Summary of our research into #Bolivia's economic crisis and the possible solutions.

"...the crisis was 'not the result of bad luck or external shocks,' but rather the nation’s choice to 'crowd out private investment and long-term competitiveness' across the economy.

https://t.co/DNmJLtM65D

@ricardo_hausman@ClementBrenot@venturilucila

This is unfortunately quite true. From any rational, decision-theoretic standpoint, the Economics profession under-invests in imperfectly identified analyses of big/important/relevant questions relative to well-identified but comparatively uninteresting questions.

@RobinBrooksIIF Don't have the US figures for July, but Euro area trade deficit in June was ~$25bn (prob less than 2.5% of GDP annualized), while the US's was ~$80bn. Yes the US and the USD are different, but still

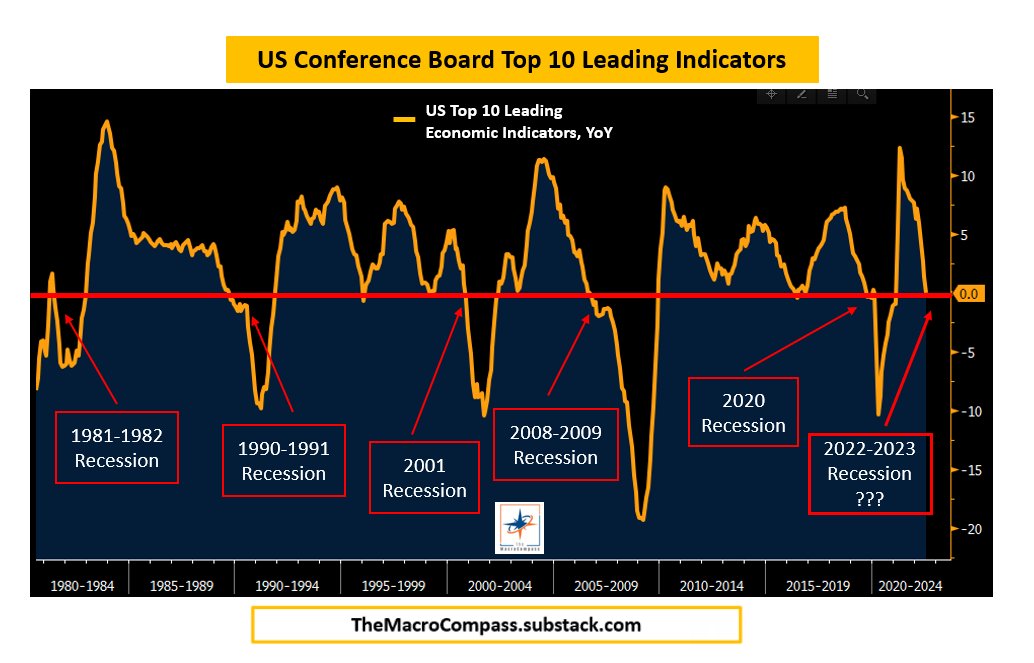

The index of the US Top 10 Leading Indicators has a 100% success rate in anticipating every recession over the last 40+ years.

By the time you get 2-3 consecutive negative prints, it's a done deal.

Last release was at 0%.

So: 2016 growth scare only or proper recession?

@Claudia_Sahm Rebasing at the trough rather than at the pre-recession peak is likely to be misleading. Without knowing how far we are from full employment at 100, hard to gauge what being at 115 means (just right? Overheating? Still some way to go?)

@_alice_evans Why wouldn't preference for seclusion apply? For instance for very conservative Muslim men, the possibility to have to interact with women at work, eg share offices or tools or interact with female public, may well be a factor keeping them from taking a number of jobs

@Sam_Dumitriu If policy was perfect and unconstrained by anything, the world would be better, sure. But what about real life? Political economy constraints, asymmetries of information, etc

@BruceJPreston Isn't it a huge problem that structural models can't achieve some form of data coherence though? Otherwise you could always argue "the internal logic is flawless, it's just that that's not how the real world actually works"

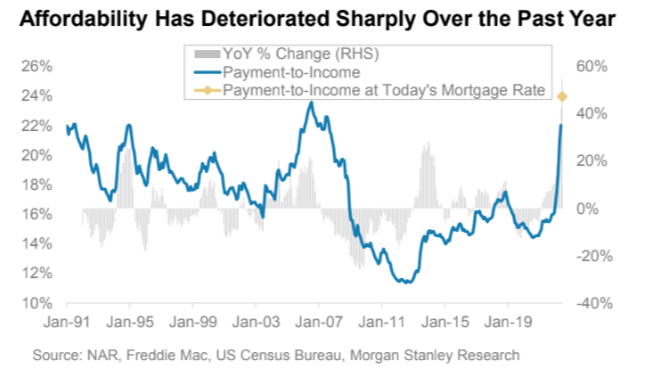

US mortgage payments-to-income ratio (blue, left hand side) at the same level as in 2007.

The rate of change is even more impressive: almost +60% increase against 12 months ago.

Housing affordability is as bad as it can get.

@juliaonjobs If you start the chart in Feb 2020 at about full employment / close to zero spare capacity, isn't this a chart about overheating? If the end of the story is Fed Funds rates up and both full-time and part-time employment crashing down, not my favorite chart anymore in 6 months

(1) New Working Paper: the fundamental driver of growth in modern economies, Total Factor Productivity (TFP), is linear, not exponential.

This is a paper I did not expect to write...

@heimbergecon This is even more true if you look at exports to the EU specifically (#1 European export market for Russia is Germany, #2 Netherlands) - Still from: https://t.co/Q4nScfeHyS

Nice exercise in modesty for economists by @martinwolf_, taking stock of old and new ideas (including by @asdomash and @LHSummers

And it's so surprising to see inflation...

https://t.co/6eyimzWhWL

The market has priced in seven 25-bps hikes this year and two more next year. #Fed tightening is in everyone's mind.

I though reminding people of what we used to call the "hairy caterpillar" chart might be useful: The market has a poor record of predicting the Fed. 1/3

@nick_bunker Is the historical average the goalpost though? To return to pre-covid employment rate you would need a significant bump above historical rate of "unretirement" for a bit...

“Today, the Democrats’ working-class problem isn’t limited to white workers. The party is also losing support from working-class Blacks and Hispanics.” https://t.co/Yhiwv7GKzh