The Next Generation of Commodity Intelligence

AI agents built to research, interpret, and deliver insights with the precision of an experienced desk analyst.

https://t.co/HOE2JjNCIE: New Name, New Brains.

We Didn’t Just Rebrand — We Rebuilt Everything

We’re excited to introduce https://t.co/HOE2JjNCIE, rebuilt from the ground up. Our new AI agents deliver insights with the speed and precision of an experienced desk analyst — simply ask a question and get an answer.

Click here to join the wait list to complimentary access:

https://t.co/JcpFN87OHf

Understanding The Hormuz Risk Premium in Global #LNG

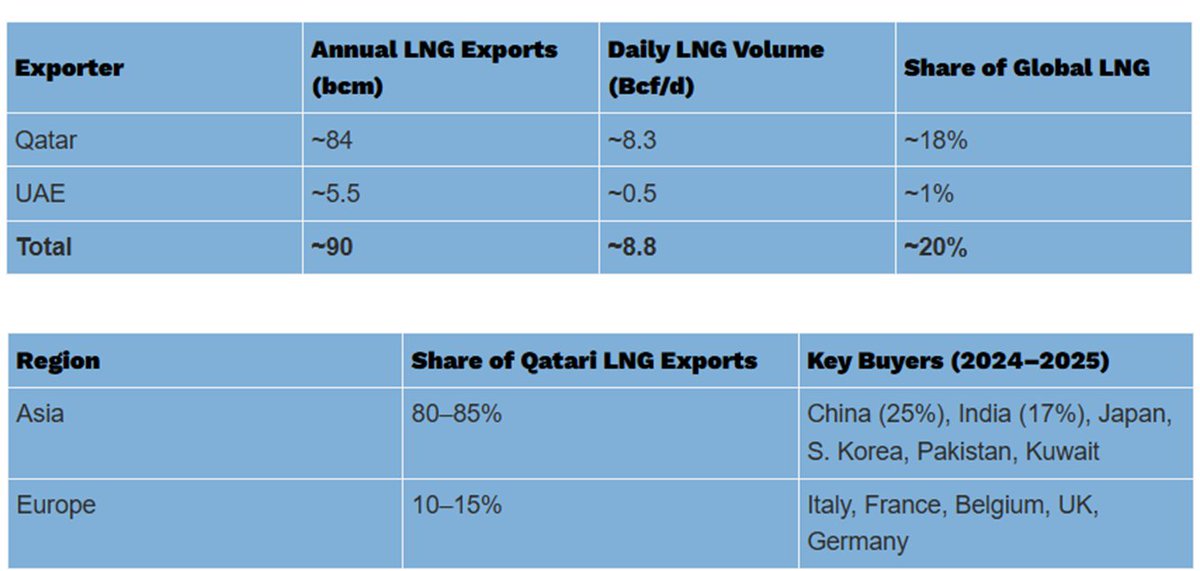

1/ The Strait of #Hormuz is a critical chokepoint for LNG. ~90 bcm/year (≈ 8.8 bcfd) of LNG from Qatar & UAE passes through it — roughly 20% of global LNG supply. On average, 6–8 LNG tankers/day transit the strait.

2/ Despite decades of tension, Hormuz has never been fully closed to LNG shipping — even during wars and major regional crises. A full shutdown would also cripple Gulf exporters, making it a last-resort (“nuclear”) option.

3/ Markets still price a Hormuz risk premium. Why?

#Qatar & #UAE LNG have no alternative export routes, so even threats raise LNG prices via higher insurance, freight rates, and supply-loss risk — especially for JKM (Asia) and TTF (Europe).

4/ A real disruption would be severe: losing ~20% of global LNG would tighten supply fast. Asia would be hit first, Europe would feel knock-on price spikes, shipping rates would surge, and buyers would scramble for US LNG and other marginal supply.

Read the full analysis here: https://t.co/fHIpqc3kKx

#ONGT #energy #natgas

Rapid Research: Europe’s New Russia Oil Sanctions: What They Mean for Diesel, Jet Fuel, and Price Risk

1. Expanded Import Ban: Russian-Origin Crude in Third-Country Products

2. Key Exemptions and Carve-Outs

3. Key Impacts on Imports (Jet Fuel & Diesel)

4. Market Impact from Additional Sanctions (as of Jan 2026):

https://t.co/joa89cEAix

#oil #OOTT #energy

Rapid Report: Freeze-Offs in Focus - What Really Moves Marcellus & Utica Supply

1️⃣ Highest freeze-off risk = SWPA & WV

Wet gas and older gathering systems make them most vulnerable. Ohio Utica is moderate risk; NEPA is lower risk but not immune. A multi-day Marcellus/Utica freeze-off would be bullish for regional prices and Henry Hub.

2️⃣ Weather is turning supportive for freeze-offs

The 8–14 day outlook points to below-normal temps across the Midwest and Northeast, raising late-January risk. No major events yet this winter — but risk is elevated, especially in SWPA/WV.

3️⃣ What drives duration

Short freezes + fast warmups = same-day recovery.

Prolonged cold, wet gas exposure, power issues, and slow field response = multi-day production losses.

4️⃣ January 2025 reminder

Arctic cold drove a major event.

Peak losses reached ~9 Bcf/d (Jan 16), with most volumes back in 2–3 days. SWPA and WV were hit hardest.

#natgas #energy #production #marcellus

https://t.co/g3hlqtSAxW

PJM 2026 Forecast: The Load Is Coming (Delayed, Not Denied)

https://t.co/qz3qjYuSnG

PJM 2026–2030 Load Forecast: Key Takeaways

PJM’s 2026 Long-Term Load Forecast (Jan 2026) projects RTO-wide summer peak load to grow at 3.6%/yr (10-yr avg), reaching ~222 GW by 2036 (up ~66 GW from today).

Winter peak load is forecast to grow even faster at 4.0%/yr, reaching ~205 GW by 2036.

Net energy for load is expected to increase by 4.8%/yr over the next decade.

Change vs. Prior Forecast:

Near-term (2026–2032) peak demand was revised down by 0.7–2.6% vs. last year, mainly due to:Stricter vetting of large load (data center) requests

Softer economic/EV adoption assumptions

Long-term growth remains robust, with the main risk being the timing of large load additions, not the magnitude.

#PJM #natgas #Power

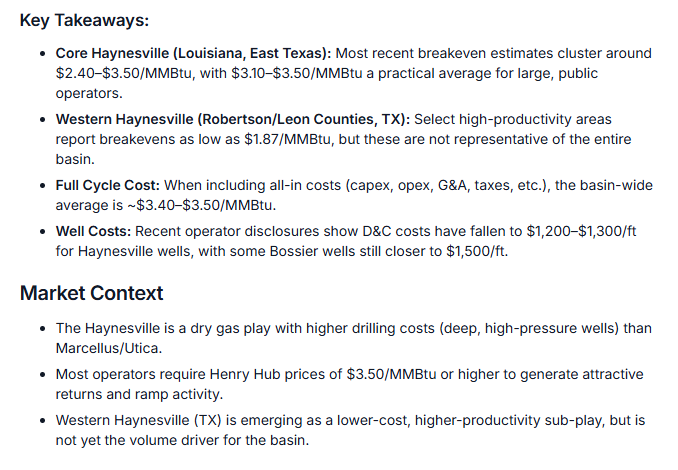

Haynesville Curtailment: The Multi-Bcf Question https://t.co/wNE2ntRGY0

Public:

Expand Energy (EXE): Largest US gas producer, ~3.2 Bcf/d Haynesville. 2026 capex guided for “maintenance mode” unless prices rise “materially higher” than $3.50/MMBtu. No plans to add rigs at current strip.

Comstock Resources (CRK): ~4–6 rigs, focus on Western Haynesville. Aggressively reducing D&C costs (now ~$31M/well). 2026 plan is “hold acreage,” with TILs and pad size flexible to price. No 2026 volume growth unless strip >$4.

BP: All have cut rigs or deferred TILs in 2025; BP is considering adding rigs if $4+ strip holds for 2026.

Private:

Aethon Energy: Largest private, 7 rigs, “maintenance mode” in 2025/26. Explicitly requires $5/MMBtu for growth.

GEP Haynesville II, Tellurian: Focused on core; breakevens $2.70–$3.20/MMBtu. No growth at sub-$3.50/MMBtu.

See our Rapid Analysis (Generated with 3-Prompt in 3-Minute)

The Venezuela Shift: Global Oil Market Impacts of US Asset Control

https://t.co/YGOyDtJuwy

See our Rapid Analysis (Generated with 3-Prompt in 3-Minute)

The Venezuela Shift: Global Oil Market Impacts of US Asset Control

https://t.co/YGOyDtJuwy

Here is what @ComdtyAI thinks:

The oil industry plays a crucial and multifaceted role in the global economy and energy markets, with direct implications for energy security, economic growth, and the ongoing energy transition. Here’s a concise breakdown of its key roles, using the latest market and policy context:

1. Backbone of Global Energy Supply

Oil and gas currently provide nearly 55% of the world’s energy supply, powering transportation, industry, heating, and electricity generation.

The U.S. remains the world’s largest oil producer, averaging 13.5 million bbl/d in 2025–2026 (EIA STEO Oct 2025).

Oil is vital for the production of fuels (gasoline, diesel, jet fuel) and as feedstock for chemicals, plastics, fertilizers, and pharmaceuticals.

2. Economic Engine and Job Creator

The sector is a $3.2 trillion global industry, supporting over 4.5 million direct jobs and millions more indirectly.

U.S. oil and gas industry alone is projected to provide $1.6 trillion in federal and state tax revenue between 2012 and 2025, funding infrastructure, schools, and public services.

Oil production lowers energy costs for consumers and is critical for trade balances, especially in major producing nations.

3. Enabler of Energy Security

Oil companies manage strategic reserves and supply chains, providing a buffer against geopolitical shocks, natural disasters, and market disruptions.

The industry’s ability to ramp up or curtail production directly influences global price stability and national security.

4. Catalyst for Technological Innovation

The sector drives advancements in exploration (e.g., deepwater, shale), refining, and emissions reduction (e.g., carbon capture, methane management).

Oil and gas infrastructure and expertise are being leveraged to scale up hydrogen and carbon capture technologies, supporting the energy transition.

5. Central to the Energy Transition

Natural gas is a key “bridge fuel,” enabling a shift from coal to lower-carbon energy while renewables scale up.

Oil majors are investing in renewables, biofuels, and clean energy tech, but fossil fuels are projected to remain a significant part of the energy mix through 2050, even in net-zero scenarios (McKinsey, IEA).

6. Geopolitical Influence

Oil supply and pricing are deeply tied to geopolitics—OPEC+ decisions, sanctions (e.g., on Russia), and regional conflicts can rapidly shift global flows and prices.

National oil companies (NOCs) and supermajors play a pivotal role in market stability and energy diplomacy.

Current Market View:

Neutral to slightly bearish fundamentals for 2026.

Global oil inventories are building (forecast: +2.1 million bbl/d in 2026), putting downward pressure on prices.

OPEC+ is increasing production, but below targets, which moderates oversupply.

Demand growth is led by non-OECD countries, but overall consumption growth is slower than supply growth.

Geopolitical risks (Russia, Middle East) remain, but are currently outweighed by supply fundamentals.

#OOTT #oil

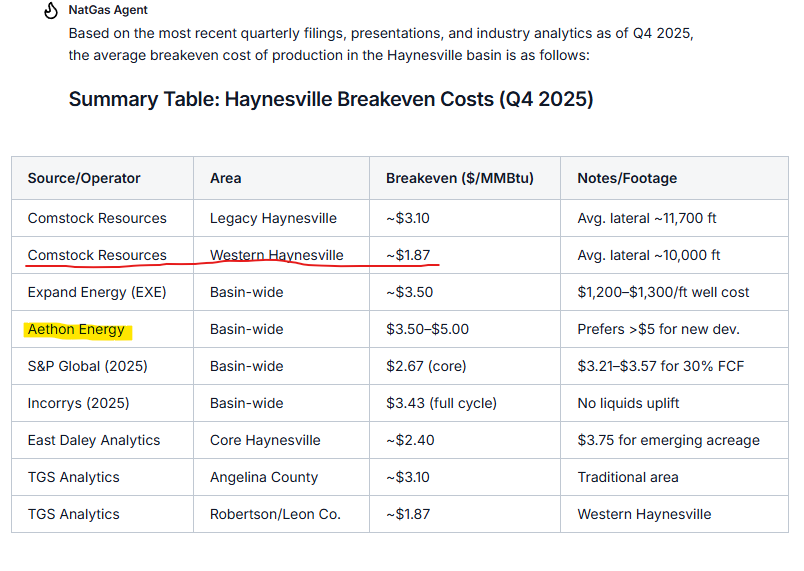

Been playing around with the new updated https://t.co/zbtHwQAU0Q courtesy of @ComdtyAI (it's an excellent natgas agent).

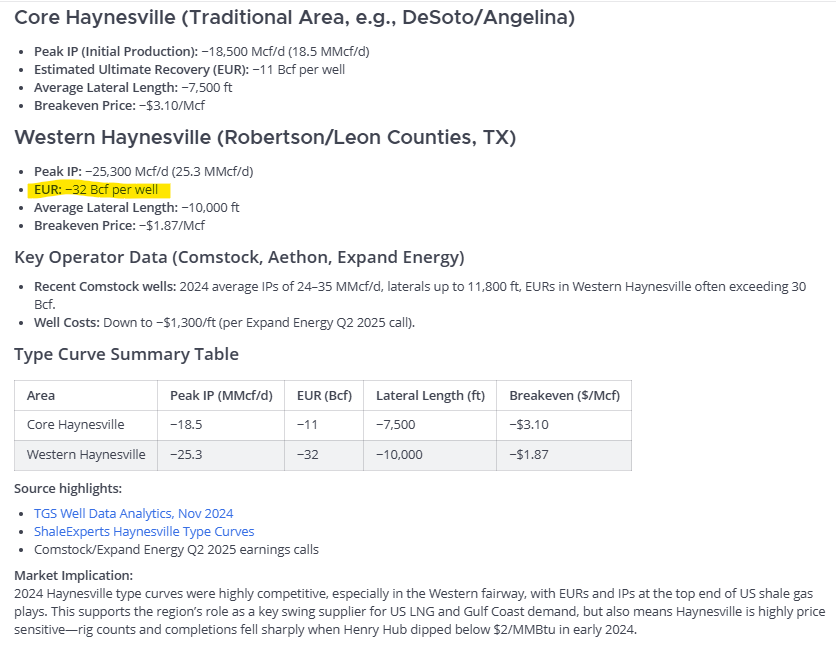

Taking the reported breakeven price estimate, and perusing through individual well data via TXRRC on Waynesville performance to date. I'm can't math these wells to average 32 BCF EUR, not even close. How are these analysts coming up with this??

Golden Pass LNG hits major milestone: first cool-down cargo arrived Dec 2025. 3 trains (total 2.4 Bcf/d) ramping up through early 2027. Bullish for US gas—feedgas demand rising, tightening Gulf Coast basis. Initial exports likely to Europe, shifting to Asia as demand rebounds.

https://t.co/DBYK28RANY

#LNG #ONGT #Natgas #energy #JKM #TTF