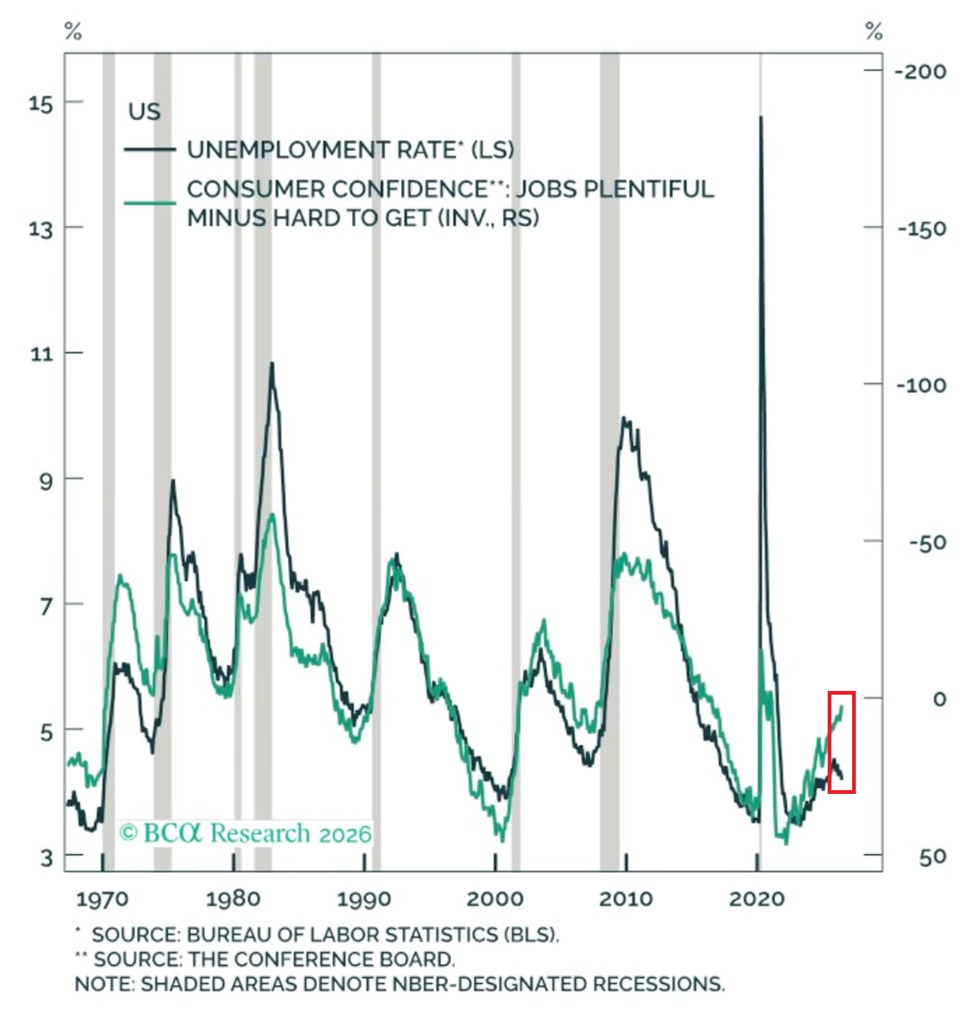

US consumer sentiment points to further job market weakness:

The gap between consumers saying jobs are "plentiful" versus "hard to find" fell to just 2.4 points in June, the lowest since the 2020 pandemic.

Just 24.9% of consumers now say jobs are "plentiful," down from ~55.0% in 2022, while 22.5% say jobs are "hard to find," up from ~10.0% over the same period, and the highest since January 2021.

Historically, this measure has been one of the most reliable leading indicators of rising unemployment, and it now suggests the US unemployment rate could rise to as high as 6.0%, from the current 4.2%.

Meanwhile, the labor force participation rate, which measures the working-age population of those either employed or looking for a job, fell to 61.5% in June, the lowest since June 1976, excluding the pandemic period.

This comes as the labor force dropped -720,000 last month, to 169.36 million, the lowest since December 2024.

The job market is much weaker than headlines suggest.

Alan Greenspan, former Fed chairman, dies at age 100.

The year he was born Calvin Coolidge was President.

US population was 117 million.

A Ford T model cost $300.

Mussolini was ruling Italy.

Stalin consolidating power.

Lots changed.

May he rest in peace.

BREAKING: Venezuela’s crude oil exports have surged +61% YoY, to 1.25 million barrels per day, the highest in 7 years.

The surge was led by rising shipments to the US at ~558,000 barrels per day, India at ~427,000 barrels per day, and Europe at ~169,000 barrels per day.

In total, 67 cargoes were exported from Venezuelan ports in May.

Since November 2025, Venezuela’s oil exports have surged +150%, or ~750,000 barrels,

This comes as the US eased sanctions on Venezuela's oil industry following the capture of Maduro earlier this year.

Venezuela's oil ministry is now targeting output of 1.37 million barrels per day by year-end, which would mark a +22% increase from 2025 levels and the highest since US sanctions were first imposed in 2019.

Venezuelan oil is increasingly flowing into global markets.

Americans are defaulting on their student loan debt at a record pace:

Delinquent federal student loan debt jumped +$12.2 billion in Q1 2026, to $171.4 billion, an all-time high.

This has officially surpassed the $166.8 billion peak recorded in Q4 2019.

At the same time, the proportion of seriously delinquent loans rose +0.7 percentage points, to 10.3%, the highest since Q1 2020.

This comes as 2.6 million borrowers defaulted in Q1 2026, followed by ~1.0 million in Q4 2025.

The average borrower entering default is now nearly 40 years old, up from 36.4 before the 2020 pandemic.

The US student loan crisis is intensifying.

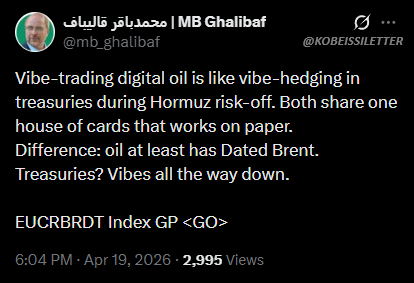

BREAKING: Iran's Speaker of the Parliament Ghalibaf comments on "vibe trading digital oil" after Iran shuts down the Strait of Hormuz.

"Vibe-trading digital oil is like vibe-hedging in treasuries during Hormuz risk-off. Both share one house of cards that works on paper. Difference: oil at least has Dated Brent. Treasuries? Vibes all the way down," he says.

US trucking costs are rapidly rising:

The per-mile cost to hire a truck to move goods is up to $2.97 per mile, the highest since June 2022.

At the same time, the dry-van rate, the most common truck type used for general freight like retail and packaged goods, is up to $2.50 per mile, the highest since May 2022.

Both rates have risen roughly +30% since September 2025.

This comes as diesel prices have spiked nearly +50% since the start of the Iran war, forcing haulers to raise weekly per-mile fuel surcharges.

Meanwhile, truck transportation payrolls are down to 1.46 million, the lowest since September 2020, which was already tightening the supply of available drivers and pushing rates higher even before the war.

Fewer drivers and surging fuel costs are now being passed directly to shippers, raising inflation pressures across the economy.

Inflation will soon follow.

BREAKING: The S&P 500 officially falls below 6,400 for the first time since September 2025.

This puts the S&P 500 just 90 points away from entering correction territory.

BREAKING: Institutional investors sold -$11.0 billion of US equities last week, the largest weekly sale in 5 weeks.

This comes after 3 consecutive weekly purchases totaling +$12.6 billion.

At the same time, hedge funds bought +$1.8 billion worth of US equities, following 4 straight weeks of sales.

Meanwhile, retail investors sold -$80 million, posting just their 3rd weekly sale over the last 10.

In total, US equities recorded -$9.3 billion in outflows last week, up from -$1.0 billion the prior week, bringing the 16-week total to -$25.5 billion.

This was primarily driven by single stocks, which saw -$8.3 billion in outflows, the 4th-largest since 2008, while ETFs posted -$1.1 billion in withdrawals, the most in 6 months.

Institutional investors are moving to the sidelines.

BREAKING: The US and Israel have now struck ~15,000 targets in Iran since the war began on February 28th, per WSJ.

War details include:

1. ~50,000 American servicemembers have now been sent Middle East to support the operation

2. US and Israel have conducted 11,500 combat flights

3. The US has destroyed more than 100 Iranian naval vessels

4. Total US cost of Iran War is nearing $25 billion, or $11,500/second

5. Average US gas price is now up +40% since December

We are now on day 19 of the Iran War.

Apple has introduced the new AirPods Max 2

- Same design

- H2 chip

- 1.5x better ANC

- New high dynamic range amplifier

- Conversation Awareness and Voice Isolation

- Adaptive Audio and Live Translation

- Same colors

- $549 price

Order on March 25. Available early next month

BREAKING: President Trump is reviewing a "set of options" to lower oil prices as soon as today amid their historic surge, per Reuters.

Details include:

1. Options include restricting US exports, intervening in oil futures markets, and waiving some federal taxes

2. Trump could also lift requirements under the Jones Act, which says domestic fuel must move only on US-flagged ships

3. The White House is "worried" that the surge in oil prices will hurt US businesses and consumers

4. Trump is reportedly considering the mid-term election implications of higher oil prices

US oil prices are now below $95/barrel.

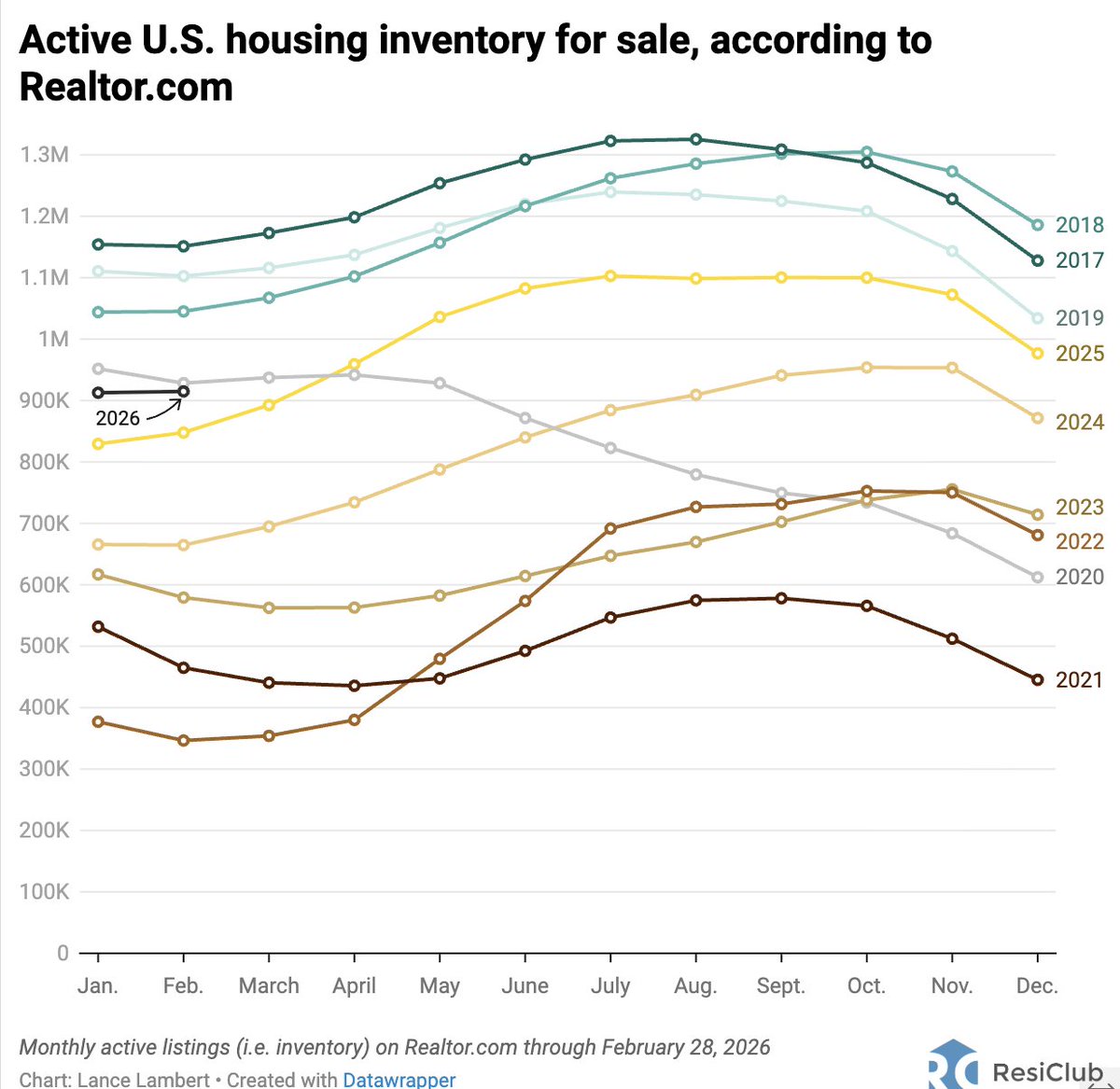

Active inventory for sale (through end of February)

Feb 2017 -> 1,151,120

Feb 2018 -> 1,045,153

Feb 2019 -> 1,102,660

Feb 2020 -> 928,343

Feb 2021 -> 464,919

Feb 2022 -> 346,511

Feb 2023 -> 579,264

Feb 2024 -> 664,716

Feb 2025 -> 847,825

Feb 2026 -> 914,860

The AI boom is fueling the South Korean economy:

South Korea exports surged +47% YoY in the first 20 days of February, the strongest reading in at least 2 years.

This follows a +34% gain in January, marking the 2nd consecutive monthly acceleration in growth.

These figures also came despite fewer working days due to the 3-day Lunar New Year holiday falling within the reporting period.

The surge was driven by semiconductor exports that soared +134% YoY, fueled by AI and data center investment demand.

Furthermore, shipments of computer peripherals and petrochemical products jumped +129% and +11%.

Exports to Taiwan and China rose +76% and +31%, and shipments to the US increased +22%.

South Korea is seeing massive economic growth.

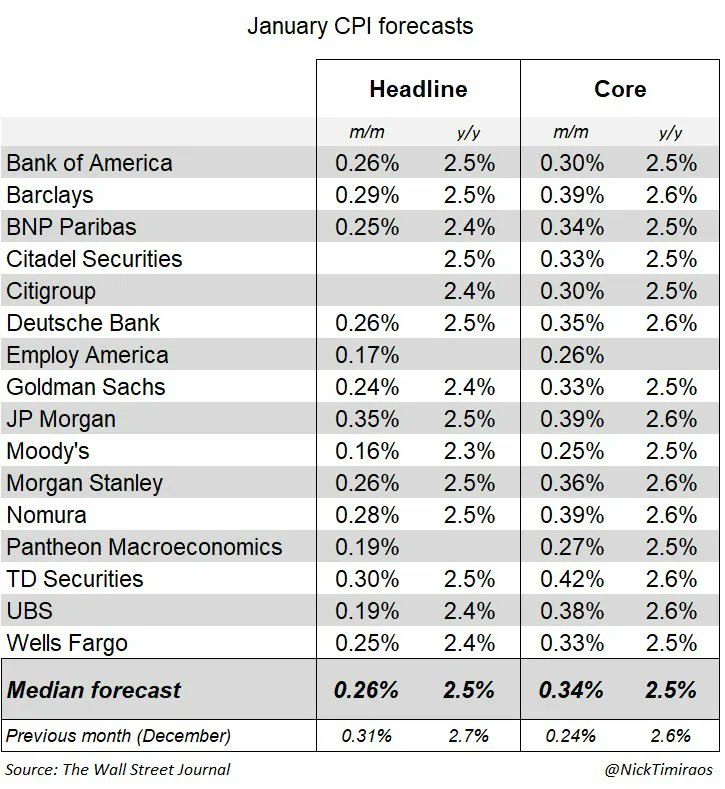

Official US inflation for January cooled below market expectations.

US CPI was 2.4% Y/Y, down from the previous 2.7% and lower than the market consensus of 2.5%.

US Core CPI 2.5% Y/Y, down from 2.6% and aligned with market expectations.

Meanwhile, Truflation's custom US CPI was 0.72% Y/Y today, and we've seen inflation dropping below 2% in January and below 1% in February.

Based on our data, we correctly predicted that the US BLS CPI would come in cooler than expected today, between 2.2% and 2.4%. For January CPI reports, we typically provide a range forecast rather than a single number because the BLS adjusts its data weights for the year ahead.

Worth noting that in categories where the BLS still sees elevated inflation: food at 3.1%, utility costs 10.8%, and shelter 3.2%, we already see significant and often persistent cooling, with food and housing categories already entering a slight deflation.

US CPI today, according to our independent price data, is 0.72% Y/Y.

The latest US CPI report for December was 2.7%.

In 1h, the BLS will release its official US CPI (US headline inflation) for January and the revised weights it will use for 2026.

Market predictions for this read range from 2.3% to 2.7%, with the majority between 2.4% and 2.5%

Extrapolating our data to BLS CPI trends, we estimate today's number to be between 2.2% and 2.4%, and we hope the BLS will catch up with the real price trends.

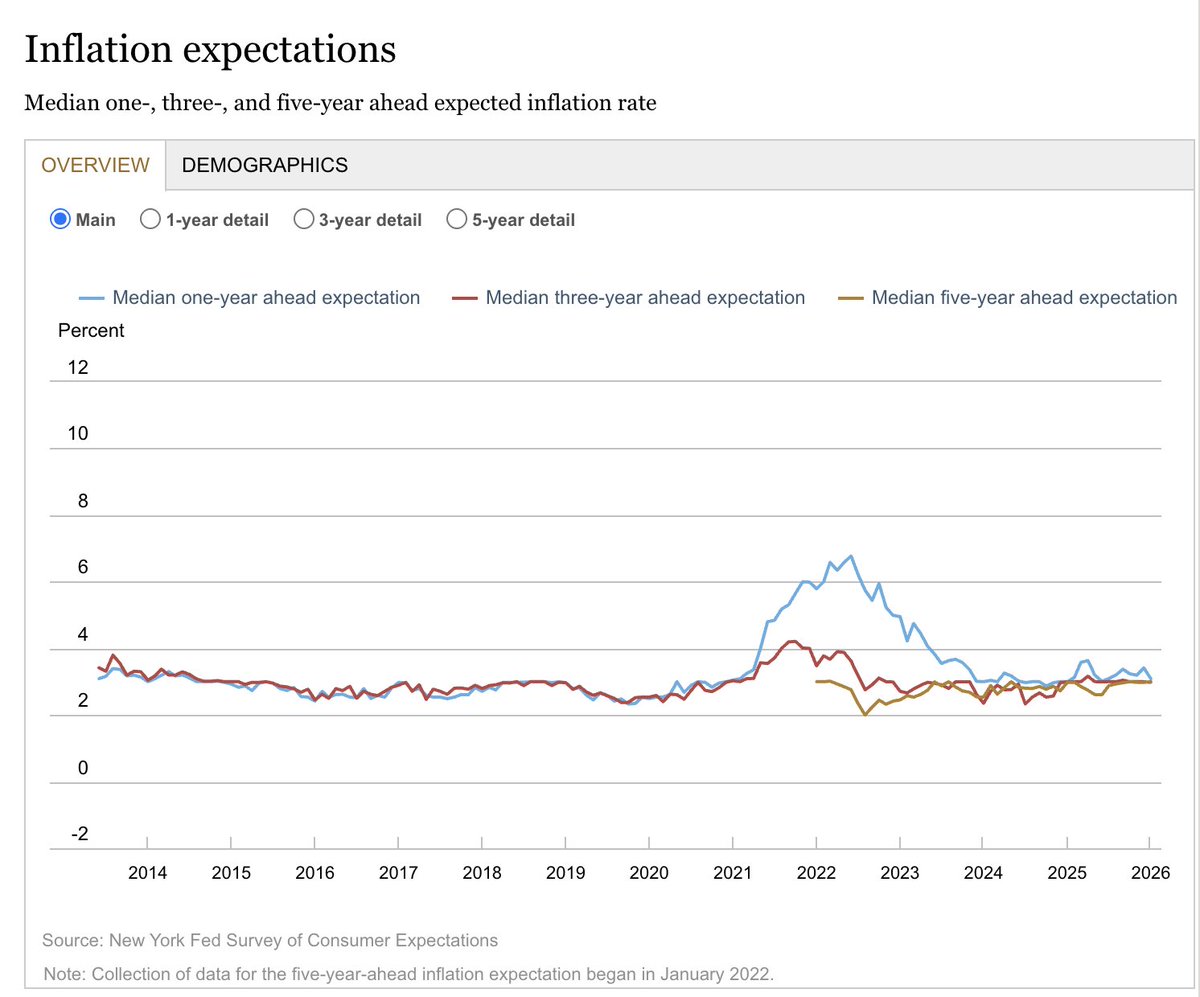

Short-term inflation expectations eased to 3.1% (down 0.3), according to the NY Fed survey.

The 3Y & 5Y inflation expectations stay anchored at 3.0%.

Earnings expectations rose to 2.7% (up 0.2), esp. among lower-income households.

Expectations of job loss dipped by 0.4 to 14.8% while job-finding confidence rose by 2.5 to 45.6%.

However, both currently perceived and 1Y-ahead financial situation expectations deteriorated.

Historically, inflation expectations have been well correlated with real inflation and can be taken as an early gauge of changing inflation trends, suggesting some short-term cooling we also see in our data.

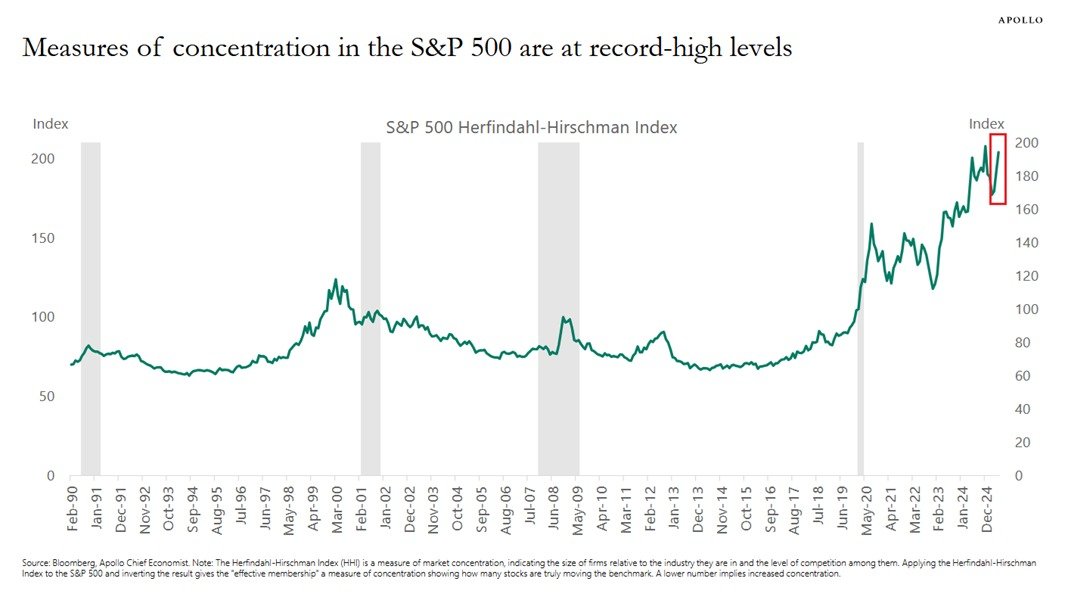

US stock market concentration is at record levels:

The S&P 500 Herfindahl-Hirschman Index (HHI) is up to 195 points, near the highest on record.

This metric measures how evenly market value is distributed across all 500 stocks in the index.

A higher number indicates increased concentration, meaning fewer stocks are driving market performance.

This index has more than DOUBLED since the 2020 pandemic.

By comparison, the HHI index peaked at 125 points during the 2000 Dot-Com Bubble.

The market has never been this top-heavy.

US Q3 2025 GDP signalling the highest growth in 2 years.

Q3 2025 GDP was revised by +0.1% from 4.3% to 4.4% annualized.

Growth estimate was driven by increased consumer spending, exports, government spending & investment. Also, imports, which are subtracted from the calculation of GDP, decreased.

Stronger GDP growth and cooling inflation (as we see in our data) might suggest rising economic resilience. Do you think BEA got this data right?