $MMAT & $MMTLP Legal Developments

In my opinion, this is a massive win for the community. Here is the breakdown of the court's recent decisions regarding FINRA’s motions to quash and the difference between the two types of trading data involved:

1. FINRA’s Motion to Quash: DENIED

Data Source: TRF (Trade Reporting Facility)

• The Focus: Transaction-level data.

• The Purpose: Used for regulatory transparency and clearing.

• The Scope: Identifies the executing and contra-side broker-dealers.

• Note: This data does not reveal the end customer, but it is a critical step for transparency.

2. FINRA’s Motion to Quash: GRANTED

Data Source: CAT (Consolidated Audit Trail)

• The Focus: Specific customer-level identifiers.

• The Purpose: Connects trades directly to the specific individuals or entities that placed them.

• The Scope: Requires detailed information on allocations and representative orders.

The Bottom Line: While the CAT data remains protected for now, gaining access to the TRF data is a significant step forward in uncovering the mechanics of these trades.

What are your thoughts on this outcome? Comment below!