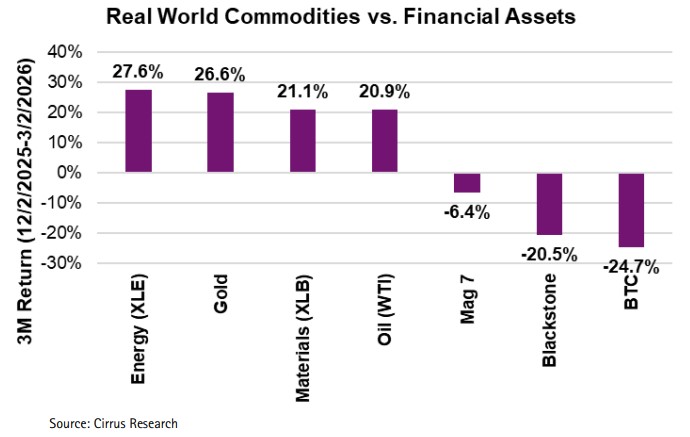

Bitcoin (BTC), down roughly 3.2% in the past year counters the general assumption that if smaller stocks are working, speculation is rampant. Int’l Markets, EM and US Small Caps, massively discounted, have led the US Large Cap market.

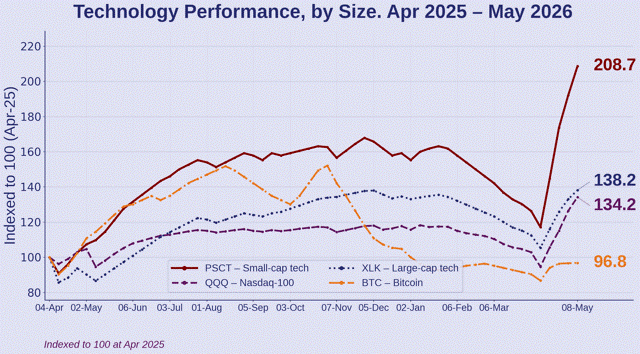

Broader markets also driving US Small Cap Tech to outperform in the AI footrace. Diffused AI spending forcing a trend that started at the market bottom in 2025!

The duration of the war is working against market stabilization. Rising Oil prices will likely force a defensive, valuation-sensitive bias without an off-ramp. Small Cap Industrial multiples, at record highs, will likely come under increasing pressure.

Rotational Market to Spin on Iran's Axis. As the Iran War inflates commodities and depresses risk assets, a de-escalation reverts to the fracturing of trade partners, central bankers fading US $ reserves, a bid for Gold & discounted risk assets (Int'l stocks, Small Caps & EM).

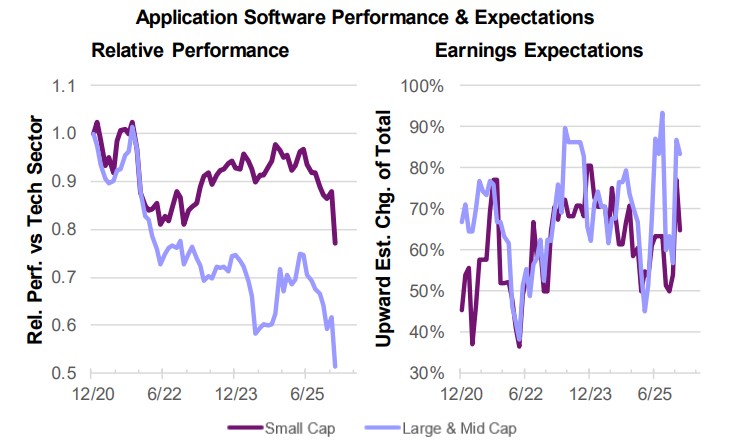

The AI disruption for Software/SaaS model has intensified but unlikely to reverse quickly. While earnings forecasts have begun to get pared back, it appears benign, as if Sell-side forecasts are behind the ball esp. among Large Cap Software firms. IMHO, too early to bottom fish.

The January run-up in US Small Caps is part of a broader movement as seen in Metals, EM, etc. A combination of central banks continuing to lower dollar reserves, new trade agreements such as Europe/India dampens USD flows, and a highly speculative US market forces the broadening.

The January Effect is back, R2 leads SP5 by about 570 bps as of mid-January! If the literature of Jan Effect occurring in the first few days of the month holds, 2026 can officially be stamped as a Jan Effect year. If valuations matter, markets will broaden, favoring smaller caps!

The Price Momentum factor sharply lagged for 2025, first time in three years! It's ironic that sell side analysts typically get “beat up" on their forecasts, and yet our Business Momentum pillar performance, primarily Consensus Est. Revision, was dominant for the year (+32%).

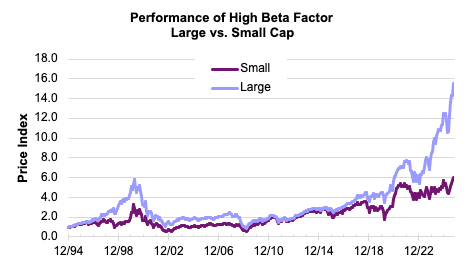

High Beta extremes seen in Mega Cap/AI! Broadening markets reflect investors’ urge to lower their market risks by adding exposure to most markets overseas and down cap; South Korea (+96%), Germany (+28%), Emerging Mkts (+42%) and US Micro Caps (+54%) since the April bottom.

Markets are broadening! Small Caps, Micro Caps rebound sharply, tracing paths seen in overseas markets as well as Gold. The spike in Mega Cap speculation, multi-decade discounting among the smaller firms & the need for the Fed to prop up mega caps underscore a rotational market.

The extreme equity market crowding in the US runs its course punishing the performance results of active Large Cap Growth blends. They have given up over 1000 BPS in a few short months.

A global bullish consensus on AI spending accelerates demand for AI applications and spending outside of AI Chips. Technology valuations, outside of the Mag-7 or Large Cap Tech sector, are massively depressed as AI dollars begin to surge

Downstream AI themes are outperforming Upstream (AI Chips) this year! The initial wave of spending in AI chips requires downstream spending from firms to go to market to monetize the initial chip investment. This will continue drive share price performance.

Even with the pullback of the US Mega Caps, Mag-7, there is plenty of room to see markets broaden. The backup of the term structure will continue to force a shorter duration, Value bias.

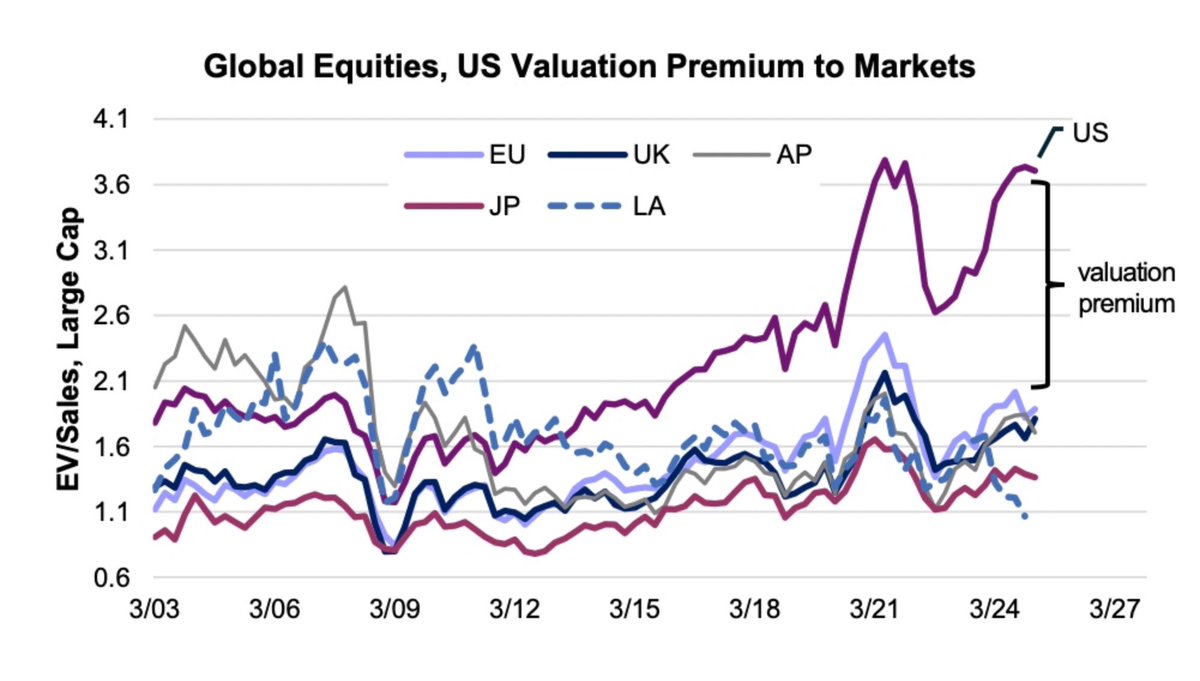

The fallout in the US Term Structure is Not driving a “Sell America” but instead Buy Value posture. US markets carry the highest multiples across all regions and are accompanied by historically high growth/margin assumptions.

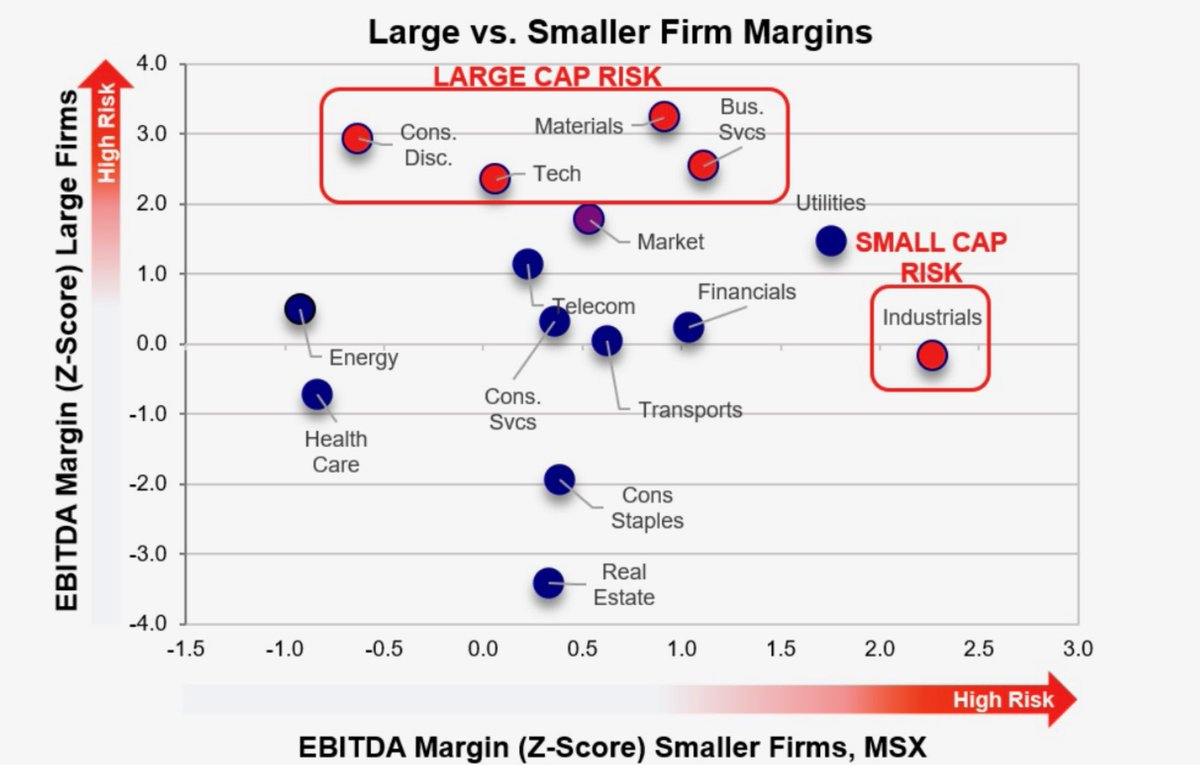

Peak margins amplify downside earnings cuts as rising input costs and tariff uncertainty act as “Sand in the Gearbox.” The margins for Large Cap Tech and Consumer Cyclicals groups are currently 2x to 3x standard deviations above normal!

NVDA’s earnings report confirms that sales growth continues to decelerate. The recent pullback in markets is not just tied to tariffs, but also the valuation risk of NVDA as its buyers begin to look elsewhere.