New paper w/ @prof_cookson@marinaniessner & Chukwuma Dim on using LLMs to measure investor disagreement. The basic question: can we capture how differently people react to the same financial news, at scale? 🧵 1/10

Wanna know what's happening at the cutting edge of big data + finance? Come to the 6th Future of Financial Information Conference! I'll be presenting "High-Throughput Asset Pricing or: How I learned to stop worrying and love data mining" (w/ @ChukwumaCDim). Stockholm, May 27-28.

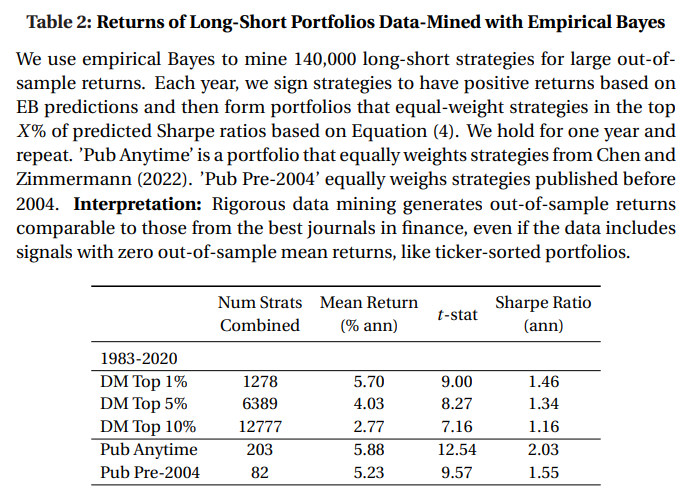

@ChukwumaCDim and I just updated "High-Throughput Asset Pricing." 🚨We now provide data and code for our high-throughput tests!🚨 Why study 200 cherry-picked anomalies when you can study *thousands* of anomalies that are systematically generated without look-ahead bias?

Pleased that our *Optimism Shifting* paper (https://t.co/PLFBaHaNzU) got the MFA 2024 *Best Paper award in Asset Pricing & Investments*. Thanks to the award committee, program chair @csialm, session chair @prof_cookson & discussant @schiller061 for thinking highly of our work.

New working paper!! The paper is called "High-Throughput Asset Pricing" (w/ @ChukwumaCDim). But in my heart, it will always be called "How I learned to stop worrying and love data mining." ❤️🧵

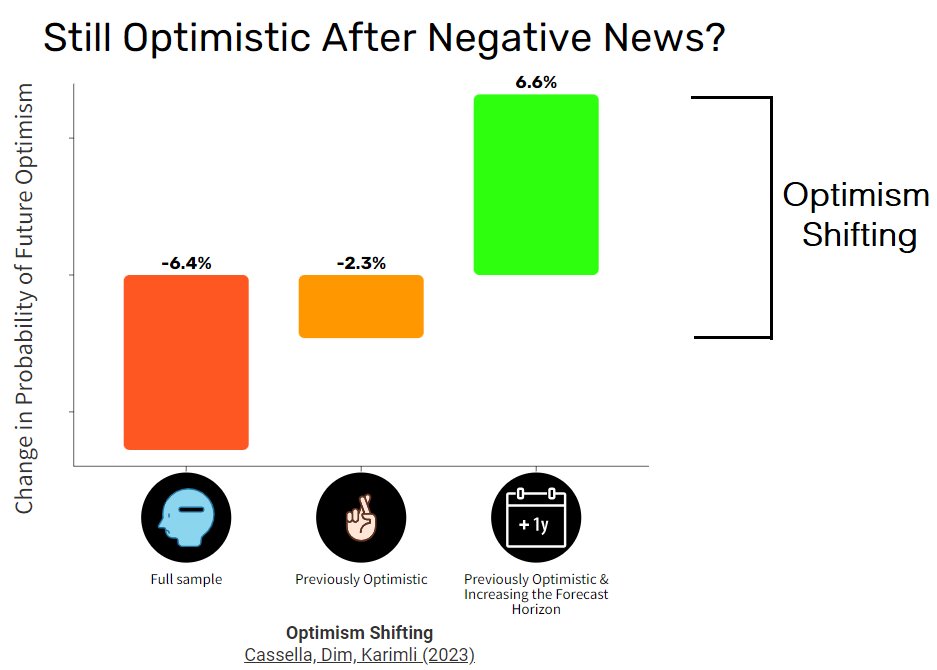

New research shows that investors defy pessimism with 'optimism shifting'! They turn bad news into fuel for long-term optimism. Optimism shifting can facilitate confirmation bias; has implications for disposition effect; is grounded in motivated beliefs.

https://t.co/PLFBaHblps

📢📢

We are so happy to announce the new 2023 #StiglerAffiliate Fellows at @ChicagoBooth, a multidisciplinary group of economists, business scholars, lawyers, and political scientists.

Read about them on @ProMarket_org: https://t.co/7d3cZIsyh6 🧵