🔥 @Andrada_Mining - Is the market missing the bigger picture ⁉️

Current #ATM share price: ~3.9p

Hannam & Partners target valuation: 22p

Potential upside: +471% 🚀

What stands out?

✅ #Tin prices have surged to near all-time highs

✅ ATM is already producing and generating cashflow from Uis

✅ Expansion funding now secured through equity and long-term Namibian bank financing

✅ Ore sorting and crushing upgrades set to increase production materially

✅ Lithium Ridge continues to deliver high-grade results with SQM funding exploration

✅ Brandberg West adds significant tungsten upside at a time of tight global supply

The key point for me:

A producer selling into a strong tin market is very different to an explorer hoping to build a mine one day.

With tin prices near record levels, Hannam estimates that a 10% move in the tin price could drive a 31% swing in Andrada’s earnings. That’s serious leverage to one of the hottest critical metals in the market.

The question isn’t whether ATM has assets.

The question is whether the market is pricing them correctly. 👀

$ATM #Tin #Lithium #CriticalMinerals #MiningStocks #AIM #Investing #Namibia #CommodityBullMarket #SmallCaps

This is why many investors view @Andrada_Mining as one of the very few genuine listed ways to gain direct exposure to the #tin price on AIM. #ATM

“AI demand keeps growing, tin stays above $50,000/t and supply remains constrained”

🥇 Andrada Mining – producing today and generating cash flow.

🥈 First Tin – development story.

🥉 Metals Exploration – secondary tin exposure.

🚨 ⛏️ each month that passes tin prices over the past 6 months have been incredible , Take the photo below average price around $53,000k a tonne , the ones previously have been around $49k and $48k , the plant started as a pilot plant and now is growing into something bigger . Just one cog ⚙️ of this company assets , producing tantalum and lithium circuit is in motion . #ATM @Andrada_Mining

@DavidBurton1971@ColinPolykett@Andrada_Mining As much as negative sentiment has tethered share progress, if tin stays anywhere near where is it now, let alone further appreciation, this tiny company could be a life changer. 10 bagger within 5 years? Let’s start with a modest easy single bag and we will take it from there.

@APathNotTaken The management have no difficulty in attracting JV partners, strategic partnerships and well known investors but as mentioned by others there has been disappointments in the past and there’s a lot of smaller investors getting frustrated and negative despite all the signs

@Treespotter25@DavidBurton1971@Andrada_Mining 100% agree. The tin price has transformed the the company compared to its last reported figures. The expansion will be in place within this financial year as well - it won’t just be a creep over the line to profitability, it’ll be a giant leap. Then we have the other metals…..

A fair question keeps coming up re @Andrada_Mining :

“…𝙄𝙛 𝘼𝙣𝙙𝙧𝙖𝙙𝙖 𝙞𝙨 𝙥𝙧𝙤𝙛𝙞𝙩𝙖𝙗𝙡𝙚, 𝙬𝙝𝙮 𝙝𝙖𝙨 𝙞𝙩 𝙧𝙖𝙞𝙨𝙚𝙙 𝙢𝙤𝙣𝙚𝙮 𝙩𝙬𝙞𝙘𝙚 𝙞𝙣 𝙩𝙝𝙚 𝙡𝙖𝙨𝙩 6 𝙢𝙤𝙣𝙩𝙝𝙨?…”

The answer is actually quite simple.

Those raises weren’t about plugging a hole in the balance sheet. They were about accelerating growth and bringing high-quality strategic investors onto the register.

✅ T10

✅ Coffey

✅ Everblue

These aren’t short-term traders. They’re experienced resource investors who wanted meaningful exposure to the #ATM story.

Their investment has helped provide the capital to:

🔹 Accelerate expansion plans at Uis

🔹 Progress ore sorting and processing improvements

🔹 Advance lithium development opportunities

🔹 Strengthen the balance sheet for future growth

🔹 Capitalise on a tin price sitting near multi-year highs

Remember, Andrada is already producing and generating revenue. The raises have allowed management to push harder on growth initiatives rather than taking a slower, more cautious route.

Sometimes the best time to raise capital is when you don’t desperately need it.

Strong strategic investors. Stronger balance sheet. Accelerating growth pipeline.

With #tin around record levels and production increasing, the company appears to have positioned itself to maximise the opportunity ahead.

$ATM #AndradaMining #Tin #Lithium #MiningStocks #AIMStocks #Investing

🔥 The market is obsessed with the expansion story at #ATM…

But what if it’s missing what’s happening RIGHT NOW with @Andrada_Mining 👀

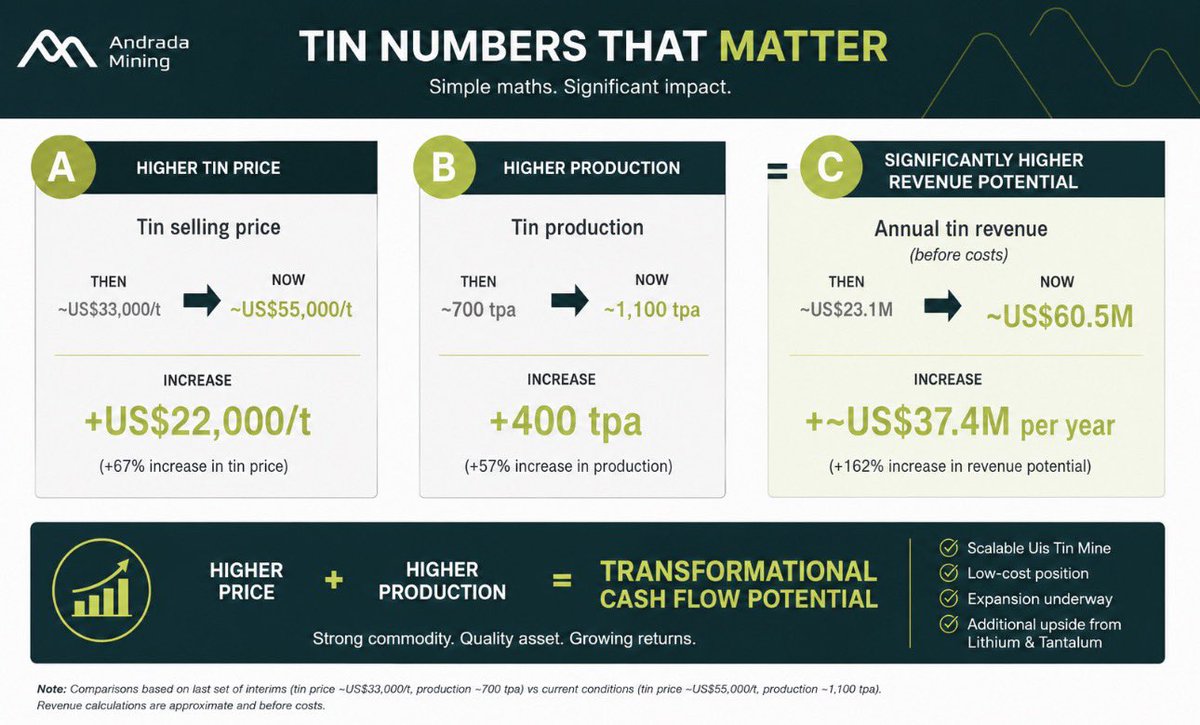

At the last interims, #tin was selling for around US$33,000/t with all-in sustaining costs of approximately US$30,000/t.

Today it’s ~US$55k/t. 💰

Production has increased to around 1,100tpa. 📈

So while everyone talks about what Andrada could become…

…the company is already generating cash and benefiting from a tin price sitting near all-time highs.

📈 Higher tin price

➕

📈 Higher production

🟰💰💰💰

Feels like the market hasn’t fully joined the dots yet.

#ATM - Upward trendline still in play and would suggest we bounce from here

Seller looks to be done

Other than a quick flush below in March this has been a reliable trendline since the lows last year

Fundamnetally in a VERY strong position

Back into 4p+ range this week

👀 The price doesn’t lie… except when it does. Take @Andrada_Mining#ATM

Screen showing 3.63p–3.70p?

Try buying any meaningful size.

📸 250,000 shares available at 3.78p+

📸 Multiple market makers already quoting well above the displayed price.

That’s the difference between a screen price and a real market price.

When buyers start competing for stock, the headline quote can quickly become irrelevant.

✅ Tight availability

✅ Size difficult to source

✅ Premium required for meaningful orders

✅ Demand clearly outweighing visible supply

The question isn’t what the screen says…

It’s what someone actually has to pay to get stock.

PS - Seller oooooooooooot helps 👀🤫

@APathNotTaken Has also been hit several times with early, large, investors getting out, which has been a huge weight on the SP even as the business has improved dramatically. Those sellers have to run out at some point……

@APathNotTaken@DavidBurton1971 Delayed expansion, many losing patience, which is understandable, but #ATM is arguably now in the best shape it’s ever been in. Printing cash on the current tin operation, two JVs fully funded and the tin expansion also fully funded and due to complete this year.

#ATM

Can someone kindly tell me why this is so unloved?

ASIC $25k pt

Tin price $55k pt

Tungsten 3.55% grades

Lithium JV

Ore processed +8%

Processing rate +7%

Conc +15%

Contained tin +11%

So ASIC likely even lower

SP keeps drifting lower

#ATM - Even if you just look at their Tin production they are clearing $30k profit per tonne

Then factor in Brandberg West & Lithium Ridge... Its a solid buy here

Will have its day in the sun soon, i have no doubt