US CANNABIS: the 2 weeks that could re-rate the sector.

In 14 days the DEA opens its hearing on moving ALL marijuana — incl. adult-use — to Schedule III. The medical half already moved in April.

The setup into June 29 🧵

#MSOS#MSOGang#CannabisStocks#Rescheduling

🗓️ WEEK AHEAD:

• Jun 29 DEA hearing on broad Schedule III

• Any D.C. Circuit stay ruling

• More uplistings ($GTBIF $CURLF)

• Hemp ban clock → Nov 12

🟢 Green Terminal soon. Not investment advice.

🇺🇸 Trump nominated Todd Blanche — architect of April's Schedule III order that killed 280E for medical operators — for permanent AG. Continuity intact.

📈 $MSOS hit a 2026 high (~$5.75), then -4.5% to $5.49. +103.7% 1-yr vs S&P +29.8%.

🟢 US CANNABIS — WEEKLY WRAP (Jun 8–12) 🧵

The week the sector grew up: the first US operator hit the NYSE, a bank started lending, and $MSOS tagged a 2026 high.

Wrap + week ahead 👇

🟢 US CANNABIS — WEEKLY WRAP & WEEK AHEAD (Jun 8–12)

The week the sector grew up: the first US operator rang the NYSE bell, a bank started lending, and $MSOS tagged a 2026 high.

What moved — and the catalysts that define the week ahead. 🧵

$3.5 trillion.

That’s combined AI infrastructure capex from five hyperscalers — MSFT, AMZN, GOOGL, META, ORCL — between 2026 and 2030.

And it still won’t be enough.

Three data points the consensus is mispricing about the AI Factory build-out:

1. The financing gap inside listed AI infrastructure is structural, not cyclical.

The top 5 listed AI/DC operators — $DLR, $EQIX, $CRWV, $NBIS, $IREN — face $124.7 Bn of 2027–28 capex needs against $13.6 Bn of cash.

That’s an $111 Bn financing gap inside the listed sector alone.

The valuation dispersion tells the story. Operators with REIT-grade financing (CRWV at 4.3x EV/Rev’27) trade at 7x.

The gap isn’t about quality. It’s about whose capital stack works.

2. AI Factory unit economics break every framework the market is using.

Industry-standard colocation: 5–10 kW/rack, ~50% EBITDA margins, enterprise leases.

AI Factory operators in the public market — see $CRWV’s 73–75% gross margins in recent quarterly disclosures — run structurally different unit economics than legacy DC operators.

Take-or-pay GPU contracts on 5–15 year terms convert variable software consumption into bankable infrastructure rent.

The unit economics aren’t priced through a Bloomberg colocation comp screen, and the cap-rate frameworks the market is using were built for a different asset class.

3. The binding constraint isn’t chips. It’s power.

NVIDIA can ship the silicon. Grids can’t deliver the megawatts.

That’s why pure-play AI Factories are being built where long-duration baseload power already exists — Nordic hydro, North African solar, Iberian renewables. Sub-$0.05/kWh 10-to-25-year PPAs are emerging as the binding constraint on capacity deployment.

Sovereign AI capacity is now defined by who can secure 100 MW of green baseload, not by who can buy GPUs.

Power is the moat. Most allocators are still pricing it as a commodity.

—

The structural answer is a three-leg architecture:

▸ REIT for the real-asset base — priced by infrastructure investors

▸ GPU-collateralised debt for the compute layer — priced by structured credit

▸ OpCo equity for the operating business — priced by growth equity

Each leg priced by the capital pool that actually understands it.

Today, most AI Factory deals are forcing one structure to do three jobs. Each leg gets mispriced because the wrong pool is underwriting it.

The structures are being built now. The valuations are still anchored to the wrong frameworks.

If you build, finance, operate, or allocate to AI Factories — let’s talk.

Compute is the new oil. The capital stack hasn’t caught up. Yet.

Sources: Omdia (hyperscaler capex), LK Green Capital analysis (financing gap, sector synthesis).

$AAWH Q1’26 — operational discipline while the sector compresses.

• Revenue $116.9M (–8.6% YoY, in-line)

• Adj gross profit $53.9M (+3.4% YoY on declining revenue)

• Adj gross margin 46.1% vs 42.0% est (+410 bps beat, +530 bps YoY)

• Adj EBITDA $26.3M (+10% vs Haywood), margin 22.5%

• 10 consecutive quarters of positive CFO; senior notes refinanced — 5-yr runway

The analytical insight the Street keeps under-pricing: the verticality dividend.

530 bps of structural gross margin expansion on a –8.6% top line.

That’s vertical integration manifesting in the P&L — not seasonal mix. As the 10-dispensary pipeline ramps (51 → 60+ stores by YE26), the margin floor compounds on a growing base.

The free option layered on top: Q1 booked $11.9M income tax expense on a $17.6M pre-tax loss — 280E in full display.

Medical cannabis is now Schedule III (DEA Final Order, April 23); adult-use rescheduling hearing this summer.

AAWH operates in 6 adult-use states (IL, MD, MA, MI, NJ, OH) plus medical PA. Management explicitly flagged the expected UTP reserve benefit.

Verticality is the standalone thesis — rescheduling is the kicker.

Watch items: wholesale –22.5% YoY, net debt $241.2M, $19.1M semi-annual coupon and a $17M arbitration settlement both absorbed in Q1.

Trades 5.1x ’27E EV/EBITDA vs Tier 2 peer median 5.6x.

Haywood target $1.00 (Buy) — ~79% upside from $0.56.

Not the headline grabber in cannabis this quarter. The compounding one.

#cannabis #MSOs #280E

$MRMD Q1’26 — operational discipline, refined for the post-April 23 rescheduling reality.

THE PRINT

• Revenue $39.5M (+4.2% YoY) — Wholesale +4.4%, Retail +4.8%

• Adj EBITDA $3.6M (+43% YoY), margin 9.1% vs 6.6%

• GAAP op income flipped positive: +$125K vs -$910K

• Gross margin -110 bps (38.7% vs 39.8%) — best-in-class vs MSO peers running -200 to -400 bps

OPERATING LEVERAGE

Revenue +4.2% → Adj EBITDA +43%. ~10x incremental margins.

• Bad debt: $76K vs $1,388K (cleanup done)

• Personnel -1.2%, Marketing -16% YoY

• Both channels growing — no channel cannibalization

THE 280E REAL OPTION — why April 23 matters

The DEA Final Order moved two narrow categories to Schedule III: FDA-approved marijuana products and state-licensed MEDICAL marijuana.

Adult-use stays Schedule I until the June 29 expedited hearing produces a broader rule.

For MRMD specifically:

• Medical revenue gets immediate 280E relief

• Adult-use (majority of mix) stays under 280E for now

• Tax accounting fragments: medical = deductible, adult-use = not

The Q1 numbers through this lens:

• $2.65M tax provision on a $1.1M pre-tax LOSS — annualized $10.6M of phantom 280E taxes

• $29.6M income taxes payable on the balance sheet, +$2.6M QoQ — accrued but deferred

• Acting AG Blanche explicitly “encouraged” Treasury to consider retrospective 280E relief for periods operators held state medical licenses — not granted, but the door is open

CATALYST PATH

1.June 29: expedited hearing on broader (adult-use) rescheduling begins

2.Broader final rule: timing uncertain, executive priority

3.IRS guidance on retrospective relief: asymmetric upside, no downside

4.Litigation risk: treaty-authority pathway likely challenged; injunctions possible

If the broader rule lands: full revenue base gets 280E relief, normalized tax bill drops near zero on current op loss, the $29.6M accrued liability becomes negotiable, and uplisting optionality (CSE/OTCQB → NYSE/Nasdaq) opens.

CAPITAL STACK

March 2 Series B restructuring eliminated Feb ’26 mandatory conversion. $14.725M conversion risk → $6.9M new mezz + ~$5.8M long-dated notes. WAM 4.6 yrs. $699K extinguishment gain. Near-term refi risk: gone.

WHAT TO WATCH

• Cash $7.9M — tight, watch burn (operating CF +$0.9M Q1)

• Inventory +$2.7M QoQ — channel build for rescheduling, or stale-product risk?

• Long-term notes +$5.8M QoQ — net leverage rising

• Accumulated deficit $131.7M — no margin for execution error

TAKEAWAY

The market is pricing partial rescheduling as the ceiling. The June 29 hearing is the binary catalyst that flips the equation. Operational execution is already best-in-class. The asymmetry is in the optionality nobody wants to underwrite.

Not the biggest name in cannabis.

Among the cleanest setups.

#cannabis #280E

White House Drug Strategy Shows Trump Administration's Conflicts On Marijuana And Other Issues, Experts Say: “The administration...is moving in a direction of liberalizing access to cannabis, but at the same time...it talks about the dangers of doing so."

https://t.co/maWOebAntt

🧵 US Cannabis | Week in Review — May 4–8, 2026

3 MSO/REIT Q1 prints.

1 CRS report.

1 peer-reviewed study.

52 days to the DEA hearing.

The post-rescheduling tape is bifurcating the sector — and most of this app is missing why.

Institutional read ↓

$MSOS $TCNNF $GTBIF $CURLF $CRLBF $VREOF

24% adjusted EBITDA margin. $19M operating cash flow. A refinanced $195M term loan, an upsized $100M revolver, and a $20M buyback authorization — all delivered in what has been the most punishing capital environment US cannabis has faced.

This is what disciplined capital allocation through a credit cycle looks like.

We are proud to be a long-standing investor in $VRNO.

The thesis has always been the TEAM.

Execution through cycles — not just tailwinds — is what builds enduring franchises in this industry.

Congratulations to @GeorgeArchos, @AaronMiles, and the Verano team. Genuinely excellent work.

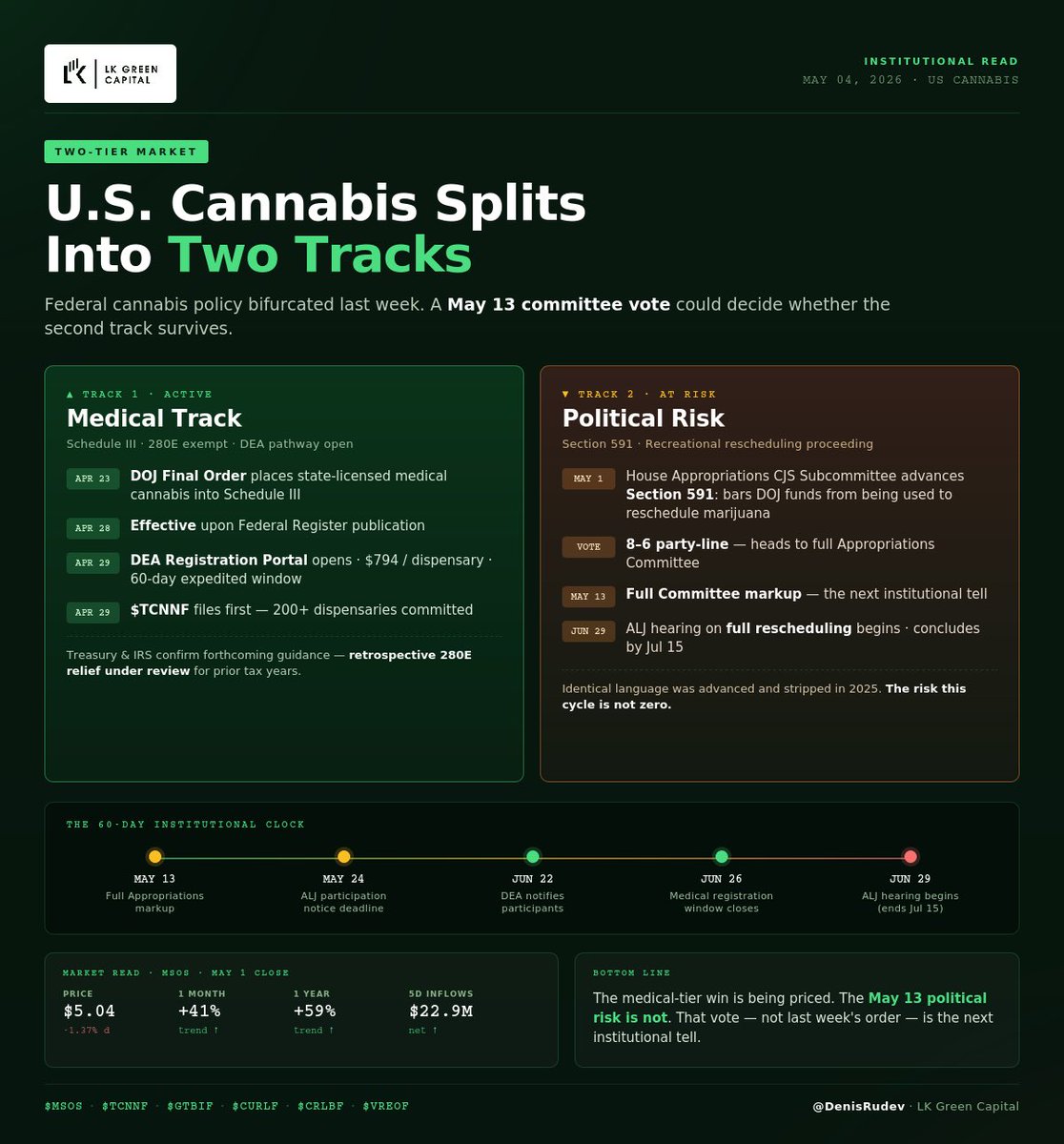

🌿 The Two-Tier U.S. Cannabis Market Is Now Real

The headline most accounts are still missing: federal cannabis policy split into two tracks last week, and a May 13 vote could decide which one survives.

📋 What’s already happened:

→ Apr 23: DOJ Final Order places state-licensed medical cannabis into Schedule III

→ Apr 28: Effective on Federal Register publication

→ Apr 29: DEA Medical Dispensary Registration Portal goes live — $794/location, 60-day expedited window (closes Jun 26)

→ Apr 29: $TCNNF files first — 200+ dispensaries committed

→ Treasury/IRS confirm forthcoming guidance, including retrospective 280E relief under review

📊 What this means structurally:

▸ Medical operators → Schedule III, 280E-exempt for the entire 2026 tax year, federal banking/payments exposure improves

▸ Recreational operators → status quo. 280E intact. Outcome contingent on the broader ALJ proceeding

▸ Mixed operators face an expense-allocation question the IRS hasn’t answered yet

🚨 The catch most are underweighting:

May 1 — House Appropriations CJS Subcommittee voted 8-6 (party-line) to advance Section 591, barring DOJ from using any funds to reschedule marijuana. Full Committee markup: May 13.

Identical language was advanced and stripped in 2025. The risk isn’t zero this time.

📅 The 60-day institutional clock:

→ May 13: Full Appropriations Committee markup

→ May 24: ALJ participation notice deadline (electronic)

→ Jun 22: DEA notifies selected participants

→ Jun 29 – Jul 15: ALJ hearing on full rescheduling

→ Jun 26: DEA medical registration window closes

📈 Market read:

$MSOS closed May 1 at $5.04. +41% on the month, +59% trailing 12-month. Net inflows of $22.9M over the past 5 days. The medical-tier win is being priced. The May 13 political risk is not.

The bull case is procedural: DOJ has the record, the EO has the cover, and the hearing has firm deadlines.

The bear case is institutional: a single committee vote could stall the broader proceeding regardless of executive momentum.

Watch the Appropriations Committee on May 13. That vote — not last week’s order — is the next institutional tell.

$MSOS $TCNNF $GTBIF $CURLF $CRLBF $VREOF

#USCannabis #Rescheduling #280E #MSOGang #CannabisInvesting

🚨 $CURLF Q1/26: The print the Street is mispricing.

Revenue: $324.2M (+6% YoY) | Beat guidance

Domestic +2% | International +35%

Adj. EBITDA: $63.4M (19.6% margin)

Gross margin: 49%

Net income (cont. ops): +$70.1M vs. -$54.8M Q1/25 — a $124.9M YoY swing

Cash: $106.1M | Debt: $565.1M

The 200bps EBITDA compression headline misses the nuance: 170bps of that drag is international — meaning domestic margins are flat in the worst pricing environment in years.

ATB Capital reiterates Outperform, C$5.25 PT on CURA-TSX. Forward stack:

• 280E medical relief begins Q2/26

• Q2 guidance tracking AHEAD of consensus

• H2/26 lift from Nov 12 hemp ban (190 days)

• 2027 international medical exports = vertical integration leverage

For 24 months the bear case was pricing + 280E + debt wall. Q1/26 is the first quarter all three variables bend in the operator’s favor — and CURLF carries the highest rescheduling beta given its leverage profile.

Margin compression is the noise. Net income inflection is the signal.

$MSOS $TCNNF $GTBIF $CRLBF $VREOF

#USCannabis #Rescheduling #280E #MSOGang #CannabisInvesting

Trump’s DOJ green-lit Schedule III for state-licensed medical cannabis + opened DEA applications for federal protections this week.

280E tax relief incoming.

This isn’t full legalization — it’s the biggest federal unlock for American-grown cannabis IP, genetics, and research in 50+ years.

U.S. operators now have the edge no other country can copy.

Next: SAFE Banking + descheduling so we can actually bank, list, and export the best medicine on earth.

Who’s building? @tomangell@MarijuanaMoment@USCRorg@POTUS

#USCannabis #ScheduleIII #CannabisReform

The April 23 Schedule III move for state-licensed medical cannabis finally gives researchers, patients, and providers real federal breathing room—but the June 29 expedited hearing is where the real game changes.

This the clearest signal yet that federal policy is catching up to 38+ state programs, opening doors to legitimate banking access, accelerated R&D, and tax clarity that could finally level the playing field for legitimate operators.

The missing piece? Congress acting on the bipartisan momentum already on the table to clear interstate commerce barriers and protect smaller players from consolidation.

Full reform in 2026 is the logical next step that unlocks legitimate economic scale while safeguarding public safety and state sovereignty.

Who’s ready to turn this regulatory thaw into actual industry growth? What is the one reform you’d prioritize post-hearing?

#USCannabis #CannabisReform #ScheduleIII