Ethereum’s been bleeding, and even the Foundation is struggling: budget cuts, core team leaving, and everyone on crypto twitter asking if it’s over for ETH.

But Joe Lubin, the Consensys/MetaMask boss, came out to spin it: says it's not a crisis and the EF needs to slim down and stick to core tech.

Sounds nice on paper.

But think about it: if the Foundation takes a backseat, who takes over the biz dev and the real money-making parts of the ecosystem?

This isn't just restructuring. It's a massive power reallocation inside the Ethereum ecosystem.

BTC’s latest drop shouldn’t be blamed on the SpaceX IPO too quickly.

The story sounds smooth:

Retail sells crypto to chase a SpaceX listing at nearly a $1.8T valuation.

It feels logical. It’s easy to spread.

But the problem is, on-chain data doesn’t really back it up.

During the selloff, USDC and USDT didn’t show abnormal large-scale outflows.

Instead, around 66.5K BTC and 2.49M ETH moved out of exchanges.

That looks more like someone buying the dip and withdrawing coins, not everyone panic-dumping and running away.

The real bleeding was in ETFs.

Spot BTC ETFs had seen 13 straight days of net outflows, totaling around $4.4B.

So the real question isn’t:

Did SpaceX drain money from crypto?

It’s:

When AI, space, and mega IPOs become the hottest stories in global markets again, can BTC still compete for attention?

BTC wasn’t killed by SpaceX.

But SpaceX exposed one uncomfortable truth:

Crypto’s narrative power is being stolen by the outside world.

The scariest part about ZEC today is not the 40% drop.

It is this set of facts:

ZEC hit an intraday high of around $550 and a low of around $261.

The Orchard vulnerability had existed since May 2022.

It was not discovered until May 29, 2026, by security researcher Taylor Hornby.

In theory, this bug could have allowed an attacker to create unlimited, undetectable counterfeit ZEC inside the Orchard shielded pool.

This is not a normal bug.

It strikes directly at the most fundamental question for Zcash:

How can a privacy-focused asset prove that it has not been secretly diluted?

Zcash did not respond slowly.

On June 2, Zebra 4.5.3 temporarily disabled Orchard through a soft fork.

On June 3, Zebra 5.0.0 / NU6.2 re-enabled the fixed Orchard through a hard fork.

The official side also said there is currently no evidence of unauthorized issuance, and that Sapling and transparent transactions are operating normally.

But what the market truly fears is not whether “the bug has been fixed now.”

It is another line:

Shielded Labs admitted that cryptography alone cannot ultimately prove whether the vulnerability had been exploited before it was fixed.

That is the core of ZEC’s crash.

Privacy was supposed to be Zcash’s biggest moat.

But when a bug touches supply credibility, privacy can also become the biggest audit black box.

So today’s ZEC move is not just a simple correction.

It is being repriced by the market:

The value of a privacy coin does not only depend on whether it can hide transactions.

It also depends on whether, in the worst-case scenario, it can prove that no one secretly printed more coins.

Stablecoins are getting scary for one simple reason:

people are actually using them now.

DWF’s latest data shows stablecoin velocity has hit 49.7x, a new all-time high.

In plain English:

one stablecoin is changing hands almost 50 times a year.

In the first five months of this year alone, filtered stablecoin volume reached $6.64 trillion.

But here’s the real signal:

the fastest growth isn’t coming from exchange trading.

It’s coming from remittances, B2B payments, and B2C payments.

Stablecoins are moving from “cash chips before gambling on crypto” to “dollar pipes on-chain.”

And that’s the irony.

BTC and ETH are still being dragged around by ETF outflows. Everyone is asking whether the bull market is dead.

Stablecoins don’t care.

They’re answering a different question:

does crypto have real demand?

Right now, the answer is getting harder to ignore.

Prices can cool.

Narratives can fade.

Trading can slow down.

But as long as cross-border payments are slow, bank settlement is expensive, and dollar access is restricted, stablecoins will keep getting used.

The first crypto product to truly go mainstream may not be a chain.

It may not be a meme.

It may be the most boring thing in the room:

stablecoins.

Sui’s real risk isn’t that the network halted 3 times in 48 hours.

It’s that Sui has been priced as the “next Solana.”

For a new L1, the scariest thing isn’t downtime.

It’s what happens after downtime:

the market suddenly realizes it can live without you.

Solana also had outages.

But it survived because users, liquidity, memes, developers, and trading activity still came back.

That’s the real moat.

So now Sui has to answer the same question:

Are you just another high-performance narrative,

or are you an ecosystem people actually need?

“Next Solana” is not earned by TPS.

It’s earned when things break,

and the market still waits for you to come back.

People used to watch BTC through one simple lens:

Are stocks going up?

If equities were strong and risk appetite was alive, BTC was supposed to feel fine too.

But this week’s market looked different.

The S&P kept rising.

Brent crude stayed around $92.

Treasuries also strengthened.

Macro did not obviously break.

Yet BTC fell 2.6%, ETH fell 2.5%, and SOL fell 2.2%.

That tells us something has changed.

BTC is no longer just a simple macro risk asset.

Since spot ETFs launched, institutional flows have become a much more direct steering wheel.

When ETF inflows are strong, price has support.

When inflows weaken, even a decent macro backdrop may not be enough.

This does not mean macro no longer matters.

It means BTC now has another framework:

Before, people watched CPI, the Fed, and Nasdaq.

Now they also need to watch ETF net flows.

Crypto has not left macro behind.

But it no longer moves perfectly in sync with it.

One of the most confusing things in this market:

Why does BTC look like it has not collapsed, while altcoins keep feeling like nobody wants to buy them?

One whale position explains it pretty clearly.

He is holding around $50M in BTC longs,

while also shorting XLM, with an unrealized loss of about $570K.

If you only look at the XLM short, it looks like a bet that Stellar will go down.

But if you put both legs together, the logic changes.

This looks more like one thing:

Long BTC,

short alts,

selling altcoin beta.

Because in a BTC-dominant market, the most awkward thing about altcoins is not that they must fall.

It is that they often fail to outperform BTC.

When BTC goes up, they may go up too, but not enough.

When BTC goes down, they often fall harder.

So the $570K loss on the XLM short may not be a wrong trade by itself.

It may just be one hedge leg inside the whole structure.

That is also why this account can still be up $37M across the full cycle.

Retail asks:

Will XLM go down?

This kind of position asks:

Will XLM keep underperforming BTC?

Those are two very different questions.

SpaceX isn't public yet, but the on-chain market is already pricing it.

The SPCX contract on Hyperliquid opened at $150 and surged to $216.

Trading volume exceeded $33M.

Pushing its implied valuation to $1.78 trillion.

But the price isn't the point.

SPCX doesn't represent SpaceX equity,

has no official authorization,

pays no dividends,

and carries zero legal binding.

It's purely a USDC-settled on-chain contract fed by an oracle.

Here's the contrast:

When the companies behind Anthropic and OpenAI's synthetic stocks spoke out saying "unauthorized," prices dumped over 40% the same day.

With SPCX so far, SpaceX hasn't pumped the brakes publicly, Musk has said nothing, and the SEC hasn't made a move.

The market is taking this silence as a signal.

What this really opens up isn't just a single SpaceX contract.

It's the possibility of HIP-3 bringing the "pricing power of pre-IPO companies" on-chain.

The regulatory framework isn't out yet, but the market is already running.

The next company to be priced might not stay this quiet.

Fear & Greed Index: 22.

Translated, that number means this:

That friend of yours who spent last year spamming “send it, brothers” in the bull-market group chat hasn’t said a word in three months.

The Binance Square comment section has gone from “when $150K?” to “how much lower can it go?”

And the KOLs making content on Twitter have started pivoting to macro, gold, and “long-termism” — you know, those words that only show up when there’s no market to trade.

BTC is at $73,400, down roughly 30% from $105,000 a year ago. If you went all in around this time last year, every $100 in your account is now $70. And it’s been like this for 180 days — watching it slide from $90K to $70K, thinking every day it must be the bottom, and every day being wrong.

ETH is even worse. Cut in half in six months. $1,990 is basically where it was at the end of 2023. Two and a half years later, it hasn’t just gone nowhere — it has gone backward. Those reports that once screamed “ETH to $10K” are now impossible to find.

The last time the index hit 22 was the summer after LUNA collapsed in 2022, around the Three Arrows Capital blow-up. Back then, everyone thought “crypto is dead.”

You know what happened after that.

But the word “after” offers no comfort to someone cutting losses right now.

In November 2022, FTX had just collapsed. BTC was at 17,601. Everyone was screaming “zero,” and nobody dared to touch it.

CryptoCred tweeted: cut exposure, too much risk.

Three and a half years later, in May 2026, BTC is at 75,931.

The price he called “too risky” now looks like the cleanest bottom-buying opportunity of this entire cycle.

When fear is thickest at the bottom, even professional analysts will tell you to get off the train.

This isn’t mockery.

This is what cycles look like.

That tweet is still there.

Vitalik just published a long essay arguing that chasing 250ms latency and one-million TPS is a “road to mediocrity.”

The problem is, in the very same week, Hyperliquid’s FDV surpassed Solana’s.

On one side, Ethereum’s founder is saying:

“We don’t play that game.”

On the other side, the market is handing the trophy to the people who play that game best.

HYPE’s annualized revenue is $790 million, higher than Solana and even Ethereum.

This isn’t the market failing to understand idealism.

This is the market voting with money and telling everyone:

The game you don’t want to play has already gone live.

The more ironic part is that Vitalik also said 90% of his net worth is still in ETH.

He may disagree with this direction.

But his wealth is still tied to the old world that now has the most to prove.

Vitalik is on defense today.

Because the Ethereum Foundation has already lost 9 core people this year,

and 5 left in May alone.

And Dankrad went straight for the internal shout:

“Give me $1 billion and I’ll build another organization to save ETH.”

This is not resignation.

This is a coup.

A few hours ago, V God published the heaviest essay of 2026,

basically taking the whole CT with one sentence:

“Ethereum will not be a faster chain.

Chasing scale is the path of mediocre apps; we will definitely lose.

What we need is sanctuary technology —

censorship resistance, seizure resistance, open source, privacy.”

Translated into human language:

× Stop copying Solana TPS

× EF will become more important, but slimmer

× Stop dumping ETH from the treasury

× Use AI formal verification to bring protocol bugs close to zero within months

ETH is now $2,103.

Down 40% from ATH.

ETF net outflows hit $22.6B.

Soul question:

Is this Ethereum’s “re-aggregation,”

or is it the moment Nokia selected the wrong CTO?

Go comment under Vitalik 👇

Go dunk on Dankrad 👇

Good news: large models are getting smarter.

Bad news: they’re learning to ask me for money directly.

MoonPay’s recent integration into ChatGPT Apps sends a pretty sharp signal: you ask AI, “What is this token used for?” It finishes answering, and right below the answer, there’s a MoonPay payment link lying there.

No need to switch screens. Pick the token and amount, and it generates a checkout bill right on the spot.

In the past, buying crypto meant overcoming layers of psychological resistance just to open a trading app. Now, the moment the thought barely appears in your head, AI has already slapped the receipt in your face.

Crypto user acquisition is shifting from “users actively looking for products” to “you’re seriously doing research, and a random roaming sales rep picks you up on the spot.”

Whoever is closest to user intent is closest to the money.

@elonmusk This is why SpaceX is no longer just a rocket company — it’s becoming the tradeable proxy for satellite internet, AI compute, Mars, and the entire Musk premium.

https://t.co/BAICvF0VXH

The world’s first trillion-dollar individual may not be created by Tesla, but by SpaceX ringing the opening bell.

Forbes estimated in May that Elon Musk’s net worth was around $782 billion, while the combined SpaceX + xAI entity was valued at roughly $1.25 trillion.

If SpaceX’s IPO valuation reaches $1.75 trillion to $2 trillion, Musk’s stake could be repriced to more than $700 billion to $800 billion.

One IPO could effectively add the equivalent of New Zealand’s annual GDP to his paper wealth.

But the most fascinating part of SpaceX is that it is no longer just a traditional rocket company.

For ordinary investors, buying SpaceX after it goes public is roughly like buying:

40% Starlink cash flow,

25% rocket / Starship upside,

20% xAI / Grok and AI compute narrative,

10% Anthropic compute contracts,

5% that 18,712 BTC bonus.

So it doesn’t look like an “aerospace stock” anymore. It looks more like a super expectation ticket that bundles satellite internet, AI compute, the Mars narrative, Bitcoin assets, and Musk’s empire into one trade.

If Tesla defined the last round of the “Musk premium,” SpaceX may define the next round of the “human future premium.”

The world’s first trillion-dollar individual may not be created by Tesla, but by SpaceX ringing the opening bell.

Forbes estimated in May that Elon Musk’s net worth was around $782 billion, while the combined SpaceX + xAI entity was valued at roughly $1.25 trillion.

If SpaceX’s IPO valuation reaches $1.75 trillion to $2 trillion, Musk’s stake could be repriced to more than $700 billion to $800 billion.

One IPO could effectively add the equivalent of New Zealand’s annual GDP to his paper wealth.

But the most fascinating part of SpaceX is that it is no longer just a traditional rocket company.

For ordinary investors, buying SpaceX after it goes public is roughly like buying:

40% Starlink cash flow,

25% rocket / Starship upside,

20% xAI / Grok and AI compute narrative,

10% Anthropic compute contracts,

5% that 18,712 BTC bonus.

So it doesn’t look like an “aerospace stock” anymore. It looks more like a super expectation ticket that bundles satellite internet, AI compute, the Mars narrative, Bitcoin assets, and Musk’s empire into one trade.

If Tesla defined the last round of the “Musk premium,” SpaceX may define the next round of the “human future premium.”

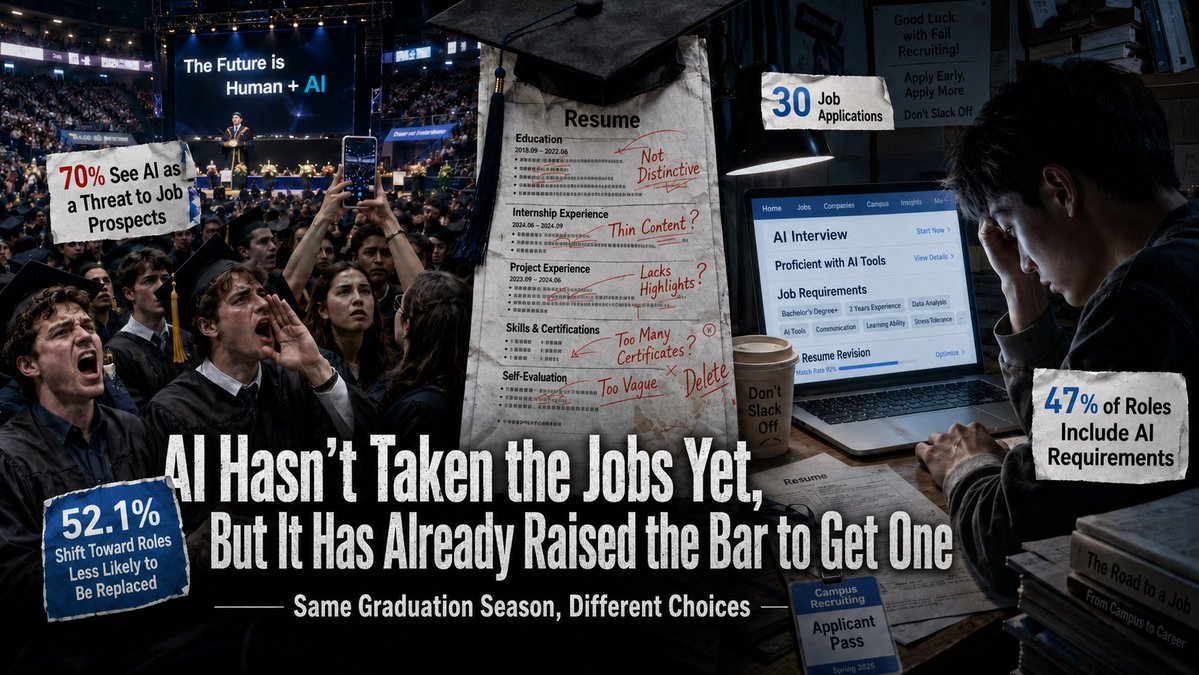

American students are booing AI at graduation ceremonies.

Chinese students are a little more practiced:

They rewrite their resumes first.

In the U.S., some students have already sent out 30 job applications before graduation and still haven’t landed anything. Around 70% of college students see AI as a threat to job hunting, and 42% of Gen Z believe it will squeeze job opportunities and wages for people like them. So when someone on stage says “AI will change every profession,” it does not sound like the future. It sounds like a debt collector.

In China, AI did not show up in the auditorium first.

It showed up first in job descriptions, interviews, and resumes. 47% of roles already include AI-related requirements. In Tencent’s spring recruitment, AI penetration reached 56% across roles, and 75% for technical positions. 61.4% of fresh graduates specifically study AI-related job requirements, 56.6% are actively improving their AI skills, and 52.1% have already shifted their job search toward roles “less likely to be replaced by AI.”

So the graduation cap falls in both places.

American students can still boo from the audience.

Chinese students often go back, open their laptops, and rewrite themselves into someone closer to what the job wants.

This still does not mean crypto companies have received a ticket to the Federal Reserve’s main hall.

For now, it is only at the proposed rule / public comment stage. Who can apply, how they will be reviewed, and how large the limits will be all depend on how regulators draw the lines next.

But the signal is very real:

Crypto companies have talked about compliance for years.

In the end, they still cannot avoid one very old-school question:

Will the bank counter recognize you?

The Federal Reserve is discussing allowing some fintech and crypto companies to plug into the Fed’s payment and clearing rails.

But what they’re getting is not the full banking main hall.

It looks more like a small service window next to the counter.

This payment account can only be used for limited clearing and settlement:

No interest,

no access to Fed credit,

and limited balances.

For crypto companies, this is not a direct pass into the inner banking circle.

It is more like finally getting a queue number:

Now they are allowed to line up.

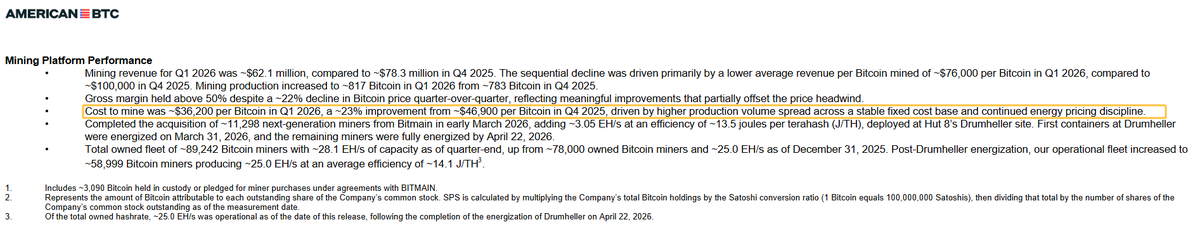

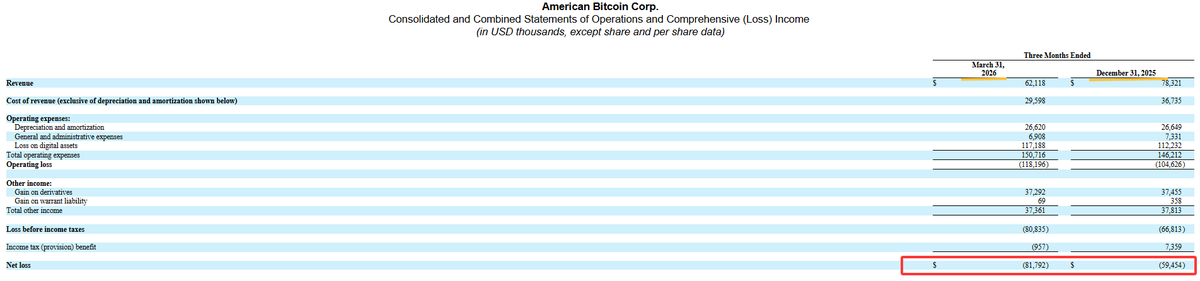

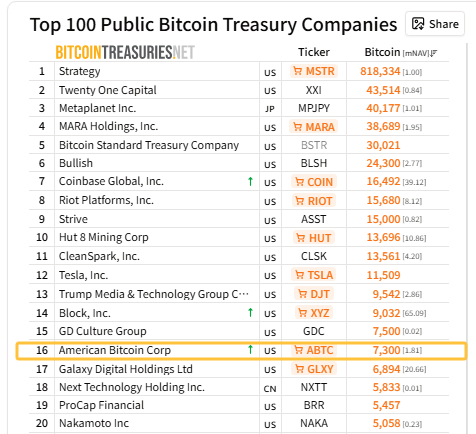

American Bitcoin (ABTC) has just delivered a first-quarter 2026 earnings report that has Wall Street frowning and Bitcoin believers silent.

The numbers themselves are split: a net loss of $81.8 million in Q1 2026, an expansion of 37.5% compared to Q4 2025's $59.5 million loss; yet during the same period, the company's Bitcoin holdings net increased by over 1,600 coins.

Revenue fell by 20%, and the company's stock price (ABTC) dropped 9% in a single day. At the current price of $1.16, it has already fallen 92.15% from its post-IPO high of $14.65.

What's Behind the Numbers

Let's get the accounts straight.

American Bitcoin's Q1 2026 net loss figure is striking, but after reviewing the details, you realize it's not as bad as it looks: approximately $117.2 million is due to FASB accounting rules requiring mark-to-market revaluation of Bitcoin holdings. A purely accounting treatment, with nothing to do with the company's actual operational capabilities.

The company's CEO Mike Ho said it directly on the earnings call: "If we exclude the non-cash Bitcoin market value adjustments, our underlying business is profitable. And we didn't sell a single Bitcoin in Q1."

This is the key point. Not a single Bitcoin sold, yet a net increase of over 1,600 coins. What does this mean? The company not only believes Bitcoin will rise, but believes in it so firmly that it is unwilling to liquidate a single piece of inventory during a downturn.

Bitcoin mining costs are also improving:

Down from $46,900 per coin in Q4 last year to $36,200, a 23% decrease. This means, even if Bitcoin prices continue to face downward pressure, the company's cost pressure is marginally improving.

The Trump Family's Business

American Bitcoin's founding story itself is dramatic enough.

The company was established in March 2025, as a deep binding between Hut 8 and the Trump family — not "endorsement," but genuine ownership and control. Eric Trump is co-founder and Chief Strategy Officer, Donald Trump Jr. is a significant shareholder, and the two of them combined with Hut 8 hold 98% of shares, this is not celebrity endorsement, this is the immediate family of the current U.S. President directly entering the game.

This structure gave American Bitcoin something no other mining company has: extremely high topic appeal and traffic, and implicit policy imagination space. After Trump's return to the White House, the family's encryption布局 clearly accelerated!

World Liberty Financial, USD1 stablecoin, plus American Bitcoin, all mean that cryptocurrency is becoming an increasingly core part of the Trump family's business landscape.

But this binding is a double-edged sword. The benefit is abundant liquidity and narrative attraction; the downside is that the superposition of political risks is completely unpredictable. Once the White House policy shifts, regulatory attitudes change, or the Trump family's crypto business faces Congressional investigation, American Bitcoin's stock price may bear the brunt first. This kind of risk almost never exists in traditional mining companies.

The Mining Company's Choice

Back to the business model itself.

Bitcoin mining companies are essentially a leveraged instrument, naturally long Bitcoin. When Bitcoin rises, mining machine computing power value, holdings market cap, and mining revenue all rise simultaneously; when Bitcoin falls, operational losses, asset impairments, and financing pressure all squeeze simultaneously. American Bitcoin is no exception.

Bitcoin's price retreated from the historical high of $126,000 touched in October 2025 to the current price near $80,000, a decline of about 40%! This background is the key to truly measuring the degree of damage to American Bitcoin's holdings.

American Bitcoin's strategic choice is interesting: it did not choose "mine and sell" to maintain cash flow, but continuously accumulated Bitcoin reserves.

As of end of Q1 2026, holding approximately 7,021 Bitcoin; as of early May, Eric Trump stated it exceeded 7,300, already ranking 16th among global publicly listed companies in Bitcoin holdings.

The benefit of this strategy is: once Bitcoin usher in the next bull market, the accumulated position will be amplified. The downside is: if it is currently a bear market or volatile market, the company's financial pressure will continue, even intensify. Eric Trump said in a statement "mining Bitcoin at 47% below spot price"; this statement sounds attractive, but needs to be treated with caution.

Based on the company's mining cost of $36,200 per coin, if Bitcoin's average price is $80,000, theoretically there is approximately $44,000 of "mining profit" space per coin. But this profit is on paper — it can only be realized when Bitcoin is sold.

Conclusion

American Bitcoin exchanged over $81.8 million in book losses in Q1 2026 for more than 1,600 Bitcoin in strategic reserves, while simultaneously bearing the reality of a 92% stock price decline and extremely deteriorated liquidity.

If Bitcoin rebounds to a new all-time high, this strategy will be called "visionary"; if Bitcoin continues to underperform or enters a long-term bear market, this strategy will be called "a failed gambler's behavior."

And this is a theoretically justified, but unregistered gamble. The Trump family has wagered not just capital, but political credibility and family branding; the scale of this bet has exceeded the scope of ordinary listed company decisions.

#BTC #Bitcoin #ABTC #Trump #CoinMeta

1. The Source: Not Trump Himself

First and foremost, this statement did not come directly from Donald Trump, but from his son Eric Trump speaking at a Bitcoin conference.

During that event, Eric Trump mentioned that the U.S. government currently holds approximately 300,000 BTC and suggested these assets would not be sold. This view was subsequently spread through secondary transmission and gradually evolved into the "Trump statement" version, rapidly spreading on social media.

This transmission path itself has already planted the seeds of information bias.

2. 300,000 BTC: Largely True, But a "Historical Legacy"

From a data perspective, the claim of "300,000 BTC" is not unfounded.

The U.S. government has seized large amounts of Bitcoin through law enforcement actions (such as combating dark web platforms and cybercrime). The most typical case is the "Silk Road" incident. These assets are typically managed by the United States Marshals Service and have been gradually disposed of through auctions in the past.

Therefore, current market estimates that the U.S. government holds between 200,000 to 300,000 BTC, which can be considered "largely true."

However, it should be noted that these BTC are not actively allocated but passively obtained enforcement assets, fundamentally different from sovereign wealth funds or central bank reserves.

3. "Not Selling": Policy Tendency, Not Certain Fact

What truly triggered market sentiment volatility is the statement "not selling."

From a policy perspective, the Trump camp has indeed released clearly crypto-friendly signals in recent years. For example, discussions around "strategic Bitcoin reserves" are gradually heating up, with logic similar to gold reserves, treating Bitcoin as a long-term strategic asset.

But the problems are:

- The U.S. government has auctioned BTC multiple times in history, not held long-term

- "Strategic reserves" currently remain more at the policy concept level

- There is no legally binding mechanism explicitly stating "never sell"

In other words, a more accurate statement at present should be:

👉 Policy direction may tend to reduce selling, but "never sell" has not been institutionally confirmed

4. Why Is the Market So Excited?

Despite the information bias, this news quickly spread, reflecting the market's high sensitivity to "national-level buying."

At the current stage, Bitcoin prices have been long constrained by macro liquidity and selling pressure structure. If the U.S. government shifts from a "potential seller" to a "long-term holder," its symbolic significance far outweighs actual supply-demand changes:

- Selling pressure expectations decline (reduced auctions)

- Narrative upgrade (transition from risk asset to reserve asset)

- Enhanced policy endorsement (sovereign-level recognition)

This is why similar statements, even unconfirmed, can still affect market sentiment in a short period.

5. Conclusion: Beyond True or False, More Importantly the Trend

Returning to the original question—"Trump claims the U.S. holds 300,000 BTC and won't sell, is it true?"

The answers are:

- ✔️ Holdings scale: Largely true

- ❗ Information source: Not U.S. President Trump himself, but his son Eric Trump

- ❗ Not selling: Not yet formally confirmed

But more noteworthy than truth is that such narratives are gradually becoming one of the market's main themes.

When "whether Bitcoin will be held long-term by nations" shifts from assumption to policy discussion, the market's pricing logic may also change accordingly.

#BTC #CoinMeta